united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

| Investment Company Act file number | 811-08228 | |

The Timothy Plan

(Exact name of registrant as specified in charter)

1055 Maitland Center Commons, Maitland, FL 32751

(Address of principal executive offices) (Zip code)

Art Ally, The Timothy Plan

1055 Maitland Center Commons, Maitland, FL 32751

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-846-7526

Date of fiscal year end: 9/30

Date of reporting period: 9/30/23

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Registrant’s audited annual financial reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 are as follows:

ANNUAL REPORT

September 30, 2023

TIMOTHY PLAN FAMILY OF FUNDS

Table of Contents

| | |

Section 1 | Shareholder Letters | 2 |

Section 2 | Fund Performance | 22 |

Section 3 | Schedule of Investments | 34 |

Section 4 | Statements of Assets and Liabilities | 78 |

Section 5 | Statements of Operations | 84 |

Section 6 | Statements of Changes in Net Assets | 88 |

Section 7 | Financial Highlights | 94 |

Section 8 | Notes to Financial Statements | 130 |

Section 9 | Opinion Letter | 154 |

Section 10 | Expense Examples | 155 |

Section 11 | Officers & Trustees | 162 |

Section 12 | Privacy Notice | 169 |

ANNUAL REPORT | 1

September 30, 2023

Dear Shareholder,

This report covers our fiscal year ending September 30, 2023. As you review the details of our funds and their respective performance on the following pages, including remarks by our various sub-advisors who serve as the money managers for the specific funds under their purview, you will see that this fiscal year has rebounded very well vs. last fiscal year’s negative performance. The equities market was led by technology stocks, with growth outperforming value and interest-rate sensitive sectors being the worst performing. Our performance (10-1-22 thru 9-30-23) was positive among nearly all market segments, with the exceptions of Growth & Income (down 5.02% for Class A), Fixed Income (down 5.02% for Class A) and Israel Common Values (down 15.44% for Class A). On an absolute return basis, six of our funds were up between 10.41% and 19.18%, three were up between 4.46% and 8.48% and two of the three mentioned above were down less than 1%.

For more complete details and information about the individual funds, please read each of the sub-advisor’s annual review letters in the pages that follow. They more fully detail the various factors that impacted this fiscal year’s performance along with their economic outlook for the coming year. All of that simply underscores the wisdom of asset allocation since different market segments perform differently over differing periods.

Timothy Partners, Ltd, (the “Advisor”) has always attempted to take a conservative approach to the markets as we believe our shareholders prefer a preservation of principal course to that of chasing returns. I do need to reiterate, however, that, in the capital markets in general and our funds in particular, returns can never be guaranteed.

Although we cannot guarantee any actual outcome, I remain confident that all our sub- advisors are, in our opinion, among the best in the industry and they each continue to honor our overall policy to manage their respective funds both in accordance with our screening restrictions and with a continued conservative bias.

Finally, I would once again like to thank you for your moral convictions that led you to becoming part of the Timothy Plan Family.

Yours in Christ,

Arthur D. Ally

President

ANNUAL REPORT | 2

Timothy Plan Aggressive Growth Fund Letter from the Manager – September 30, 2023 |  |

The stock market bottomed last October and proceeded to stage a remarkable recovery over the 12-month period ending 9/30/23, with the Russell Midcap Growth up 17.5%. This is in stark contrast to the prior 12 months where the Russell Midcap Growth index was down 29.5%. In that period, inflation was accelerating, the Fed was early in their rate-raising campaign, we had two down quarters of GDP, and the Russia/Ukraine war had just started. The rally in the past year was largely due to the directional improvement in inflation (Core Sept CPI down to +4.1% year-over-year), though still not close to the Fed’s target of 2% -- and along with this, the expectation that the Fed is either at or close-to the end of their rate tightening. Additionally, the economy has held up much stronger than many had expected it to after 500 basis-points of increases in the Fed Funds rate. In fact, earlier this year, a 2024 recession had been many economists’ “base case,” but now, as reported by the Wall Street Journal, the odds are seen as less than 50% (for a recession in the next 12 months). As of this writing, however, in addition to the Russia/Ukraine war showing no promise of resolution, the Israel/Hamas conflict has begun and has a high risk of contagion/acceleration. And on the domestic political front, not only are we facing a possible government shutdown in November, but we are soon going to be upon another presidential election cycle that is likely to be a “heated” one. All this is to say that the upcoming 12-months could see higher market volatility than we have had recently.

The Fund’s gross return was +17.8%, as compared to the benchmark Russell Midcap Growth’s rise of 17.5%. Analyzing the sector returns, the Industrials sector performed very well due to excellent stock selection and a modest overweighting. We also generated good relative outperformance in the Information Tech sector. Conversely, the Materials sector had the worst performance due to subpar stock selection.

For the portfolio, there has been no change to our time-tested, bottom-up fundamental approach to managing mid-cap growth investments. As an overview, the Fund remains well diversified by issuers and sectors, as all areas of the economy are impacted by broad macroeconomic trends. We are currently underweight in the Consumer Discretionary sector and overweight in the Energy and Industrials sectors. We remain focused on generating alpha and producing the strongest investment results over the long run. We thank you for your continuing support and investment.

Chartwell Investment Partners, LLC

ANNUAL REPORT | 3

The Timothy Plan International Fund

Letter from The Manager - September 30, 2023

Equity markets were strong in this twelve-month period rebounding from the prior period when central banks raised interest rates aggressively and worries spiked over the potential for a recession. International equities rallied as inflation fell across the globe and as optimism rose that central bank rate hikes would not tilt the global economy into a severe recession. Markets focused on this soft-landing scenario and equities followed suit. The Fund had a strong positive absolute move over the last twelve months and a similar performance to the MSCI AC World ex. US index on a relative basis.

Sector allocation was a big positive for this period while stock selection was slightly negative. An overweight to a strong performing Industrials sector led sector allocation in addition to underweights to underperforming Real Estate and Communication Services sectors. On the stock selection front, positive selection in Materials and Utilities led the way while negative selection in Consumer Discretionary, Health Care, and Technology sectors was a headwind for the portfolio. From a country standpoint, the largest detractors were stock selection in Japan and underweight allocation to Denmark. Positive country selection in France and Canada and an underweight to China and an overweight to Ireland all helped performance. Key positive stock attributors for the period included construction materials company CRH (Materials-Ireland), airplane engine manufacturer Safran SA (Industrials-France), and electrical equipment company Schneider Electric SE (Industrials-France). Negative attributors for the period were led by not owning screened out diabetes and obesity drug company Novo Nordisk as well as owning underperforming health care equipment manufacturer Olympus Corp (Health Care-Japan), and power tools leader Techtronic Industries (Industrial-Hong Kong).

Other key areas of interest during the fiscal year included the US Dollar and Japan. While the US Dollar appeared to have peaked early in the period and began to depreciate, helping international equity returns, it soon reversed course and recovered some of its lost ground in the 2nd half of the fiscal year, creating a headwind to international equity returns. Japan was also a strong focus in this period as calls for better corporate governance by the Tokyo Stock Exchange to Japanese corporates was heard loud and clear and companies began to make adjustments which gave hope to global investors of better shareholder treatment from Japanese corporates going forward.

Global interest rates have risen significantly over the last twelve months and there are concerns their lagged effect will impact economic growth negatively which could influence markets. International equity valuations are attractive not only compared to their own history but also compared to the US. We remain committed to a disciplined and consistent investment approach dedicated to finding long-term investments for shareholders and we thank you for your continued investment in the Fund.

