Exhibit 99.1 SEACOR Marine Holdings Inc. st 31 Annual Pareto Securities Energy Conference SMHI LISTED John Gellert NYSE President & Chief Executive Officer 11 September 2024

Forward-Looking Statements Forward-Looking Statements discussed in this release as well as in other reports, materials and oral statements that SEACOR Marine Holdings Inc. (“SEACOR Marine” or the “Company”) releases from time to time to the public constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Generally, words such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “believe,” “plan,” “target,” “forecast” and similar expressions are intended to identify forward-looking statements and includes the information on Slide 26. Such forward- looking statements concern management's expectations, strategic objectives, business prospects, anticipated economic performance and financial condition and other similar matters. Forward- looking statements are inherently uncertain and subject to a variety of assumptions, risks and uncertainties such as the completion of our financial close process for the quarter, that could cause actual results to differ materially from those anticipated or expected by the management of the Company. These statements are not guarantees of future performance and actual events or results may differ significantly from these statements. Actual events or results are subject to significant known and unknown risks, uncertainties and other important factors, many of which are beyond the Company's control. It should be understood that it is not possible to predict or identify all such factors. Investors and analysts should not place undue reliance on forward-looking statements. Forward-looking statements speak only as of the date of the document in which they are made. The Company disclaims any obligation or undertaking to provide any updates or revisions to any forward-looking statement to reflect any change in the Company's expectations or any change in events, conditions or circumstances on which the forward-looking statement is based, except as required by law. It is advisable, however, to consult any further disclosures the Company makes on related subjects in its filings with the U.S. Securities and Exchange Commission, including Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K (if any). These statements constitute the Company's cautionary statements under the Private Securities Litigation Reform Act of 1995. Non-GAAP Financial Measures This presentation includes certain non-GAAP financial measures. Direct Vessel Profit (defined as operating revenues less operating costs and expenses including major repairs and drydocking expenses, “DVP”), when applied to individual vessels, fleet categories or the combined fleet. DVP is a critical financial measure used by the Company to analyze and compare the operating performance of its individual vessels, fleet categories, regions and combined fleet, without regard to financing decisions (depreciation for owned vessels vs. leased-in expense for leased-in vessels). DVP is also useful when comparing the Company’s fleet performance against those of our competitors who may have differing fleet financing structures. DVP has material limitations as an analytical tool in that it does not reflect all of the costs associated with the ownership and operation of our fleet, and it should not be considered in isolation or used as a substitute for our results as reported under GAAP. Adjusted EBITDA is defined as DVP less general and administrative expenses and lease expenses. We believe that the presentation of Adjusted EBITDA provides useful information to investors and management uses it to assess our on-going operations. Our use of Adjusted EBITDA should not be viewed as an alternative to measures calculated in accordance with GAAP. Adjusted EBITDA has limitations as analytical tool such as: (i) Adjusted EBITDA does not reflect the impact of earnings or charges that we consider not to be indicative of our on-going operations, (ii) Adjusted EBITDA does not reflect interest and income tax expense; and (iii) other companies, including other companies in our industry, may calculate Adjusted EBITDA differently than we do. Net Debt is defined as total debt (the most comparable GAAP measure, calculated as long-term debt plus current portion of long-term debt excluding discount and issuance costs) less cash and cash equivalents (including restricted cash). We believe that the presentation of Net Debt provides useful information to investors and management uses it to compare total debt less cash and cash equivalents across periods on a consistent basis. Reconciliation for each of these non-GAAP measures are included as an appendix to this presentation. seacormarine.com 2

