UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number

NEW YORK LIFE INVESTMENTS FUNDS TRUST

(Exact name of registrant as specified in charter)

51 Madison Avenue New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

30 Hudson Street

Jersey City, New Jersey 07302

(Name and Address of Agent for Service)

(NYLI MacKay Arizona Muni Fund, NYLI MacKay Colorado Muni Fund,

NYLI MacKay Oregon Muni Fund and NYLI MacKay Utah Muni Fund only)

Registrant's telephone number, including area code:

Date of reporting period:

Item 1. Report to Stockholders.

a.) The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

b.) A copy of the notice transmitted to shareholders in reliance on Rule 30e-3 under the 1940 Act that contains disclosures specified by paragraph (c)(3) of that rule is included in the Annual Report. Not applicable. Notices do not incorporate disclosures from the shareholder reports.

NYLI MacKay Arizona Muni Fund

(formerly known as MainStay MacKay Arizona Muni Fund)

Class A/AZTAX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Arizona Muni Fund (the "Fund") for the period July 22, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the period since inception?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class A | $22^ | 0.80% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | Class A shares commenced operations during the reporting period. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend, was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to 4% coupons bonds, driven by security selection | Contributed |

| Sector | Underweight allocation to state general obligation holdings, primarily due to security selection | Contributed |

| Maturity | Underweight exposure to bonds maturing in 3 to 9 years, as the short end of the curve outperformed the long end | Detracted |

| Credit quality | Underweight exposure to A-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $15,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period and reflects the deduction of all sales charges.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Since

Inception1 |

| Class A Shares - Including sales charges | 7/22/2024 | (2.56)% |

| Class A Shares - Excluding sales charges | | 0.45%) |

| Bloomberg Municipal Bond Index2 | | 0.46)%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.60)%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.20)%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $156,184,420% |

| Total number of portfolio holdings | $90% |

| Total advisory fees paid | $347,145% |

| Portfolio turnover rate | $39% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City of Phoenix Civic Improvement Corp., 4.00%-5.00%, due 7/1/26-7/1/45 | 9.0% |

| Arizona Industrial Development Authority, 2.12%-5.00%, due 1/1/28-2/1/58 | 8.3% |

| Maricopa County Industrial Development Authority, 4.00%-5.00%, due 7/1/33-1/1/53 | 4.9% |

| City of Peoria, 2.00%-3.375%, due 7/15/32-7/15/39 | 4.7% |

| Salt River Project Agricultural Improvement & Power District, 4.00%-5.25%, due 12/1/34-1/1/53 | 4.3% |

| Chandler Industrial Development Authority, 5.00%, due 9/1/52 | 3.8% |

| Maricopa County Pollution Control Corp., 2.40%-3.60%, due 6/1/35-2/1/40 | 3.7% |

| City of Mesa, 4.00%-5.00%, due 7/1/32-7/1/36 | 3.6% |

| Arizona Department of Transportation State Highway Fund, 5.00%, due 7/1/25-7/1/33 | 3.5% |

| Maricopa County Special Health Care District, 5.00%, due 7/1/32-7/1/34 | 3.0% |

| * Excluding short-term investments |

| Other Revenue | 33.1% |

| General Obligation | 29.3% |

| Education | 12.8% |

| Utilities | 6.6% |

| Transportation | 5.8% |

| Hospital | 4.8% |

| Water & Sewer | 1.4% |

| General | 1.2% |

| Housing | 0.5% |

| Short-Term Investment | 2.9% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Arizona Muni Fund” to “NYLI MacKay Arizona Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund.

For more complete information, you may review the Fund’s next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Arizona Muni Fund

(formerly known as MainStay MacKay Arizona Muni Fund)

Class C/AZTCX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Arizona Muni Fund (the "Fund") for the period April 1, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last seven months?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class C | $87^ | 1.48% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | The Fund changed its fiscal and tax year end from March 31 to October 31. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend, was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to 4% coupons bonds, driven by security selection | Contributed |

| Sector | Underweight allocation to state general obligation holdings, primarily due to security selection | Contributed |

| Maturity | Underweight exposure to bonds maturing in 3 to 9 years, as the short end of the curve outperformed the long end | Detracted |

| Credit quality | Underweight exposure to A-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period. Effective July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund's historical performance. Therefore, the performance information shown is that of the Predecessor Fund, which had a different fee structure from the Fund. The returns of the Predecessor Fund have not been adjusted to reflect the applicable expenses of the Fund.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Seven

