As filed with the Securities and Exchange Commission on July 12, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM F-1

REGISTRATION STATEMENT

UNDER THESECURITIES ACT OF 1933

TANTECH HOLDINGS LTD

(Exact name of registrant as specified in its charter)

British Virgin Islands

2400

Not Applicable

(State or other jurisdiction

(Primary Standard Industrial

(I.R.S. Employer

of incorporation or organization)

Classification Code Number)

Identification No.)

c/o Tantech Holdings (Lishui) Co., Ltd.

No. 10 Cen Shan Road, Shuige Industrial Zone

Lishui City, Zhejiang Province 323000

People’s Republic of China

+86 (578) 226-2305

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

CT Corporation System

28 Liberty St.

New York, NY 10005

+1-212-894-8940 — telephone

(Name, address including zip code, and telephone number, including area code, of agent for service)

Copies to:

Anthony W. Basch, Esq.

Yan (Natalie) Wang, Esq.

Kaufman & Canoles, P.C.

Two James Center, 14th Floor

1021 East Cary Street

Richmond, Virginia 23219

+1-804-771-5700 — telephone

+1-888-360-9092 — facsimile

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The Selling Shareholders may not sell these securities pursuant to this prospectus until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Subject to Completion, dated July 12, 2024

Up to 61,313,874 Common Shares

TANTECH HOLDINGS LTD

This prospectus relates to the resale, from time to time, by the Selling Shareholders (the “Selling Shareholders”) identified in this prospectus under the caption “Selling Shareholders,” of up to 61,313,874 common shares, no par value (the “Common Shares”), of Tantech Holdings Ltd, consisting of (i) 3,750,000 Common Shares held by the Selling Shareholders, (ii) up to 450,000 Common Shares issuable upon the exercise of pre-funded warrants, or the Pre-Funded Warrants, to purchase Common Shares held by the Selling Shareholders, (iii) up to a maximum of 45,985,404 Common Shares issuable upon the exercise of Series A warrants, or the Series A Warrants, to purchase Common Shares, including Common Shares that may become issuable pursuant to certain anti-dilution adjustments described more fully in the Series A Warrants, and (iv) up to a maximum of 11,128,470 Common Shares issuable upon the exercise of Series B warrants, or the Series B Warrants, to purchase Common Shares.

We are registering the Common Shares on behalf of the Selling Shareholders to be sold by them from time to time.

We are not selling any Common Shares under this prospectus and will not receive any proceeds from the sale of Common Shares by the Selling Shareholders. We may receive cash proceeds equal to the total exercise price of the Pre-Funded Warrants, Series A Warrants and the Series B Warrants, or the Warrants, to the extent that the Warrants are exercised using cash. The exercise price of each Pre-Funded Warrant or Series B Warrant is $0.0001 per Common Share and the exercise price of the Series A Warrant is $0.75 per Common Share, subject to adjustments. See “Use of Proceeds.”

The Selling Shareholders may sell the Common Shares offered by this prospectus from time to time on terms to be determined at the time of sale through ordinary brokerage transactions or through any other means described in this prospectus under the caption “Plan of Distribution.” The Common Shares may be sold at fixed prices, at prevailing market prices at the time of sale, at prices related to the prevailing market price, at varying prices determined at the time of sale, or at negotiated prices.

Our Common Shares are listed on the Nasdaq Capital Market (“Nasdaq”) under the symbol “TANH.” On July 11, 2024, the last reported sale price of our Common Shares was $0.7358 per share. There is no established market for the Warrants and we do not intend to apply to list the Warrants on any securities exchange or other nationally recognized trading system.

We are not a Chinese operating company but a British Virgin Islands holding company with operations conducted by our subsidiaries established in People’s Republic of China (“PRC” or “China”), Hong Kong Special Administrative Region of the People’s Republic of China (“HKSAR” or “Hong Kong”) and United States. Therefore, investing in our securities being offered pursuant to this prospectus involves unique and a high degree of risk. You should carefully read and consider the “Risk Factors” beginning on page 41 of this prospectus and those included in the periodic and other reports we file with the Securities and Exchange Commission for more information before you make your investment decision.

The securities offered in this offering are of the offshore holding company Tantech Holdings Ltd (the “Company”), which owns equity interests, directly or indirectly, of the operating subsidiaries. Subsidiaries conduct most of the Company’s business operations in China and the holding company does not conduct operations in China. Unless otherwise stated, as used in this prospectus and in the context of describing our operations and consolidated financial information, “Tantech” “we,” “us,” “Company,” or “our,” refers to Tantech Holdings Ltd, a British Virgin Islands business company. “PRC Subsidiaries” refer to our subsidiaries incorporated in mainland China, and “Hong Kong Subsidiaries” refer to our subsidiaries incorporated in Hong Kong. We will also refer to all of our subsidiaries, “Subsidiaries”.

We are also subject to legal and operational risks associated with being based in and having the majority of the company’s operations in PRC. The Chinese government may intervene or influence the operation of our PRC operating entities and exercise significant oversight and discretion over the conduct of their business and may intervene in or influence their operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operations and/or the value of our Common Shares. Further, any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

On July 6, 2021, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly released the Opinions on Severely Cracking Down on Illegal Securities Activities According to Law, or the Opinions. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Effective measures, such as promoting the construction of relevant regulatory systems will be taken to deal with the risks and incidents of China-concept overseas listed companies, and cybersecurity and data privacy protection requirements, etc. The Opinions and any related implementing rules to be enacted may subject us to compliance requirement in the future.

On February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the relevant system and rules for the management of overseas listing records, which has been implemented from March 31, 2023. A total of six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”) and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement, misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the listing and trading of our Common Shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required. Further, we believe, as of the date of this annual report, none of the circumstances prohibiting the overseas offering and listing by domestic companies established in mainland China as listed above applies to us, and we can offer and continue to offer our Common Shares on Nasdaq.

In accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we had been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our Mainland China Subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our Mainland China Subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

Further, on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which has come into effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators, any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws and regulations. Any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected of committing a crime. As of the date of this prospectus, we believe that we and our subsidiaries have not provided or publicly disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. We intend to strictly comply with the Confidentiality Provisions and other relevant PRC laws and regulations in our offering and listing on Nasdaq in future.

However, any failure of us or our mainland China subsidiaries to fully comply with the Listing Records Rules and/or the Confidentiality Provisions, may significantly limit or completely hinder our ability to offer or continue to offer our Common Shares on Nasdaq, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our Common Shares to significantly decline in value or become worthless. See “Risk Factor — Risks Related to Doing Business in China — The filing with the CSRC is required, and the approval of, filing or other procedures with other Chinese regulatory authorities may be required, in connection with issuing securities to foreign investors under PRC law, and, if required, we cannot predict whether we will be able, or how long it will take us, to obtain such approval or complete such filing or other procedures.

We or our Subsidiaries may also be subject to PRC laws relating to the use, sharing, retention, security and transfer of confidential and private information, such as personal information and other data. On November 14, 2021, the Cyberspace Administration of China (“CAC”) released the Regulations on the Network Data Security Management (Draft for Comments), or the Data Security Management Regulations Draft, to solicit public opinion and comments till December 13, 2021, which has not been promulgated as of the date of this prospectus. Pursuant to the Data Security Management Regulations Draft, data processors holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. Data processing activities refers to activities such as the collection, retention, use, processing, transmission, provision, disclosure, or deletion of data. According to the latest amended Cybersecurity Review Measures, which was promulgated on November 16, 2021, and became effective on February 15, 2022, an online platform operator holding more than one million users/users’ individual information shall be subject to cybersecurity review before listing abroad. As of the date of this prospectus, we have not been informed by any PRC governmental authority of any requirement that we or our Subsidiaries file for approval for this offering. We don’t believe that we or any of our Subsidiaries will be subject to either the amended Cybersecurity Review Measures or the Data Security Management Regulations Draft since none of us hold more than one million users/users’ individual information. However, it is uncertain how the above-mentioned new laws or regulations will be enacted, interpreted or implemented, and whether it will affect us. Since the regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, if any, and the potential impact such modified or new laws and regulations will have on our Subsidiaries’ daily business operation, their ability to accept foreign investments, and our ability to continue to list or offer securities on an U.S. exchange. See “Risk Factor — The Chinese government exerts substantial influence over the manner in which we must conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Common Shares.”

On February 7, 2021, the Anti-Monopoly Committee of the State Council promulgated the Anti-monopoly Guidelines for the Platform Economy Sector, or the Anti-monopoly Guideline, aiming to improve anti-monopoly administration on online platforms. The Anti-monopoly Guideline, operating as the compliance guidance under the then-existing PRC anti-monopoly regulatory regime for platform economy operators, specifically prohibits certain acts of the platform economy operators that may have the effect of eliminating or limiting market competition, such as concentration of undertakings.

The PRC anti-monopoly regulatory regime started with the Anti-Monopoly Law promulgated by the Standing Committee of the National People’s Congress of China (“SCNPC”) on August 30, 2007 and effective on August 1, 2008, which requires that transactions which are deemed concentrations and involve parties with specified turnover thresholds must be cleared by the Ministry of Commerce of China (“MOFCOM”) before they can be completed. In addition, on February 3, 2011, the General Office of the State Council promulgated a Notice on Establishing the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, or Circular 6, which officially established a security review system for mergers and acquisitions of domestic enterprises by foreign investors. Further, on August 25, 2011, MOFCOM promulgated the Regulations on Implementation of Security Review System for the Merger and Acquisition of Domestic Enterprises by Foreign Investors, or the MOFCOM Security Review Regulations, which became effective on September 1, 2011, to implement Circular 6. Under Circular 6, a security review is required for mergers and acquisitions by foreign investors having “national defense and security” concerns and mergers and acquisitions by which foreign investors may acquire the “de facto control” of domestic enterprises with “national security” concerns. Under the MOFCOM Security Review Regulations, MOFCOM will focus on the substance and actual impact of the transaction when deciding whether a specific merger or acquisition is subject to security review. If MOFCOM decides that a specific merger or acquisition is subject to security review, it will submit it to the Inter-Ministerial Panel, an authority established under the Circular 6 led by the NDRC, and MOFCOM under the leadership of the State Council, to carry out the security review. The regulations prohibit foreign investors from bypassing the security review by structuring transactions through trusts, indirect investments, leases, loans, control through contractual arrangements or offshore transactions.

As a holding company, we may rely upon dividends paid to us by our subsidiaries in the PRC to pay dividends and to finance any debt we may incur. As of the date of this prospectus, none of our subsidiaries has issued any dividends or distributions to us and we have not made any dividends or distributions to our shareholders. Our subsidiaries in the PRC generate and retain cash generated from operating activities and re-invest it in our business.

Under BVI law, we may pay a dividend on our shares out of either profit, provided that in no circumstances may a dividend be paid if this would result in us being unable to pay our debts due in the ordinary course of business. If we determine to pay dividends, as a holding company, we will be dependent on receipt of funds from our subsidiaries in PRC through our Hong Kong subsidiaries.

Current PRC regulations permit our subsidiary in mainland China to pay dividends to the Company only out of its accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. Under our current corporate structure, we rely on dividend payments or other distributions from our subsidiaries to fund any cash and financing requirements we may have, including the funds necessary to pay dividends and other cash distributions to our shareholders or to service any debt we may incur. If any subsidiary incurs debt on its own behalf in the future, the instruments governing such debt may restrict its ability to pay dividends to us. In addition, under PRC laws and regulations, each of our Chinese subsidiaries is required to set aside a portion of their net income each year to fund a statutory surplus reserve until such reserve reaches 50% of its registered capital. This reserve is not distributable as dividends. As a result, our PRC subsidiaries are restricted in their ability to transfer a portion of its net assets to us in the form of dividends, loans or advances. Further, the PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. If we are unable to receive funds from our subsidiaries, we may be unable to pay cash dividends on our common shares.

