The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Filed Pursuant to Rule 424(b)(2)

Registration Statement Nos. 333-273353

333-273353-01

SUBJECT TO COMPLETION. DATED DECEMBER 12, 2024

PRICING SUPPLEMENT TO THE PROSPECTUS DATED JULY 20, 2023 AND THE

PRODUCT PROSPECTUS SUPPLEMENT DATED FEBRUARY 29, 2024

US$

Nomura America Finance, LLC

Senior Global Medium-Term Notes, Series A

Fully and Unconditionally Guaranteed by Nomura Holdings, Inc.

Capped Leveraged Barrier Notes Linked to the Class A Common Stock of Reddit, Inc. due December 30, 2025

| · | Nomura America Finance, LLC is offering the capped leveraged barrier notes linked to the Class A common stock of Reddit, Inc. (the “reference asset”) due December 30, 2025 (the “notes”) described below. The notes are unsecured securities. All payments on the notes are subject to our credit risk and that of the guarantor of the notes, Nomura Holdings, Inc. |

| · | 2x exposure to any positive return of the reference asset, subject to a cap of at least 52.00% (to be determined on the trade date) |

| · | If the reference asset declines by more than 50.00%, 1-to-1 downside exposure to any decrease in the closing value of the reference asset. |

| · | Approximately a one year maturity |

| · | The notes will not be listed on any securities exchange. |

| · | The notes are not ordinary debt securities, and you should carefully consider whether the notes are suited to your particular circumstances. |

Investing in the notes involves significant risks, including our and Nomura’s credit risk. You should carefully consider the risk factors under “Additional Risk Factors Specific to Your Notes” beginning on page PS-5 of this pricing supplement, under “Risk Factors” beginning on page 6 in the accompanying prospectus, under “Additional Risk Factors Specific to the Notes” beginning on page PS-18 of the accompanying product prospectus supplement, and any risk factors incorporated by reference into the accompanying prospectus before you invest in the notes.

The estimated value of your notes at the time the terms of your notes are set on the trade date (as determined by reference to pricing models used by Nomura Securities International, Inc.) is expected to be between $910.00 and $960.00 per $1,000 principal amount, which is expected to be less than the price to public.

We expect delivery of the notes will be made against payment therefor on or about the original issue date specified below.

The notes will be our unsecured obligations. We are not a bank, and the notes will not constitute deposits insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency or instrumentality.

| Price to Public | Agent’s Commission | Proceeds to Issuer | |

| Per Note | 100.00% | Up to 1.25% | At least 98.75% |

| Total | $ | $ | $ |

Nomura Securities International, Inc., acting as the distribution agent, will purchase the notes from us at the price to the public less the agent’s commission. The price to public, agent’s commission and proceeds to issuer listed above relate to the notes we sell initially. We may decide to sell additional notes after the trade date but prior to the original issue date, at a price to public, agent’s commission and proceeds to issuer that differ from the amounts set forth above, but the agent’s commission will not exceed the amount set forth above and the proceeds to issuer will not be less than the amount set forth above. Certain dealers who purchase the notes for sale to certain fee-based advisory accounts may forgo some or all of their selling concessions, fees or commissions.

We will use this pricing supplement in the initial sale of the notes. In addition, Nomura Securities International, Inc. or another of our affiliates may use the final pricing supplement in market-making transactions in the notes after their initial sale. Unless we or our agent informs the purchaser otherwise in the confirmation of sale, the final pricing supplement is being used in a market-making transaction.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this pricing supplement. Any representation to the contrary is a criminal offense.

Nomura

December , 2024

PS-1

| TERMS OF THE NOTES | |

| Issuer: | Nomura America Finance, LLC (“we” or “us”) |

| Guarantor: | Nomura Holdings, Inc. (“Nomura”) |

| Principal Amount: | US$ |

| Reference Asset: | The Class A common stock of Reddit, Inc. (Ticker: RDDT). |

| Trade Date: | December 17, 2024 |

| Original Issue Date: | December 20, 2024 (expected to be the third scheduled business day after the trade date) |

| Final Valuation Date: | December 24, 2025, subject to postponement as described under “General Terms of the Notes—Market Disruption Events” in the accompanying product prospectus supplement. |

| Stated Maturity Date: | December 30, 2025, unless that date is not a business day, in which case the maturity date will be the next following business day. The actual maturity date for the notes may be different if postponed as described under “General Terms of the Notes—Market Disruption Events” in the accompanying product prospectus supplement. |

| Cap: | At least 52.00% (to be determined on the trade date) |

| Upside Participation Rate: | 200.00% (2x) |

| Payment at Maturity: | At maturity, for each $1,000 principal amount of notes, we will pay you a cash payment equal to the cash settlement amount. |

| Cash Settlement Amount: | If the final value is greater than the initial value, the lesser of:

(a) $1,000 + ($1,000 × reference asset performance × upside participation rate); and

(b) $1,000 + ($1,000 × cap).

