UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-09491

Allianz Variable Insurance Products Trust

(Exact name of registrant as specified in charter)

5701 Golden Hills Drive, Minneapolis, MN 55416-1297

(Address of principal executive offices) (Zip code)

Citi Fund Services Ohio, Inc., 4400 Easton Commons, Suite 200, Columbus, OH 43219-8000

(Name and address of agent for service)

Registrant’s telephone number, including area code: 800-624-0197

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

AZL® DFA Five-Year Global Fixed Income Fund

Annual Report

December 31, 2022

Table of Contents

This report is submitted for the general information of the shareholder of the Fund. The report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus, which contains details concerning the sales charges and other pertinent information.

|

|

AZL® DFA Five-Year Global Fixed Income Fund Review (Unaudited) |

Allianz Investment Management LLC serves as the Manager for the AZL® DFA Five-Year Global Fixed Income Fund and Dimensional Fund Advisors LP serves as Subadviser to the Fund.

What factors affected the Fund’s performance during the year ended December 31, 2022?*

During the 12-month period, the AZL DFA Five-Year Global Fixed Income Fund returned (6.82)%. That compares to a total return of (4.49)% for the FTSE World Government Bond Index, 1-5 Years, (currency-hedged to USD), the Fund’s primary benchmark.1

In global developed markets and the U.S. Treasury fixed-income market, interest rates rose sharply throughout the year in response to inflationary pressures. Yield curves in global developed markets generally flattened and inverted in some cases during the year in the Fund’s eligible maturity range. Credit spreads widened during the year. Longer-term bonds underperformed shorter-term bonds, and corporate bonds underperformed government bonds.

The Fund underperformed its benchmark during the period. As eligible yield curves flattened during the second half of the year, the Fund increased its emphasis on bonds in the zero- to three-year maturity range. These moves benefited relative performance as shorter-term interest rates rose. However, in the first half of the year, the Fund’s holdings had a longer duration than the benchmark and contained more bonds with a four- to five-year maturity than the benchmark. The Fund also held fewer bonds in the one- to

two-year maturity range relative to the benchmark. These under- and overweightings detracted from the Fund’s relative performance.

The Fund also held fewer Japanese yen-denominated bonds than the benchmark. This underweighting also detracted from its relative performance, as these bonds were among the strongest performers during the period.

The Fund used currency forward contracts to hedge its foreign currency exposure during the period. Given that the Fund’s benchmark index is also currency hedged, this strategy did not affect the Fund’s relative performance.

Past performance does not guarantee future results.

| * | The Fund’s portfolio composition is subject to change. There is no guarantee that any sectors mentioned will continue to perform as described or that securities in such sectors will be held by the Fund in the future. The information contained in this commentary is for informational purposes only and should not be construed as a recommendation to purchase or sell securities in the sector mentioned. The Fund’s holdings and weightings are as of December 31, 2022. |

| 1 | For a complete description of the Fund’s performance benchmark please refer to page 2 of this report. |

1

|

|

AZL® DFA Five-Year Global Fixed Income Fund Review (Unaudited) |

Fund Objective

The Fund’s investment objective is to seek to provide a market rate of return for a fixed income portfolio with low relative volatility of returns, and to seek to focus the eligible universe on securities with relatively less expected upward or downward movement in market value. This objective may be changed by the Trustees of the Fund without shareholder approval. The Fund seeks to achieve its objective by investing in a universe of U.S. and foreign debt securities that mature within five years from the date of settlement.

Investment Concerns

Bonds offer a relatively stable level of income, although bond prices will fluctuate, providing the potential for principal gain or loss. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return.

International investing may involve risk of capital loss from unfavorable fluctuations in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations.

Debt securities held by the Fund may decline in value due to rising interest rates.

Investing in derivative instruments involves risks that may be different from or greater than the risk associated with investing directly in securities or other traditional instruments.

Derivatives are subject to a number of other risks, such as liquidity risk, interest rate risk, market risk, credit risk, counterparty risk, and selection risk.

For a complete description of these and other risks associated with investing in the Fund, please refer to the Fund’s prospectus.

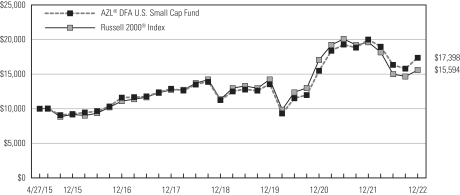

Growth of $10,000 Investment

The chart above represents a comparison of a hypothetical investment in the Fund versus a similar investment in the Fund’s benchmark and represents the reinvestment of dividends and capital gains in the Fund.

| | | | | | | | | | | | | | | | | | | | |

| Average Annual Total Returns as of December 31, 2022 |

| | | 1

Year | | 3

Year | | 5

Year | | Since

Inception

(4/27/15) |

AZL® DFA Five-Year Global Fixed Income Fund | | | | (6.82 | )% | | | | (2.69 | )% | | | | (0.71 | )% | | | | (0.21 | )% |

FTSE World Government Bond Index, 1-5 Years, Currency-Hedged in USD Terms | | | | (4.49 | )% | | | | (0.75 | )% | | | | 0.73 | % | | | | 0.85 | % |

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.Allianzlife.com.

| | | | | |

| Expense Ratio | | Gross |

AZL® DFA Five-Year Global Fixed Income Fund | | | | 0.91 | % |

The above expense ratio is based on the current Fund prospectus dated April 29, 2022. The Manager and the Fund have entered into a written agreement reducing the management fee to 0.50% through at least April 30, 2024. The Manager and the Fund have entered into a written contract limiting operating expenses, excluding certain expenses (such as interest expense), to 0.95% through April 30, 2024. Additional information pertaining to the December 31, 2022 expense ratio can be found in the Financial Highlights.

The total return of the Fund does not reflect the effect of any insurance charges, the annual maintenance fee or the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Such charges, fees and tax payments would reduce the performance quoted.

The Fund’s performance is measured against the FTSE World Government Bond Index, 1-5 Years, Currency-Hedged in USD Terms, an unmanaged index that is designed to measure the performance of fixed-rate; local currency, investment-grade sovereign bonds, and currently comprises sovereign debt from over 20 countries. This index follows the same inclusion criteria and methodology as the FTSE (Non-USD) World Government Bond Index, which is a market capitalization-weighted index that tracks 10 government bond indexes, excluding the U.S. (“WGBI”), but only includes the securities from the WGBI with a weighted average life of greater than or equal to 1 and less than 5 years. The index does not reflect the deduction of fees associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for services provided to the Fund. Investors cannot invest directly in an index.

2

AZL DFA Five-Year Global Fixed Income Fund

Expense Examples

(Unaudited)

As a shareholder of the AZL DFA Five-Year Global Fixed Income Fund (the “Fund”), you incur ongoing costs, including management fees, distribution fees, and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. Please note that the expenses shown in each table do not reflect expenses that apply to the subaccount or the insurance contract. If the expenses that apply to the subaccount or the insurance contract were included, your costs would have been higher.

These examples are based on an investment of $1,000 invested at the beginning of the period and held for the periods presented below.

The Actual Expense table below provides information about actual account values and actual expenses. You may use the information below, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

| | | | | | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

7/1/22 | | Ending

Account Value

12/31/22 | | Expenses Paid

During Period

7/1/22 - 12/31/22* | | Annualized Expense

Ratio During Period

7/1/22 - 12/31/22 |

| | | | |

AZL DFA Five-Year Global Fixed Income Fund | | | $ | 1,000.00 | | | | $ | 992.40 | | | | $ | 3.97 | | | | | 0.79 | % |

The Hypothetical Expense table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

| | | | | | | | | | | | | | | | | | | | |

| | | Beginning

Account Value

7/1/22 | | Ending

Account Value

12/31/22 | | Expenses Paid

During Period

7/1/22 - 12/31/22* | | Annualized Expense

Ratio During Period

7/1/22 - 12/31/22 |

| | | | |

AZL DFA Five-Year Global Fixed Income Fund | | | $ | 1,000.00 | | | | $ | 1,021.22 | | | | $ | 4.02 | | | | | 0.79 | % |

| * | Expenses are equal to the average account value multiplied by the Fund’s annualized expense ratio multiplied by 184/365 (the number of days in the most recent fiscal half-year divided by the number of days in the fiscal year). |

Portfolio Composition

(Unaudited)

| | | | | |

| Investments | | Percent of Net Assets |

| |

Foreign Bonds | | | | 54.1 | % |

| |

Yankee Debt Obligations | | | | 28.8 | |

| |

U.S. Treasury Obligations | | | | 9.5 | |

| |

Corporate Bonds | | | | 7.3 | |

| |

Unaffiliated Investment Company | | | | 3.1 | |

| | | | | |

| |

Total Investment Securities | | | | 102.8 | |

| |

Net other assets (liabilities) | | | | (2.8 | ) |

| | | | | |

| |

Net Assets | | | | 100.0 | % |

| | | | | |

3

AZL DFA Five-Year Global Fixed Income Fund

Schedule of Portfolio Investments

December 31, 2022

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Corporate Bonds (7.3%): | | | |

| Capital Markets (0.4%): | | | |

| $ | 1,629,000 | | | National Securities Clearing Corp., 0.75%, 12/7/25, Callable 11/7/25 @ 100(a) | | $ | 1,444,495 | |

| | | | | | | | |

| Diversified Financial Services (1.2%): | | | |

| | 4,160,000 | | | Berkshire Hathaway, Inc., 3.13%, 3/15/26, Callable 12/15/25 @ 100 | | | 3,995,476 | |

| | | | | | | | |

| Food Products (0.3%): | | | |

| | 1,248,000 | | | Nestle Holdings, Inc., 0.63%, 1/15/26, Callable 12/15/25 @ 100(a) | | | 1,107,731 | |

| | | | | | | | |

| Health Care (0.6%): | | | |

| | 2,000,000 | | | Roche Holdings, Inc., 3.35%, 9/30/24, Callable 6/30/24 @ 100(a) | | | 1,950,808 | |

| | | | | | | | |

| Household Products (1.3%): | | | |

| | 300,000 | | | Procter & Gamble Co. (The), 0.63%, 10/30/24 | | | 306,987 | |

| | 4,406,000 | | | Procter & Gamble Co. (The), 1.00%, 4/23/26 | | | 3,938,374 | |

| | | | | | | | |

| | | | | | | 4,245,361 | |

| | | | | | | | |

| Internet & Direct Marketing Retail (1.6%): | | | |

| | 2,000,000 | | | Amazon.com, Inc., Class A, 2.73%, 4/13/24 | | | 1,950,340 | |