Cash dividends, if any, on our common shares will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10%. A 10% PRC withholding tax is applicable to dividends payable to investors that are non-resident enterprises. Any gain realized on the transfer of common shares by such investors is also subject to PRC tax at a current rate of 10% which in the case of dividends will be withheld at source if such gain is regarded as income derived from sources within the PRC.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC resident enterprise. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including without limitation that (a) the Hong Kong resident enterprise must be the beneficial owner of the relevant dividends; and (b) the Hong Kong resident enterprise must directly hold no less than 25% share ownership in a PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot be certain that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by our PRC subsidiaries to our Hong Kong subsidiaries. As of the date of this prospectus, we have not applied for the tax resident certificate from the relevant Hong Kong tax authority. Our Hong Kong subsidiaries intend to apply for the tax resident certificate when our subsidiaries in mainland China plan to declare and pay dividends to their Hong Kong parent companies.

As an offshore holding company, we will be permitted under PRC laws and regulations to provide funding from the proceeds of our offshore fund-raising activities to our subsidiaries in China only through loans or capital contributions, subject to the satisfaction of the applicable government registration and approval requirements. Before providing loans to our PRC subsidiaries, we will be required to make filings about details of the loans with the State Administration of Foreign Exchange of the PRC (the “SAFE”) in accordance with relevant PRC laws and regulations. Our PRC subsidiaries that receive the loans are only allowed to use the loans for the purposes set forth in these laws and regulations. Under regulations of the SAFE, Renminbi is not convertible into foreign currencies for capital account items, such as loans, repatriation of investments and investments outside of China, unless the prior approval of the SAFE is obtained and prior registration with the SAFE is made. In addition, in accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we have been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our mainland China subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our mainland China subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

Under PRC law, we may provide funding to our PRC subsidiaries only through capital contributions or loans, and prior to the dismantling of our PRC consolidated affiliated entities only through loans to our former consolidated affiliated entities, subject to satisfaction of applicable government registration and approval requirements.

For the years ended December 31, 2021, the Company provided working capital loans of $12.0 million to our wholly owned subsidiary, USCNHK Group Limited, and $7.0 million to our wholly owned subsidiary, Zhejiang Tantech Bamboo Charcoal Co., Ltd.

For the years ended December 31, 2022, the Company provided working capital loans of $8.9 million to our wholly owned subsidiary, USCNHK Group Limited, $350,000 to our wholly owned subsidiary, EPakia Inc., $20,000 to our wholly owned subsidiary EPakia Canada Inc., and $2,000 to our wholly owned subsidiary, EAG International Vantage Capitals Limited.

For the years ended December 31, 2023, the Company provided working capital loans of $5.9 million to Tantech Bamboo Charcoal Co., Ltd., a wholly owned subsidiary; $890,000 to EPakia Inc., a wholly owned subsidiary, and $30,000 to EPakia Canada Inc., a wholly owned subsidiary.

We have not declared or paid any cash dividends, nor do we have any present plan to pay any cash dividends on our common shares in the foreseeable future. We currently intend to retain most, if not all, of our available funds and any future earnings to operate and expand our business.

As of the date of this prospectus, we do not anticipate any difficulties on our ability to transfer cash between subsidiaries. We have not installed any cash management policies that dictate the amount of such funds and how such funds are transferred.

Our common shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the Holding Foreign Companies Accountable Act (the “HFCAA”) if the PCAOB determines it is unable to inspect or investigate completely our auditors for two consecutive years. Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. Our auditor, YCM CPA Inc., headquartered in Irvine, California, has been inspected by the PCAOB on a regular basis. Our auditor was not among the PCAOB-registered public accounting firms headquartered in the PRC or Hong Kong that were subject to PCAOB’s determination. On December 15, 2022, the PCAOB removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. Notwithstanding the foregoing, in the future, if it is determined that the PCAOB is unable to inspect or investigate our auditor completely, or if there is any regulatory change or step taken by PRC regulators that does not permit our auditor to provide audit documentations to the PCAOB for inspection or investigation, or the PCAOB expands the scope of the Determination so that we are subject to the HFCAA, as the same may be amended, you may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected or investigated by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditor’s audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities, including trading on the national exchange or “over-the-counter” markets, may be prohibited under the HFCAA. See “Risk Factors — Our shares may be delisted under the Holding Foreign Companies Accountable Act if the PCAOB is unable to inspect our auditors for two consecutive years” for more information.

Investing in our securities being offered pursuant to this prospectus involves a high degree of risk. You should carefully read and consider the risk factors beginning on page 41 of this prospectus, as well as those included in the periodic and other reports we file with the Securities and Exchange Commission before you make your investment decision.

Neither the Securities and Exchange Commission, any United States state securities commission, the British Virgin Islands Monetary Authority, nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus and our SEC filings that are incorporated by reference into this prospectus contain or incorporate by reference forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. All statements other than statements of historical fact are “forward-looking statements,” including any projections of earnings, revenue or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements concerning proposed new projects or other developments, any statements regarding future economic conditions or performance, any statements of management’s beliefs, goals, strategies, intentions and objectives, and any statements of assumptions underlying any of the foregoing. The words “believe,” “anticipate,” “estimate,” “plan,” “expect,” “intend,” “may,” “could,” “should,” “potential,” “likely,” “projects,” “continue,” “will,” and “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Forward-looking statements reflect our current views with respect to future events, are based on assumptions and are subject to risks and uncertainties. We cannot guarantee that we actually will achieve the plans, intentions or expectations expressed in our forward-looking statements and you should not place undue reliance on these statements. There are a number of important factors that could cause our actual results to differ materially from those indicated or implied by forward-looking statements. These important factors include those discussed under the heading “Risk Factors” contained or incorporated by reference in this prospectus and in the applicable prospectus supplement and any free writing prospectus we may authorize for use in connection with a specific offering. These factors and the other cautionary statements made in this prospectus should be read as being applicable to all related forward-looking statements whenever they appear in this prospectus. Except as required by law, we undertake no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