If the final value is less than or equal to the initial value but greater than or equal to the barrier value:

$1,000 (i.e., zero return).

If the final value is less than the barrier value:

$1,000 + ($1,000 × reference asset performance).

Under these circumstances, you will lose 1% of the principal amount of your notes for each percentage point that the final value is below the initial value. If the final value is less than the barrier value, you will lose some or all of your investment. |

| Reference Asset Performance: | The quotient, expressed as a percentage, calculated as follows: final value - initial value initial value |

| Barrier Value: | 50.00% of the initial value. |

| Barrier Percentage: | -50.00% |

| Initial Value: | The closing value of the reference asset on the trade date, subject to adjustment as described under “General Terms of the Notes — Anti-Dilution Adjustments” in the product |

PS-2

| prospectus supplement. | |

| Final Value: | The closing value of the reference asset on the final valuation date. |

| Denominations: | $1,000 and integral multiples thereof |

| Defeasance: | Not applicable |

| Program: | Senior Global Medium-Term Notes, Series A |

| CUSIP No.: | 65541KAN4 |

| ISIN No.: | US65541KAN46 |

| Currency: | U.S. dollars |

| Calculation Agent: | Nomura Securities International, Inc. |

| Trustee, Paying Agent and Transfer Agent: | Deutsche Bank Trust Company Americas |

| Clearance and Settlement: | The Depository Trust Company (“DTC”) (including through its indirect participants Euroclear and Clearstream, as described under “Legal Ownership and Book-Entry Issuance” in the accompanying prospectus) |

| Minimum Initial Investment Amount: | $1,000 |

| Original Issue Price (Price to Public): | 100.00% |

| Listing: | The notes will not be listed on any securities exchange |

| Distribution Agent: | Nomura Securities International, Inc. |

The trade date and the other dates set forth above are subject to change, and will be set forth in the final pricing supplement relating to the notes.

PS-3

ADDITIONAL INFORMATION

You should read this pricing supplement together with the prospectus, dated July 20, 2023 (the “prospectus”), and the product prospectus supplement, dated February 29, 2024 (the “product prospectus supplement”), relating to our Senior Global Medium-Term Notes, Series A, of which these notes are a part. In the event of any conflict between the terms of this pricing supplement and the terms of the prospectus or the product prospectus supplement, the terms of this pricing supplement will control.

This pricing supplement, together with the prospectus and the product prospectus supplement, contains the terms of the notes. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the accompanying prospectus under “Additional Risk Factors Specific to the Notes” in the accompanying product prospectus supplement, and under “Additional Risk Factors Specific to Your Notes” beginning on page PS-5 of this pricing supplement. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the notes.

We have not authorized anyone to provide any information or to make any representations other than those contained or incorporated by reference in this pricing supplement. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may provide. This pricing supplement is an offer to sell only the securities offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this pricing supplement is current only as of its date.

You may access the prospectus and the product prospectus supplement on the SEC website at www.sec.gov as follows:

· Prospectus dated July 20, 2023:

https://www.sec.gov/Archives/edgar/data/1383951/000110465923082805/tm2320650-3_424b3.htm

· Product Prospectus Supplement dated February 29, 2024:

https://www.sec.gov/Archives/edgar/data/1163653/000110465924029404/tm247408-1_424b3.htm

PS-4

ADDITIONAL RISK FACTORS SPECIFIC TO YOUR NOTES

An investment in the notes is subject to the risks described below, as well as the risks described under “Risk Factors” in the accompanying prospectus and under “Additional Risk Factors Specific to the Notes” in the accompanying product prospectus supplement. You should carefully consider whether the notes are suited to your particular circumstances. The notes are not secured debt.

Please note that in this section entitled “Additional Risk Factors Specific to Your Notes,” references to “holders” mean those who own notes registered in their own names, on the books that we, Nomura or the trustee maintain for this purpose, and not those who own beneficial interests in notes registered in street name or in notes issued in book-entry form through DTC or another depositary. Owners of beneficial interests in the notes should read the section entitled “Legal Ownership and Book-Entry Issuance” in the accompanying prospectus.

We urge you to read all of the following information about some of the risks associated with the notes, together with the other information in this pricing supplement, the accompanying prospectus and the accompanying product prospectus supplement before investing in the notes.

Risks Relating to the Structure or Features of the Notes

Your Investment in the Notes May Result in a Loss.