| | 1,500,000 | | | Amazon.com, Inc., 0.45%, 5/12/24 | | | 1,415,116 | |

| | 2,241,000 | | | Amazon.com, Inc., 1.00%, 5/12/26, Callable 4/12/26 @ 100 | | | 1,989,764 | |

| | | | | | | | |

| | | | | | | 5,355,220 | |

| | | | | | | | |

| Oil, Gas & Consumable Fuels (0.3%): | | | |

| | 100,000 | | | Chevron Corp., 1.55%, 5/11/25, Callable 4/11/25 @ 100 | | | 93,231 | |

| | 754,000 | | | Chevron USA, Inc., 0.69%, 8/12/25, Callable 7/12/25 @ 100 | | | 675,217 | |

| | 200,000 | | | Exxon Mobil Corp., 0.14%, 6/26/24, Callable 5/26/24 @ 100 | | | 204,151 | |

| | | | | | | | |

| | | | | | | 972,599 | |

| | | | | | | | |

| Pharmaceuticals (1.3%): | | | |

| | 462,000 | | | Merck & Co., Inc., 0.75%, 2/24/26, Callable 1/24/26 @ 100 | | | 409,952 | |

| | 400,000 | | | Novartis Capital Corp., 3.40%, 5/6/24 | | | 391,902 | |

| | 2,400,000 | | | Roche Holdings, Inc., 1.88%, 3/8/24(a) | | | 2,322,521 | |

| | 1,106,000 | | | Roche Holdings, Inc., 0.99%, 3/5/26, Callable 2/5/26 @ 100(a) | | | 987,493 | |

| | | | | | | | |

| | | | | | | 4,111,868 | |

| | | | | | | | |

| Technology Hardware, Storage & Peripherals (0.3%): | | | |

| | 1,000,000 | | | Apple, Inc., 2.51%, 8/19/24, Callable 6/19/24 @ 100 | | | 711,612 | |

| | 231,000 | | | Apple, Inc., 1.13%, 5/11/25, Callable 4/11/25 @ 100 | | | 212,632 | |

| | | | | | | | |

| | | | | | | 924,244 | |

| | | | | | | | |

| | Total Corporate Bonds (Cost $26,030,033) | | | 24,107,802 | |

| | | | | |

| Foreign Bonds (54.1%): | | | |

| Banks (7.1%): | | | |

| | 3,000,000 | | | Bank of Montreal, 2.89%, 6/20/23+ | | | 2,193,625 | |

| | 700,000 | | | Bank of Montreal, 2.70%, 9/11/24+ | | | 498,309 | |

| | 1,200,000 | | | Bank of Nova Scotia (The), 2.29%, 6/28/24+ | | | 852,223 | |

| | 22,000 | | | BNP Paribas SA, 2.88%, 9/26/23, MTN+ | | | 23,571 | |

| | 3,200,000 | | | Canadian Imperial Bank of Commerce, 2.97%, 7/11/23+ | | | 2,338,165 | |

| | 1,300,000 | | | Dexia Credit Local SA, 0.50%, 7/22/23+ | | | 1,541,022 | |

| | 600,000 | | | Dexia Credit Local SA, 1.63%, 12/8/23, MTN+ | | | 711,488 | |

| | 1,700,000 | | | Dexia Credit Local SA, 1.25%, 11/26/24+ | | | 1,751,565 | |

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Foreign Bonds, continued | | | |

| Banks, continued | | | |

| $ | 600,000 | | | DNB Bank ASA, 0.05%, 11/14/23, MTN+ | | $ | 625,841 | |

| | 200,000 | | | National Australia Bank, Ltd., 0.25%, 5/20/24, MTN+ | | | 205,921 | |

| | 500,000 | | | National Australia Bank, Ltd., 2.90%, 2/25/27, MTN+ | | | 311,460 | |

| | 600,000 | | | Nordic Investment Bank, 3.40%, 2/6/26, MTN+ | | | 397,428 | |

| | 1,350,000 | | | Royal Bank of Canada, 2.33%, 12/5/23+ | | | 972,862 | |

| | 500,000 | | | Royal Bank of Canada, 4.20%, 6/22/26, MTN+ | | | 330,833 | |

| | 1,300,000 | | | Svenska Handelsbanken AB, 0.13%, 6/18/24, MTN+ | | | 1,326,464 | |

| | 200,000 | | | Svenska Handelsbanken AB, 1.00%, 4/15/25, MTN+ | | | 202,862 | |

| | 4,300,000 | | | Toronto-Dominion Bank (The), 3.01%, 5/30/23+ | | | 3,150,422 | |

| | 2,500,000 | | | Toronto-Dominion Bank (The), 1.91%, 7/18/23+ | | | 1,815,316 | |

| | 200,000 | | | Toronto-Dominion Bank (The), 0.63%, 7/20/23, MTN+ | | | 211,626 | |

| | 2,500,000 | | | Toronto-Dominion Bank (The), 3.23%, 7/24/24+ | | | 1,797,071 | |

| | 600,000 | | | Westpac Banking Corp., 0.75%, 10/17/23, MTN+ | | | 631,794 | |

| | 2,400,000 | | | Westpac Banking Corp., 4.13%, 6/4/26, MTN+ | | | 1,593,242 | |

| | | | | | | | |

| | | | | | | 23,483,110 | |

| | | | | | | | |

| Capital Markets (1.5%): | | | |

| | 1,500,000 | | | FMS Wertmanagement, 0.63%, 12/15/23+ | | | 1,758,956 | |

| | 100,000 | | | FMS Wertmanagement, 1.38%, 3/7/25+ | | | 113,185 | |

| | 1,000,000 | | | International Finance Corp., 4.00%, 4/3/25, MTN+ | | | 679,099 | |

| | 3,500,000 | | | International Finance Corp., 3.20%, 7/22/26, MTN+ | | | 2,300,773 | |

| | | | | | | | |

| | | | | | | 4,852,013 | |

| | | | | | | | |

| Diversified Financial Services (8.8%): | | | |

| | 1,000,000 | | | Agence Francaise de Developpement EPIC, 4.00%, 3/14/23+ | | | 1,072,309 | |

| | 2,600,000 | | | Agence Francaise de Developpement EPIC, 3.13%, 1/4/24, MTN+ | | | 2,783,774 | |

| | 290,000 | | | Berkshire Hathaway, Inc., 3.54%, 3/12/25, Callable 2/12/25 @ 100+ | | | 287,588 | |

| | 1,000,000 | | | BNG Bank NV, 3.88%, 5/26/23+ | | | 1,075,788 | |

| | 200,000 | | | BNG Bank NV, 0.05%, 7/11/23, MTN+ | | | 211,056 | |

| | 2,360,000 | | | BNG Bank NV, 3.25%, 7/15/25, MTN+ | | | 1,563,925 | |

| | 1,000,000 | | | Caisse D Amortissement de La Dette Sociale, 1.38%, 11/25/24, MTN+ | | | 1,032,815 | |

| | 73,000 | | | Council Of Europe Development Bank, 0.13%, 5/25/23, MTN+ | | | 77,429 | |

| | 500,000 | | | CPPIB Capital, Inc., 0.38%, 7/25/23+ | | | 592,525 | |

| | 1,400,000 | | | CPPIB Capital, Inc., 0.38%, 6/20/24, MTN+ | | | 1,435,962 | |

| | 700,000 | | | CPPIB Capital, Inc., 0.88%, 12/17/24+ | | | 787,460 | |

| | 420,000 | | | European Financial Stability Facility, 0.13%, 10/17/23, MTN+ | | | 440,575 | |

| | 1,100,000 | | | European Financial Stability Facility, 2.13%, 2/19/24, MTN+ | | | 1,166,766 | |

| | 700,000 | | | European Financial Stability Facility, 2.93%, 4/19/24+ | | | 721,630 | |

| | 549,000 | | | European Financial Stability Facility, 1.75%, 6/27/24, MTN+ | | | 577,046 | |

| | 200,000 | | | European Financial Stability Facility, 0.40%, 2/17/25, MTN+ | | | 202,622 | |

| | 120,000 | | | European Financial Stability Facility, 0.50%, 7/11/25, MTN+ | | | 120,771 | |

| | 550,000 | | | European Financial Stability Facility, 2.96%, 10/15/25+ | | | 542,612 | |

| | 600,000 | | | European Investment Bank, 0.00%, 10/16/23+ | | | 629,039 | |

| | 140,000 | | | European Investment Bank, 0.50%, 11/15/23, MTN+ | | | 147,005 | |

| | 1,310,000 | | | European Investment Bank, 0.88%, 12/15/23, MTN+ | | | 1,539,734 | |

| | 200,000 | | | European Investment Bank, 0.05%, 12/15/23, MTN+ | | | 208,545 | |

See accompanying notes to the financial statements.