This prospectus describes the general manner in which the Selling Shareholders may offer from time to time up to an aggregate of 61,313,874 Common Shares, consisting of 3,750,000 Common Shares held by the Selling Shareholders, up to 450,000 Common Shares issuable upon the exercise of the Pre-Funded Warrants, up to a maximum of 45,985,404 Common Shares issuable upon the exercise of the Series A Warrants, including Common Shares that may become issuable pursuant to certain anti-dilution adjustments, and up to a maximum of 11,128,470 Common Shares issuable upon the exercise of the Series B Warrants. You should rely only on the information contained in this prospectus and the related exhibits, any prospectus supplement or amendment thereto and the documents incorporated by reference, or to which we have referred you, before making your investment decision. Neither we nor the Selling Shareholders have authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus, any prospectus supplement or amendments thereto do not constitute an offer to sell, or a solicitation of an offer to purchase, the Common Shares offered by this prospectus, any prospectus supplement or amendments thereto in any jurisdiction to or from any person to whom or from whom it is unlawful to make such offer or solicitation of an offer in such jurisdiction. You should not assume that the information contained in this prospectus, any prospectus supplement or amendments thereto, as well as information we have previously filed with the U.S. Securities and Exchange Commission (the “SEC”), is accurate as of any date other than the date on the front cover of the applicable document.

If necessary, the specific manner in which the Common Shares may be offered and sold will be described in a supplement to this prospectus, which supplement may also add, update or change any of the information contained in this prospectus. To the extent there is a conflict between the information contained in this prospectus and the prospectus supplement, you should rely on the information in the prospectus supplement, provided that if any statement in one of these documents is inconsistent with a statement in another document having a later date-for example, a document incorporated by reference in this prospectus or any prospectus supplement-the statement in the document having the later date modifies or supersedes the earlier statement.

Neither the delivery of this prospectus nor any distribution of Common Shares pursuant to this prospectus shall, under any circumstances, create any implication that there has been no change in the information set forth or incorporated by reference into this prospectus or in our affairs since the date of this prospectus. Our business, financial condition, results of operations and prospects may have changed since such date.

As permitted by SEC rules and regulations, the registration statement of which this prospectus forms a part includes additional information not contained in this prospectus. You may read the registration statement and the other reports we file with the SEC at its website or at its offices described below under “Where You Can Find More Information.”

Except as otherwise indicated by the context, references in this prospectus to:

·

“we,” “us,” “the Company,” “our,” “THL” and “Tantech” are to Tantech Holdings Ltd, a British Virgin Islands company limited by shares (formerly, Sinoport Enterprises Limited);

·

USCNHK are to USCNHK Group Limited, a Hong Kong limited company, which is a wholly owned subsidiary of THL;

·

EAG are to EAG International Vantage Capitals Limited, a Hong Kong limited company, which is a wholly owned subsidiary of THL;

·

China East are to China East Trade Co., Limited., a Hong Kong company, which is a wholly owned subsidiary of Eurasia.

·

EPakia are to EPakia Inc., a Delaware corporation, which is a wholly owned subsidiary of THL;

·

“PRC Subsidiaries” and “Operating Subsidiaries” are to our subsidiaries established and operated in mainland China, including:

·

Tantech Holdings (Lishui) Co., Ltd. (“Lishui Tantech”), which is a wholly owned subsidiary of USCNHK ;

Euroasia New Energy Automotive (Jiangsu) Co., Ltd. (“Euroasia New Energy”), which is a wholly owned subsidiary of EAG;

·

Shanghai Jiamu Investment Management Co., Ltd. (“Jiamu”), which is a wholly owned subsidiary of EAG;

·

Lishui Xincai Industrial Co., Ltd. (“Lishui Xincai”), which is a wholly owned subsidiary of Lishui Tantech;

·

Lishui Smart New Energy Automobile Co., Ltd. (“Lishui Smart”), which is a wholly owned subsidiary of Lishui Tantech;

·

Zhejiang Shangnilai Technology Co., Ltd. (“Shangnilai,” formerly Zhejiang Shangchi New Energy Automobile Co., Ltd.), which is a wholly owned subsidiary of Lishui Tantech;

·

Lishui Jikang Energy Technology Co., Ltd. (“Jikang Energy”), which is a wholly owned subsidiary of Lishui Xincai;

·

Hangzhou Tanbo Technology Co., Ltd., a PRC company (“Tanbo Tech”), which is a wholly owned subsidiary of Lishui Xincai;

·

Hanzhou Wangbo Investment Management Co., Ltd (“Wangbo”), which is a wholly owned subsidiary of Jiamu;

·

Hangzhou Jiyi Investment Management Co., Ltd. (“Jiyi”), which is a wholly owned subsidiary of Jiamu:

·

Shangchi Automobile Co., Ltd. (“Shangchi Automobile”), which is 51% owned by Wangbo, 19% owned by Jiyi, and 30% owned by an unrelated third party;

·

Shenzhen Yimao New Energy Sales Co., Ltd. (“Shenzhen Yimao”), which is a wholly owned subsidiary of Shangchi Automobile.

·

Eurasia Holdings (Zhejiang) Co., Ltd. (“Eurasia Zhejiang”), which is a wholly owned subsidiary of EAG;

·

Hangzhou Eurasia Supply Chain Co., Ltd. (“Hangzhou Eurasia”), which is a wholly owned subsidiary of Eurasia Zhejiang;

·

Gangyu Trading (Jiangsu) Co., Ltd., which is a wholly owned subsidiary of Euroasia New Energy;

·

Shangchi (Zhejiang) Intelligent Equipment Co., Ltd (“Shangchi Intelligent Equipment”), which is a wholly owned subsidiary of Euroasia;

·

Shanghai Wangju Industrial Group Co., Ltd. (“Shanghai Wangju”), which is a wholly owned subsidiary of Jiamu;

·

Shenzhen Shangdong Trading Co., Ltd. (“Shenzhen Shangdong”), which is a wholly owned subsidiary of Shanghai Wangju;

·

First International Commercial Factoring (Shenzhen) Co., Ltd., which is 75% owned by Shenzhen Shangdong and 25% by China East; and

·

Zhejiang Shangchi Medical Equipment Co., Ltd., which is a wholly owned subsidiary of Shangchi Intelligent Equipment.