You will be exposed to the decline in the final value from the initial value if the final value is less than the barrier value. Accordingly, if the reference asset performance is less than the barrier percentage, your payment at maturity will be less than the principal amount of your notes, and may be zero. You will lose some or all of your investment at maturity if the reference asset performance is less than the barrier percentage.

The Amount Payable on The Notes is Not Linked to The Value of The Reference Asset At Any Time Other Than on The Final Valuation Date.

The final value will be based on the closing value of the reference asset on the final valuation date, subject to postponement for non-trading days and certain market disruption events. Even if the value of the reference asset appreciates during the term of the notes other than on the final valuation date but then decreases on the final valuation date to a value that is less than the initial value, the payment at maturity may be less, and may be significantly less, than it would have been had the payment at maturity been linked to the value of the reference asset prior to such decrease. Although the actual value of the reference asset on the stated maturity date or at other times during the term of the notes may be higher than the final value, the payment at maturity will be based solely on the closing value of the reference asset on the final valuation date.

The Return on The Notes is Limited By The Cap.

You will not participate in any appreciation in the value of the reference asset (as multiplied by the upside participation rate) beyond the cap. You will not receive a return on the notes greater than the cap.

The Notes Will Not Bear Interest.

As a holder of the notes, you will not receive interest payments.

Risks Relating to the Reference Asset

The Reference Asset Has Very Limited Historical Information.

The reference asset began trading on March 21, 2024. Because the reference asset is of recent origin and very limited actual historical performance data exists with respect to it, your investment in the notes may involve a greater risk than investing in securities linked to a reference asset with more established records of performance.

You Will Have Limited Anti-Dilution Protection.

The calculation agent may make adjustments to the initial value of the reference asset for certain events affecting the reference asset. However, the calculation agent will not make an adjustment in response to all events that could affect the reference asset. If an event occurs that does not require the calculation agent to make an adjustment, the value of the notes may be materially and adversely affected. In addition, all determinations and calculations concerning any such adjustment will be made by the calculation agent. You should refer to “General Terms of the Notes—Anti-Dilution Adjustments,” “General Terms of the Notes—Modification of the Reference Asset or Unavailability of the Price or Level of the Reference Asset” and “General Terms of the Notes—Role of Calculation Agent” in the accompanying product prospectus supplement for a description of the items that the calculation agent is responsible for determining.

PS-5

Tax Risks

The Tax Treatment of the Notes Is Uncertain.

Significant aspects of the tax treatment of the notes are uncertain. You should consult your tax advisor about your own tax situation. See “U.S. Federal Income Tax Considerations” in the prospectus and “Supplemental Discussion of U.S. Federal Income Tax Consequences” in this pricing supplement.

General Risk Factors

You Are Subject to Nomura’s Credit Risk, and the Value of Your Notes May Be Adversely Affected by Negative Changes in the Market’s Perception of Nomura’s Creditworthiness.

By purchasing the notes, you are making, in part, a decision about Nomura’s ability to pay you the amounts you are owed pursuant to the terms of your notes. Substantially all of our assets consist of loans to and other receivables from Nomura and its subsidiaries. Our obligations under your notes are guaranteed by Nomura. Therefore, as a practical matter, our ability to pay you amounts we owe on the notes is directly or indirectly linked solely to Nomura’s creditworthiness. In addition, the market’s perception of Nomura’s creditworthiness generally will directly impact the value of your notes. If Nomura becomes or is perceived as becoming less creditworthy following your purchase of notes, you should expect that the notes will decline in value in the secondary market, perhaps substantially. If you sell your notes in the secondary market in such an environment, you may incur a substantial loss.

The Estimated Value of Your Notes at the Time the Terms of Your Notes Are Set on the Trade Date (as Determined by Reference to Our Pricing Models) Will Be Less Than the Original Issue Price of Your Notes.

The original issue price for your notes will exceed the estimated value of your notes as of the time the terms of your notes are set on the trade date, as determined by reference to our pricing models. Such estimated value will be set forth on the front cover of the final pricing supplement. After the trade date, the estimated value, as determined by reference to these pricing models, may be affected by changes in market conditions, our and Nomura’s creditworthiness and other relevant factors. If Nomura Securities International, Inc. buys or sells your notes, it will do so at prices that reflect the estimated value determined by reference to such pricing models at that time. The price at which Nomura Securities International, Inc. will buy or sell your notes at any time also will reflect, among other things, its then current bid and ask spread for similar sized trades of structured notes.