Eagle Global Advisors, LLC

ANNUAL REPORT | 4

Timothy Plan Large/Mid Cap Growth Fund Letter from the Manager – September 30, 2023 | |

The stock market bottomed last October and proceeded to stage a remarkable recovery over the 12-month period ending 9/30/23, with the S&P500 gaining 21.6% and the Russell 1000 Growth up 27.7%. This is in stark contrast to the prior 12 months (S&P500 and R1G down 15.5% and 22.6%, respectively). In that period, inflation was accelerating, the Fed was early in their rate-raising campaign, we had two down quarters of GDP, and the Russia/Ukraine war had just started. The rally in the past year was largely due to the directional improvement in inflation (Core Sept CPI down to +4.1% year-over-year), though still not close to the Fed’s target of 2% -- and along with this, the expectation that the Fed is either at or close-to the end of their rate tightening. Additionally, the economy has held up much stronger than many had expected it to after 500 basis- points of increases in the Fed Funds rate. In fact, earlier this year, a 2024 recession had been many economists’ “base case,” but now, as reported by the Wall Street Journal, the odds are seen as less than 50% (for a recession in the next 12 months). As of this writing, however, in addition to the Russia/Ukraine war showing no promise of resolution, the Israel/Hamas conflict has begun and has a high risk of contagion/acceleration. And on the domestic political front, we are not only facing a possible government shutdown in November, but we are soon going to be upon another presidential election cycle that is likely to be a “heated” one. All this is to say that the upcoming 12-months could see higher market volatility than we have had recently.

After 2 years of the Russell 1000 Value outperforming its Growth counterpart, the R1G made a comeback and outperformed by over 13 percentage points over the last year (up 27.7% vs. +14.4% for the R1V). This scenario usually presents a challenge for the Fund’s relative performance, as we are restricted from owning most of the large growth stocks in the benchmark index. Size was an even larger differentiator: the Russell Top 200 stocks gained 23.9%, while the small-cap Russell 2000 only rose by 8.9%. This, too, is a headwind for the Fund, as the restrictions on many large-cap stocks create a significant lower-cap “skew” for the fund. With these challenges, we were pleased to have an upside capture (ratio of the Fund gross return to the R1G) of 86%. A related aside: Strategas Research just published a report showing that the “Magnificent Seven*” now accounts for nearly 50% of the market cap of the R1G, up from 29% five years ago and 12% ten years ago.

The Fund’s gross return was +19.0%, as compared to the benchmark Russell 1000 Growth’s rise of 27.7%. Sector allocation had an inordinate impact on relative performance; underweights in Technology and Communication Services, combined with an overweight in Materials, accounted for much of the allocation shortfall. Cash averaging 6% was also a detractor in a strong up market. Stock selection, though overall about neutral, was very additive in the Tech sector, with the Fund holdings returning 51% vs. the benchmark sector +43%. Additionally, the Industrials sector served the Fund well; our holdings gained 44%, well ahead of the R1G sector rise of 22.0%. On the downside, the fund holdings in the Financial sector, down 7.9%, markedly well short of the benchmark’s gain of 24.5%.

For the portfolio, there has been no change to our time-tested, bottom-up fundamental approach to managing large and mid-cap growth investments. As an overview, the Fund remains well diversified by issuers and sectors, as all areas of the economy are impacted by broad macroeconomic trends. We are currently underweight in the Tech sector by 5-6 percentage points and overweight in Industrials and Materials. We are looking at the Healthcare sector closely after some rather large hits have been taken by stocks thought to be negatively impacted by the success of the “GLP-1” (diabetes/obesity) drugs. For the first time in quite a while, we are neutral to slightly underweight in the sector, having been overweight previously. Some strategists, (RBC, to name one) believe that large-cap growth stocks are “over-owned and overvalued,” particularly the Magnificent Seven. If this gets corrected in the coming months by their underperformance, that will bode well for outperformance by the Fund.

Chartwell Investment Partners, LLC

*the Magnificent Seven: Apple, Microsoft, Alphabet (Google), Amazon, NVIDIA, Meta, Tesla

ANNUAL REPORT | 5

LETTER FROM THE MANAGER

September 30, 2023

TIMOTHY PLAN SMALL CAP VALUE FUND

We are pleased to provide you with our report on the Timothy Plan Small Cap Value Fund for the twelve months ending September 30, 2023, and would like to thank you for entrusting your assets with us.

Market Overview

Despite the best efforts of the Federal Reserve, the economy continued to chug along, and the U.S. stock market responded in kind, rising by more than 20% for the twelve months ended September 30, 2023. The S&P 500 Index gained 21.62% for the period, eclipsing the index’s long-term average. Small-cap stocks, as measured by the Russell 2000 Index, trailed the broad market, gaining 8.93%.

The biggest story in the year was the Federal Reserve, which began to raise interest rates in March 2022 and has increased its benchmark federal funds rate by 525 basis points over the past 18 months. The inflation rate, measured by the Consumer Price Index (CPI), peaked in June 2022, and has trended downward since. However, Fed chair Jerome Powell has reiterated the Fed’s 2% inflation target and has hinted that rates would remain high until the inflation monster has been slain.

The equity market was led by technology stocks, as the sector gained 41.1% in the last twelve months, driven primarily by companies involved in artificial intelligence, as semiconductor companies were among the primary beneficiaries. Interest-rate sensitive sectors Utilities and Real Estate were the worst performing sectors for the year, declining as the Federal Reserve accelerated its rate hike campaign.

The bond market didn’t fare as well, beset by rising interest rates and deteriorating credit conditions. The Bloomberg U.S. Aggregate, a broad bond market measure, gained 0.64% for the year; the index was led by corporate credits (the Bloomberg U.S. Credit added 3.47%), while government bonds were the lagging sector, as the Bloomberg U.S. Government declined 0.74%. During the year, the Treasury yield curve became significantly inverted, only to flatten out in September. The ten-year treasury rose from 3.83% to 4.57%, gaining 74 basis points, nearly all of that gain in the third quarter, in large part due to the Federal Reserve’s messaging of “higher for longer.”

Fund Performance

For the twelve months ending September 30, 2023, the Timothy Plan Small Cap Value Fund produced a return of 15.78%, compared to the benchmark Russell 2000 Index, which gained 8.93%.

On an absolute basis, only two sectors provided a negative total return: Utilities and Financials. In the case of Utilities, the sector struggled as interest rates rose; Financials were in much the same boat, though higher interest rates had a greater impact on balance sheets, as some smaller banks were required to mark to market certain long-dated Treasury bonds, causing a liquidity crisis as long bond prices fell. The top performing sectors in the fund included Industrials and Communications Services, both adding more than 50%, while Energy and Consumer Staples were also strong gainers.

From a relative perspective, performance was driven largely by stock selection, as two sectors – Industrials and Health Care – drove most of the gains for the year. Selection in Communication Services was also a positive factor returns, driven primarily by one company. Asset allocation was a factor in Health Care, where we were underweight the worst-performing sector in the index, and in Financials, where we were overweight the second worst-performing sector.

Net returns are net of the sub-adviser’s fees, not the mutual fund fees.

Past performance is not indicative of future results. Portfolio returns reflect the reinvestment of dividend and interest income. All information provided is for informational purposes only and is not intended to be, and should not be interpreted as, an offer, solicitation, or recommendation to buy or sell or otherwise invest in any of the securities/sectors/countries that may be mentioned. A description of the methodology used to calculate the attribution analysis or a complete list of each holding’s contribution to overall performance during the measurement period may be obtained by contacting info@westwoodgroup.com. Benchmark Data Source: © 2022 FactSet Research Systems Inc. All Rights Reserved. Russell Investment Group is the owner of the trademarks, service marks, and copyrights related to its indexes, which have been licensed for use by Westwood.

ANNUAL REPORT | 6

A diverse group of companies were the top contributors for the trailing twelve months. There were two “graduates” from the portfolio, stocks which exceeded our market cap range or were purchased by a bigger company, in our top five. Rambus (RMBS), a semiconductor designer and manufacturer, gained more than 75% while we held it, growing to a bigger company than our market cap limitations allow. Hostess Brands Inc. (TWNK), the snack food maker, was a focus of takeover speculation for most of the year, and the company finally agreed to be purchased by J.M. Smucker Co. in August. The purchase price was a 30% premium, and we sold the position on the news.

Other top contributors included Boise Cascade Co. (BCC), which advanced on strong demand and firm pricing for lumber and engineered wood products, and Northern Oil & Gas Inc. (NOG), gaining on higher prices for oil and natural gas. Rounding out the top five was Comfort Systems USA, Inc. (FIX), a Houston-based HVAC installation and repair company, advancing on strong growth opportunities.