4

AZL DFA Five-Year Global Fixed Income Fund

Schedule of Portfolio Investments

December 31, 2022

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Foreign Bonds, continued | | | |

| Diversified Financial Services, continued | | | |

| $ | 7,000,000 | | | European Investment Bank, 0.75%, 9/9/24, MTN+ | | $ | 685,799 | |

| | 200,000 | | | European Investment Bank, 0.88%, 9/13/24, MTN+ | | | 206,486 | |

| | 500,000 | | | European Investment Bank, 0.75%, 11/15/24, MTN+ | | | 565,819 | |

| | 1,122,000 | | | European Investment Bank, 1.38%, 3/7/25, MTN+ | | | 1,270,824 | |

| | 140,000 | | | European Investment Bank, 3.03%, 3/25/25, MTN+ | | | 140,181 | |

| | 2,000,000 | | | European Investment Bank, 1.25%, 5/12/25, MTN+ | | | 182,200 | |

| | 800,000 | | | European Investment Bank, 2.90%, 10/17/25, MTN+ | | | 526,545 | |

| | 500,000 | | | European Stability Mechanism, 0.10%, 7/31/23+ | | | 527,646 | |

| | 366,000 | | | European Stability Mechanism, 0.13%, 4/22/24, MTN+ | | | 377,677 | |

| | 800,000 | | | European Stability Mechanism, 3.01%, 12/16/24+ | | | 807,989 | |

| | 900,000 | | | European Stability Mechanism, 3.01%, 3/14/25+ | | | 902,485 | |

| | 350,000 | | | Kommunalbanken AS, 1.00%, 12/12/24, MTN+ | | | 395,156 | |

| | 600,000 | | | Kommunekredit, 2.00%, 6/25/24, MTN+ | | | 700,239 | |

| | 150,000 | | | Kommunekredit, 0.38%, 11/15/24+ | | | 167,795 | |

| | 1,000,000 | | | Kommuninvest I Sverige AB, 1.00%, 11/13/23, MTN+ | | | 94,253 | |

| | 500,000 | | | Kreditanstalt fuer Wiederaufbau, 3.20%, 9/11/26, MTN+ | | | 328,808 | |

| | 1,100,000 | | | Landwirtschaftliche Rentenbank, 4.75%, 5/6/26, MTN+ | | | 761,160 | |

| | 300,000 | | | Nederlandse Waterschapsbank NV, 3.00%, 11/16/23+ | | | 320,977 | |

| | 1,050,000 | | | Nederlandse Waterschapsbank NV, 2.00%, 12/16/24, MTN+ | | | 1,206,966 | |

| | 300,000 | | | NRW Bank, 1.38%, 12/15/23+ | | | 354,003 | |

| | 800,000 | | | NRW Bank, 0.38%, 12/16/24, MTN+ | | | 892,160 | |

| | 500,000 | | | Op Corporate Bank PLC, 1.00%, 5/22/25, MTN+ | | | 503,425 | |

| | | | | | | | |

| | | | | | | 29,135,569 | |

| | | | | | | | |

| Financial Services (1.0%): | | | |

| | 255,000 | | | International Development Association, 0.75%, 12/12/24+ | | | 287,045 | |

| | 1,300,000 | | | OMERS Finance Trust, 0.45%, 5/13/25+ | | | 1,296,577 | |

| | 950,000 | | | Ontario Teachers’ Finance Trust, 0.50%, 5/6/25+ | | | 948,821 | |

| | 900,000 | | | PSP Capital, Inc., 2.09%, 11/22/23+ | | | 650,063 | |

| | | | | | | | |

| | | | | | | 3,182,506 | |

| | | | | | | | |

| Financials (0.1%): | | | |

| | 150,000 | | | Euroclear Bank SA, 0.13%, 7/7/25, MTN+ | | | 147,703 | |

| | | | | | | | |

| Health Care (0.1%): | | | |

| | 100,000 | | | Novo Nordisk Finance Netherlands BV, 0.75%, 3/31/25, Callable 2/28/25 @ 100, MTN+ | | | 100,961 | |

| | 200,000 | | | Roche Finance Europe BV, 0.88%, 2/25/25, Callable 11/25/24 @ 100, MTN+ | | | 206,803 | |

| | | | | | | | |

| | | | | | | 307,764 | |

| | | | | | | | |

| Industrial Services (1.3%): | | | |

| | 613,000 | | | Network Rail Infrastructure Finance plc, 4.75%, 1/22/24, MTN+ | | | 744,426 | |

| | 1,100,000 | | | Societe Nationale SNCF SA, 4.88%, 6/12/23+ | | | 1,186,451 | |

| | 800,000 | | | Societe Nationale SNCF SA, 4.63%, 2/2/24+ | | | 868,242 | |

| | 1,250,000 | | | Societe Nationale SNCF SA, 4.13%, 2/19/25, MTN+ | | | 1,357,431 | |

| | | | | | | | |

| | | | | | | 4,156,550 | |

| | | | | | | | |

| Insurance (0.3%): | | | |

| | 600,000 | | | UNEDIC ASSEO, 2.38%, 5/25/24, MTN+ | | | 634,645 | |

| | 400,000 | | | UNEDIC ASSEO, 0.13%, 11/25/24, MTN+ | | | 403,455 | |

| | | | | | | | |

| | | | | | | 1,038,100 | |

| | | | | | | | |

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Foreign Bonds, continued | | | |

| National (3.3%): | | | |

| $ | 1,200,000 | | | Agence Francaise de Developpement EPIC, 3.23%, 3/25/25, MTN+ | | $ | 1,196,404 | |

| | 600,000 | | | BNG Bank NV, 2.00%, 4/12/24, MTN+ | | | 703,293 | |

| | 200,000 | | | Bpifrance SACA, 0.75%, 11/25/24+ | | | 204,485 | |

| | 200,000 | | | Bpifrance SACA, 0.50%, 5/25/25, MTN+ | | | 200,775 | |

| | 1,000,000 | | | Export Development Canada, 1.38%, 12/8/23, MTN+ | | | 1,181,546 | |

| | 500,000 | | | Export Development Canada, 3.27%, 1/27/25, MTN+ | | | 500,578 | |

| | 400,000 | | | Kreditanstalt fuer Wiederaufbau, 0.13%, 10/4/24+ | | | 407,993 | |

| | 540,000 | | | Kreditanstalt fuer Wiederaufbau, 2.90%, 11/15/24, MTN+ | | | 547,785 | |

| | 1,120,000 | | | Kreditanstalt fuer Wiederaufbau, 2.95%, 2/18/25, MTN+ | | | 1,126,605 | |

| | 159,000 | | | Kreditanstalt fuer Wiederaufbau, 0.38%, 4/23/25+ | | | 160,465 | |

| | 1,200,000 | | | Kreditanstalt Fuer Wiederaufbau, 0.88%, 7/18/24, MTN+ | | | 1,375,821 | |

| | 64,000 | | | Kreditanstalt Fuer Wiederaufbau, 0.01%, 3/31/25, MTN+ | | | 64,149 | |

| | 2,500,000 | | | Oesterreichische Kontrollbank AG, 0.00%, 4/6/23, MTN+ | | | 2,660,705 | |

| | 400,000 | | | Oesterreichische Kontrollbank AG, 1.25%, 12/15/23, MTN+ | | | 471,535 | |

| | | | | | | | |

| | | | | | | 10,802,139 | |

| | | | | | | | |

| Oil, Gas & Consumable Fuels (0.4%): | | | |

| | 590,000 | | | Shell International Finance BV, 1.13%, 4/7/24+ | | | 615,284 | |

| | 300,000 | | | Shell International Finance BV, 0.50%, 5/11/24, MTN+ | | | 309,678 | |

| | 500,000 | | | Shell International Finance BV, 0.75%, 5/12/24, MTN+ | | | 517,831 | |

| | | | | | | | |

| | | | | | | 1,442,793 | |

| | | | | | | | |

| Pharmaceuticals (0.1%): | | | |

| | 200,000 | | | Abbott Ireland Financing DAC, 0.10%, 11/19/24, Callable 10/19/24 @ 100+ | | | 201,606 | |

| | 100,000 | | | Sanofi, 0.88%, 4/6/25, Callable 3/6/25 @ 100+ | | | 102,182 | |

| | | | | | | | |

| | | | | | | 303,788 | |

| | | | | | | | |

| Regional & Local (2.6%): | | | |

| | 15,000,000 | | | Kommuninvest I Sverige AB, 1.00%, 10/2/24, MTN+ | | | 1,380,982 | |

| | 15,000,000 | | | Kommuninvest I Sverige AB, 1.00%, 5/12/25, MTN+ | | | 1,358,631 | |

| | 1,000,000 | | | Province of Alberta Canada, 0.50%, 4/16/25+ | | | 1,005,512 | |

| | 1,300,000 | | | Province of Alberta Canada, 0.63%, 4/18/25+ | | | 1,309,712 | |

| | 700,000 | | | Province of Quebec Canada, 0.88%, 1/15/25+ | | | 712,961 | |

| | 4,000,000 | | | Queensland Treasury Corp., 3.25%, 7/21/26+(a) | | | 2,654,097 | |

| | 200,000 | | | State of Hesse, 3.14%, 3/10/25+ | | | 200,049 | |

| | | | | | | | |

| | | | | | | 8,621,944 | |

| | | | | | | | |

| Sovereign Bond (24.3%): | | | |

| | 23,000,000 | | | African Development Bank, 0.24%, 4/14/23, MTN+ | | | 2,189,511 | |

| | 150,000 | | | Asian Development Bank, 2.50%, 12/19/24, MTN+ | | | 175,160 | |

| | 1,000,000 | | | Asian Development Bank, 3.75%, 3/12/25, MTN+ | | | 675,280 | |

| | 1,000,000 | | | Asian Development Bank, 0.50%, 5/5/26, MTN+ | | | 603,065 | |

| | 600,000 | | | Austria Treasury Bill, 0.00%, 4/27/23+(b) | | | 637,728 | |

| | 5,000,000 | | | Denmark Government Bond, 1.50%, 11/15/23+ | | | 712,249 | |

| | 66,000,000 | | | Denmark Government Bond, 2.82%, 11/15/24+ | | | 9,020,076 | |

| | 200,000 | | | European Union, 1.88%, 4/4/24+ | | | 211,435 | |

| | 600,000 | | | European Union, 0.50%, 4/4/25, MTN+ | | | 608,669 | |

| | 4,920,000 | | | European Union, 0.80%, 7/4/25+ | | | 4,993,985 | |

| | 700,000 | | | Finland Government Bond, 2.93%, 9/15/24+(a) | | | 713,179 | |

| | 1,300,000 | | | Finland Government Bond, 0.88%, 9/15/25+(a) | | | 1,320,662 | |

See accompanying notes to the financial statements.