In estimating the value of your notes as of the time the terms of your notes are set on the trade date, as will be disclosed on the front cover of the final pricing supplement, our pricing models consider certain variables, including principally Nomura’s internal funding rates, interest rates (forecasted, current and historical rates), volatility, price-sensitivity analysis and the time to maturity of the notes. These pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. In addition, our internal funding rate used in our models generally results in a higher estimated value of your notes than would result if we estimated the value using our credit spreads for our conventional fixed rate debt. As a result, the actual value you would receive if you sold your notes in the secondary market may differ, possibly even materially, from the estimated value of your notes that we will determine by reference to our pricing models as of the time the terms of your notes are set on the trade date due to, among other things, any differences in pricing models, third-parties’ use of our credit spreads in their models, or assumptions used by other market participants.

The difference between the estimated value of your notes as of the time the terms of your notes are set on the trade date and the original issue price is a result of certain factors, including principally the underwriting discount and commissions, the expenses incurred in creating, documenting and marketing the notes, and an estimate of the difference between the amounts we pay to our affiliates and the amounts our affiliates pay to us in connection with their agreement to hedge our obligations on your notes. These costs will be used or retained by us or one of our affiliates, except for underwriting discounts paid to unaffiliated distributors.

If We Were to Repurchase Your Notes Immediately After the Original Issue Date, the Price You Receive May Be Higher Than the Estimated Value of The Notes.

Assuming that all relevant factors remain constant after the original issue date, the price at which we may initially buy or sell the notes in the secondary market, if any, and the value that may initially be used for customer account statements, if any, may exceed the estimated value on the trade date for a temporary period expected to be approximately 1 month after the original issue date. This temporary price difference may exist because, in our discretion, we may elect to effectively reimburse to investors a portion of the estimated cost of hedging our obligations under the notes and other costs in connection with the notes that we will no longer expect to incur over the term of the notes. We will make such discretionary election and determine this temporary reimbursement period on the basis of a number of factors, including the tenor of the

PS-6

notes and any agreement we may have with the distributors of the notes. The amount of our estimated costs which we effectively reimburse to investors in this way may not be allocated ratably throughout the reimbursement period, and we may discontinue such reimbursement at any time or revise the duration of the reimbursement period after the original issue date of the notes based on changes in market conditions and other factors that cannot be predicted.

Because Nomura Is a Holding Company, Your Right to Receive Payments on Nomura’s Guarantee of the Notes Is Subordinated to the Liabilities of Nomura’s Other Subsidiaries.

The ability of Nomura to make payments, as guarantor, on the notes, depends upon Nomura’s receipt of dividends, loan payments and other funds from subsidiaries. In addition, if any of Nomura’s subsidiaries becomes insolvent, the direct creditors of that subsidiary will have a prior claim on its assets, and Nomura’s rights and the rights of Nomura’s creditors, including your rights as an owner of the notes, will be subject to that prior claim.

Nomura’s subsidiaries are subject to various laws and regulations that may restrict Nomura’s ability to receive dividends, loan payments and other funds from subsidiaries. In particular, many of Nomura’s subsidiaries, including its broker-dealer subsidiaries, are subject to laws and regulations, including regulatory capital requirements, that authorize regulatory bodies to block or reduce the flow of funds to the parent holding company, or that prohibit such transfers altogether in certain circumstances. For example, Nomura Securities Co., Ltd., Nomura Securities International, Inc., Nomura International plc and Nomura International (Hong Kong) Limited, Nomura’s main broker-dealer subsidiaries, are subject to regulatory capital requirements that could limit the transfer of funds to Nomura. These laws and regulations may hinder Nomura’s ability to access funds needed to make payments on Nomura’s obligations.

You Must Rely on Your Own Evaluation of the Merits of an Investment Linked to the Reference Asset.

In the ordinary course of business, Nomura or any of its affiliates may have expressed views on expected movements in the reference asset, and may do so in the future. These views or reports may be communicated to Nomura’s clients and clients of its affiliates. However, any such views are and will be subject to change from time to time. Moreover, other professionals who deal in markets relating to the reference asset may at any time have significantly different views from those of Nomura or its affiliates. For these reasons, you are encouraged to derive information concerning the reference asset from multiple sources, and you should not rely on any of the views that may have been expressed or that may be expressed in the future by Nomura or any of its affiliates. Neither the offering of the notes nor any view which Nomura or any of its affiliates from time to time may express in the ordinary course of business constitutes a recommendation as to the merits of an investment in the notes or any of the component securities.

Your Return May Be Lower Than the Return on Other Debt Securities of Comparable Maturity.

The notes do not provide any interest. Consequently, unless the cash settlement amount you receive on the maturity date substantially exceeds the amount you paid for your notes, the overall return you earn on your notes could be less than what you would have earned by investing in non–underlier-linked debt securities that bear interest at prevailing market rates. For example, your return may be less than the return you would earn if you bought a traditional interest-bearing debt security with the same maturity date. Your investment may not reflect the full opportunity cost to you when you take into account factors that affect the time value of money.