Months1 | One

Year | Five

Years | Ten

Years |

| Class C Shares - Including sales charges | 4/1/1996 | (0.20)% | 5.52% | (0.45)% | 0.77% |

| Class C Shares - Excluding sales charges | | 0.80%) | 6.52% | (0.45)% | 0.77% |

| Bloomberg Municipal Bond Index2 | | 1.20)%% | 9.70%% | 1.05)%% | 2.30%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.96)%% | 7.53%% | 1.14)%% | 2.06%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.86)%% | 11.82%% | 0.58)%% | 1.69%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $156,184,420% |

| Total number of portfolio holdings | $90% |

| Total advisory fees paid | $347,145% |

| Portfolio turnover rate | $39% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City of Phoenix Civic Improvement Corp., 4.00%-5.00%, due 7/1/26-7/1/45 | 9.0% |

| Arizona Industrial Development Authority, 2.12%-5.00%, due 1/1/28-2/1/58 | 8.3% |

| Maricopa County Industrial Development Authority, 4.00%-5.00%, due 7/1/33-1/1/53 | 4.9% |

| City of Peoria, 2.00%-3.375%, due 7/15/32-7/15/39 | 4.7% |

| Salt River Project Agricultural Improvement & Power District, 4.00%-5.25%, due 12/1/34-1/1/53 | 4.3% |

| Chandler Industrial Development Authority, 5.00%, due 9/1/52 | 3.8% |

| Maricopa County Pollution Control Corp., 2.40%-3.60%, due 6/1/35-2/1/40 | 3.7% |

| City of Mesa, 4.00%-5.00%, due 7/1/32-7/1/36 | 3.6% |

| Arizona Department of Transportation State Highway Fund, 5.00%, due 7/1/25-7/1/33 | 3.5% |

| Maricopa County Special Health Care District, 5.00%, due 7/1/32-7/1/34 | 3.0% |

| * Excluding short-term investments |

| Other Revenue | 33.1% |

| General Obligation | 29.3% |

| Education | 12.8% |

| Utilities | 6.6% |

| Transportation | 5.8% |

| Hospital | 4.8% |

| Water & Sewer | 1.4% |

| General | 1.2% |

| Housing | 0.5% |

| Short-Term Investment | 2.9% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Arizona Muni Fund” to “NYLI MacKay Arizona Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund. The expenses shown above include expenses of the Predecessor Fund, which had a different fee structure from the Fund, from April 1, 2024 through the reorganization.

For more complete information, you may review the Fund’s next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Arizona Muni Fund

(formerly known as MainStay MacKay Arizona Muni Fund)

Class I/AZTYX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Arizona Muni Fund (the "Fund") for the period April 1, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last seven months?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class I | $39^ | 0.67% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | The Fund changed its fiscal and tax year end from March 31 to October 31. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend, was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to 4% coupons bonds, driven by security selection | Contributed |

| Sector | Underweight allocation to state general obligation holdings, primarily due to security selection | Contributed |

| Maturity | Underweight exposure to bonds maturing in 3 to 9 years, as the short end of the curve outperformed the long end | Detracted |

| Credit quality | Underweight exposure to A-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period. Effective July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund's historical performance. Therefore, the performance information shown is that of the Predecessor Fund, which had a different fee structure from the Fund. The returns of the Predecessor Fund have not been adjusted to reflect the applicable expenses of the Fund.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Seven