The Financials sector was a detractor in the year, and three of the top five detractors were banks: Veritex Holdings (VBTX), Sandy Spring Bancorp (SASR), and First Bancorp (FBNC). Regional bank stocks suffered after the shuttering of Signature Bank (not owned) and Silicon Valley Bank (not owned) in March, largely due to liquidity issues as interest rates rose and the value of the banks’ long-dated bond holdings declined. Other detractors included Monro, Inc. (MNRO), one of several companies in the auto services industry seeing declines as sales and earnings have slowed due to a pullback by consumers and sharply higher oil and gas prices.

Industrial chemical supplier Stepan Co. (SCL) was a detractor after poor earnings reports led to declines in the second and third quarters.

Market Outlook

Current market conditions continue to produce dislocations with respect to valuation and increased levels of fundamental skepticism that we believe play to our strengths. Our emphasis on bottom-up fundamental analysis in both equity and credit markets helps us see beyond headlines and understand how businesses can perform over the long term.

In the U.S. equity markets, we see a very modest improvement to S&P 500 earnings in 2024, but the fourth quarter may prove to be more challenging in terms of overall earnings growth. We believe that the consensus (year-over- year) earnings growth estimates of 7.8% for the fourth quarter may be slightly optimistic as the actual effects of the Fed’s extended prohibitive rate prescription and subsequent economy-slowing actions are realized.

The macro environment remains challenging and warrants caution. We are carefully monitoring our holdings and actively managing risk in the portfolio. While we believe the portfolio is positioned appropriately, striking a good balance between upside and potential downside as we navigate this period of elevated uncertainty, the upcoming earnings season will likely be choppy – misses will likely be punished, as investors will look to sell first and ask questions later. On the other hand, companies that perform well, meeting or exceeding expectations, will likely be rewarded – and we believe the companies exhibiting the quality factors we seek are likely to lead in a difficult market.

Nevertheless, we continue to focus on investing at the intersection of quality and value. The portfolio’s superior quality profile relative to the benchmark is underappreciated and the reward/risk for the portfolio continues to look very attractive. We especially like our Industrials and Energy holdings, although we worry about our underweight in the latter and are actively evaluating new ideas to add to the portfolio.

We thank you for your continued confidence in the Westwood process and investment teams and we look forward to serving your investment needs through the years ahead.

Westwood Management Corp.

Net returns are net of the sub-adviser’s fees, not the mutual fund fees.

Past performance is not indicative of future results. Portfolio returns reflect the reinvestment of dividend and interest income. All information provided is for informational purposes only and is not intended to be, and should not be interpreted as, an offer, solicitation, or recommendation to buy or sell or otherwise invest in any of the securities/sectors/countries that may be mentioned. A description of the methodology used to calculate the attribution analysis or a complete list of each holding’s contribution to overall performance during the measurement period may be obtained by contacting info@westwoodgroup.com. Benchmark Data Source: © 2022 FactSet Research Systems Inc. All Rights Reserved. Russell Investment Group is the owner of the trademarks, service marks, and copyrights related to its indexes, which have been licensed for use by Westwood.

ANNUAL REPORT | 7

LETTER FROM THE MANAGER

September 30, 2023

TIMOTHY PLAN LARGE/MID CAP VALUE FUND

We are pleased to provide you with our report on the Timothy Plan Large/Mid Cap Value Fund for the twelve months ending September 30, 2023, and would like to thank you for entrusting your assets with us.

Market Overview

Despite the best efforts of the Federal Reserve, the economy continued to chug along, and the U.S. stock market responded in kind, rising by more than 20% for the twelve months ended September 30, 2023. The S&P 500 Index gained 21.62% for the period, eclipsing the index’s long-term average.

The biggest story in the year was the Federal Reserve, which began to raise interest rates in March 2022 and has increased its benchmark federal funds rate by 525 basis points over the past 18 months. The inflation rate, measured by the Consumer Price Index (CPI), peaked in June 2022, and has trended downward since. However, Fed chair Jerome Powell has reiterated the Fed’s 2% inflation target and has hinted that rates would remain high until the inflation monster has been slain.

The equity market was led by technology stocks, as the sector gained 41.1% over the last twelve months, driven primarily by companies involved in artificial intelligence, as semiconductor companies were among the primary beneficiaries. Interest-rate sensitive sectors Utilities and Real Estate were the worst performing sectors for the year, declining as the Federal Reserve accelerated its rate hike campaign.

The bond market didn’t fare as well, beset by rising interest rates and deteriorating credit conditions. The Bloomberg U.S. Aggregate, a broad bond market measure, gained 0.64% for the year; the index was led by corporate credits (the Bloomberg U.S. Credit added 3.47%), while government bonds were the lagging sector, as the Bloomberg U.S. Government declined 0.74%. During the year, the Treasury yield curve became significantly inverted, only to flatten out in September. The ten-year treasury rose from 3.83% to 4.57%, gaining 74 basis points, nearly all of that gain in the third quarter, in large part due to the Federal Reserve’s messaging of “higher for longer.”

Fund Performance

For the twelve months ending September 30, 2023, the Timothy Plan Large/Mid Cap Value Fund produced a return of 14.21%, compared to the S&P 500® Index which gained 21.62%. It's important to note that for the last twelve months, large-cap growth stocks (measured by the Russell 1000 Growth Index) gained 27.72%, compared to just 14.44% for large-cap value stocks (measured by the Russell 1000 Value Index). This discrepancy was driven in large part by the so-called “Magnificent Seven,” seven growth stocks that most value managers do not hold.

For the year, our top-performing sector was Information Technology, followed by Energy and Consumer Discretionary. We benefitted from one of the Magnificent Seven – NVIDIA (NVDA), which accounted for about a third of the return in the sector. Energy was driven by higher oil and natural gas prices throughout the period, while our Consumer Discretionary holdings were companies with strong fundamentals.

From a relative perspective, stock selection was the primary cause of our underperformance versus the index. One of the sectors detracting from relative performance was Communication Services, where two of the Magnificent Seven (Google and Meta) helped drive returns; these are growth-oriented names that we don’t hold in this

Net returns are net of the sub-adviser’s fees, not the mutual fund fees.

Past performance is not indicative of future results. Portfolio returns reflect the reinvestment of dividend and interest income. All information provided is for informational purposes only and is not intended to be, and should not be interpreted as, an offer, solicitation, or recommendation to buy or sell or otherwise invest in any of the securities/sectors/countries that may be mentioned. A description of the methodology used to calculate the attribution analysis or a complete list of each holding’s contribution to overall performance during the measurement period may be obtained by contacting info@westwoodgroup.com. Benchmark Data Source: © 2022 FactSet Research Systems Inc. All Rights Reserved. Russell Investment Group is the owner of the trademarks, service marks, and copyrights related to its indexes, which have been licensed for use by Westwood.

ANNUAL REPORT | 8

portfolio. On the other hand, stock selection was beneficial in the Information Technology sector, where we held NVIDIA as our top performer. Our underweight in the health care sector was positive overall, while the underweight in the Communication Services sector was a drawback.

Four of the top five performers in the calendar year are linked to the technology sector. NVIDIA Corp (NVDA) was one of the top performers in the stock market for the year, gaining over 250% as the chip maker’s applications for artificial intelligence (AI) became known and appreciated. Broadcom (AVGO) was another strong performer, as the semiconductor manufacturer showed upside potential for their AI-related business. Lattice Semiconductor (LSCC) and ASML Holding NV (ASML) also soared in the year, in a similar fashion both companies make chips that help make artificial intelligence possible. The lone top performer that was not in technology was Eaton Corp (ETN), an industrial company that builds electrification solutions for data centers and other facilities – data centers, of course, are also tied to the boom around artificial intelligence.