The Historical Performance of the Reference Asset Should Not Be Taken as an Indication of Its Future Performance.

The historical prices of the reference asset included in this pricing supplement should not be taken as an indication of its future performance. Changes in the prices of the reference asset will affect the market value of the notes, but it is impossible to predict whether the prices of the reference asset will rise or fall during the term of the notes. The prices of the reference asset will be influenced by complex and interrelated political, economic, financial and other factors.

Our or Our Affiliates’ Hedging and Trading Activities May Adversely Affect the Market Value of the Notes.

As described under “Use of Proceeds and Hedging” in the accompanying product prospectus supplement, we or one or more of our affiliates may hedge our obligations under the notes by entering into transactions involving purchases of futures and/or other derivative instruments linked to the reference asset. We also expect that we or one or more of our affiliates will adjust these hedges by, among other things, purchasing or selling any of the foregoing, and perhaps other instruments linked to any of the foregoing, at any time and from time to time, and unwind the hedge by selling any of the foregoing on or before the final valuation date for the notes or in connection with the redemption of the notes. Our or our affiliates’ hedging activities may result in our or our affiliates’ receiving a substantial return on these hedging activities even if your investment in the notes results in a loss to you. These hedging activities could adversely affect the prices of the reference asset and, therefore, the market value of the notes and the cash settlement amount payable on the notes.

PS-7

We or one or more of our affiliates may also issue or underwrite other securities or financial or derivative instruments with returns linked or related to changes in the performance of the reference asset. By introducing competing products into the marketplace in this manner, we or one or more of our affiliates could adversely affect the market value of the notes and the cash settlement amount payable on the notes.

We or one or more of our affiliates may also engage in business with the component securities issuers or trading activities related to the component securities, which may present a conflict of interest between us (or our affiliates) and you.

There Are Potential Conflicts of Interest Between You and the Calculation Agent and Between You and Our Other Affiliates.

The calculation agent will make important determinations as to the notes. Among other things, the calculation agent will determine the final value of the reference asset and, in certain circumstances, adjustments to the initial value of the reference asset. We have initially appointed our affiliate, Nomura Securities International, Inc., to act as the calculation agent. We may change the calculation agent after the original issue date without notice to you. For a fuller description of the calculation agent’s role, see “General Terms of the Notes— Role of Calculation Agent” in the accompanying product prospectus supplement. The calculation agent will exercise its judgment when performing its functions and will make any determination required or permitted of it in its sole discretion. For example, the calculation agent may have to determine whether a market disruption event affecting the reference asset has occurred and may also have to determine its closing value in such case. This determination may, in turn, depend on the calculation agent’s judgment whether the event has materially interfered with our ability or the ability of one of our affiliates to unwind our hedge positions. All determinations by the calculation agent are final and binding on you absent manifest error. Since this determination by the calculation agent will affect the cash settlement amount payable on the notes, the calculation agent may have a conflict of interest if it needs to make a determination of this kind, and the cash settlement amount payable on your notes may be adversely affected. In addition, if the calculation agent determines that a market disruption event has occurred on the final valuation date, it can postpone such date, which may have the effect of postponing the maturity date. If this occurs, you will receive the cash settlement amount, if any, after the originally scheduled stated maturity date but will not receive any additional payment or any interest on such postponed cash settlement amount.

We or our affiliates may have other conflicts of interest with holders of the notes. See “Additional Risk Factors Specific to the Notes—Our or Our Affiliates’ Business Activities May Create Conflicts of Interest” in the accompanying product prospectus supplement.

There May Not Be an Active Trading Market for the Notes—Sales in the Secondary Market May Result in Significant Losses.

The notes will not be listed on any securities exchange, and there may be little or no secondary market for the notes. Nomura Securities International, Inc. and other affiliates of ours currently intend to make a market for the notes, although they are not required to do so. Nomura Securities International, Inc. or any other affiliate of ours may stop any such market-making activities at any time. Even if a secondary market for the notes develops, it may not provide significant liquidity and the notes may not trade at prices advantageous to you. We expect that transaction costs in any secondary market would be high. As a result, the difference between bid and ask prices for your notes in any secondary market could be substantial.

Furthermore, if you sell your notes, you will likely be charged a commission for secondary market transactions, or the price will likely reflect a dealer discount.

If you sell your notes before the maturity date, you may have to do so at a substantial discount from the issue price and as a result you may suffer substantial losses.