Months1 | One

Year | Five

Years | Ten

Years |

| Class I Shares | 4/1/1996 | 1.25% | 7.43% | 0.51% | 1.77% |

| Bloomberg Municipal Bond Index2 | | 1.20%% | 9.70%% | 1.05%% | 2.30%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.96%% | 7.53%% | 1.14%% | 2.06%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.86%% | 11.82%% | 0.58%% | 1.69%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $156,184,420% |

| Total number of portfolio holdings | $90% |

| Total advisory fees paid | $347,145% |

| Portfolio turnover rate | $39% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City of Phoenix Civic Improvement Corp., 4.00%-5.00%, due 7/1/26-7/1/45 | 9.0% |

| Arizona Industrial Development Authority, 2.12%-5.00%, due 1/1/28-2/1/58 | 8.3% |

| Maricopa County Industrial Development Authority, 4.00%-5.00%, due 7/1/33-1/1/53 | 4.9% |

| City of Peoria, 2.00%-3.375%, due 7/15/32-7/15/39 | 4.7% |

| Salt River Project Agricultural Improvement & Power District, 4.00%-5.25%, due 12/1/34-1/1/53 | 4.3% |

| Chandler Industrial Development Authority, 5.00%, due 9/1/52 | 3.8% |

| Maricopa County Pollution Control Corp., 2.40%-3.60%, due 6/1/35-2/1/40 | 3.7% |

| City of Mesa, 4.00%-5.00%, due 7/1/32-7/1/36 | 3.6% |

| Arizona Department of Transportation State Highway Fund, 5.00%, due 7/1/25-7/1/33 | 3.5% |

| Maricopa County Special Health Care District, 5.00%, due 7/1/32-7/1/34 | 3.0% |

| * Excluding short-term investments |

| Other Revenue | 33.1% |

| General Obligation | 29.3% |

| Education | 12.8% |

| Utilities | 6.6% |

| Transportation | 5.8% |

| Hospital | 4.8% |

| Water & Sewer | 1.4% |

| General | 1.2% |

| Housing | 0.5% |

| Short-Term Investment | 2.9% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Arizona Muni Fund” to “NYLI MacKay Arizona Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund. The expenses shown above include expenses of the Predecessor Fund, which had a different fee structure from the Fund, from April 1, 2024 through the reorganization.

For more complete information, you may review the Fund’s next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Arizona Muni Fund

(formerly known as MainStay MacKay Arizona Muni Fund)

Class Z/AZTFX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Arizona Muni Fund (the "Fund") for the period April 1, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last seven months?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class Z | $49^ | 0.84% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | The Fund changed its fiscal and tax year end from March 31 to October 31. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend, was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to 4% coupons bonds, driven by security selection | Contributed |

| Sector | Underweight allocation to state general obligation holdings, primarily due to security selection | Contributed |

| Maturity | Underweight exposure to bonds maturing in 3 to 9 years, as the short end of the curve outperformed the long end | Detracted |

| Credit quality | Underweight exposure to A-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period and reflects the deduction of all sales charges. Effective July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund's historical performance. Therefore, the performance information shown is that of the Predecessor Fund, which had a different fee structure from the Fund. The returns of the Predecessor Fund have not been adjusted to reflect the applicable expenses of the Fund.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Seven

Months1 | One

Year | Five

Years | Ten

Years |

| Class Z Shares - Including sales charges | 3/13/1986 | (1.88)% | 4.05% | (0.23)% | 1.31% |

| Class Z Shares - Excluding sales charges | | 1.15%) | 7.26% | 0.38%) | 1.62% |

| Bloomberg Municipal Bond Index2 | | 1.20)%% | 9.70%% | 1.05)%% | 2.30%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.96)%% | 7.53%% | 1.14)%% | 2.06%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.86)%% | 11.82%% | 0.58)%% | 1.69%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $156,184,420% |

| Total number of portfolio holdings | $90% |

| Total advisory fees paid | $347,145% |

| Portfolio turnover rate | $39% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City of Phoenix Civic Improvement Corp., 4.00%-5.00%, due 7/1/26-7/1/45 | 9.0% |

| Arizona Industrial Development Authority, 2.12%-5.00%, due 1/1/28-2/1/58 | 8.3% |

| Maricopa County Industrial Development Authority, 4.00%-5.00%, due 7/1/33-1/1/53 | 4.9% |

| City of Peoria, 2.00%-3.375%, due 7/15/32-7/15/39 | 4.7% |

| Salt River Project Agricultural Improvement & Power District, 4.00%-5.25%, due 12/1/34-1/1/53 | 4.3% |

| Chandler Industrial Development Authority, 5.00%, due 9/1/52 | 3.8% |

| Maricopa County Pollution Control Corp., 2.40%-3.60%, due 6/1/35-2/1/40 | 3.7% |