Detracting from performance were a couple of regional banks, hard-hit due to liquidity issues in the industry. Western Alliance Bancorp (WAL) and Cullen/Frost Bankers Inc. (CFD). Both were sold from the portfolio amid concerns about higher interest rates. Crown Castle Inc. (CCI) is a real estate company that manages land for wireless towers; the stock came under pressure as Real Estate declined amid higher interest rates. Cable One Inc. (CABO) fell by about 20% on declining demand for the company’s set-top box business. Last, Dollar General (DG) was the top detractor, as the company faced pressure from increasing wages and poor sales execution.

Market Outlook

Current market conditions continue to produce dislocations with respect to valuation and increased levels of fundamental skepticism that we believe play to our strengths. Our emphasis on bottom-up fundamental analysis in both equity and credit markets helps us see beyond headlines and understand how businesses can perform over the long term.

In the U.S. equity markets, we see a very modest improvement to S&P 500 earnings in 2024, but the fourth quarter may prove to be more challenging in terms of overall earnings growth. We believe that the consensus (year-over- year) earnings growth estimates of 7.8% for the fourth quarter may be slightly optimistic as the actual effects of the Fed’s extended prohibitive rate prescription and subsequent economy-slowing actions are realized.

We expect earnings estimates to continue to fall for the current and future quarters as the fourth quarter earnings season begins. That being said, there are still many areas of growth, but stock selection will be critical. As earnings growth becomes less stable, quality characteristics, which are a key attribute of our process, are likely to be an important driver of excess returns.

We will continue to focus on the intersection of quality and value, seeking select businesses trading at an attractive valuation. These basic rules form a strong investment foundation that applies across the market capitalization spectrum. We’ve found our approach to be especially effective in uncertain economic environments like we see today. With higher interest rates increasing the cost of capital, we believe high-caliber, high-demand businesses that have sustainable competitive advantages, strong cash flows, attractive dividends and a history of execution, tend to perform better and can limit downside risk.

We thank you for your continued confidence in the Westwood process and investment teams and we look forward to serving your investment needs through the years ahead.

Westwood Management Corp.

Net returns are net of the sub-adviser’s fees, not the mutual fund fees.

Past performance is not indicative of future results. Portfolio returns reflect the reinvestment of dividend and interest income. All information provided is for informational purposes only and is not intended to be, and should not be interpreted as, an offer, solicitation, or recommendation to buy or sell or otherwise invest in any of the securities/sectors/countries that may be mentioned. A description of the methodology used to calculate the attribution analysis or a complete list of each holding’s contribution to overall performance during the measurement period may be obtained by contacting info@westwoodgroup.com. Benchmark Data Source: © 2022 FactSet Research Systems Inc. All Rights Reserved. Russell Investment Group is the owner of the trademarks, service marks, and copyrights related to its indexes, which have been licensed for use by Westwood.

ANNUAL REPORT | 9

Letter from the Manager

September 30, 2023

Timothy Plan Fixed Income Fund

The fiscal year ending September 30, 2023 witnessed extreme volatility in U.S. Treasury (UST) yields as the Federal Reserve (Fed) remained hawkish in response to persistent inflation, continued strength in employment and concerns over the economic effects of U.S. bank failures. The Timothy Plan Fixed Income Fund invests in the broad U.S. investment grade bond market benchmarked to the Bloomberg Aggregate Index which began the last 12 months with a yield-to-worst of 4.63% and ended at 5.39%.

After raising the Fed Funds rate by 150 basis points (bps), between October 2022 and February 2023, the Fed took a step back and lowered the level of the rate hike at its March meeting. Prior to the failure of Silicon Valley Bank, the Fed Funds Futures market had predicted a 50bp increase at the March Fed meeting. Instead, the Fed complied with the market’s reduced forecast of a 25bps hike. By the end of 1Q23, only one more 25bp hike was priced in by Fed Funds Futures, but with nearly 75bps of cuts predicted to follow by the end of 2023.

The Fed was torn between ensuring financial stability amid an ongoing bank crisis and achieving their goal of reducing inflation to their long-term target of 2.0%. Core-PCE (the Fed’s preferred measure of inflation) had fallen to a 4.6% y/y rate by February, only an 80bp reduction from the peak-rate of one-year prior. The Fed continued to look to the U.S. labor market for confirmation that its aggressive rate increases over the past twelve months had some effect in slowing the economy and inflation. The labor market continued to defy the Fed’s hopes with unemployment falling to a 54-year low of 3.4% in January, and only climbing to 3.5% by March.

The Fed paused its rate hike cycle in June after 10-consecutive meetings with a hike. Inflation remained stubbornly high through much of 2Q23 although the June Consumer Price Index (CPI) rose at a lower than forecast 3.0% y/y rate. The debt ceiling debate, strong economic data, and hawkish Fed rhetoric sparked a sell-off in USTs during 2Q23. The 10-year UST yield started the fiscal period at 3.83%, fell to a low of 3.31% in early April, but ended September higher at 4.57%. By comparison, the 2-year rate started the period at 4.28%, dropped to 3.84% on March 23rd only to close the last 12 months higher at 5.05%.

Investment Grade (IG) Credit spreads started the last 12 months at 147bps and ended at 112bps by September 2023. At the beginning of 4Q22, IG Credit offered a yield-to-maturity of 5.57% and at the end of the fiscal period it was 5.95%. A key driver of the YTD credit spread tightening has been resilient profits and management teams restraining themselves from boosting shareholder payouts. In addition, higher yields have begun to attract inflows into IG Credit. IG balance sheets are, in most cases, well prepared for an economic slowdown. However, technicals can overwhelm fundamentals in a market downturn as well. The Fed’s 550bps

ANNUAL REPORT | 10

of rate hikes have tightened financial conditions, but so far, this is only noticeable in the level of spreads in the Bank sector. Industrials trade inside of their long-term average, so a recession could see them underperform Banks and Utilities. The rating agencies have become more cautious in recent months, increasing the number of issuers with negative outlooks to a higher number than those with positive outlooks. However, low-BBB Corporates still have a net positive outlook at the ratings agencies, reflecting the continued strength of their balance sheets and conservative management teams.

Mortgage-backed securities (MBS) underperformed IG Credit during the fiscal year ending September. Over the 12-month period, the MBS sector, within the Bloomberg Aggregate, generated a return of -0.17% versus 3.47% for IG Credit. During 4Q21, issuance declined 44% q/q which was driven by higher mortgage rates. The 30-year fixed mortgage rate ended 2022 at 6.76% and climbed further to reach a rate of 7.50% by the end of September 2023. Purchase activity also collapsed as the vast majority of the 72% of borrowers with a mortgage rate of 4.00% or less are unwilling to assume the punitive increase in monthly payments that would come with moving to a new home. The 2023 year-to-date new issuance total of $172B represented a 63% decline versus the same period from 2022.

According to Morningstar, the Timothy Fixed Income Fund A shares returned -0.55% over the 12-month period ending September 30, 2023 which was behind the Bloomberg Aggregate Index at 0.64%. The overweight allocation to Mortgages detracted from relative performance as the sector generated nominal returns below IG Credit bonds and the overall index. In addition, an underweight in Financials negatively impacted performance as they posted the highest nominal returns of any other sector. Helping performance was an overweight to Utilities which outperformed the overall index during the period. Lastly, a lower duration stance for most of the last 12-months also contributed to performance. We remain focused on generating income consistent with a prudent level of risk.

ANNUAL REPORT | 11

Letter from the Manager

September 30, 2023

Timothy Plan High Yield Fund

During the fiscal year ending September 30, 2023, Ba/B High Yield (HY) spreads started at 464 basis points (bps), fell to a low of 296bps by the end of July, and finished the period at 325bps. The Timothy Plan High Yield Fund invests primarily in BB and B rated HY bonds benchmarked to the Bloomberg US HY Ba/B 3% Issuer Cap Index. The benchmark began the last 12 months with a yield-to-worst (YTW) of 8.80% and ended lower at 8.25%. Over the period, the HY market posted a return of 9.79% which was better than the return of investment grade credit bonds of 3.47%.