1. Company Overview seacormarine.com 3

SEACOR Marine – Global OSV Owner with Modern Fleet Company Overview Global Presence • Leading provider of marine and support transportation services to offshore energy facilities worldwide with one of the youngest fleets in the industry Middle East & Asia (1) • Listed on the NYSE (ticker: SMHI) with a market capitalization of $273.9M 15 vessels West Africa & Europe • Operates and manages a diverse fleet of 56 offshore support vessels (“OSVs”) that 22 vessels 10 vessels provides crew transportation, supply, accommodation and maintenance support United States 9 vessels Latin America • U.S. Jones Act operator with presence in all major offshore basins, serving a diverse range of customers in the oil and gas and offshore wind sectors • Early adopter of value-added technology (hybrid power, walk-to-work, etc.) to enhance sustainable operations SEACOR Marine (2) (2) Company Highlights Fleet Composition Region / Asset Type PSV FSV Liftboat AHTS United States 2 3 5 - Contract Backlog Stewards of Capital and Energy Efficiency and CO Latin America 6 2 1 - 2 > $400.0M (incl. options) Operational Excellence Emission Reduction Africa & Europe 8 11 - 3 Cash & Cash Equivalents• Disciplined capital• 7 hybrid PSVs Middle East & Asia 5 7 2 1 $42.9M Total 21 23 8 4 • Continued deleveraging• 4 hybrid systems on order (3) Net Debt 56 Vessels – Average Age of 10.1 Years • Safety first culture• Offshore wind support $296.1M 40 international flag / 16 US flag (Jones Act compliant) (1) Bloomberg, as of market close on September 9, 2024. (2) Company Highlights and Fleet Composition as of June 30, 2024. Fleet count includes 1 managed vessel and 1 leased-in vessel as of June 30, 2024. seacormarine.com 4 (3) Net Debt is a non-GAAP financial measure. See Slide 2 for a discussion of Net Debt and the Appendix to this presentation for a reconciliation to GAAP.

High-Quality and Youngest Fleet of any Peer Competitor Platform Supply Vessels (PSV) Work Scope • Shallow water and deepwater activities • 21 vessels • Delivery of cargo, drilling fluids, fuel and water to rigs • Average age of 7.0 years 2 • Construction, maintenance support and standby • 11 vessels with deck space > 800m (average age of 5.4 years) • Accommodation and walk-to-work • 7 with hybrid power, 4 additional hybrid systems on order • Offshore wind support Fast Support Vessels (FSV) • High-speed cargo transport to offshore facilities • 23 vessels (1 managed) • Transport of personnel at high-speed and comfort, walk-to-work capable • Average age of 11.0 years • High-speed cargo transport to offshore facilities • Aluminum monohulls or catamarans, up to 150 passengers • Support drilling and production operations • DP-2 or DP-3, 30-40 knots speed • Emergency response services Liftboats • Self-elevating, self-propelled work platforms • 8 vessels • Accommodation • Average age of 13.2 years (9.5 years for premium liftboats) • Well workover, maintenance and well production enhancement • Working water depth up to 275 feet • Decommissioning, plug and abandonment • Accommodation up to 150 berths • Offshore wind support in the U.S. • Midstream: commissioning and repair of pipelines and offshore gas facilities Anchor Handling Tug & Supply (AHTS) • Offshore drilling support by towing, positioning, mooring rigs • 4 vessels (1 leased-in) • Carry and launch equipment such as remote operated vehicles • Average age of 15.2 years • Transportation of drilling fluids and bulk products • 7,000 to 11,000 BHP, 120t + Bollard Pull • Emergency response services • DP-2 seacormarine.com 5

Revenue Diversification With a Reputable Customer Base (1) (2) 2023 Total Revenue Main Customers High-Quality Customers % of FY 2023 Customer Name Total Revenue 6% 70% 0% ExxonMobil 17% United States United States $61M Saudi Aramco 15% $60M (primarily Gulf of Mexico) (primarily Gulf of Mexico) 10% Azule Energy 15% (BP / ENI Joint Venture) 14% Ørsted 6% PSV FSV Liftboat AHTS Other Total Chevron 6% QatarEnergy 4% MexMar 3% APA Corporation 3% 4% 1% 15% 0% 80% Fugro 2% $44M Latin America Latin America $59M Van Oord 2% PSV FSV Liftboat AHTS Other Total Top 10 customers account for 73% of FY 2023 Revenues (3) 0% 10% Total Revenue by Type 48% 0% $60M Africa & Europe Africa & Europe 42% $90M Other 5% Offshore Wind PSV FSV Liftboat AHTS Other Total 10% Independents IOCs 10% 42% 0% 2% 48% $53M 31% Offshore Contractors Middle East & Asia Middle East & Asia $71M NOCs 12% 19% 22% PSV FSV Liftboat AHTS Other Total (1) For the twelve months ended December 31, 2023. For continuing operations. Numbers in percentage of Total Revenue per respective geography. (2) Main Customers may be direct or indirect end-users. seacormarine.com 6 (3) For FY 2023.