| City of Mesa, 4.00%-5.00%, due 7/1/32-7/1/36 | 3.6% |

| Arizona Department of Transportation State Highway Fund, 5.00%, due 7/1/25-7/1/33 | 3.5% |

| Maricopa County Special Health Care District, 5.00%, due 7/1/32-7/1/34 | 3.0% |

| * Excluding short-term investments |

| Other Revenue | 33.1% |

| General Obligation | 29.3% |

| Education | 12.8% |

| Utilities | 6.6% |

| Transportation | 5.8% |

| Hospital | 4.8% |

| Water & Sewer | 1.4% |

| General | 1.2% |

| Housing | 0.5% |

| Short-Term Investment | 2.9% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Arizona Muni Fund” to “NYLI MacKay Arizona Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Trust of Arizona (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund. The expenses shown above include expenses of the Predecessor Fund, which had a different fee structure from the Fund, from April 1, 2024 through the reorganization.

For more complete information, you may review the Fund’s next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Colorado Muni Fund

(formerly known as MainStay MacKay Colorado Muni Fund)

Class A/COTAX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Colorado Muni Fund (the "Fund") for the period July 22, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the period since inception?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class A | $22^ | 0.80% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | Class A shares commenced operations during the reporting period. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to zero coupon bonds driven by security selection | Contributed |

| Maturity | Overweight exposure to bonds maturing inside of 3 years, as the short end of the curve outperformed the long end | Contributed |

| Sector | Underweight allocation to water & sewer bonds, driven by security selection | Detracted |

| Credit rating | Overweight allocation to AA-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $15,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period and reflects the deduction of all sales charges.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Since

Inception1 |

| Class A Shares - Including sales charges | 7/22/2024 | (2.63)% |

| Class A Shares - Excluding sales charges | | 0.39%) |

| Bloomberg Municipal Bond Index2 | | 0.46)%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.60)%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.20)%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $118,523,100% |

| Total number of portfolio holdings | $85% |

| Total advisory fees paid | $316,009% |

| Portfolio turnover rate | $33% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City & County of Denver, 4.00%-5.00%, due 6/1/30-8/1/42 | 8.5% |

| Colorado Housing and Finance Authority, 3.75%-4.60%, due 10/1/39-5/1/50 | 6.3% |

| Larimer Weld & Boulder County School District R-2J, 4.25%-5.00%, due 12/15/24-12/15/35 | 4.9% |

| Adams & Weld Counties School District No. 27J, 5.00%, due 12/1/24-12/1/42 | 4.7% |

| Colorado Health Facilities Authority, 4.00%-5.00%, due 11/1/28-5/15/45 | 4.3% |

| City of Colorado Springs, 5.00%, due 11/15/34-11/15/39 | 3.8% |

| Colorado Educational & Cultural Facilities Authority, 4.00%-5.25%, due 3/1/26-7/1/44 | 2.8% |

| City of Grand Junction, 5.00%, due 3/1/41-12/1/43 | 2.5% |

| Foothills Park & Recreation District, 4.00%-5.00%, due 12/1/26-12/1/35 | 2.4% |

| Southeast Colorado Hospital District, 5.00%, due 2/1/25 | 2.3% |

| * Excluding short-term investments |

| General Obligation | 30.1% |

| Other Revenue | 26.0% |

| Certificate of Participation/Lease | 12.8% |

| Hospital | 7.3% |

| Transportation | 6.2% |

| Water & Sewer | 6.1% |

| Education | 5.2% |

| Short-Term Investment | 3.0% |

| Other Assets, Less Liabilities | 3.3% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Colorado Muni Fund” to “NYLI MacKay Colorado Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Colorado Muni Fund

(formerly known as MainStay MacKay Colorado Muni Fund)

Class C/COTCX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Colorado Muni Fund (the "Fund") for the period April 1, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last seven months?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class C | $90^ | 1.54% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | The Fund changed its fiscal and tax year end from March 31 to October 31. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to zero coupon bonds driven by security selection | Contributed |

| Maturity | Overweight exposure to bonds maturing inside of 3 years, as the short end of the curve outperformed the long end | Contributed |

| Sector | Underweight allocation to water & sewer bonds, driven by security selection | Detracted |

| Credit rating | Overweight allocation to AA-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period. Effective July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund's historical performance. Therefore, the performance information shown is that of the Predecessor Fund, which had a different fee structure from the Fund. The returns of the Predecessor Fund have not been adjusted to reflect the applicable expenses of the Fund.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Seven