5

AZL DFA Five-Year Global Fixed Income Fund

Schedule of Portfolio Investments

December 31, 2022

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Foreign Bonds, continued | | | |

| Sovereign Bond, continued | | | |

| $ | 600,000 | | | French Republic Government Bond OAT, 0.00%, 3/25/24+ | | $ | 619,766 | |

| | 100,000 | | | French Republic Government Bond OAT, 2.25%, 5/25/24+ | | | 106,120 | |

| | 300,000 | | | French Republic Government Bond OAT, 1.75%, 11/25/24+ | | | 314,443 | |

| | 3,200,000 | | | French Republic Government Bond OAT, 2.89%, 2/25/25+(b) | | | 3,220,824 | |

| | 1,100,000 | | | Inter American Development Bank, 1.38%, 12/15/24+ | | | 1,253,166 | |

| | 300,000 | | | Inter-American Development Bank, 2.75%, 10/30/25, MTN+ | | | 196,441 | |

| | 300,000 | | | Inter-American Development Bank, 4.25%, 6/11/26, MTN+ | | | 204,075 | |

| | 2,500,000 | | | International Bank for Reconstruction & Development, 0.50%, 5/18/26, MTN+ | | | 1,503,594 | |

| | 4,950,000 | | | Ireland Government Bond, 3.40%, 3/18/24+ | | | 5,331,878 | |

| | 3,400,000 | | | Irish Government, 5.40%, 3/13/25+ | | | 3,825,328 | |

| | 600,000 | | | Kingdom of Belgium Government Bond, 2.60%, 6/22/24+(a) | | | 639,802 | |

| | 3,300,000 | | | Kingdom of Belgium Government Bond, 0.50%, 10/22/24+(a) | | | 3,392,114 | |

| | 900,000 | | | Kingdom of Belgium Government Bond, 0.80%, 6/22/25+(a) | | | 919,342 | |

| | 100,000 | | | Kuntarahoitus OYJ, 0.13%, 3/7/24, MTN+ | | | 103,366 | |

| | 300,000 | | | Kuntarahoitus OYJ, 0.00%, 11/15/24+ | | | 302,566 | |

| | 1,300,000 | | | Kuntarahoitus OYJ, 0.88%, 12/16/24, MTN+ | | | 1,464,232 | |

| | 450,000 | | | Landeskreditbank Baden Wuerttemberg Foerderbank, 1.38%, 12/15/23, MTN+ | | | 531,309 | |

| | 1,154,000 | | | Landeskreditbank Baden Wuerttemberg Foerderbank, 0.38%, 12/9/24, MTN+ | | | 1,293,511 | |

| | 750,000 | | | Netherlands Government Bond, 0.00%, 1/15/24+(a) | | | 779,524 | |

| | 2,100,000 | | | Netherlands Government Bond, 2.00%, 7/15/24+(a) | | | 2,220,652 | |

| | 300,000 | | | Netherlands Government Bond, 0.25%, 7/15/25+(a) | | | 301,920 | |

| | 8,700,000 | | | New South Wales Treasury Corp., 4.00%, 5/20/26+ | | | 5,920,948 | |

| | 2,900,000 | | | New Zealand Government Bond, 5.50%, 4/15/23+ | | | 1,844,479 | |

| | 500,000 | | | New Zealand Government Bond, 0.50%, 5/15/24+ | | | 298,214 | |

| | 4,500,000 | | | New Zealand Local Government Funding Agency Bond, 2.25%, 4/15/24+ | | | 2,740,336 | |

| | 500,000 | | | New Zealand Local Government Funding Agency Bond, 2.75%, 4/15/25+ | | | 298,917 | |

| | 11,100,000 | | | Norway Government Bond, 1.75%, 3/13/25+(a) | | | 1,101,764 | |

| | 21,500,000 | | | Norwegian Government, 3.00%, 3/14/24+(a) | | | 2,192,496 | |

| | 3,500,000 | | | Province of Ontario Canada, 2.60%, 9/8/23+ | | | 2,550,259 | |

| | 100,000 | | | Province of Ontario Canada, 0.50%, 12/15/23+ | | | 117,045 | |

| | 600,000 | | | Province of Ontario Canada, 0.38%, 6/14/24+ | | | 615,226 | |

| | 100,000 | | | Province of Ontario Canada, 0.88%, 1/21/25, MTN+ | | | 101,781 | |

| | 500,000 | | | Province of Ontario Canada, 3.10%, 8/26/25, MTN+ | | | 329,128 | |

| | 300,000 | | | Province of Quebec Canada, 0.75%, 12/13/24+ | | | 337,193 | |

| | 1,000,000 | | | Republic of Austria, 1.65%, 10/21/24+(a) | | | 1,045,573 | |

| | 550,000 | | | Republic of Austria Government Bond, 1.75%, 10/20/23+(a) | | | 583,189 | |

| | 700,000 | | | State of North Rhine-Westphalia Germany, 0.63%, 12/16/24+ | | | 784,938 | |

| | 100,000 | | | Svensk Exportkredit AB, Series E, 1.38%, 12/15/23, MTN+ | | | 117,962 | |

| | 18,000,000 | | | Sweden Government Bond, 1.50%, 11/13/23+(a) | | | 1,703,503 | |

| | 17,000,000 | | | Sweden Government Bond, 2.50%, 5/12/25+(a) | | | 1,618,253 | |

| | 7,000,000 | | | Sweden Treasury Bill, 0.00%, 6/21/23+(a)(b) | | | 663,319 | |

| | 7,700,000 | | | Treasury Corp. of Victoria, 0.50%, 11/20/25, MTN+ | | | 4,749,106 | |

| | | | | | | | |

| | | | | | | 80,098,601 | |

| | | | | | | | |

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Foreign Bonds, continued | | | |

| Supranationals (3.2%): | | | |

| $ | 4,600,000 | | | Asian Development Bank, 1.38%, 12/15/23, MTN+ | | $ | 5,432,552 | |

| | 438,000 | | | Council Of Europe Development Bank, 0.38%, 3/27/25, MTN+ | | | 440,353 | |

| | 100,000 | | | Eurofima Europaeische Gesellschaft fuer die Finanzierung von Eisenbahnmaterial, 0.25%, 2/9/24, MTN+ | | | 103,549 | |

| | 2,800,000 | | | Inter American Development Bank, 1.25%, 12/15/23+ | | | 3,302,575 | |

| | 500,000 | | | Inter American Development Bank, 2.70%, 1/29/26, MTN+ | | | 325,156 | |

| | 1,100,000 | | | International Bank For Reconstruction, 2.50%, 8/3/23+ | | | 802,282 | |

| | 2,000,000 | | | Nordic Investment Bank, 1.50%, 3/13/25, MTN+ | | | 196,529 | |

| | | | | | | | |

| | | | | | | 10,602,996 | |

| | | | | | | | |

| Transportation Infrastructure (0.0%†): | | | |

| | 100,000 | | | SNCF Reseau, 4.50%, 1/30/24+ | | | 108,429 | |

| | | | | | | | |

| | Total Foreign Bonds (Cost $181,342,621) | | | 178,284,005 | |

| | | | | |

| Yankee Debt Obligations (28.8%): | | | |

| Banks (8.1%): | | | |

| | 500,000 | | | Australia & New Zealand Banking Group, Ltd., 4.05%, 5/12/25, MTN | | | 335,104 | |

| | 1,000,000 | | | Commonwealth Bank of Australia, 4.20%, 8/18/25, MTN | | | 672,300 | |

| | 2,208,000 | | | Commonwealth Bank of Australia, 1.13%, 6/15/26(a) | | | 1,942,333 | |

| | 20,000 | | | Cooperatieve Rabobank UA, 1.38%, 1/10/25 | | | 18,683 | |

| | 1,400,000 | | | Dexia Credit Local SA, 0.50%, 7/16/24 | | | 1,311,328 | |

| | 400,000 | | | National Australia Bank, Ltd., 1.39%, 1/12/25(a) | | | 373,120 | |

| | 2,000,000 | | | National Australia Bank, Ltd., 3.90%, 5/30/25, MTN | | | 1,336,360 | |

| | 1,000,000 | | | National Australia Bank, Ltd., 3.38%, 1/14/26 | | | 957,182 | |

| | 1,690,000 | | | Nordea Bank Abp, 0.75%, 8/28/25(a) | | | 1,510,950 | |

| | 2,000,000 | | | Skandinaviska Enskilda Banken AB, 0.85%, 9/2/25(a) | | | 1,788,512 | |

| | 6,779,000 | | | Skandinaviska Enskilda Banken AB, 1.20%, 9/9/26(a) | | | 5,913,139 | |

| | 1,250,000 | | | Svenska Handelsbanken AB, 0.55%, 6/11/24(a) | | | 1,171,416 | |

| | 2,663,000 | | | Toronto-Dominion Bank (The), 0.75%, 1/6/26, MTN | | | 2,353,746 | |

| | 17,000 | | | Toronto-Dominion Bank (The), 1.20%, 6/3/26 | | | 15,032 | |

| | 1,000,000 | | | Westpac Banking Corp., 1.02%, 11/18/24 | | | 929,575 | |

| | 1,891,000 | | | Westpac Banking Corp., 2.35%, 2/19/25 | | | 1,794,850 | |

| | 700,000 | | | Westpac Banking Corp., 2.70%, 3/17/25, MTN | | | 457,153 | |

| | 1,000,000 | | | Westpac Banking Corp., 2.85%, 5/13/26 | | | 937,865 | |

| | 3,423,000 | | | Westpac Banking Corp., 1.15%, 6/3/26 | | | 3,025,805 | |

| | | | | | | | |

| | | | | | | 26,844,453 | |

| | | | | | | | |

| Capital Markets (1.5%): | | | |

| | 1,800,000 | | | Erste Abwicklungsanstalt, 0.25%, 3/1/24, MTN | | | 1,708,830 | |

| | 2,400,000 | | | Erste Abwicklungsanstalt, 0.88%, 10/30/24, MTN | | | 2,238,768 | |

| | 1,000,000 | | | PSP Capital, Inc., 0.50%, 9/15/24 | | | 932,590 | |

| | | | | | | | |

| | | | | | | 4,880,188 | |

| | | | | | | | |

| Diversified Financial Services (3.2%): | | | |

| | 4,800,000 | | | Agence Francaise de Developpement EPIC, 0.63%, 1/22/26, MTN | | | 4,267,152 | |

| | 796,000 | | | Caisse D Amortissement de La Dette Sociale, 3.38%, 3/20/24, MTN | | | 782,986 | |

| | 541,000 | | | European Investment Bank, 3.25%, 1/29/24 | | | 532,252 | |

| | 900,000 | | | Kommunalbanken AS, 4.25%, 7/16/25, MTN | | | 611,513 | |

| | 2,800,000 | | | Kommunalbanken AS, 0.60%, 6/1/26, MTN | | | 1,677,041 | |

| | 2,634,000 | | | Kreditanstalt fuer Wiederaufbau, 0.25%, 3/8/24 | | | 2,498,125 | |

| | | | | | | | |

| | | | | | | 10,369,069 | |

| | | | | | | | |

See accompanying notes to the financial statements.