2. Market Outlook seacormarine.com 7

Strong Industry Fundamentals – Increased Demand Drivers Growing Global Offshore Upstream Capital Expenditures Robust Global Offshore Project Sanctioning Pipeline $300M $200M 174 $180M 246 164 162 241 $250M 230 229 $160M 147 218 146 208 209 138 136 $140M $200M 185 119 $120M 107 166 122 90 137 110 105 103 131 101 74 101 139 139 73 $150M $100M 74 120 94 83 79 109 82 $80M 81 56 72 71 $100M $60M 49 46 120 $40M 119 114 74 109 73 106 $50M 67 98 65 63 88 59 85 52 75 67 68 45 $20M 38 35 33 $M $M 2020 2021 2022 2023 2024E 2025E 2026E 2027E 2028E 2029E 2030E 2020 2021 2022 2023 2024E 2025E 2026E 2027E 2028E 2029E 2030E Shelf Deepwater Shelf Deepwater Source: Rystad Energy. seacormarine.com 8 8

Sustained Growth in OSV Demand – Tight Supply / Demand Balance Growing OSV Demand Comments Active > PSV 1,000+ DWT & AHTS 4,000+ BHP• OSV demand progress was evident on a global basis in 2023, with tangible improvement in all regional markets 3,000 ~13% • PSV demand has improved at a faster rate than other asset classes against the backdrop of higher activity in the Gulf of 2,500 Mexico, Brazil and West Africa (the “Golden Triangle”) • Development of new areas requiring more vessels (e.g. Guyana, 2,000 Suriname, Namibia, Mozambique) • Total OSV demand is expected to continue its growth in the 3,033 1,500 2,898 coming years with limited additional supply, further tightening the 2,737 2,746 2,648 2,511 2,500 chartering market 2,439 2,259 2,230 2,208 2,022 2,032 1,000 2,012 • From 2023 to 2026, OSV demand is expected to increase by ~13% 500 - 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024E 2025E 2026E Active OSVs Forecast Source: Clarksons Research Services. seacormarine.com 9

Supply Side Constraints Remain Aging Stacked Fleet Limited Supply 1,400 70% 250 12% 571 stacked OSVs per FYE 2023 Total OSV Fleet of 3,431 vessels per FYE 2023 10% 1,200 60% 200 8% 1,000 50% 150 6% 800 40% 100 4% 600 30% 50 2% 400 20% 0 0% 200 10% -50 -2% 0 0% -100 -4% 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 AHTS Attrition & Conversion PSV Attrition & Conversion Stacked < 1 Year Stacked 1-2 Years AHTS Deliveries PSV Deliveries Stacked 2-3 Years Stacked > 3 Years % of Fleet Stacked > 3 Years (rhs) % of OSV Fleet Stacked (rhs) Fleet Growth (rhs) Limited orderbook, constrained financing and continued development of local cabotage leads to a favorable supply and demand balance Source: Clarksons Research Services. seacormarine.com 10 Number of Vessels Number of Vessels

Tight Supply / Demand Balance Leads to Improved Pricing and Utilization Global PSV Average Day Rates Global PSV Average Utilization $45,000 100% $40,000 90% $35,000 $30,000 80% $25,000 70% $20,000 $15,000 60% $10,000 50% $5,000 $0 40% PSV 3,200 DWT Time Charter Rate PSV 4,000 DWT Time Charter Rate PSV 3,000 - 4,000dwt PSV 4,000dwt + Contracting terms and duration improve in addition to PSV average day rates and utilization Source: Clarksons Research Services. seacormarine.com 11