PS-8

ILLUSTRATIVE EXAMPLES

The following table and examples are provided for illustrative purposes only and are hypothetical. They do not purport to be representative of every possible scenario concerning increases or decreases in the value of the reference asset relative to the initial value. We cannot predict the closing value of the reference asset on the final valuation date. The assumptions we have made in connection with the illustrations set forth below may not reflect actual events. You should not take this illustration or these examples as an indication or assurance of the expected performance of the reference asset or the return on the notes.

The table and examples below illustrate how the cash settlement amount would be calculated with respect to a $1,000 investment in the notes, given a range of hypothetical performances of the reference asset. The hypothetical returns on the notes below are numbers, expressed as percentages, that result from comparing the cash settlement amount per $1,000 principal amount to $1,000. The numbers appearing in the following table and examples may have been rounded for ease of analysis. The following table and examples assume the following. These are not the actual terms of the notes and the notes’ terms may be more or less favorable than those shown in the following table and examples:

| 🞂 | Principal amount: | $1,000 |

| 🞂 | Hypothetical initial value: | $100.00 |

| 🞂 | Upside participation rate: | 200.00% (2.0x) |

| 🞂 | Hypothetical cap: | 52.00% (the actual cap will be at least 52.00%, to be determined on the trade date) |

| 🞂 | Hypothetical barrier value: | $50.00 (50.00% of the hypothetical initial value) |

| Hypothetical Final Value | Hypothetical Reference Asset Performance | Hypothetical Cash Settlement Amount | Hypothetical Return on the Notes |

| $200.00 | 100.00% | $1,520.00 | 52.00% |

| $150.00 | 50.00% | $1,520.00 | 52.00% |

| $126.00 | 26.00% | $1,520.00 | 52.00%(1) |

| $120.00 | 20.00% | $1,400.00 | 40.00% |

| $110.00 | 10.00% | $1,200.00 | 20.00% |

| $105.00 | 5.00% | $1,100.00 | 10.00% |

| $100.00(2) | 0.00% | $1,000.00 | 0.00% |

| $90.00 | -10.00% | $1,000.00 | 0.00% |

| $80.00 | -20.00% | $1,000.00 | 0.00% |

| $70.00 | -30.00% | $1,000.00 | 0.00% |

| $50.00 | -50.00%(3) | $1,000.00 | 0.00% |

| $49.99 | -50.01% | $499.90 | -50.01% |

| $40.00 | -60.00% | $400.00 | -60.00% |

| $30.00 | -70.00% | $300.00 | -70.00% |

| $25.00 | -75.00% | $250.00 | -75.00% |

| $0.00 | -100.00% | $0.00 | -100.00% |

| (1) | The return on the notes will be limited to the hypothetical cap. |

| (2) | The hypothetical initial value of $100 used in these examples has been chosen for illustrative purposes only, and does not represent a likely actual initial value of the reference asset. |

| (3) | This is the barrier percentage. |

PS-9

The following examples indicate how the cash settlement amount would be calculated with respect to a hypothetical $1,000 investment in the notes assuming that the notes are held to maturity.

Example 1: The value of the reference asset increases from the initial value of $100.00 to a final value of $110.00

Because the reference asset performance is positive, and the reference asset performance multiplied by the upside participation rate is less than the hypothetical cap, the final settlement value would be $1,200.00 per $1,000 principal amount, calculated as follows:

$1,000 + ($1,000 × reference asset performance × upside participation rate)

= $1,000 + ($1,000 × 10.00% × 200.00%)

=$1,200.00

Example 1 shows that you will receive the return of your principal investment plus a return equal to the reference asset performance multiplied by the upside participation rate when the reference asset appreciates and such reference asset performance multiplied by the upside participation rate does not exceed the hypothetical cap.

Example 2: the value of the reference asset increases from the initial value of $100.00 to a final value of $130.00.

Because the reference asset performance is positive, and the reference asset performance multiplied by the upside participation rate is greater than the hypothetical cap, the final settlement value would be $1,520.00 per $1,000 principal amount, calculated as follows:

$1,000 + ($1,000 × cap)

= $1,000 + ($1,000 × 52.00%)

= $1,520.00

Example 2 shows that you will receive the return of your principal investment plus a return equal to the hypothetical cap when the reference asset performance is positive, and such reference asset performance multiplied by the upside participation rate exceeds the hypothetical cap.

Example 3: the value of the reference asset decreases from the initial value of $100.00 to a final value of $90.00.

Because the reference asset performance is less than zero but greater than the barrier percentage of -50.00%, the final settlement value would be $1,000.00 per $1,000 principal amount (a zero return).

Example 4: the value of the reference asset decreases from the initial value of $100.00 to a final value of $40.00.