Despite the Federal Reserve’s continued rate hikes, coming into 2023, and their Quantitative Tightening program, the HY market remained resilient. The Bloomberg US HY Ba/B 3% Issuer Cap Index posted positive returns in each of the four quarters during the fiscal period. The HY market’s continued increase in quality (BBs making up a higher percentage) and higher mix of secured bonds in the Index are factors that have led to the resilience of the sector. The price stratification is sizable within the HY market, highlighting why, going forward, credit selection will be an even more important component of future returns.

According to Morningstar, the Timothy High Yield Fund A shares generated a total return of 10.00% over the 12-month period ending September 30, 2023 while the Bloomberg US HY Ba/B 3% Issuer Cap index returned 9.79%. An overweight to Financials contributed to performance as the sector generated the highest nominal and excess returns in the index. In addition, an underweight to Utilities helped relative performance as this sector posted returns below the overall index. An underweight in Cyclical Services detracted from performance as the subsector performed better than the index. Lastly, an overweight to REIT holdings negatively impacted performance as the category’s performance trailed the index. The portfolio remains focused on generating a higher level of carry income consistent with a reasonable level of risk.

ANNUAL REPORT | 12

September 30, 2023

Dear Shareholder,

The Defensive Strategies Fund was designed and is managed to do what its name implies, hedge against a possible scenario of hyper-inflation which could result from our Congress’s proven unwillingness to address our core problems of too much spending and too much debt. The Fund was also designed with built-in flexibility that allows it to be adjusted to address a possible risk of extreme deflation, with the ability to convert the inflation sensitive assets to cash and fixed income securities during a deflationary environment, and to be adjusted to a more normal, traditional investment strategy.

The Fund’s portfolio is primarily comprised of several inflation sensitive investment sleeves: commodities (commodity company stocks and ETF’s), real estate (in the form of REITs), precious metals (primarily gold bullion) and silver ETFs, TIPs (Treasury Inflation Protected Bonds), and our newer Market Neutral ETF with the balance in cash. Timothy Partners, Ltd. (the “Advisor”) is responsible for setting the percentages of the Fund that will be allocated to each investment sleeve. Different sub-advisors manage the holdings in each sleeve. This past year rewarded us with a nice recovery following the turbulent previous fiscal year, with the commodity sleeve performing very well, the REIT sleeve in the low-positive territory, and the metals peaking early but dropping during the year. As a result, this Fund experienced a positive 8.30% return for the fiscal year ended September 30, 2023. For a more complete description of the elements that impacted Fund performance and the outlook for the future, please read the various sub-advisors’ reports in the pages that follow.

I would like to point out that, since there does not exist an appropriate benchmark index with which to compare our performance, we have created a blended index comprised of roughly 33% each of U.S. Government TIPs, FTSE NAREIT Equity Index and Bloomberg Commodity Index. We believe the blend offers a fairly accurate reflection and comparison of the composition of the Fund. For the fiscal year ended September 30, 2023, the blended index had a return of 1.79%.

While no one can predict future events, I remain confident that our sub-advisors (i.e. money management firms that manage the various sleeves of this Fund) are, in our opinion, among the best in the industry, and they each continue to honor our overall policy that they manage their respective Fund sleeve both in accordance with our screening restrictions and with a conservative bias. As I stated in last year’s report, although we will do our very best to be successful, we cannot guarantee results in any of these scenarios.

Finally, I would once again like to thank you for your moral convictions that led you to become part of the Timothy Plan Family.

Yours in Christ,

Arthur D. Ally

Fund Advisor

ANNUAL REPORT | 13

Letter from the Manager

September 30, 2023

Timothy Plan Defensive Fund – Treasury Inflation Protected Securities (TIPS)

The Federal Reserve (Fed) raised the Fed Funds rate 125 basis points (bps) in 4Q22 to end the year at 4.50%. The hiking cycle was the most aggressive since the early-1980s and the inversion of the UST yield curve reached its most inverted measure since 1981. According to the Bureau of Labor Statistics, the Consumer Price Index for All Urban Consumers (CPI) accelerated 3.70% year-over-year (y/y) at the end of September 2023. The Timothy Defensive Fund has an allocation of U.S. Treasury Inflation Protected Securities (TIPS) designed to help protect assets from higher rates of inflation.

Coming into 2023, investors were pricing in four rate hikes in 2023 via the Fed Funds futures rate. However, by the end of 1Q23, futures were projecting only one more hike partly due to the second and third-largest bank failures in U.S. history. The March decline in UST yields reflected a reduction in the forecast for additional Fed rate hikes. Prior to the failure of Silicon Valley Bank, the Fed Funds Futures market had predicted a 50bp increase at the March Fed meeting. Instead, the Fed complied with the market’s reduced forecast of a 25bps hike. By the end of 1Q23, only one more 25bp hike was priced in by Fed Funds Futures, but with nearly 75bps of cuts predicted to follow by the end of 2023.

The Fed was torn between ensuring financial stability amid an ongoing bank crisis and achieving their goal of reducing inflation to their long-term target of 2.0%. Core-PCE (the Fed’s preferred measure of inflation) had fallen to a 4.6% y/y rate by February. The Fed continued to look to the U.S. labor market for confirmation that its rate increases over the prior twelve months had some effect in slowing the economy and inflation. The labor market continued to defy the Fed’s hopes with unemployment falling to a 54-year low of 3.4% in January, and only climbing to 3.5% by March.

The Federal Reserve (Fed) paused its rate hike cycle in June after 10-consecutive meetings with a hike. Inflation remained stubbornly high through much of 2Q23 although the June Consumer Price Index (CPI) rose at a lower than forecast 3.0% y/y rate. However, the pause was short lived as the Fed hiked rates by 25bps during 3Q23 which ended at 5.50% by the end of the fiscal period. Higher energy prices sparked fears of a re-acceleration in inflation, but TIPS implied inflation forecast was little changed in 3Q.

Over the previous 12-month period, investors’ future inflation expectations climbed modestly. We measure investors’ inflation expectations as the difference between the U.S. Treasury 10-year and the U.S. TIPS 10- year. This “breakeven rate” of inflation is what would be required to make these two securities have the same yield. The “breakeven rate” of inflation started the fiscal period at 2.24%, reached a 12-month high of 2.59% in November 2022 but subsequently declined to 2.31% by the end of September 2023. The Bloomberg U.S.

TIPS Index generated a 12-month return of 1.25% versus 2.22% for the Barrow Hanley TIPS portfolio. Relative to the Bloomberg U.S. TIPS Index, the portfolio ended the fiscal year-end period with an overweight to the 1 to 4.99-year maturity segment, underweight to the 5 to 9.99-year, and overweight to 20+ year securities. The primary goal of the TIPS allocation continues to be protection from rising inflation rates.

ANNUAL REPORT | 14

The Timothy Plan Defensive Strategies Fund

Real Estate Sleeve (the “Portfolio”)

Annual Manager Letter: 12 months ended September 30, 2023

In the year ending September 30, 2023, the MSCI US REIT Index (Bloomberg: RMZ) produced a total return of +3.2%. While the performance was positive, most of the developments in the economy over the past 12 months have had a negative impact on real estate. Most importantly, the Fed’s original projection for the February 2023 rate hike to be ‘one and done’ did not come true; instead, the resilient economy and continued high inflation reports forced the Fed to continue its unprecedented rate hike cycle, reaching a Fed Funds Rate of 5.25-5.50% as of September 30, 2023. While the majority of economist project that the Fed is ‘done’, there is still a chance for more hikes.

Furthermore, the strength of the economy has now lowered the chances of a recession in the near term, which also ‘took away’ several expected rate cuts for 2024, pushing up long term Treasury yields. As a result, the 10 year Treasury yield closed at 4.6% on September 30, 2023, the highest level since October 2007. The newfound ‘higher for longer’ mantra in the markets is rippling through all asset classes, as investors are speculating the level at which long term interest rates will stabilize. While the effects of higher rates are only just starting to be felt by private real estate investors and showing up in income statements, we believe that the downside to public REIT prices is somewhat limited as they have already sold off % from the 12/31/2021 high, as measured by the RMZ through September 30, 2023.