6

AZL DFA Five-Year Global Fixed Income Fund

Schedule of Portfolio Investments

December 31, 2022

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Yankee Debt Obligations, continued | | | |

| National (4.1%): | | | |

| $ | 900,000 | | | BNG Bank NV, 3.50%, 8/26/24(a) | | $ | 882,630 | |

| | 1,665,000 | | | Export Development Canada, 2.63%, 2/21/24 | | | 1,624,006 | |

| | 205,000 | | | FMS Wertmanagement, 2.75%, 1/30/24 | | | 200,640 | |

| | 600,000 | | | Kommunalbanken AS, 0.25%, 12/8/23, MTN | | | 574,850 | |

| | 300,000 | | | Kommunalbanken AS, 2.75%, 2/5/24 | | | 293,844 | |

| | 1,000,000 | | | Kommunalbanken AS, 2.00%, 6/19/24, MTN | | | 960,360 | |

| | 1,150,000 | | | Nederlandse Waterschapsbank NV, 1.13%, 3/15/24, MTN | | | 1,100,130 | |

| | 2,402,000 | | | Oesterreichische Kontrollbank AG, 0.50%, 9/16/24 | | | 2,240,206 | |

| | 2,000,000 | | | Svensk Exportkredit AB, 0.38%, 3/11/24 | | | 1,897,868 | |

| | 1,800,000 | | | Svensk Exportkredit AB, 3.63%, 9/3/24 | | | 1,764,587 | |

| | 2,000,000 | | | Swedish Export Credit, 0.50%, 11/10/23 | | | 1,927,314 | |

| | | | | | | | |

| | | | | | | 13,466,435 | |

| | | | | | | | |

| Oil, Gas & Consumable Fuels (1.1%): | | | |

| | 4,000,000 | | | Equinor ASA, 1.75%, 1/22/26, Callable 12/22/25 @ 100 | | | 3,659,600 | |

| | | | | | | | |

| Regional & Local (3.2%): | | | |

| | 1,300,000 | | | Kommunekredit, 1.00%, 12/15/23 | | | 1,254,968 | |

| | 1,200,000 | | | Kommuninvest I Sverige, 3.25%, 1/16/24, MTN | | | 1,180,890 | |

| | 300,000 | | | Kommuninvest I Sverige, 0.38%, 2/16/24 | | | 285,396 | |

| | 3,000,000 | | | Kommuninvest I Sverige AB, 1.38%, 5/8/24, MTN | | | 2,865,186 | |

| | 1,000,000 | | | Kommuninvest I Sverige AB, 1.38%, 5/8/24(a) | | | 955,062 | |

| | 1,486,000 | | | Kommuninvest I Sverige AB, 2.88%, 7/3/24(a) | | | 1,444,162 | |

| | 2,581,000 | | | Landeskreditbank Baden-Wuerttemberg Foerderbank, 2.00%, 7/23/24, MTN | | | 2,477,631 | |

| | | | | | | | |

| | | | | | | 10,463,295 | |

| | | | | | | | |

| Sovereign Bond (5.7%): | | | |

| | 844,000 | | | Asian Infrastructure Investment Bank (The), 2.25%, 5/16/24 | | | 815,111 | |

| | 3,714,000 | | | International Bank for Reconstruction & Development, 2.50%, 3/19/24 | | | 3,615,278 | |

| | 500,000 | | | Ontario Province of, 3.40%, 10/17/23 | | | 493,670 | |

| | 600,000 | | | Province of Alberta Canada, 2.95%, 1/23/24 | | | 588,122 | |

| | 1,000,000 | | | Province of Manitoba Canada, 2.60%, 4/16/24 | | | 972,701 | |

| | 2,400,000 | | | Province of Ontario Canada, 3.05%, 1/29/24 | | | 2,352,398 | |

| | | | | | | | |

Principal

Amount | | | | | Value | |

| Yankee Debt Obligations, continued | | | |

| Sovereign Bond, continued | | | |

| $ | 5,120,000 | | | Province of Quebec Canada, 2.50%, 4/9/24 | | $ | 4,973,870 | |

| | 2,800,000 | | | SFIL SA, 0.63%, 2/9/26, MTN | | | 2,487,800 | |

| | 2,800,000 | | | Svensk Exportkredit AB, 0.38%, 7/30/24 | | | 2,614,212 | |

| | | | | | | | |

| | | | | | | 18,913,162 | |

| | | | | | | | |

| Supranationals (1.9%): | | | |

| | 3,528,000 | | | Asian Development Bank, 1.63%, 3/15/24 | | | 3,397,623 | |

| | 454,000 | | | Inter-American Development Bank, 3.00%, 2/21/24 | | | 445,450 | |

| | 1,000,000 | | | Inter-American Development Bank, 3.25%, 7/1/24 | | | 979,523 | |

| | 324,000 | | | Inter-American Investment Corp., 1.75%, 10/2/24 | | | 307,871 | |

| | 1,000,000 | | | International Bank for Reconstruction & Development, 2.25%, 3/28/24 | | | 969,697 | |

| | | | | | | | |

| | | | | | | 6,100,164 | |

| | | | | | | | |

| | Total Yankee Debt Obligations (Cost $100,045,183) | | | 94,696,366 | |

| | | | | |

| U.S. Treasury Obligations (9.5%): | | | |

| U.S. Treasury Notes (9.5%): | |

| | 3,750,000 | | | 0.13%, 8/15/23 | | | 3,644,531 | |

| | 4,708,700 | | | 0.75%, 12/31/23 | | | 4,526,238 | |

| | 5,500,000 | | | 0.88%, 1/31/24 | | | 5,275,703 | |

| | 3,000,000 | | | 2.50%, 1/31/24 | | | 2,928,750 | |

| | 1,500,000 | | | 0.13%, 2/15/24 | | | 1,425,000 | |

| | 8,000,000 | | | 0.38%, 4/15/24 | | | 7,570,000 | |

| | 6,400,000 | | | 0.25%, 5/15/24 | | | 6,024,000 | |

| | | | | | | | |

| | | | | | | 31,394,222 | |

| | | | | | | | |

| | Total U.S. Treasury Obligations (Cost $31,648,358) | | | 31,394,222 | |

| | | | | |

| | |

| Shares | | | | | Value | |

| Unaffiliated Investment Company (3.1%): | | | |

| Money Markets (3.1%): | | | |

| | 10,319,797 | | | Dreyfus Treasury Securities Cash Management Fund, Institutional Shares, 3.90%(b) | | | 10,319,797 | |

| | | | | | | | |

| | Total Unaffiliated Investment Company (Cost $10,319,797) | | | 10,319,797 | |

| | | | | |

| | Total Investment Securities (Cost $349,385,992) — 102.8%(c) | | | 338,802,192 | |

| | Net other assets (liabilities) — (2.8)% | | | (9,117,853 | ) |

| | | | | | | | |

| | Net Assets — 100.0% | | $ | 329,684,339 | |

| | | | | | | | |

Percentages indicated are based on net assets as of December 31, 2022.

MTN—Medium Term Note

| + | The principal amount is disclosed in local currency and the fair value is disclosed in U.S. Dollars. |

| † | Represents less than 0.05%. |

| (a) | Rule 144A, Section 4(2) or other security which is restricted to resale to institutional investors. |

| (b) | The rate represents the effective yield at December 31, 2022. |

| (c) | See Federal Tax Information listed in the Notes to the Financial Statements. |

See accompanying notes to the financial statements.

7

AZL DFA Five-Year Global Fixed Income Fund

Schedule of Portfolio Investments

December 31, 2022

The following represents the concentrations by country of risk (based on the domicile of the security issuer) relative to the total value of investments as of December 31, 2022:

| | | | |

| Country | | Percentage | |

| |

Australia | | | 8.5 | % |

Austria | | | 2.3 | % |

Belgium | | | 1.5 | % |

Canada | | | 12.7 | % |

Denmark | | | 3.5 | % |

Finland | | | 1.7 | % |

France | | | 8.3 | % |

Germany | | | 5.9 | % |

Ireland | | | 2.8 | % |

Luxembourg | | | 1.1 | % |

Netherlands | | | 3.6 | % |

New Zealand | | | 1.5 | % |

Norway | | | 3.6 | % |

Supranational | | | 13.8 | % |

Sweden | | | 9.5 | % |

United Kingdom | | | 0.2 | % |

United States | | | 19.5 | % |

| | | | |

| | | 100.0 | % |

| | | | |

Forward Currency Contracts

At December 31, 2022, the Fund’s open forward currency contracts were as follows:

| | | | | | | | | | | | | | | | | | | | |

| Currency Purchased | | | | | Currency Sold | | | | | Counterparty | | Settlement

Date | | | Net Unrealized

Appreciation/

(Depreciation) | |

Norwegian Krone | | | 4,038,267 | | | U.S. Dollar | | | 394,065 | | | HSBC | | | 1/5/23 | | | $ | 18,750 | |

Norwegian Krone | | | 1,970,005 | | | U.S. Dollar | | | 185,227 | | | HSBC | | | 1/5/23 | | | | 16,158 | |

Norwegian Krone | | | 3,361,544 | | | U.S. Dollar | | | 316,923 | | | HSBC | | | 1/5/23 | | | | 26,713 | |

Norwegian Krone | | | 5,093,693 | | | U.S. Dollar | | | 492,064 | | | HSBC | | | 1/5/23 | | | | 28,643 | |

U.S. Dollar | | | 2,879,736 | | | Swedish Krona | | | 29,805,153 | | | HSBC | | | 1/11/23 | | | | 19,712 | |

Australian Dollar | | | 83,891 | | | U.S. Dollar | | | 54,627 | | | ANZ Banking Group | | | 1/17/23 | | | | 2,520 | |

Australian Dollar | | | 881,369 | | | U.S. Dollar | | | 589,574 | | | ANZ Banking Group | | | 1/17/23 | | | | 10,817 | |

U.S. Dollar | | | 1,588,571 | | | Swedish Krona | | | 16,485,351 | | | Bank of America | | | 1/17/23 | | | | 6,035 | |

Australian Dollar | | | 514,719 | | | U.S. Dollar | | | 349,188 | | | Bank of America | | | 1/17/23 | | | | 1,440 | |

U.S. Dollar | | | 643,120 | | | European Euro | | | 600,063 | | | BNY Mellon | | | 1/18/23 | | | | 52 | |

British Pound | | | 620,420 | | | U.S. Dollar | | | 706,414 | | | Bank of America | | | 1/20/23 | | | | 43,907 | |

British Pound | | | 348,095 | | | U.S. Dollar | | | 402,687 | | | Bank of America | | | 1/20/23 | | | | 18,291 | |

British Pound | | | 257,754 | | | U.S. Dollar | | | 304,695 | | | Bank of America | | | 1/20/23 | | | | 7,026 | |

British Pound | | | 320,816 | | | U.S. Dollar | | | 359,139 | | | Bank of America | | | 1/20/23 | | | | 28,848 | |