Months1 | One

Year | Five

Years | Ten

Years |

| Class C Shares - Including sales charges | 4/30/1996 | (0.63)% | 3.97% | (0.65)% | 0.35% |

| Class C Shares - Excluding sales charges | | 0.36%) | 4.97% | (0.65)% | 0.35% |

| Bloomberg Municipal Bond Index2 | | 1.20)%% | 9.70%% | 1.05)%% | 2.30%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.96)%% | 7.53%% | 1.14)%% | 2.06%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.86)%% | 11.82%% | 0.58)%% | 1.69%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $118,523,100% |

| Total number of portfolio holdings | $85% |

| Total advisory fees paid | $316,009% |

| Portfolio turnover rate | $33% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City & County of Denver, 4.00%-5.00%, due 6/1/30-8/1/42 | 8.5% |

| Colorado Housing and Finance Authority, 3.75%-4.60%, due 10/1/39-5/1/50 | 6.3% |

| Larimer Weld & Boulder County School District R-2J, 4.25%-5.00%, due 12/15/24-12/15/35 | 4.9% |

| Adams & Weld Counties School District No. 27J, 5.00%, due 12/1/24-12/1/42 | 4.7% |

| Colorado Health Facilities Authority, 4.00%-5.00%, due 11/1/28-5/15/45 | 4.3% |

| City of Colorado Springs, 5.00%, due 11/15/34-11/15/39 | 3.8% |

| Colorado Educational & Cultural Facilities Authority, 4.00%-5.25%, due 3/1/26-7/1/44 | 2.8% |

| City of Grand Junction, 5.00%, due 3/1/41-12/1/43 | 2.5% |

| Foothills Park & Recreation District, 4.00%-5.00%, due 12/1/26-12/1/35 | 2.4% |

| Southeast Colorado Hospital District, 5.00%, due 2/1/25 | 2.3% |

| * Excluding short-term investments |

| General Obligation | 30.1% |

| Other Revenue | 26.0% |

| Certificate of Participation/Lease | 12.8% |

| Hospital | 7.3% |

| Transportation | 6.2% |

| Water & Sewer | 6.1% |

| Education | 5.2% |

| Short-Term Investment | 3.0% |

| Other Assets, Less Liabilities | 3.3% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Colorado Muni Fund” to “NYLI MacKay Colorado Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund. The expenses shown above include expenses of the Predecessor Fund, which had a different fee structure from the Fund, from April 1, 2024 through the reorganization.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Colorado Muni Fund

(formerly known as MainStay MacKay Colorado Muni Fund)

Class I/COTYX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Colorado Muni Fund (the "Fund") for the period April 1, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last seven months?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class I | $43^ | 0.73% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | The Fund changed its fiscal and tax year end from March 31 to October 31. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to zero coupon bonds driven by security selection | Contributed |

| Maturity | Overweight exposure to bonds maturing inside of 3 years, as the short end of the curve outperformed the long end | Contributed |

| Sector | Underweight allocation to water & sewer bonds, driven by security selection | Detracted |

| Credit rating | Overweight allocation to AA-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period. Effective July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund's historical performance. Therefore, the performance information shown is that of the Predecessor Fund, which had a different fee structure from the Fund. The returns of the Predecessor Fund have not been adjusted to reflect the applicable expenses of the Fund.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Seven