·

all references to “RMB,” “Renminbi” and “¥” are to the legal currency of China and all references to “USD,” “U.S. dollars,” “dollars,” and “$” are to the legal currency of the United States; and

·

“China” and “PRC” refer to the People’s Republic of China, and for the purpose of this prospectus only, excluding Taiwan, Hong Kong and Macau.

Tantech is not a PRC operating company but a holding company incorporated in the British Virgin Islands. As a holding company, we own equity interests, directly or indirectly, in our Subsidiaries based in mainland China, Hong Kong and the U.S. The vast majority of the business operations are conducted by our Subsidiaries based in mainland China.

Investors in Tantech’s securities are not purchasing an equity interest in our operating subsidiaries in mainland China, but instead are purchasing an equity interest in a British Virgin Islands holding company.

This summary highlights selected information that is presented in greater detail elsewhere, or incorporated by reference, in this prospectus. It does not contain all of the information that may be important to you and your investment decision. Before investing in the securities that we are offering, you should carefully read this entire prospectus, including the matters set forth under the section of this prospectus captioned “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements” and the financial statements and related notes and other information that we incorporate by reference herein, including, but not limited to, our 2023 Annual Report and our other SEC reports.

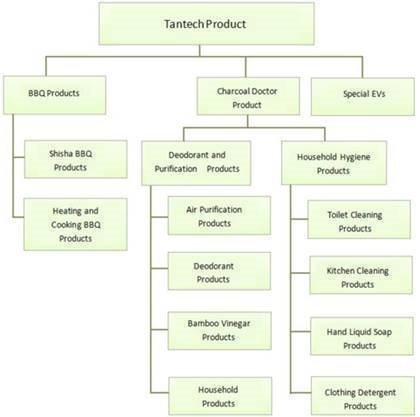

Overview

Our PRC Subsidiaries develop and manufacture bamboo-based charcoal products for industrial energy applications and household cooking, heating, purification, agricultural and cleaning uses. We have grown over the past decade to become a pioneer in charcoal products industry made from carbonized bamboo. We are a highly specialized high-tech enterprise producing, researching and developing bamboo charcoal-based products with an established domestic and international sales and distribution network. On July 12, 2017, we completed the acquisition of Suzhou E Motors Co, which became known as Shangchi Automobile, a specialty electric vehicles manufacturer based in Zhangjiagang City, Jiangsu Province. Manufacturing and sale of electric vehicles and specialty vehicles are a major segment of our business operations. Two of our PRC Subsidiaries focus on production and sale of electric vehicles.

The following diagram depicts our main business segments and lines of products:

We oversee a national sales network that has a presence in 19 cities throughout China for our charcoal products. Through distributors, our charcoal products are also sold in Japan, South Korea, Taiwan, the Middle East and Europe. In addition to our bamboo charcoal products, we also derive revenues from our trading activities, which primarily relate to industrial purchases and sales of charcoal.

Further, we own an indirect 18% interest in Libo Haokun Stone Co., Ltd., a marble mining operating company, and an indirect 14.76% interest in Fuquan Chengwang, a basalt mining company.

Shangchi Automobile has to date developed a full range of electric buses and specialty vehicles. Its products include electric buses, electric logistics cars, and electric specialty vehicles, such as high-speed brushless cleaning cars, electric cleaning cars, special emergency vehicles, and funeral cars.

Since 2022, we expanded into two new lines of business—biodegradable packaging business and commercial factoring service. Biodegradable packaging is a type of packaging that is designed to break down naturally in the environment, without leaving behind harmful pollutants or waste. The market for biodegradable packaging has been growing rapidly in recent years, driven by increased awareness of environmental issues and the desire to reduce plastic waste. We generated approximately $0.7 million and $4.0 million revenue from biodegradable packaging business in fiscal 2023 and 2022, respectively.

We offer commercial factoring services to customers seeking financing for their receivables. We generated approximately $2.2 million and $1.4 million financing interest income in fiscal 2023 and 2022, respectively.

We rely on a combination of patent, trademark and trade secret laws and non-disclosure agreements and other methods to protect our intellectual property rights. We currently own six patents and fifty-eight trademarks in China with respect to our bamboo charcoal production and two patents and fifteen trademarks in China with respect to our vehicle production.

The following diagram illustrates our current corporate structure:

Holding Company Structure

Tantech is a British Virgin Islands holding company incorporated on November 9, 2010 under the BVI Companies Act, 2004, as a company limited by shares. Tantech is currently not actively engaging in any business. You may never hold equity interests in the operating PRC Subsidiaries. As of the date of this prospectus, Tantech is authorized to issue unlimited number of common shares, no par value each. As of the date of this prospectus, there are 8,343,755 common shares issued and outstanding. Tantech controls and receives the economic benefits of the business operations of our PRC subsidiaries through equity ownership. USCNHK was formed on October 17, 2008 under the Companies Ordinance (Chapter 32) of Hong Kong. Euroasia was formed on April 27, 2015 as a limited company in Hong Kong. USCNHK and Euroasiais are each a holding company owning equity interests in our subsidiaries based in mainland China. We currently do not have a VIE in our corporate structure.

Summary of Risk Factors

Investing in our Common Shares involves significant risks. You should carefully consider all of the information in this prospectus before making an investment in our Common Shares. Below please find a summary of the principal risks we face, organized under relevant headings. These risks are discussed more fully in the section titled “Risk factors.”

Risks Related To This Offering

·

A large number of Common Shares may be sold in the market following this offering, which may significantly depress the market price of our Common Shares.

·

We cannot assure you that our Common Shares will remain listed on Nasdaq or any other securities exchange.

·

There has been and may continue to be significant volatility in the volume and price of our Common Shares on Nasdaq.

·

We have not paid and do not intend to pay dividends on our Common Shares and investors may never receive a return on their investment.

We are based in China and have the majority of our operations in China, and as a result, we face risks and uncertainties related to doing business in China. Such risks include, without limitation:

·

Uncertainties with respect to the PRC legal system could have a material adverse effect on us.