British Pound | | | 134,722 | | | U.S. Dollar | | | 154,134 | | | Bank of America | | | 1/20/23 | | | | 8,795 | |

British Pound | | | 411,903 | | | U.S. Dollar | | | 468,953 | | | HSBC | | | 1/20/23 | | | | 29,192 | |

British Pound | | | 477,597 | | | U.S. Dollar | | | 560,347 | | | HSBC | | | 1/20/23 | | | | 17,247 | |

British Pound | | | 382,916 | | | U.S. Dollar | | | 443,117 | | | State Street | | | 1/20/23 | | | | 19,972 | |

British Pound | | | 417,547 | | | U.S. Dollar | | | 500,520 | | | UBS | | | 1/20/23 | | | | 4,451 | |

U.S. Dollar | | | 289,759 | | | New Zealand Dollar | | | 448,692 | | | UBS | | | 1/20/23 | | | | 4,892 | |

U.S. Dollar | | | 380,075 | | | Swedish Krona | | | 3,947,365 | | | HSBC | | | 1/23/23 | | | | 987 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | 314,448 | |

| | | | | | | | | | | | | | | | | | | | |

U.S. Dollar | | | 1,443,388 | | | European Euro | | | 1,445,120 | | | Bank of America | | | 1/3/23 | | | | (103,650 | ) |

U.S. Dollar | | | 1,234,263 | | | European Euro | | | 1,248,902 | | | Bank of America | | | 1/3/23 | | | | (102,718 | ) |

U.S. Dollar | | | 686,336 | | | European Euro | | | 684,540 | | | Bank of America | | | 1/3/23 | | | | (46,481 | ) |

U.S. Dollar | | | 635,571 | | | European Euro | | | 612,681 | | | Barclays Bank | | | 1/3/23 | | | | (20,320 | ) |

U.S. Dollar | | | 1,498,252 | | | European Euro | | | 1,508,369 | | | HSBC | | | 1/3/23 | | | | (116,496 | ) |

U.S. Dollar | | | 463,519 | | | European Euro | | | 463,109 | | | HSBC | | | 1/3/23 | | | | (32,251 | ) |

U.S. Dollar | | | 3,086,479 | | | Danish Krone | | | 22,943,596 | | | State Street | | | 1/3/23 | | | | (217,685 | ) |

U.S. Dollar | | | 1,583,059 | | | European Euro | | | 1,570,543 | | | State Street | | | 1/3/23 | | | | (98,247 | ) |

U.S. Dollar | | | 399,822 | | | European Euro | | | 407,588 | | | State Street | | | 1/3/23 | | | | (36,512 | ) |

U.S. Dollar | | | 14,583,981 | | | European Euro | | | 14,592,484 | | | State Street | | | 1/3/23 | | | | (1,037,646 | ) |

See accompanying notes to the financial statements.

8

AZL DFA Five-Year Global Fixed Income Fund

Schedule of Portfolio Investments

December 31, 2022

| | | | | | | | | | | | | | | | | | | | |

| Currency Purchased | | | | | Currency Sold | | | | | Counterparty | | Settlement

Date | | | Net Unrealized

Appreciation/

(Depreciation) | |

U.S. Dollar | | | 353,131 | | | European Euro | | | 350,563 | | | State Street | | | 1/3/23 | | | $ | (22,155 | ) |

U.S. Dollar | | | 428,682 | | | European Euro | | | 431,156 | | | UBS | | | 1/3/23 | | | | (32,882 | ) |

U.S. Dollar | | | 1,457,657 | | | European Euro | | | 1,480,328 | | | UBS | | | 1/3/23 | | | | (127,072 | ) |

U.S. Dollar | | | 343,896 | | | Australian Dollar | | | 513,780 | | | Bank of America | | | 1/5/23 | | | | (5,909 | ) |

U.S. Dollar | | | 389,657 | | | Australian Dollar | | | 599,611 | | | Bank of America | | | 1/5/23 | | | | (18,586 | ) |

U.S. Dollar | | | 5,279,758 | | | Norwegian Krone | | | 55,716,875 | | | Bank of America | | | 1/5/23 | | | | (415,941 | ) |

U.S. Dollar | | | 43,817 | | | Norwegian Krone | | | 438,239 | | | Barclays Bank | | | 1/5/23 | | | | (982 | ) |

U.S. Dollar | | | 3,325,595 | | | Danish Krone | | | 23,289,041 | | | Bank of America | | | 1/6/23 | | | | (29,165 | ) |

U.S. Dollar | | | 1,280,236 | | | Swedish Krona | | | 14,415,665 | | | Citigroup | | | 1/11/23 | | | | (103,053 | ) |

U.S. Dollar | | | 470,071 | | | Swedish Krona | | | 4,922,530 | | | HSBC | | | 1/11/23 | | | | (2,282 | ) |

U.S. Dollar | | | 759,901 | | | Swedish Krona | | | 7,920,307 | | | Bank of America | | | 1/17/23 | | | | (420 | ) |

U.S. Dollar | | | 10,296,976 | | | Canadian Dollar | | | 14,091,842 | | | Bank of America | | | 1/17/23 | | | | (113,220 | ) |

Australian Dollar | | | 1,469,426 | | | U.S. Dollar | | | 1,001,229 | | | Bank of America | | | 1/17/23 | | | | (251 | ) |

U.S. Dollar | | | 30,391,749 | | | Australian Dollar | | | 48,251,901 | | | Citigroup | | | 1/17/23 | | | | (2,477,586 | ) |

Australian Dollar | | | 487,982 | | | U.S. Dollar | | | 335,663 | | | Citigroup | | | 1/17/23 | | | | (3,249 | ) |

U.S. Dollar | | | 6,964,432 | | | European Euro | | | 7,070,929 | | | Bank of America | | | 1/18/23 | | | | (613,255 | ) |

U.S. Dollar | | | 816,457 | | | European Euro | | | 774,360 | | | BNY Mellon | | | 1/18/23 | | | | (13,400 | ) |

U.S. Dollar | | | 723,119 | | | Danish Krone | | | 5,148,536 | | | Bank of America | | | 1/18/23 | | | | (19,272 | ) |

U.S. Dollar | | | 1,421,128 | | | European Euro | | | 1,359,311 | | | Bank of America | | | 1/18/23 | | | | (35,602 | ) |

U.S. Dollar | | | 428,731 | | | European Euro | | | 411,741 | | | Bank of America | | | 1/18/23 | | | | (12,519 | ) |

U.S. Dollar | | | 1,199,251 | | | European Euro | | | 1,151,118 | | | Bank of America | | | 1/18/23 | | | | (34,366 | ) |

U.S. Dollar | | | 867,696 | | | Danish Krone | | | 6,553,430 | | | Bank of America | | | 1/18/23 | | | | (77,274 | ) |

U.S. Dollar | | | 936,644 | | | European Euro | | | 930,219 | | | Barclays Bank | | | 1/18/23 | | | | (60,242 | ) |

U.S. Dollar | | | 353,740 | | | European Euro | | | 331,072 | | | Citigroup | | | 1/18/23 | | | | (1,059 | ) |

U.S. Dollar | | | 251,362 | | | European Euro | | | 236,334 | | | Citigroup | | | 1/18/23 | | | | (1,910 | ) |

U.S. Dollar | | | 1,730,584 | | | European Euro | | | 1,635,668 | | | State Street | | | 1/18/23 | | | | (22,309 | ) |

U.S. Dollar | | | 861,528 | | | European Euro | | | 829,383 | | | UBS | | | 1/18/23 | | | | (27,295 | ) |

U.S. Dollar | | | 839,184 | | | European Euro | | | 803,660 | | | Barclays Bank | | | 1/19/23 | | | | (22,134 | ) |

U.S. Dollar | | | 100,785 | | | European Euro | | | 96,693 | | | Citigroup | | | 1/19/23 | | | | (2,845 | ) |

U.S. Dollar | | | 1,448,446 | | | Danish Krone | | | 10,336,569 | | | Citigroup | | | 1/19/23 | | | | (42,156 | ) |

U.S. Dollar | | | 7,882,395 | | | Canadian Dollar | | | 10,796,292 | | | HSBC | | | 1/19/23 | | | | (93,347 | ) |

U.S. Dollar | | | 2,798,475 | | | European Euro | | | 2,662,724 | | | State Street | | | 1/19/23 | | | | (55,283 | ) |

U.S. Dollar | | | 786,729 | | | European Euro | | | 746,288 | | | State Street | | | 1/19/23 | | | | (13,101 | ) |

U.S. Dollar | | | 7,218,031 | | | European Euro | | | 6,928,341 | | | State Street | | | 1/19/23 | | | | (207,377 | ) |

U.S. Dollar | | | 358,269 | | | European Euro | | | 346,271 | | | State Street | | | 1/19/23 | | | | (12,845 | ) |

U.S. Dollar | | | 404,705 | | | European Euro | | | 383,493 | | | State Street | | | 1/19/23 | | | | (6,301 | ) |

U.S. Dollar | | | 1,025,019 | | | European Euro | | | 971,201 | | | State Street | | | 1/19/23 | | | | (15,860 | ) |

U.S. Dollar | | | 399,114 | | | European Euro | | | 383,798 | | | State Street | | | 1/19/23 | | | | (12,219 | ) |

U.S. Dollar | | | 1,781,130 | | | European Euro | | | 1,680,385 | | | State Street | | | 1/19/23 | | | | (19,812 | ) |

U.S. Dollar | | | 294,269 | | | European Euro | | | 283,402 | | | State Street | | | 1/19/23 | | | | (9,465 | ) |

U.S. Dollar | | | 33,580,793 | | | British Pound | | | 30,160,537 | | | HSBC | | | 1/20/23 | | | | (2,894,614 | ) |

British Pound | | | 555,305 | | | U.S. Dollar | | | 678,825 | | | State Street | | | 1/20/23 | | | | (7,253 | ) |

U.S. Dollar | | | 1,813,420 | | | Swedish Krona | | | 19,260,304 | | | Bank of America | | | 1/23/23 | | | | (36,256 | ) |

U.S. Dollar | | | 4,251,519 | | | New Zealand Dollar | | | 6,794,700 | | | UBS | | | 1/24/23 | | | | (62,560 | ) |

U.S. Dollar | | | 562,042 | | | British Pound | | | 500,235 | | | State Street | | | 1/25/23 | | | | (43,015 | ) |

U.S. Dollar | | | 684,826 | | | European Euro | | | 674,616 | | | State Street | | | 1/25/23 | | | | (38,498 | ) |

U.S. Dollar | | | 14,688,888 | | | European Euro | | | 14,556,862 | | | State Street | | | 1/25/23 | | | | (918,992 | ) |

U.S. Dollar | | | 3,208,019 | | | Danish Krone | | | 22,338,689 | | | HSBC | | | 1/30/23 | | | | (16,353 | ) |

U.S. Dollar | | | 26,479,525 | | | European Euro | | | 24,795,383 | | | State Street | | | 1/30/23 | | | | (115,546 | ) |

U.S. Dollar | | | 622,783 | | | New Zealand Dollar | | | 1,004,961 | | | Citigroup | | | 2/28/23 | | | | (15,481 | ) |

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | $ | (10,744,575 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total Net Forward Currency Contracts | | | | | | | | | | | | | | | | | | $ | (10,430,127 | ) |

| | | | | | | | | | | | | | | | | | | | |

Balances Reported in the Statement of Assets and Liabilities for Forward Currency Contracts

| | | | | | | | | | |

| | | Unrealized

Appreciation | | Unrealized

Depreciation |

Forward currency contracts | | | $ | 314,448 | | | | $ | (10,744,575 | ) |

See accompanying notes to the financial statements.