Months1 | One

Year | Five

Years | Ten

Years |

| Class I Shares | 4/30/1996 | 0.82% | 5.98% | 0.33% | 1.36% |

| Bloomberg Municipal Bond Index2 | | 1.20%% | 9.70%% | 1.05%% | 2.30%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.96%% | 7.53%% | 1.14%% | 2.06%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.86%% | 11.82%% | 0.58%% | 1.69%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $118,523,100% |

| Total number of portfolio holdings | $85% |

| Total advisory fees paid | $316,009% |

| Portfolio turnover rate | $33% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City & County of Denver, 4.00%-5.00%, due 6/1/30-8/1/42 | 8.5% |

| Colorado Housing and Finance Authority, 3.75%-4.60%, due 10/1/39-5/1/50 | 6.3% |

| Larimer Weld & Boulder County School District R-2J, 4.25%-5.00%, due 12/15/24-12/15/35 | 4.9% |

| Adams & Weld Counties School District No. 27J, 5.00%, due 12/1/24-12/1/42 | 4.7% |

| Colorado Health Facilities Authority, 4.00%-5.00%, due 11/1/28-5/15/45 | 4.3% |

| City of Colorado Springs, 5.00%, due 11/15/34-11/15/39 | 3.8% |

| Colorado Educational & Cultural Facilities Authority, 4.00%-5.25%, due 3/1/26-7/1/44 | 2.8% |

| City of Grand Junction, 5.00%, due 3/1/41-12/1/43 | 2.5% |

| Foothills Park & Recreation District, 4.00%-5.00%, due 12/1/26-12/1/35 | 2.4% |

| Southeast Colorado Hospital District, 5.00%, due 2/1/25 | 2.3% |

| * Excluding short-term investments |

| General Obligation | 30.1% |

| Other Revenue | 26.0% |

| Certificate of Participation/Lease | 12.8% |

| Hospital | 7.3% |

| Transportation | 6.2% |

| Water & Sewer | 6.1% |

| Education | 5.2% |

| Short-Term Investment | 3.0% |

| Other Assets, Less Liabilities | 3.3% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Colorado Muni Fund” to “NYLI MacKay Colorado Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund. The expenses shown above include expenses of the Predecessor Fund, which had a different fee structure from the Fund, from April 1, 2024 through the reorganization.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Colorado Muni Fund

(formerly known as MainStay MacKay Colorado Muni Fund)

Class Z/COTFX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Colorado Muni Fund (the "Fund") for the period April 1, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the last seven months?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class Z | $51^ | 0.87% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | The Fund changed its fiscal and tax year end from March 31 to October 31. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond Index 1-15 Yr Blend was primarily driven by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Exposure to zero coupon bonds driven by security selection | Contributed |

| Maturity | Overweight exposure to bonds maturing inside of 3 years, as the short end of the curve outperformed the long end | Contributed |

| Sector | Underweight allocation to water & sewer bonds, driven by security selection | Detracted |

| Credit rating | Overweight allocation to AA-rated credits, primarily due yield curve positioning | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $10,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period and reflects the deduction of all sales charges. Effective July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund. As accounting successor to the Predecessor Fund, the Fund has assumed the Predecessor Fund's historical performance. Therefore, the performance information shown is that of the Predecessor Fund, which had a different fee structure from the Fund. The returns of the Predecessor Fund have not been adjusted to reflect the applicable expenses of the Fund.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Seven

Months1 | One

Year | Five

Years | Ten

Years |

| Class Z Shares - Including sales charges | 5/21/1987 | (2.28)% | 2.71% | (0.33)% | 0.99% |

| Class Z Shares - Excluding sales charges | | 0.74%) | 5.88% | 0.28%) | 1.30% |

| Bloomberg Municipal Bond Index2 | | 1.20)%% | 9.70%% | 1.05)%% | 2.30%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.96)%% | 7.53%% | 1.14)%% | 2.06%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.86)%% | 11.82%% | 0.58)%% | 1.69%% |

| 1. | Not annualized. |

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |

| 3. | The Bloomberg Municipal Bond Index 1-15 Yr Blend, which is generally representative of the market sectors or types of investments in which the Fund invests, covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

| 4. | The Morningstar Muni Single State Intermediate Category Average is representative of funds that invest in bonds issued by state and local governments to fund public projects. The income from such bonds is generally free from federal taxes and from state taxes in the issuing state. To get the state-tax benefit, these funds buy bonds from only one state. These funds have durations of 4.0 to 6.0 years (or average maturities of five to 12 years). Results are based on average total returns of similar funds with all dividends and capital gain distributions reinvested. |

Keep in mind that the Fund ’s past performance is not a good predictor of how the Fund will perform in the future.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit newyorklifeinvestments.com/funds for the most recent performance information.

| Fund's net assets | $118,523,100% |

| Total number of portfolio holdings | $85% |

| Total advisory fees paid | $316,009% |

| Portfolio turnover rate | $33% |

Graphical Representation of Holdings

The tables below show the investment makeup of the Fund; percentages indicated are based on the Fund's net assets.