Because the reference asset performance is less than the barrier percentage of -50.00%, the final settlement value would be $400.00 per $1,000 principal amount, calculated as follows:

$1,000 + [$1,000 × reference asset performance]

= $1,000 + [$1,000 × (-60.00%)]

= $400.00

Example 4 shows that you are exposed on a 1-to-1 basis to declines in the value of the reference asset beyond the initial value if the reference asset performance is less than the barrier percentage. You will lose some or all of your investment.

PS-10

THE REFERENCE ASSET

Description of Reddit, Inc.

Reddit, Inc. operates an online forum-based platform. Information filed by the company with the SEC under the Exchange Act can be located by reference to its SEC file number: 001-41983, or its CIK Code: 0001713445. This reference asset trades on the New York Stock Exchange under the symbol “RDDT.”

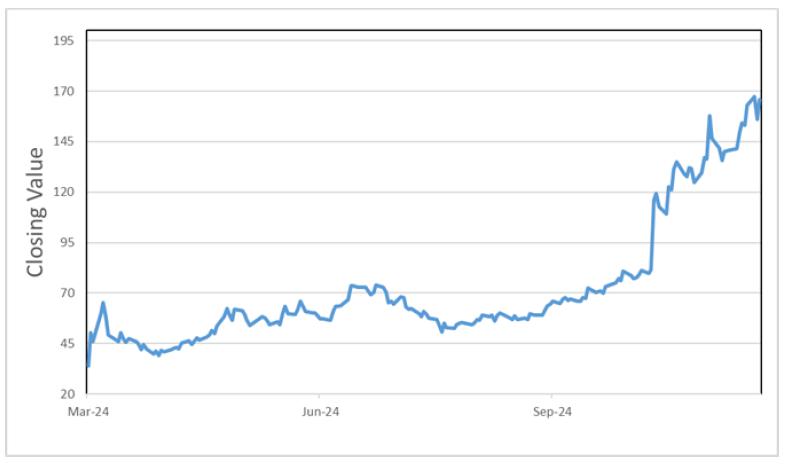

Historical performance of the Class A common stock of Reddit, Inc.

The following graph sets forth the historical performance of the Class A common stock of Reddit, Inc. based on the daily historical closing values from March 21, 2024, the date when this stock began trading, through December 11, 2024. We obtained the closing values below from Bloomberg L.P. (“Bloomberg”). We have not undertaken any independent review of, or made any due diligence inquiry with respect to, the information obtained from Bloomberg.

The historical values of the Class A common stock of Reddit, Inc. should not be taken as an indication of future performance, and no assurance can be given as to the closing value of the Class A common stock of Reddit, Inc. on the final valuation date.

PS-11

SUPPLEMENTAL DISCUSSION OF U.S. FEDERAL INCOME TAX CONSEQUENCES

You should carefully consider the matters set forth in “U.S. Federal Income Tax Considerations” in the accompanying prospectus. The following discussion summarizes the U.S. federal income tax consequences of the purchase, beneficial ownership, and disposition of the notes. This summary supplements the section “U.S. Federal Income Tax Considerations” in the accompanying prospectus and supersedes it to the extent inconsistent therewith.

There is no direct legal authority as to the proper tax treatment of the notes, and therefore significant aspects of the tax treatment of the notes are uncertain as to both the timing and character of any inclusion in income in respect of the notes. Under one approach, a note should be treated as a pre-paid derivative contract with respect to the reference asset. We intend to treat the notes consistent with this approach. Pursuant to the terms of the notes, you agree to treat the notes under this approach for all U.S. federal income tax purposes. Subject to the limitations described therein, and based on certain factual representations received from us, in the opinion of our special U.S. tax counsel, Mayer Brown LLP, it is reasonable to treat a note as a pre-paid derivative contract with respect to the reference asset. Because there are no statutory provisions, regulations, published rulings or judicial decisions addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as those of the notes, other characterizations and treatments are possible and the timing and character of income in respect of the notes might differ from the treatment described herein.

U.S. Holders. Please see the discussion under the heading “U.S. Federal Income Tax Considerations — Tax Treatment of U.S. Holders — Certain Notes Treated as a Put Option and a Deposit or a Derivative Contract — Certain Notes Treated as Prepaid Derivative Contracts” in the accompanying prospectus for a further discussion of U.S. federal income tax considerations applicable to U.S. holders (as defined in the accompanying prospectus). Pursuant to the approach discussed above, we intend to treat any gain or loss upon maturity or an earlier sale, exchange, or call as capital gain or loss in an amount equal to the difference between the amount you receive at such time and your tax basis in the note. Any such gain or loss will be long-term capital gain or loss if you have held the note for more than one year at such time for U.S. federal income tax purposes. Your tax basis in a note generally will equal your cost of the note.