9

AZL DFA Five-Year Global Fixed Income Fund

Statement of Assets and Liabilities

December 31, 2022

| | | | | |

Assets: | | | | | |

Investment securities, at cost | | | $ | 349,385,992 | |

| | | | | |

Investment securities, at value | | | $ | 338,802,192 | |

Interest and dividends receivable | | | | 2,053,256 | |

Foreign currency, at value (cost $298,892) | | | | 298,146 | |

Unrealized appreciation on forward currency contracts | | | | 314,448 | |

Receivable for capital shares issued | | | | 196 | |

Prepaid expenses | | | | 152 | |

| | | | | |

Total Assets | | | | 341,468,390 | |

| | | | | |

Liabilities: | | | | | |

Unrealized depreciation on forward currency contracts | | | | 10,744,575 | |

Payable for investments purchased | | | | 792,465 | |

Payable for capital shares redeemed | | | | 2,145 | |

Management fees payable | | | | 140,550 | |

Administration fees payable | | | | 12,686 | |

Distribution fees payable | | | | 70,274 | |

Custodian fees payable | | | | 7,120 | |

Administrative and compliance services fees payable | | | | 1,050 | |

Transfer agent fees payable | | | | 968 | |

Trustee fees payable | | | | 2,622 | |

Other accrued liabilities | | | | 9,596 | |

| | | | | |

Total Liabilities | | | | 11,784,051 | |

| | | | | |

Net Assets | | | $ | 329,684,339 | |

| | | | | |

Net Assets Consist of: | | | | | |

Paid in capital | | | $ | 372,946,968 | |

Total distributable earnings | | | | (43,262,629 | ) |

| | | | | |

Net Assets | | | $ | 329,684,339 | |

| | | | | |

Shares of beneficial interest (unlimited number of shares authorized, no par value) | | | | 38,984,281 | |

Net Asset Value (offering and redemption price per share) | | | $ | 8.46 | |

| | | | | |

Statement of Operations

For the Year Ended December 31, 2022

| | | | | |

Investment Income: | | | | | |

Interest | | | $ | 6,232,336 | |

Dividends | | | | 82,549 | |

Income from securities lending | | | | 3,508 | |

| | | | | |

Total Investment Income | | | | 6,318,393 | |

| | | | | |

Expenses: | | | | | |

Management fees | | | | 2,175,842 | |

Administration fees | | | | 68,270 | |

Distribution fees | | | | 906,596 | |

Custodian fees | | | | 29,051 | |

Administrative and compliance services fees | | | | 4,606 | |

Transfer agent fees | | | | 5,580 | |

Trustee fees | | | | 18,424 | |

Professional fees | | | | 14,293 | |

Shareholder reports | | | | 4,648 | |

Other expenses | | | | 9,202 | |

| | | | | |

Total expenses before reductions | | | | 3,236,512 | |

Less Management fees contractually waived | | | | (362,636 | ) |

| | | | | |

Net expenses | | | | 2,873,876 | |

| | | | | |

Net Investment Income/(Loss) | | | | 3,444,517 | |

| | | | | |

Net realized and Change in net unrealized gains/losses on investments: | | | | | |

Net realized gains/(losses) on securities and foreign currencies | | | | (28,397,669 | ) |

Net realized gains/(losses) on forward currency contracts | | | | 9,711,677 | |

Change in net unrealized appreciation/depreciation on securities and foreign currencies | | | | (2,409,361 | ) |

Change in net unrealized appreciation/depreciation on forward currency contracts | | | | (10,271,317 | ) |

| | | | | |

Net realized and Change in net unrealized gains/losses on investments | | | | (31,366,670 | ) |

| | | | | |

Change in Net Assets Resulting From Operations | | | $ | (27,922,153 | ) |

| | | | | |

See accompanying notes to the financial statements.

10

AZL DFA Five-Year Global Fixed Income Fund

Statements of Changes in Net Assets

| | | | | | | | | | |

| | | For the

Year Ended

December 31, 2022 | | For the

Year Ended

December 31, 2021 |

| | |

Change In Net Assets: | | | | | | | | | | |

Operations: | | | | | | | | | | |

Net investment income/(loss) | | | $ | 3,444,517 | | | | $ | (412,020 | ) |

Net realized gains/(losses) on investments | | | | (18,685,992 | ) | | | | 8,366,939 | |

Change in unrealized appreciation/depreciation on investments | | | | (12,680,678 | ) | | | | (14,804,697 | ) |

| | | | | | | | | | |

Change in net assets resulting from operations | | | | (27,922,153 | ) | | | | (6,849,778 | ) |

| | | | | | | | | | |

Distributions to Shareholders: | | | | | | | | | | |

Distributions | | | | (14,502,305 | ) | | | | — | |

| | | | | | | | | | |

Change in net assets resulting from distributions to shareholders | | | | (14,502,305 | ) | | | | — | |

| | | | | | | | | | |

Capital Transactions: | | | | | | | | | | |

Proceeds from shares issued | | | | 2,555,459 | | | | | 27,868,290 | |

Proceeds from dividends reinvested | | | | 14,502,305 | | | | | — | |

Value of shares redeemed | | | | (64,069,387 | ) | | | | (12,268,944 | ) |

| | | | | | | | | | |

Change in net assets resulting from capital transactions | | | | (47,011,623 | ) | | | | 15,599,346 | |

| | | | | | | | | | |

Change in net assets | | | | (89,436,081 | ) | | | | 8,749,568 | |

Net Assets: | | | | | | | | | | |

Beginning of period | | | | 419,120,420 | | | | | 410,370,852 | |

| | | | | | | | | | |

End of period | | | $ | 329,684,339 | | | | $ | 419,120,420 | |

| | | | | | | | | | |

Share Transactions: | | | | | | | | | | |

Shares issued | �� | | | 290,962 | | | | | 2,894,674 | |

Dividends reinvested | | | | 1,722,364 | | | | | — | |

Shares redeemed | | | | (7,179,059 | ) | | | | (1,276,633 | ) |

| | | | | | | | | | |

Change in shares | | | | (5,165,733 | ) | | | | 1,618,041 | |

| | | | | | | | | | |

See accompanying notes to the financial statements.

11

AZL DFA Five-Year Global Fixed Income Fund

Financial Highlights

(Selected data for a share of beneficial interest outstanding throughout the periods indicated. Does not reflect fees or expenses associated with the separate accounts that invest in the Fund or in any variable annuity contracts or variable life insurance policy for which the Fund serves as an investment vehicle.)

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, |

| | | 2022 | | 2021 | | 2020 | | 2019 | | 2018 |

| | | | | |

Net Asset Value, Beginning of Period | | | $ | 9.49 | | | | $ | 9.65 | | | | $ | 9.82 | | | | $ | 10.06 | | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Investment Activities: | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Investment Income/(Loss) | | | | 0.08 | (a) | | | | (0.01 | )(a) | | | | (0.03 | )(a) | | | | 0.01 | (a) | | | | 0.06 | |

Net Realized and Unrealized Gains/(Losses) on Investments | | | | (0.73 | ) | | | | (0.15 | ) | | | | 0.09 | | | | | 0.34 | | | | | 0.06 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total from Investment Activities | | | | (0.65 | ) | | | | (0.16 | ) | | | | 0.06 | | | | | 0.35 | | | | | 0.12 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Distributions to Shareholders From: | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Investment Income | | | | (0.38 | ) | | | | — | | | | | (0.23 | ) | | | | (0.59 | ) | | | | (0.06 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total Dividends | | | | (0.38 | ) | | | | — | | | | | (0.23 | ) | | | | (0.59 | ) | | | | (0.06 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Period | | | $ | 8.46 | | | | $ | 9.49 | | | | $ | 9.65 | | | | $ | 9.82 | | | | $ | 10.06 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total Return(b) | | | | (6.82 | )% | | | | (1.66 | )% | | | | 0.57 | % | | | | 3.50 | % | | | | 1.17 | % |

Ratios to Average Net Assets/Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Assets, End of Period (000’s) | | | $ | 329,684 | | | | $ | 419,120 | | | | $ | 410,371 | | | | $ | 434,284 | | | | $ | 460,894 | |

Net Investment Income/(Loss) | | | | 0.95 | % | | | | (0.10 | )% | | | | (0.34 | )% | | | | 0.12 | % | | | | 0.45 | % |

Expenses Before Reductions(c) | | | | 0.89 | % | | | | 0.91 | % | | | | 0.93 | % | | | | 0.92 | % | | | | 0.91 | % |

Expenses Net of Reductions | | | | 0.79 | % | | | | 0.81 | % | | | | 0.83 | % | | | | 0.82 | % | | | | 0.81 | % |

Portfolio Turnover Rate | | | | 119 | % | | | | 122 | % | | | | 62 | % | | | | 35 | % | | | | 69 | % |

| (a) | Calculated using the average shares method. |

| (b) | The returns include reinvested dividends and fund level expenses, but exclude insurance contract charges. If these charges were included, the returns would have been lower. |

| (c) | Excludes fee reductions. If such fee reductions had not occurred, the ratios would have been as indicated. |

See accompanying notes to the financial statements.