Top Ten Holdings and/or Issuers*

| City & County of Denver, 4.00%-5.00%, due 6/1/30-8/1/42 | 8.5% |

| Colorado Housing and Finance Authority, 3.75%-4.60%, due 10/1/39-5/1/50 | 6.3% |

| Larimer Weld & Boulder County School District R-2J, 4.25%-5.00%, due 12/15/24-12/15/35 | 4.9% |

| Adams & Weld Counties School District No. 27J, 5.00%, due 12/1/24-12/1/42 | 4.7% |

| Colorado Health Facilities Authority, 4.00%-5.00%, due 11/1/28-5/15/45 | 4.3% |

| City of Colorado Springs, 5.00%, due 11/15/34-11/15/39 | 3.8% |

| Colorado Educational & Cultural Facilities Authority, 4.00%-5.25%, due 3/1/26-7/1/44 | 2.8% |

| City of Grand Junction, 5.00%, due 3/1/41-12/1/43 | 2.5% |

| Foothills Park & Recreation District, 4.00%-5.00%, due 12/1/26-12/1/35 | 2.4% |

| Southeast Colorado Hospital District, 5.00%, due 2/1/25 | 2.3% |

| * Excluding short-term investments |

| General Obligation | 30.1% |

| Other Revenue | 26.0% |

| Certificate of Participation/Lease | 12.8% |

| Hospital | 7.3% |

| Transportation | 6.2% |

| Water & Sewer | 6.1% |

| Education | 5.2% |

| Short-Term Investment | 3.0% |

| Other Assets, Less Liabilities | 3.3% |

Material Fund Changes

The following is a summary of certain changes and planned changes to the Fund since April 1, 2024:

In connection with a rebranding of the New York Life Investments products, the Fund’s name was changed from “MainStay MacKay Colorado Muni Fund” to “NYLI MacKay Colorado Muni Fund.” The Fund’s name change will not impact the management of the Fund.

Effective as of the close of business on July 19, 2024, the Aquila Tax-Free Fund of Colorado (the "Predecessor Fund") was reorganized into the Fund, whereby the Fund acquired all of the assets and liabilities of the Predecessor Fund. The expenses shown above include expenses of the Predecessor Fund, which had a different fee structure from the Fund, from April 1, 2024 through the reorganization.

For more complete information, you may review the Fund's next prospectus, which we expect to be available by February 28, 2025 or upon request at 800-624-6782.

Changes in or Disagreements with Accountants

Effective as of the close of business on July 19, 2024, the Predecessor Fund was reorganized into the Fund. As a result of this reorganization, Tait, Weller & Baker LLP (“Tait”) was effectively dismissed as the Predecessor Fund’s independent registered public accounting firm. The selection of KPMG does not reflect any disagreements with or dissatisfaction by the Fund or the Board with the performance of Tait.

KPMG LLP was selected to serve as the Fund’s independent registered public accounting firm for the fiscal period ended October 31, 2024.

Availability of Additional Information

At dfinview.com/NYLIM, you can find additional information about the Fund, when available, including the Fund’s:

Prospectus

Financial information

Fund holdings

Proxy voting information

You can also request this information by contacting us at 800-624-6782.

Householding

Shareholders who have consented to receive a single annual or semiannual shareholder report at a shared address may revoke this consent by contacting their financial intermediary or calling us at 800-624-6782.

NYLI MacKay Oregon Muni Fund

(formerly known as MainStay MacKay Oregon Muni Fund)

Class A/ORTBX

ANNUAL SHAREHOLDER REPORT | October 31, 2024

This annual shareholder report contains important information about NYLI MacKay Oregon Muni Fund (the "Fund") for the period July 22, 2024 to October 31, 2024. You can find additional information about the Fund at dfinview.com/NYLIM. You can also request this information by contacting us at 800-624-6782.

This report describes changes to the Fund that occurred during the reporting period.