The portfolio performed inline with the benchmark over the year ending September 30, 2023. The Timothy Fund REIT Sleeve produced a total return of +3.1% in the relevant period, which compared to the RMZ total return of +3.2%. The top contributors to relative performance were underweight allocations to the office and triple net sectors, as well as stock selection in the healthcare sector. The top detractors from relative performance over the same period were underweight allocations to the regional mall and specialty sectors, as well as an overweight allocation to the cell tower sector. Notably, the portfolio’s secondary benchmark, Vanguard REIT ETF (NYSE: VNQ), which includes cell towers, produced a total return of -1.3% over the same period, well below the portfolio.

In the 2023 year to date period, the portfolio has outperformed the benchmark significantly, as the portfolio’s positioning for higher interest rates finally started to work. In particular, the underweight to triple net has been a large contributor. However, with the Fed getting close to the end of the rate hike cycle, we are beginning to position the portfolio for stable or declining interest rates. As such, we trimmed a data center REIT and added a triple net REIT in August. Going forward, we expect to continue to move the portfolio further to benefit from a ‘Fed pivot’. The bifurcation in performance between sectors and intra-sector has created a ripe environment for new ideas and, in particular, buying high quality businesses at a discount. We firmly believe active management will have a distinct opportunity to outperform passive in the near term using a repeatable process based on fundamental analysis and an emphasis on quality.

An investment cannot be made directly in an index. The information contained herein should be considered to be current only as of the date indicated, and we do not undertake any obligation to update the information contained herein in light of later circumstances or events. This publication may contain forward looking statements and projections that are based on the current beliefs and assumptions of Chilton Capital Management and on information currently available that we believe to be reasonable, however, such statements necessarily involve risks, uncertainties and assumptions, and prospective investors may not put undue reliance on any of these statements. This communication is provided for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any Chilton investment or any other security. Past performance does not guarantee future results.

ANNUAL REPORT | 15

The Timothy Plan Defensive Strategies Fund Commodity Sleeve (the “Portfolio”)

Annual Letter from the Manager (September 30, 2023)

We are pleased to provide you with our annual report for the Timothy Plan Defensive Strategies Fund Commodity Sleeve (the “Portfolio”) for the twelve months ending September 30, 2023. The Portfolio rose 20.1% on a gross basis, while the Bloomberg Commodity Index Total Return (the “BCOM”) declined (1.3%) during the twelve-month period. The Portfolio generated 21.4% of outperformance versus the BCOM benchmark with positive contributions from energy, agriculture, and industrial metals, while precious metals modestly detracted from relative performance.

Energy

Energy was the worst performing sector in the BCOM over the prior year, with the Bloomberg Energy Subindex Total Return falling (13.0%). In the Portfolio, however, energy holdings were the best performing sector: gaining 28.3% over the same period which made them the largest contributor to the Portfolio’s overall outperformance versus the BCOM benchmark. Crude oil prices rose over the period with a series of supply curtailments by OPEC+ coupled with rising global demand which has shifted the oil market expectation into a deficit estimated to be the largest imbalance in over a decade. U.S. natural gas prices declined significantly over the period as a result of limited heating demand due to a mild winter, rising U.S. production, muted Asian demand, and earlier-than-anticipated European gas storage fill levels. Upstream E&P companies along with integrated energy and oil service companies held in the Portfolio benefited the most from increasing oil prices and were responsible for the bulk of the outperformance from the sector. The Portfolio’s largest energy holdings as of September 30th were ConocoPhillips (COP US), TotalEnergies SE (TTE FP), and Schlumberger N.V. (SLB US).

Agriculture

Agricultural commodities rose by 1.1% as measured by the Bloomberg Commodity Agriculture and Livestock Subindex Total Return over the past year. During the same period, the Portfolio’s agricultural holdings appreciated 4.5%. Among the holdings, agricultural machinery and water companies were the two largest positive contributors, while fertilizer and pesticide companies dragged on performance within the sector alongside falling wheat and corn prices. After the extended Black Sea Grain Initiative eased supply concerns, wheat prices were further pressured by a bump in harvest from top global exporter Russia, while corn prices were weighed down due to improving growing conditions. The Portfolio’s largest agriculture holdings as of September 30th were Nutrien Ltd. (NTR US), Deere & Company (DE US), and CF Industries Holdings, Inc. (CF US).

Metals & Mining

Industrial metal commodity futures were up 5.6% for the period, as measured by the Bloomberg Industrial Metals Subindex Total Return. The Portfolio’s industrial metal holdings outperformed, rising 23.3% over the same period and contributing considerably to the Portfolio’s overall outperformance. The Portfolio’s exposure to steel – a commodity not included in the BCOM benchmark – was particularly beneficial as steel and steel-related companies, such as iron miners and metallurgical coal companies, appreciated approximately 55.0%, 17.4%, and 62.0% respectively. Additionally, copper companies rallied about 46.2% over the same period, as copper prices increased due to earlier disruptions to Latin America supply. The Portfolio’s largest industrial metal holdings as of September 30th were Rio Tinto PLC (RIO US), Vale S.A. (VALE US), and Teck Resources Ltd. (TECK/B CN).

Precious metals were the best performing sector in the BCOM, with a 12.5% gain posted by the Bloomberg Precious Metals Subindex Total Return for the twelve months ending September 30, 2023. The Portfolio’s precious metal miners were up 12.2%, modestly underperforming. The Portfolio’s largest precious metal holdings as of September 30th were B2Gold Corp. (BTG US), Gold Fields Ltd (GFI US), and Kinross Gold Corporation (KGC US).

ANNUAL REPORT | 16

Market Outlook

The Timothy Plan Defensive Strategy Fund Commodity Sleeve currently utilizes a diversified portfolio of natural resource equities that is intended to capture commodity price movements. We believe that increasing market volatility, driven by macroeconomic factors as well as geopolitical events, has led to a precarious supply situation following decades of underinvestment in the global supply of many important commodities. With projected strong demand for many commodities along with recent market tightness, we believe there is ample support for commodity prices. To the extent that geopolitical risk remains elevated, supply remains uncertain and global demand continues to grow, we expect the Portfolio to perform positively.

Past performance is not indicative of future results. STANDARD & POOR’S, and S&P are registered trademarks of Standard & Poor’s Financial Services LLC. “Bloomberg®,” “Bloomberg Commodity IndexSM” and the names of the other indexes and sub-indexes that are part of the Bloomberg Commodity Index family are service marks of Bloomberg Finance L.P. and its affiliates. Source for all Index data: Bloomberg L.P. Commodity Sectors are represented by the Bloomberg Commodity Sector Sub-Indices. This document does not constitute an offer of any commodities, securities or investment advisory services. Any such offer may be made only by means of a disclosure document or similar materials which contain a description of material terms and risks. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. The economic statistics presented herein are subject to revision by the agencies that issue them. This information is accurate only as of the date hereof, or as of historical dates otherwise indicated herein, and we do not undertake any obligation to update this material Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. All investments are subject to risk.

ANNUAL REPORT | 17

September 30, 2023

Dear Timothy Plan Strategic Growth and Conservative Growth Fund Shareholder:

This report covers the fiscal year (10-1-22 thru 9-30-23). Asset allocation has normally been, and we believe it continues to be, a very prudent approach to investing. As a review, your Timothy Plan investment is a compilation of many of Timothy’s underlying funds (including five of our ETF’s) and, as such, your performance is directly related to the performance of those underlying funds. I am pleased to report that this fiscal year produced positive performance following the recession fears of the previous year, with the equities market led by technology stocks, growth outperforming value and interest-rate sensitive sectors being the worst performing. As a result, performance in nearly all our underlying funds was positive for this past fiscal year which contributed to our 7.37% return for Strategic Growth and 4.79% return for Conservative Growth. You can find the specific details in the financial highlights of the main body of this report. Having said that, we intend to participate in this market while maintaining a more cautious outlook for the economy in the year ahead. As a result, we have adjusted our positions in the underlying funds to the allocations shown below:

| Conservative Growth | Strategic Growth |

| · Large/Mid-Cap Core Enhanced ETF 12.00 % | 12.00% | 15.00% |

| · High Dividend Stock Enhanced ETF | 6.00% | 8.00% |

| · Small-Cap Core ETF | 7.00% | 12.00% |

| · International ETF | 9.00% | 16.00% |

| · Market Neutral ETF | 15.00% | 15.00% |

| · International Fund | 11.50% | 13.00% |

| · High-Yield Bond Fund | 6.50% | 6.00% |

| · Fixed Income Fund | 30.00% | 12.00% |

| · Cash | 3.00% | 3.00% |

Even though the Portfolios have been designed to be conservatively allocated, we understand that recent market gyrations may be unsettling for some investors. Please understand that our #1 concern is preservation of principal, and, even though we do want to participate in the markets’ hoped for potential recovery, we will attempt to adjust our allocation above to changing market conditions.