12

AZL DFA Five-Year Global Fixed Income Fund

Notes to the Financial Statements

December 31, 2022

1. Organization

The Allianz Variable Insurance Products Trust (the “Trust”) was organized as a Delaware statutory trust on July 13, 1999. The Trust is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”) and thus is determined to be an investment company, and follows the investment company accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946 “Financial Services — Investment Companies.” The Trust consists of 20 separate investment portfolios (individually a “Fund,” collectively, the “Funds”), of which one is included in this report, the AZL DFA Five-Year Global Fixed Income Fund (the “Fund”), and 19 are presented in separate reports. The Fund is a diversified series of the Trust.

The Trust is authorized to issue an unlimited number of shares of the Fund without par value. Shares of the Fund are available through the variable annuity contracts and variable life insurance policies offered through the separate accounts of participating insurance companies. Currently, the Fund only offers its shares to separate accounts of Allianz Life Insurance Company of North America and Allianz Life Insurance Company of New York, affiliates of the Trust and the Manager, as defined below.

Under the Trust’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund may enter into contracts with its vendors and others that provide for general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund. However, based on experience, the Fund expects the risk of loss to be remote.

On December 13, 2022, the Board unanimously approved a reorganization whereby the AZL Enhanced Bond Index Fund will acquire all of the assets and liabilities of the Fund and costs related to the reorganization will be paid by the Manager.

2. Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The policies conform with U.S. generally accepted accounting principles (“U.S. GAAP”). The preparation of financial statements requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Security Valuation

The Fund records its investments at fair value. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between willing market participants at the measurement date. The valuation techniques used to determine fair value are further described in Note 4 below.

Investment Transactions and Investment Income

Investment transactions are accounted for on trade date. Net realized gains and losses on investments sold and on foreign currency transactions are recorded on the basis of identified cost. Interest income is recorded on the accrual basis and includes, where applicable, the amortization of premiums or accretion of discounts. Dividend income is recorded on the ex-dividend date except in the case of foreign securities, in which case dividends are recorded as soon as such information becomes available.

Foreign Currency Translation

The accounting records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the current rate of exchange to determine the fair value of investments, assets and liabilities. Purchases and sales of securities, and income and expenses are translated at the prevailing rate of exchange on the respective dates of such transactions. The Fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from fluctuations arising from changes in market prices of securities held. Such fluctuations are included in the net realized and unrealized gain or loss on investments and foreign currencies.

Distributions to Shareholders

Distributions to shareholders are recorded on the ex-dividend date. The Fund distributes its dividends from net investment income and net realized capital gains, if any, on an annual basis. The amount of distributions from net investment income and from net realized gains is determined in accordance with federal income tax regulations, which may differ from U.S. GAAP. These “book/tax” differences are either temporary or permanent in nature. To the extent these differences are permanent in nature (e.g., return of capital, net operating loss, reclassification of certain market discounts, gain/loss, paydowns, and distributions), such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences (e.g., wash sales and differing treatment on certain investments) do not require reclassification. Distributions to shareholders that exceed net investment income and net realized gains for tax purposes are reported as distributions of capital.

Expense Allocation

Expenses directly attributable to the Fund are charged directly to the Fund, while expenses attributable to more than one Fund are allocated among the respective Funds based upon relative net assets or some other reasonable method. Expenses which are attributable to more than one Trust are allocated across the Allianz Variable Insurance Products Trust, Allianz Variable Insurance Products Fund of Funds Trust and AIM ETF Products Trust based upon relative net assets or another reasonable basis. Allianz Investment Management LLC (the “Manager”), serves as the investment manager for the Trust, Allianz Variable Insurance Products Fund of Funds Trust and AIM ETF Products Trust.

This report does not reflect fees or expenses associated with the separate accounts that invest in the Fund or in any variable annuity contracts or variable life insurance policy for which the Fund serves as an investment vehicle.

Securities Lending

To generate additional income, the Fund may lend up to 331⁄3% of its assets pursuant to agreements requiring that the loan be continuously secured by any combination of cash, U.S. government or U.S. government agency securities, equal initially to at least 102% of the fair value plus accrued interest on the securities loaned (105% for foreign securities). The borrower of securities is at all times required to post collateral to the Fund in an amount equal to 100% of the fair value of the securities loaned based on the previous day’s fair value of the securities

13

AZL DFA Five-Year Global Fixed Income Fund

Notes to the Financial Statements

December 31, 2022

loaned, marked-to-market daily. Any collateral shortfalls are adjusted the next business day. The Fund bears all of the gains and losses on such investments. The Fund receives payments from borrowers equivalent to the dividends and interest that would have been earned on securities lent while simultaneously seeking to earn income on the investment of cash collateral received. In extremely low interest rate environments, the broker rebate fee may exceed the interest earned on the cash collateral which would result in a loss to the Fund. The investment of cash collateral deposited by the borrower is subject to inherent market risks such as interest rate risk, credit risk, liquidity risk, and other risks that are present in the market, and as such, the value of these investments may not be sufficient, when liquidated, to repay the borrower when the loaned security is returned. There may be risks of delay in recovery of the securities or even loss of rights in the collateral should the borrower of the securities fail financially. However, loans will be made only to borrowers, such as broker-dealers, banks or institutional borrowers of securities, deemed by the Manager to be of good standing and credit worthy and when in its judgment, the consideration which can be earned currently from such securities loans justifies the attendant risks. Loans are subject to termination by the Trust or the borrower at any time, and are, therefore, not considered to be illiquid investments. Securities on loan at December 31, 2022 are presented on the Fund’s Schedule of Portfolio Investments.

Cash collateral received in connection with securities lending is invested on behalf of the Fund in the BlackRock Liquidity FedFund, Institutional Class, a money market fund which invests in short-term investments that have a remaining maturity of 397 days or less in accordance with Rule 2a-7 under the 1940 Act. The Fund pays the securities lending agent 9% of the gross revenues received from securities lending activities and keeps 91%. The Fund paid securities lending fees of $342 during the year ended December 31, 2022. These fees have been netted against “Income from securities lending” on the Statement of Operations. The Fund did not have securities lending transactions accounted for as secured borrowings with cash collateral of overnight and continuous maturities as of December 31, 2022. At December 31, 2022, there were no master netting provisions in the securities lending agreement.

Affiliated Securities Transactions

Pursuant to Rule 17a-7 under the 1940 Act, the Fund may engage in securities transactions with affiliated investment companies and advisory accounts managed by the Manager and Subadviser. Any such purchase or sale transaction must be effected without a brokerage commission or other remuneration, except for customary transfer fees. The transaction must be effected at the current market price, which is either the security’s last sale price on an exchange or, if there are no transactions in the security that day, at the average of the highest bid and lowest asked price. During the year ended December 31, 2022, the Fund did not engage in any Rule 17a-7 transactions.

Derivative Instruments

All open derivative positions at period end are reflected on the Fund’s Schedule of Portfolio Investments. The following is a description of the derivative instruments utilized by the Fund, including the primary underlying risk exposures related to each instrument type.

Forward Currency Contracts

During the year ended December 31, 2022, the Fund entered into forward currency contracts in connections with planned purchases or sales of securities or to hedge the U.S. dollar value of securities denominated in a particular currency. In addition to the foreign currency risk related to the use of these contracts, the Fund could be exposed to risks if the counterparties to the contracts are unable to meet the terms of their contracts and from unanticipated movements in the value of a foreign currency relative to the U.S. dollar. In the event of default by the counterparty to the transaction, the Fund’s maximum amount of loss, as either the buyer or the seller, is the unrealized appreciation of the contract. The forward currency contracts are adjusted by the daily exchange rate of the underlying currency and any gains or losses are recorded for financial statement purposes as unrealized gains or losses until the contract settlement date. When the contract is closed, the Fund records a realized gain or loss equal to the difference between the value at the time it was opened and the value at the time it was closed. For the year ended December 31, 2022, the monthly average notional amount for long contracts was $4.6 million and the monthly average notional amount for short contracts was $115.3 million. Realized gains and losses are reported as “Net realized gains/(losses) on forward currency contracts” on the Statement of Operations.

Summary of Derivative Instruments

The following is a summary of the values of derivative instruments on the Fund’s Statement of Assets and Liabilities, categorized by risk exposure, as of December 31, 2022:

| | | | | | | | | | | | |

| | | Asset Derivatives | | | Liability Derivatives | |

| Primary Risk Exposure | | Statement of Assets and Liabilities Location | | Total

Value | | | Statement of Assets and Liabilities Location | | Total

Value | |

| | | |

Foreign Exchange Risk | | | | | | | | | | |

| | | | |

| Forward Currency Contracts | | Unrealized appreciation on forward currency contracts | | $ | 314,448 | | | Unrealized depreciation on forward currency contracts | | $ | 10,744,575 | |

The following is a summary of the effect of derivative instruments on the Statement of Operations, categorized by risk exposure, for the year ended December 31, 2022:

| | | | | | | | | | |

| Primary Risk Exposure | | Location of Gains/(Losses) on Derivatives Recognized | | Realized Gains/(Losses)

on Derivatives

Recognized | | | Change in Net Unrealized

Appreciation/Depreciation on

Derivatives Recognized | |

| | |

Foreign Exchange Risk | | | | | | | | |

| | | |

| Forward Currency Contracts | | Net realized gains/(losses) on forward currency contracts/ Change in net unrealized appreciation/depreciation on forward currency contracts | | $ | 9,711,677 | | | $ | (10,271,317 | ) |

The Fund is generally subject to master netting agreements that allow for amounts owed between the Fund and the counterparty to be netted. The party that has the larger payable pays the excess of the larger amount over the smaller amount to the other party. The master netting agreements do not apply to amounts owed to/from different counterparties. The amounts shown in the Statement of Assets and Liabilities do not take into consideration the effects of legally enforceable master netting agreements. The table below presents the gross and net amounts of these assets and liabilities with any offsets to reflect the Fund’s ability to transact net amounts in accordance with the master netting agreements at December 31, 2022. For financial reporting purposes, the Fund does not offset derivative assets and derivative liabilities that are subject to master netting arrangements in the Statement of Assets and Liabilities. This table also summarizes the fair values of derivative instruments on the Fund’s Statement of Assets and Liabilities, categorized by risk exposure, as of December 31, 2022.

14

AZL DFA Five-Year Global Fixed Income Fund

Notes to the Financial Statements

December 31, 2022

As of December 31, 2022, the Fund’s derivative assets and liabilities by type were as follows:

| | | | | | | | | | |

| | | Assets | | Liabilities |

| | |