Non-U.S. Holders. Please see the discussion under the heading “U.S. Federal Income Tax Considerations — Tax Treatment of Non-U.S. Holders” in the accompanying prospectus for further discussion of U.S. federal income tax considerations applicable to non-U.S. holders (as defined in the accompanying prospectus).

A “dividend equivalent” payment is treated as a dividend from sources within the United States and such payments generally would be subject to a 30% U.S. withholding tax if paid to a non-U.S. holder. Under U.S. Treasury Department regulations, payments (including deemed payments) with respect to equity-linked instruments (“ELIs”) that are “specified ELIs” may be treated as dividend equivalents if such specified ELIs reference an interest in an “underlying security,” which is generally any interest in an entity taxable as a corporation for U.S. federal income tax purposes if a payment with respect to such interest could give rise to a U.S. source dividend. However, Internal Revenue Service guidance provides that withholding on dividend equivalent payments will not apply to specified ELIs that are not delta-one instruments and that are issued before January 1, 2027. Based on the Issuer’s determination that the notes are not “delta-one” instruments, non-U.S. holders should not be subject to withholding on dividend equivalent payments, if any, under the notes. However, it is possible that the notes could be treated as deemed reissued for U.S. federal income tax purposes upon the occurrence of certain events affecting the reference asset or the notes, and following such occurrence the notes could be treated as subject to withholding on dividend equivalent payments. Non-U.S. holders that enter, or have entered, into other transactions in respect of the reference asset or the notes should consult their tax advisors as to the application of the dividend equivalent withholding tax in the context of the notes and their other transactions. If any payments are treated as dividend equivalents subject to withholding, we (or the applicable paying agent) would be entitled to withhold taxes without being required to pay any additional amounts with respect to amounts so withheld.

PS-12

PROSPECTIVE PURCHASERS OF NOTES SHOULD CONSULT THEIR TAX ADVISORS AS TO THE FEDERAL, STATE, LOCAL, AND OTHER TAX CONSEQUENCES TO THEM OF THE PURCHASE, OWNERSHIP AND DISPOSITION OF NOTES.

PS-13

SUPPLEMENTAL PLAN OF DISTRIBUTION

We will agree to sell to Nomura Securities International, Inc. (the “distribution agent”), and the distribution agent will agree to purchase from us, the aggregate principal amount of the notes specified on the front cover of the final pricing supplement. The distribution agent will agree to purchase the notes from us at least 98.75% of the principal amount. The distribution agent’s commission will be up to 1.25%. The distribution agent will offer the notes to which this pricing supplement relates to the public at the price to public set forth on the front cover of the final pricing supplement and to certain dealers at such price less a concession not in excess of 1.25% of the principal amount of the notes. If all of the notes are not sold at the original issue price, the distribution agent may change the offering price and the other selling terms. Certain dealers who purchase the notes for sale to certain fee-based advisory accounts may forgo some or all of their selling concessions, fees or commissions.

To the extent the distribution agent resells notes to a broker or dealer less a concession equal to the entire underwriting discount, such broker or dealer may be deemed to be an “underwriter” of the notes as such term is defined in the Securities Act of 1933, as amended. If the distribution agent is unable to sell all the notes at the public offering price, the distribution agent proposes to offer the notes from time to time for sale in negotiated transactions or otherwise, at prices to be determined at the time of sale.

In the future, the distribution agent may repurchase and resell the notes in market-making transactions. For more information about the plan of distribution, the distribution agreement and possible market-making activities, see “Plan of Distribution (Conflicts of Interest)” in the accompanying prospectus.

We expect that delivery of the notes will be made against payment for the notes on or about the original issue date set forth on the cover page of this document, which is more than one business day following the trade date. Under Rule 15c6-1 under the Exchange Act, trades in the secondary market generally are required to settle in one business day, unless the parties to that trade expressly agree otherwise. Accordingly, purchasers who wish to trade the notes more than one business day prior to the original issue date will be required to specify an alternate settlement cycle at the time of any such trade to prevent a failed settlement, and should consult their own advisors.

The distribution agent is our affiliate and, as such, has a “conflict of interest” in this offering within the meaning of FINRA Rule 5121. The distribution agent is not permitted to sell notes in this offering to any account over which it exercises discretionary authority without the prior specific written approval of the account holder.

The distribution agent and/or its affiliates have performed, and in the future may provide, investment banking and advisory services for us from time to time for which they have received, and expect to receive, customary fees and commissions. The distribution agent and its affiliates may, from time to time, engage in transactions with, and perform services for, us in the ordinary course of business.

PS-14