As you know, no one can guarantee future performance. However, the one thing that I can assure you of is every one of our sub-advisors is doing their very best and our team here at Timothy is working very hard to provide you an investment in which you can feel comfortable.

Sincerely,

Arthur D. Ally

President

ANNUAL REPORT | 18

The Timothy Plan Israel Common Values Fund

Letter from The Manager - September 30, 2023

Israeli equity markets were unable to participate in the global market rebound during the fiscal year as continued interest rate hikes by the Bank of Israel were joined with an unanticipated election result that created a grey cloud over the markets. The Fund succumbed to this headwind and underperformed the benchmark TA-125 index for the fiscal year. Both sector allocation and stock selection contributed to the underperformance. From a sector standpoint, an underweight to outperforming Health Care and overweight to underperforming Consumer Discretionary hurt performance. Underweights to both Utilities and Real Estate were both positive as both sectors underperformed for the period. Stock selection was positive in Industrials and Consumer Staples but detrimental in Health Care and Communication Services. Key headwind for the year was not owning screened out Health Care company Teva Pharmaceutical. Notable positive attributors for the year included defense company Leonardo DRS (Industrials), Tel Aviv Stock Exchange (Financials), and semiconductor services company Nova Ltd (Technology). In addition to not owning Teva, negative attributors included electrical products firm Elco Ltd (Industrials) and HVAC and energy company Tadiran Group Ltd (Consumer Discretionary).

While the Bank of Israel aggressively raised interest rates during the last twelve months, the Israeli economy remains well underpinned and is on a strong footing. Debt/GDP is enviable at close to 60% while unemployment levels are low, and inflation is declining markedly. Interest rates have created a headwind for those sectors affected by these higher rates such as the important Real Estate sector. Housing has slowed while commercial real estate is also affected by rising funding costs.

A major headwind during the year was the late 2022 election which resulted in a coalition government which some call the most right-wing religious government coalition in Israel’s history. The unpopular reform agenda supported by this coalition, in particular the judicial reform, was not only unpopular with many Israelis but affected the markets negatively. Protests erupted throughout the country against some of the proposed laws hurting economic and market sentiment. A grey cloud remains over the country as this coalition continues to rule.

The Fund continues to invest alongside the innovate spirit of Israeli companies providing ample attractive investment opportunities. While global economic uncertainty and domestic political struggles are likely to continue in the near term, we are optimistic of the long-term prospects for this robust economic engine. We remain committed to a consistent investment approach dedicated to finding long-term investments for shareholders and we thank you for your continued investment in the Fund.

Eagle Global Advisors, LLC

ANNUAL REPORT | 19

Letter from the Manager

September 30, 2023

Timothy Growth and Income Fund – Fixed Income Allocation

The fiscal year ending September 30, 2023 witnessed extreme volatility in U.S. Treasury (UST) yields as the Federal Reserve (Fed) remained hawkish in response to persistent inflation, continued strength in employment and concerns over the economic effects of U.S. bank failures. The fixed income allocation of the Timothy Plan Growth & Income Fund invests in the broad U.S. investment grade bond market benchmarked to the Bloomberg Aggregate Index which began the last 12 months with a yield-to-worst of 4.63% and ended at 5.39%.

After raising the Fed Funds rate by 150 basis points (bps), between October 2022 and February 2023, the Fed took a step back and lowered the level of the rate hike at its March meeting. Prior to the failure of Silicon Valley Bank, the Fed Funds Futures market had predicted a 50bp increase at the March Fed meeting. Instead, the Fed complied with the market’s reduced forecast of a 25bps hike. By the end of 1Q, only one more 25bp hike was priced in by Fed Funds Futures, but with nearly 75bps of cuts predicted to follow by the end of 2023.

The Fed was torn between ensuring financial stability amid an ongoing bank crisis and achieving their goal of reducing inflation to their long-term target of 2.0%. Core-PCE (the Fed’s preferred measure of inflation) had fallen to a 4.6% y/y rate by February, only an 80bp reduction from the peak-rate of one-year ago. The Fed continued to look to the U.S. labor market for confirmation that its aggressive rate increases over the prior twelve months had some effect in slowing the economy and inflation. The labor market continued to defy the Fed’s hopes with unemployment falling to a 54-year low of 3.4% in January, and only climbing to 3.5% by March.

The Federal Reserve (Fed) paused its rate hike cycle in June after 10-consecutive meetings with a hike. Inflation remained stubbornly high through much of 2Q although the June Consumer Price Index (CPI) rose at a lower than forecast 3.0% y/y rate. The debt ceiling debate, strong economic data, and hawkish Fed rhetoric sparked a sell-off in USTs during 2Q23. The 10-year UST yield started the fiscal period at 3.83%, fell to a low of 3.31% in early April, but ended September higher at 4.57%. By comparison, the 2-year rate started the period at 4.28%, dropped to 3.84% on March 23rd only to close the last 12 months higher at 5.05%.

Investment Grade (IG) Credit spreads started the last 12 months at 147bps and ended at 112bps by September 2023. At the beginning of 4Q22, IG Credit offered a yield-to-maturity of 5.57% and at the end of September it was 5.95%. A key driver of the YTD credit spread tightening has been resilient profits and management teams restraining themselves from boosting shareholder payouts. In addition, higher yields have begun to attract inflows into IG Credit. IG balance sheets are, in most cases, well prepared for an economic

ANNUAL REPORT | 20

slowdown. However, technicals can overwhelm fundamentals in a market downturn as well. The Fed’s 550bps of rate hikes have tightened financial conditions, but so far, this is only noticeable in the level of spreads in the Bank sector. Industrials trade inside of their long-term average, so a recession could see them underperform Banks and Utilities. The rating agencies have become more cautious in recent months, increasing the number of issuers with negative outlooks to a higher number than those with positive outlooks. However, low-BBB Corporates still have a net positive outlook at the ratings agencies, reflecting the continued strength of their balance sheets and conservative management teams.

Mortgage-backed securities (MBS) under performed IG Credit during the fiscal year ending September. Over the 12-month period, the MBS sector, within the Bloomberg Aggregate, generated a return of -0.17% versus 3.47% for IG Credit. During 4Q21, issuance declined 44% q/q which was driven by higher mortgage rates. The 30-year fixed mortgage rate ended 2022 at 6.76% and climbed further to reach a rate of 7.50% by the end of September 2023. Purchase activity also collapsed as the vast majority of the 72% of borrowers with a mortgage rate of 4.00% or less are unwilling to assume the punitive increase in monthly payments that would come with moving to a new home. The 2023 year-to-date new issuance total of $172B represented a 63% decline versus the same period from 2022.

Barrow Hanley’s fixed income portfolio of the Timothy Plan Growth & Income, generated a net of fees return of -0.70% versus the Bloomberg Aggregate of 0.64% for the 12-month period ending September 30th. The overweight allocation to Mortgages detracted from relative performance as the sector generated nominal returns below IG Credit bonds and the overall index. In addition, an underweight in Financials negatively impacted performance as they posted the highest nominal returns of any other sector. Helping performance was an overweight to Utilities which outperformed the overall index during the period. Lastly, an overweight to Energy also contributed to performance. We remain focused on generating income consistent with a prudent level of risk.