·

If the Chinese government determines that our corporate structure does not comply with Chinese regulations, or if Chinese regulations change or are interpreted differently in the future, the value of our ordinary shares may decline in value or become worthless.

·

China’s economic, political and social conditions, as well as government policies, laws and regulations may change quickly with little advance notice, and any such sudden changes could have a material adverse effect on our business and the value of our Common Shares.

·

The Chinese government exerts substantial influence over the manner in which we may conduct our business activities and may intervene or influence our operations at any time, which could result in a material change in our operations and the value of our Common Shares.

·

We are required to complete filing procedures with the CSRC in connection with securities issuance and may be subject to approval, filing or other procedures with other Chinese regulatory authorities under PRC law; we cannot predict whether we will be able, or how long it will take us, to obtain such approval or complete such filing or other procedures.

·

The PRC government exerts substantial influence over the manner in which we conduct our business through our subsidiaries in China and may intervene in or influence the operations of our subsidiaries at any time, which could result in a material change in our operations and cause the value of our ordinary shares to significantly decline or become worthless.

·

The Chinese government may exert more oversight and control over offerings that are conducted overseas and foreign investment in China-based issuers. As a result, we face uncertainty about future actions by the PRC government that could significantly affect our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless.

·

Trading in our securities may be prohibited under the Holding Foreign Companies Accountable Act if the PCAOB determines that it cannot inspect or investigate completely our auditors for two consecutive years.

·

We may be classified as a PRC “resident enterprise” for PRC enterprise income tax purposes. Such classification would likely result in unfavorable tax consequences to us and our non-PRC shareholders and have a material adverse effect on our results of operations and the value of your investment.

·

Our PRC subsidiaries are subject to restrictions on paying dividends or making other payments to us, which may restrict our ability to satisfy our liquidity requirements.

Implication of Being a Foreign Private Issuer

We are a foreign private issuer within the meaning of the rules under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). As such, we are exempt from certain provisions applicable to United States domestic public companies. For example:

·

we are not required to provide as many Exchange Act reports or provide periodic and current reports as frequently as a domestic public company;

we are exempt from certain U.S. federal securities law provisions applicable to U.S. domestic issuers and are also permitted to rely on exemptions from certain Nasdaq corporate governance standards applicable to U.S. issuers, and such exemptions may afford less protection to shareholders;

·

we are not required to provide the same level of disclosure on certain issues, such as executive compensation;

·

we are exempt from certain provisions of Regulation FD aimed at preventing issuers from making selective disclosures of material information; and

·

we are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act.

Permission Required from the PRC Authorities for the Company’s Operation and Securities Issuance

We conduct our business in China through our subsidiaries, and prior to August 2021, also through our VIEs in China. Our operations in China are governed by PRC laws and regulations. We are required to obtain certain permissions from the PRC authorities to operate, issue securities to foreign investors, and transfer certain data. The PRC government has exercised, and may continue to exercise, substantial influence or control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be undermined if our PRC subsidiaries are not able to obtain or maintain approvals to operate in China. The central or local governments could impose new, stricter regulations or interpretations of existing regulations that could require additional expenditures, and efforts on our part to ensure our compliance with such regulations or interpretations. To operate our general business activities currently conducted in mainland China, each of our PRC subsidiaries is required to obtain a business license from the local counterpart of the State Administration for Market Regulation, or SAMR. Each of our PRC subsidiaries has obtained a valid business license from the local SAMR, and no application for any such license has been denied. Our PRC subsidiaries are also required to obtain certain licenses and permits, including but not limited to the following material licenses and permits: the Wood and Bamboo Operation and Processing Approval Certificate issued by Zhejiang provincial government for our consumer product segment and our electric vehicles (EVs) and fuel vehicles being listed in the Announcement of the Vehicle Manufacturers and Products issued by the Ministry of Industry and Information Technology of PRC, or the MIIT, which is the entry approval for Shangchi Automobile to become a qualified manufacturer of vehicles and for the manufacturing and sales of our EVs and other vehicles. As of the date of this prospectus, as advised by our PRC legal counsel, Zhejiang Zhengbiao Law Firm, we and our PRC subsidiaries have received all requisite permits, approvals and certificates from the PRC government authorities to conduct our business operations in China. To our knowledge, no permission or approval has been denied or revoked. However, given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by government authorities, we cannot be certain that relevant policies in this regard will not change in the future, which may require us or our subsidiaries to obtain additional licenses, permits, filings or approvals for conducting our business in the PRC. If we or our subsidiaries do not receive or maintain required permissions or approvals, or inadvertently conclude that such permissions or approvals are not required, we may be subject to governmental investigations or enforcement actions, fines, penalties, suspension of operations, or be prohibited from engaging in relevant business or conducting securities offering, and these risks could result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless.

In connection with our previous issuance of securities to foreign investors, under current PRC laws, regulations and regulatory rules, as of the date of this prospectus, we and our PRC subsidiaries, (i) are not required to obtain permissions from the China Securities Regulatory Commission, or the CSRC, (ii) are not required to go through cybersecurity review by the Cyberspace Administration of China, or the CAC, and (iii) have not received or were denied such requisite permissions by any PRC authority. However, the PRC government has recently indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers.