What were the Fund costs for the period since inception?

(Based on a hypothetical $10,000 investment)

| Fund (Class) | Costs of a $10,000 investment | Costs paid as a percentage

of a $10,000 investment1,2 |

| Class A | $22^ | 0.80% |

| 1. | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. |

| 2. | Annualized. |

| ^ | Class A shares commenced operations during the reporting period. Expenses for a full reporting period would be higher than the amount shown. |

What factors influenced Fund performance during the reporting period?

During the reporting period ended October 31, 2024, the Fund’s performance relative to the Bloomberg Municipal Bond 1-15 Yr Blend was primarily affected by curve positioning and security selection. Since MacKay Shields LLC began serving as the Subadvisor to the Fund, the MacKay Municipal Managers strategically prioritized increasing tax-exempt income and building tax-efficiency for the benefit of shareholders, while prudently managing interest rate risk.

The following table outlines the key factors (securities, sectors, industries, market events and/or other characteristics) that materially affected the Fund’s performance during the reporting period.

| Key Factor | Summary | Impact |

| Coupon | Underweight exposure to 3% coupon bonds, driven by the shorter duration nature of the exposure | Contributed |

| Sector | Overweight allocation to hospitals, driven by security selection | Contributed |

| Credit quality | Underweight exposure to credits rated A and BBB, driven by security selection | Detracted |

| Maturity | Underweight exposure to bonds maturing in 3 to 9 years, as the short end of the curve outperformed the long end | Detracted |

Fund Performance

The following graph compares the initial and subsequent account values at the end of each of the most recently completed 10 fiscal years of the Fund (or for the life of the Fund, if shorter). It assumes a $15,000 initial investment at the beginning of the first fiscal year in an appropriate, broad-based securities market index and other additional indexes, if applicable, for the same period and reflects the deduction of all sales charges.

| Average Annual Total Returns for the Period-Ended October 31, 2024 | Inception

Date | Since

Inception1 |

| Class A Shares - Including sales charges | 7/22/2024 | (2.85)% |

| Class A Shares - Excluding sales charges | | 0.15%) |

| Bloomberg Municipal Bond Index2 | | 0.46)%% |

| Bloomberg Municipal Bond Index 1-15 Yr Blend3 | | 0.60)%% |

| Morningstar Muni Single State Intermediate Category Average4 | | 0.20)%% |

| 1. | Not annualized. |

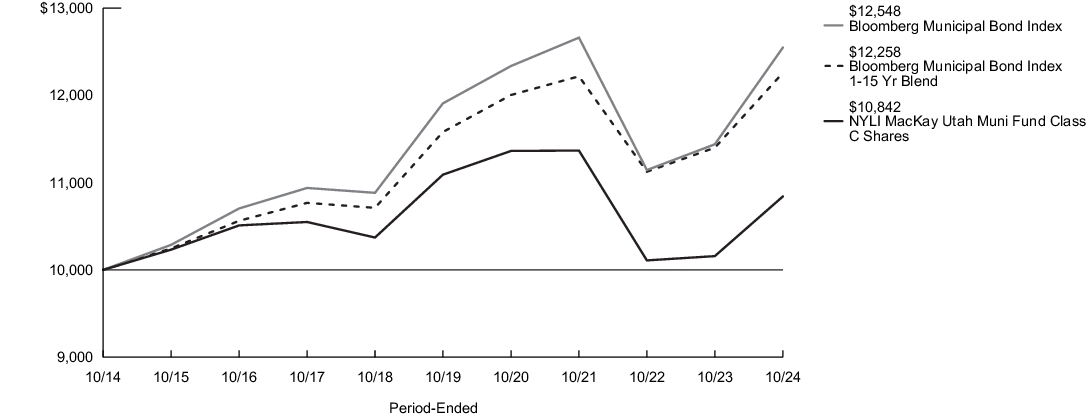

| 2. | In accordance with new regulatory requirements, the Fund has selected the Bloomberg Municipal Bond Index, which represents a broad measure of market performance, and is generally representative of the market sectors or types of investments in which the Fund invests. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with a maturity of at least one year. Bonds subject to the alternative minimum tax or with floating or zero coupons are excluded. |