ANNUAL REPORT | 21

Section 2 | Fund Performance

SEPTEMBER 30, 2023 (UNAUDITED)

Aggressive Growth Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy Aggressive Growth Fund - Class A (With Sales Charge) | 11.13% | 4.65% | 5.97% |

Russell Mid-Cap Growth Index | 17.47% | 6.97% | 9.94% |

Timothy Aggressive Growth Fund - Class C * | 15.66% | 5.02% | 5.77% |

Russell Mid-Cap Growth Index | 17.47% | 6.97% | 9.94% |

Timothy Aggressive Growth Fund - Class I | 17.78% | 6.08% | 6.81% |

Russell Mid-Cap Growth Index | 17.47% | 6.97% | 9.94% |

* | With Maximum Deferred Sales Charge |

Timothy Plan Aggressive Growth Fund vs.

Russell Mid-Cap Growth Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell Mid-Cap Growth Index on September 30, 2013 and held through September 30, 2023. The Class C returns are calculated using the traded NAV on September 29, 2023. The Russell Mid-Cap Growth Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

FUND PERFORMANCE (UNAUDITED)

ANNUAL REPORT | 22

International Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy International Fund - Class A (With Sales Charge) | 12.78% | 1.67% | 2.67% |

MSCI AC World Index ex USA Net (USD) | 20.39% | 2.58% | 3.35% |

Timothy International Fund - Class C * | 17.45% | 2.06% | 2.48% |

MSCI AC World Index ex USA Net (USD) | 20.39% | 2.58% | 3.35% |

Timothy International Fund - Class I | 19.66% | 3.10% | 3.50% |

MSCI AC World Index ex USA Net (USD) | 20.39% | 2.58% | 3.35% |

* | With Maximum Deferred Sales Charge |

Timothy Plan International Fund vs.

MSCI AC World Index ex USA Net (USD)

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the MSCI AC World Index ex USA Net (USD) on September 30, 2013 and held through September 30, 2023. The MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 26 Emerging Markets (EM) countries. With 2,377 constituents, the index covers approximately 85% of the global equity opportunity set outside the US. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

FUND PERFORMANCE (UNAUDITED)

ANNUAL REPORT | 23

Large/Mid Cap Growth Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy Large/Mid Cap Growth Fund - Class A (With Sales Charge) | 12.32% | 6.67% | 8.11% |

Russell 1000 Growth Total Return Index | 27.72% | 12.42% | 14.48% |

Timothy Large/Mid Cap Growth Fund - Class C * | 16.79% | 7.06% | 7.90% |

Russell 1000 Growth Total Return Index | 27.72% | 12.42% | 14.48% |

Timothy Large/Mid Cap Growth Fund - Class I | 19.01% | 8.15% | 8.99% |

Russell 1000 Growth Total Return Index | 27.72% | 12.42% | 14.48% |

* | With Maximum Deferred Sales Charge |

Timothy Plan Large/Mid Cap Growth Fund vs.

Russell 1000 Growth Total Return Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 1000 Growth Total Return Index on September 30, 2013 and held through September 30, 2023. The Russell 1000 Growth Total Return Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

FUND PERFORMANCE (UNAUDITED)

ANNUAL REPORT | 24

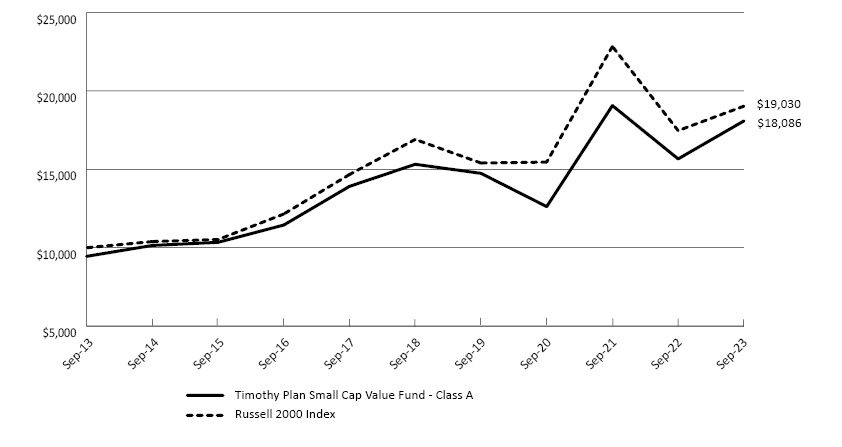

Small Cap Value Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy Small Cap Value Fund - Class A (With Sales Charge) | 9.10% | 2.21% | 6.10% |

Russell 2000 Index | 8.93% | 2.40% | 6.65% |

Timothy Small Cap Value Fund - Class C * | 13.61% | 2.60% | 5.91% |

Russell 2000 Index | 8.93% | 2.40% | 6.65% |

Timothy Small Cap Value Fund - Class I | 15.78% | 3.63% | 6.97% |

Russell 2000 Index | 8.93% | 2.40% | 6.65% |

* | With Maximum Deferred Sales Charge |

Timothy Plan Small Cap Value Fund vs.

Russell 2000 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Russell 2000 Index on September 30, 2013 and held through September 30, 2023. The Russell 2000 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

FUND PERFORMANCE (UNAUDITED)

ANNUAL REPORT | 25

Large/Mid Cap Value Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy Large/Mid Cap Value Fund - Class A (With Sales Charge) | 7.69% | 6.12% | 8.06% |

S&P 500 Index | 21.62% | 9.92% | 11.91% |

Timothy Large/Mid Cap Value Fund - Class C * | 12.06% | 6.52% | 7.86% |

S&P 500 Index | 21.62% | 9.92% | 11.91% |

Timothy Large/Mid Cap Value Fund - Class I | 14.21% | 7.60% | 8.94% |

S&P 500 Index | 21.62% | 9.92% | 11.91% |

* | With Maximum Deferred Sales Charge |

Timothy Plan Large/Mid Cap Value Fund vs.

S&P 500 Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the S&P 500 Index on September 30, 2013 and held through September 30, 2023. The S&P 500 Index is a widely recognized, unmanaged index of common stock prices. Performance figures include the change in value of the stocks in the index and the reinvestment of dividends. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

FUND PERFORMANCE (UNAUDITED)

ANNUAL REPORT | 26

Fixed Income Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy Fixed Income Fund - Class A (With Sales Charge) | (5.02)% | (1.83)% | (0.51)% |

Bloomberg U.S. Aggregate Bond Index | 0.64% | 0.10% | 1.13% |

Timothy Fixed Income Fund - Class C * | (2.21)% | (1.65)% | (0.80)% |

Bloomberg U.S. Aggregate Bond Index | 0.64% | 0.10% | 1.13% |

Timothy Fixed Income Fund - Class I | (0.30)% | (0.70)% | 0.18% |

Bloomberg U.S. Aggregate Bond Index | 0.64% | 0.10% | 1.13% |

* | With Maximum Deferred Sales Charge |

Timothy Plan Fixed Income Fund vs.

Bloomberg U.S. Aggregate Bond Index

The chart shows the value of a hypothetical initial investment of $10,000 in the Fund’s Class A shares and the Bloomberg U.S. Aggregate Bond Index on September 30, 2013 and held through September 30, 2023. The Bloomberg U.S. Aggregate Bond Index is a widely recognized, unmanaged index of bond prices. Performance figures include the change in value of the bonds in the index and the reinvestment of interest. The index return does not reflect expenses, which have been deducted from the Fund’s return. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND IS NOT PREDICTIVE OF FUTURE RESULTS.

FUND PERFORMANCE (UNAUDITED)

ANNUAL REPORT | 27

High Yield Bond Fund

Fund/Index | 1 Year

Total Return | 5 Year

Average

Annual Return | 10 Year

Average

Annual Return |

Timothy High Yield Bond Fund - Class A (With Sales Charge) | 5.00% | 2.07% | 2.73% |

Bloomberg U.S. High Yield Ba/B 3% Index | 9.79% | 3.29% | 4.26% |

Timothy High Yield Bond Fund - Class C * | 8.27% | 2.27% | 2.43% |

Bloomberg U.S. High Yield Ba/B 3% Index | 9.79% | 3.29% | 4.26% |