On February 17, 2023, with the approval of the State Council, China Securities Regulatory Commission (the “CSRC”) issued the relevant system and rules for the management of overseas listing records, which will be implemented from March 31, 2023. A total of six institutional rules (the “Listing Records Rules”) have been issued this time, including the Trial Measures for the Administration of Overseas Issuance and Listing of Securities by Domestic Enterprises (hereinafter referred to as the “Trial Measures”) and five supporting guidelines. Under the Listing Records Rules, a company established in mainland China seeking securities offering and listing, by both direct or indirect means, in an overseas market is required to undertake filing procedures with the CSRC for its overseas offering and listing activities. The Trial Measures also set forth a list of circumstance under which overseas offering and listing by domestic companies established in mainland China is prohibit, including: (i) where such securities offering and listing is explicitly prohibited by the PRC laws; (ii) where the intended securities offering and listing may endanger national security as reviewed and determined by competent PRC authorities under the State Council in accordance with PRC laws; (iii) where the domestic company established in mainland China, or its controlling shareholders and the actual controller, have committed crimes such as corruption, bribery, embezzlement, misappropriation of property or undermining the order of the socialist market economy during the latest three (3) years; (iv) where the domestic company established in mainland China seeking securities offering and listing is suspected of committing crimes or major violations of laws and regulations, and is under investigation according to law, and no conclusion has yet been made thereof; and (v) where there are material ownership disputes over equity held by the controlling shareholder of the company established in mainland China or by other shareholders that are controlled by the controlling shareholder and/or actual controller. In accordance with the Trial Measures, the listing and trading of our Common Shares on Nasdaq is deemed as an indirect overseas offering and listing by domestic companies established in mainland China, and thus, we are subject to the Listing Records Rules and the relevant filing procedures as required. Further, we believe, as of the date of this prospectus, none of the circumstances prohibiting the overseas offering and listing by domestic companies established in mainland China as listed above applies to us, and we can offer and continue to offer our Common Shares on Nasdaq.

In accordance with the Notice on the Arrangement for the Filing of Overseas Offering and Listing by Domestic Companies issued by the CSRC along with the Listing Records Rules on the same day, we are deemed as an “Existing Issuer” because we had been listed overseas before March 31, 2023. Under such Notice, we are not required to undertake the initial filing procedure immediately. However, we shall carry out filing procedures as required in a timely manner for the subsequent events, including any further follow-up offerings on Nasdaq, dual and/or secondary offering and listing on different overseas markets, and occurrence of material events including change of control, investigations or sanctions imposed by overseas securities regulatory agencies or other relevant competent authorities, change of listing status or transfer of listing segment, and voluntary or mandatory delisting. If we or our Mainland China Subsidiaries in future fail to undertake filing procedures as stipulated in the Trial Measures, or offer and list securities in an overseas market in violation of the Trial Measures, the CSRC may order rectification, issue warnings to us and/or our Mainland China Subsidiaries, and impose a fine of between RMB 1,000,000 yuan and RMB 10,000,000 yuan. The CSRC may also inform its regulatory counterparts in the overseas jurisdictions, such as the SEC, via cross-border securities regulatory cooperation mechanisms.

Further, on February 24, 2023, the CSRC, together with Ministry of Finance, National Administration of State Secrets Protection, and National Archives Administration of China, released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises (the “Confidentiality Provisions”), which will come into effect on March 31, 2023 with the Trial Measures. Under the Confidentiality Provisions, domestic companies established in mainland China seeking overseas offering and listing, by both direct and indirect means, are required to institute a sound confidentiality and archives system. If such domestic companies established in mainland China intend to, either directly or through its overseas listed entity, publicly disclose or provide to relevant individuals or entities including securities companies, securities service providers and overseas regulators, any documents and materials that contain state secrets or working secrets of government agencies, they shall obtain approval from competent authorities and complete the relevant filing procedure with the competent secrecy administrative department prior to their disclosure or provision of such documents and materials. Further, if they provide or publicly disclose documents and materials which may adversely affect national security or public interests, they shall strictly follow the corresponding procedures in accordance with relevant laws and regulations. Once effective, any failure or perceived failure by us or our subsidiaries to comply with the above confidentiality and archives administration requirements under the Confidentiality Provisions and other relevant PRC laws and regulations may cause relevant entities to be held legally liable by competent authorities, and referred to the judicial organ to be investigated for criminal liability if suspected of committing a crime. As of the date of this prospectus, we believe that we and our subsidiaries have not provided or publicly disclosed any documents or materials involving state secrets or work secrets of PRC government agencies or any of which may adversely affect national security or public interests, to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. We intend to strictly comply with the Confidentiality Provisions and other relevant PRC laws and regulations in our offering and listing on Nasdaq in future.

However, any failure of us or our mainland China subsidiaries to fully comply with the Listing Records Rules and/or the Confidentiality Provisions, once effective, may significantly limit or completely hinder our ability to offer or continue to offer our Common Shares on Nasdaq, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our Common Shares to significantly decline in value or become worthless.

On July 10, 2021, the CAC published a revised draft revision to the Cybersecurity Review Measures for public comment, or the Revised Cybersecurity Measures. Under these measures, an operator having more than one million users shall be subject to cybersecurity review before listing abroad. The cybersecurity review will evaluate the risk of critical information infrastructure, core data, important data, or a large amount of personal information being influenced, controlled or maliciously used by foreign governments after going public overseas. The procurement of network products and services, data processing activities and overseas listing should also be subject to cybersecurity review if they concern or potentially pose risks to national security. According to the effective Cybersecurity Review Measures, online platform/website operators of certain industries may be identified as critical information infrastructure operators by the CAC, once they meet standard as stated in the National Cybersecurity Inspection Operation Guide, and such operators may be subject to cybersecurity review. On December 28, 2021, the CAC, the National Development and Reform Commission (“NDRC”), and other government agencies jointly issued the final version of the Revised Measures for Cybersecurity Review, or the Measures, which took effect on February 15, 2022 and replaced the previously issued Revised Cybersecurity Review Measures. Under the Measures, an “online platform operator” in possession of personal data of more than one million users must apply for a cybersecurity review if it intends to list its securities on a foreign stock exchange. The operators of critical information infrastructure and the online platform operators (collectively, the “Operators”) carrying out data processing activities that affect or may affect national security, shall conduct a cybersecurity review, and any online platform operator who controls more than one million users’ personal information must go through a cybersecurity review by the cybersecurity review office if it seeks to be listed in a foreign country. Pursuant to the Measures, we believe we are not subject to the cybersecurity review by the CAC, given that (i) we possess personal information of a relatively small number of users in our business operations as of the date of this prospectus, significantly less than one million users; and (ii) data processed in our business does not have a bearing on national security and thus shall not be classified as core or important data by the PRC authorities. We don’t believe that we are an Operator within the meaning of the Measures, nor do we control more than one million users’ personal information, and as such, we should not be required to apply for a cybersecurity review under the Revised Measures. Further, an expert interpretation of the Measures published at the CAC’s website on February 17, 2022 indicated no application review is required for operators that have been listed abroad before the implementation of the Revised Cybersecurity Measures. However, the Measures were just recently released and there is a general lack of guidance and substantial uncertainties exist with respect to their interpretation and implementation. For example, certain terms used in the Measures are not defined and require further clarification on their meaning. Whether the data processing activities carried out by traditional enterprises (such as food, medicine, manufacturing, and merchandise sales enterprises) are subject to such review and the scope of the review remain to be further clarified by the regulatory authorities in the subsequent implementation process.

The PRC government recently initiated a series of regulatory actions and statements to regulate business operations in China, including adopting new measures to extend the scope of cybersecurity reviews, cracking down on illegal activities in the securities market, and expanding the efforts in anti-monopoly enforcement. The PRC government is increasingly focused on data security. In July 2021, the CAC opened cybersecurity probes into several U.S.-listed technology companies focusing on anti-monopoly regulation, and how companies collect, store, process and transfer data. On November 14, 2021, the CAC published the Draft Regulations on Network Data Security Management in November 2021 for public comments, which among other things, stipulates that a data processor listed overseas must conduct an annual data security review by itself or by engaging a data security service provider and submit the annual data security review report for a given year to the municipal cybersecurity department before January 31 of the following year. If the Draft Regulations on Network Data Security Management are enacted in the current form, we, as an overseas listed company, would be required to carry out an annual data security review and comply with the relevant reporting obligations. As of the date of this prospectus, the draft regulations have been released for public comment only and have not been formally adopted. The final provisions and the timeline for its adoption are subject to changes and uncertainties. We have been closely monitoring the regulatory development in China, particularly regarding the requirements of approvals, annual data security review or other procedures that may be imposed on us. If any approval, review or other procedure is in fact required, we cannot assure our investors that we will be able to obtain such approval or complete such review or other procedure timely or at all. For any approval that we may be able to obtain, it could nevertheless be revoked and the terms of its issuance may impose restrictions on our operations and/or securities offerings. The PRC regulatory requirements with respect to cybersecurity and data security are constantly evolving and can be subject to varying interpretations and significant changes, resulting in uncertainties about the scope of our responsibilities in that regard. Failure to comply with these cybersecurity and data privacy requirements in a timely manner, or at all, may subject us to government enforcement actions and investigations, fines, penalties, suspension or disruption of our operations.

Because we are relying on advice of our PRC counsel with regard to PRC laws, there is uncertainty inherent in relying on an opinion of counsel in connection with whether we are required to obtain permissions from a governmental agency that is required to approve of our operations and/or listings. In the event that an government approval is required, we cannot assure our investor that we will be able to receive clearance in a timely manner, or at all. Any failure of us to fully comply with new regulatory requirements may significantly limit or completely hinder our ability to offer or continue to offer our common shares, cause significant disruption to our business operations, severely damage our reputation, materially and adversely affect our financial condition and results of operations and cause our shares to significantly decline in value or become worthless.

For more detailed information, see “Risk Factors-Risks Relating to Doing Business in China.”

The Holding Foreign Companies Accountable Act (“HFCAA”)

Our common shares may be prohibited from trading on a national exchange or “over-the-counter” markets under the HFCAA if the Public Company Accounting Oversight Board of the United States (“PCAOB”) determines it is unable to inspect or investigate completely our auditors for two consecutive years.

In recent years, U.S. regulatory authorities have continued to express their concerns about challenges in their oversight of financial statement audits of U.S.-listed companies with significant operations in China. As part of a continued regulatory focus in the United States on access to audit and other information, the Holding Foreign Companies Accountable Act, or the HFCAA, was enacted on December 18, 2020. The HFCAA includes requirements for the SEC to identify issuers whose audit work is performed by auditors that the PCAOB is unable to inspect or investigate completely because of a restriction imposed by a non-U.S. authority in the auditor’s local jurisdiction. The HFCAA also requires that, to the extent that the PCAOB has been unable to inspect an issuer’s auditor for three consecutive years since 2021, the SEC shall prohibit its securities registered in the United States from being traded on any national securities exchange or over-the-counter markets in the United States.

Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On August 26, 2022, the CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”), governing inspections and investigations of audit firms based in mainland China and Hong Kong. On December 15, 2022, the PCAOB determined that it was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and vacated its previous Determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination. On December 29, 2022, the Accelerating Holding Foreign Companies Accountable Act was signed into law as part of the Consolidated Appropriations Act, 2023, reducing the number of consecutive non-inspection years required for triggering the prohibitions under the HFCAA from three years to two. Our current auditor, YCM CPA Inc., headquartered in Irvine, California, is a firm registered with the PCAOB and is required by the laws of the U.S. to undergo regular inspections by the PCAOB to assess its compliance with the laws of the U.S. and professional standards. YCM CPA Inc. has been subjected to PCAOB inspections. Notwithstanding the foregoing, in the future, if it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, or if there is any regulatory change or step taken by PRC regulators that does not permit our auditors to provide audit documentations to the PCAOB for inspection or investigation, you may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected or investigated by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditors’ audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities, including trading on the national exchange or “over-the-counter” markets, may be prohibited under the HFCAA.

As a holding company, we may rely upon dividends paid to us by our subsidiaries in the PRC to pay dividends and to finance any debt we may incur. As of the date of this prospectus, none of our subsidiaries has issued any dividends or distributions to us and we have not made any dividends or distributions to our shareholders. Our subsidiaries in the PRC generate and retain cash generated from operating activities and re-invest it in our business.

Under BVI law, we may pay a dividend on our shares out of either profit, provided that in no circumstances may a dividend be paid if this would result in us being unable to pay our debts due in the ordinary course of business. If we determine to pay dividends, as a holding company, we will be dependent on receipt of funds from our subsidiaries in PRC through our Hong Kong subsidiaries.