FSVs – SMHI Owns Highest Specification Fleet SMHI owns 27% of the active global fleet of DP-2 / DP-3 FSVs of 15 years of age and younger Key Attributes Global Fleet Overview • FSVs are crucial for offshore drilling and production logistics, providing fast and flexible transport solutions 195 3 • Cost-efficient, comfortable, flexible and safe alternative to helicopter transportation 87 11 • Large passenger transport capacities: up to 150 passengers with amenities 85 7 like reclining business-class seats, satellite TV, wireless internet and LED 43 2 lighting • Advanced technologies include DP-2, Dynamic Ride Control, Controllable Speed Propellers, Water Jet Propulsion and Engine Monitoring Systems Global FSV Fleet • Cargo capacities range from 140 to 425 long tons for various supplies SEACOR Marine FSV Fleet • High-speed catamarans in the fleet can reach up top 40 knots, featuring luxury amenities and equipped with DP-2 or DP-3 options for specific 27% SMHI owns 27% operational needs SEACOR Marine of the active global fleet of DP-2 / DP-3 Other FSVs of 15 years of age and younger 73% Source: SEACOR Marine Holdings Inc., Clarksons Research Services Ltd., Clarksons Securities AS. seacormarine.com 12

FSVs – Tight Supply & Demand Balance Favorable supply dynamics with orderbook standing at ~1% Crew Transportation at High Speed and in Comfort Orderbook at ~1% with Limited Fleet Growth FSV Orderbook OB as % of total fleet Fleet growth (YoY) • Market is dominated by the U.S. and Mexico, followed by West Africa and the 80 45% Middle East 35% 60 25% • Demand drivers: 40 ✓ Cost efficiency 15% 20 ✓ Safety 5% ✓ Service requirement - (5%) ✓ Alternative to helicopters 2007 2009 2011 2013 2015 2017 2019 2021 2023 • Distinctive features of SMHI’s fleet, which holds a strong market position in FSV Supply Side Considerations the high-end FSV market: • Most of the fleet was ordered and built during the previous cycle, with the ✓ Speed (30-40 knots) ✓ Dynamic Positioning (DP-2 / DP-3) orderbook peaking at 33% of the fleet in 2007 and decreasing to 1% by 2024 ✓ Comfort & onboard entertainment • Fleet growth has been negative or zero since 2019, and the current fleet ✓ Jet propulsion consists of about 410 vessels: 208 non-DP, 98 DP-1, 100 DP-2 and 3 DP-3 • The average age of the total fleet is 15 years, with the non-DP fleet averaging closer to 19 years • Limited technologies available to meet speed and emission standards create barriers for new tonnage Source: SEACOR Marine Holdings Inc., Clarksons Research Services Ltd., Clarksons Securities AS. seacormarine.com 13 No units in Orderbook Orderbook / Fleet Growth

Liftboats – Key Component to Address Legacy Offshore Infrastructure SMHI Owns highest specification fleet for U.S. Jones Act Market – Including Largest and Newest Units Global Fleet Overview Key Attributes • They provide a stable base for offshore oil and gas operations, including well intervention, maintenance and construction activities 140 6 • Equipped with cranes, living quarters, and other facilities, liftboats support 95 2 personnel and equipment for various tasks 147 0 • In the renewable energy sector, liftboats are used for the installation, 2 0 maintenance, and repair of offshore wind turbines • Their ability to operate in shallow waters and their mobility enhance Global Liftboat fleet operational efficiency and safety SEACOR Marine Liftboat fleet Liftboats Scope of Work Offshore Wind Offshore Oil and Natural Gas ✓ Well intervention and workover ✓ Tower Sections - Installation ✓ Construction, Maintenance, Repair ✓ Export Cables ✓ Subsea operations ✓ Offshore Substation ✓ Diving operations ✓ Array Cables ✓ Accommodations ✓ Commissioning ✓ Decommissioning, Plug & Abandonment ✓ Site Preparation ✓ Coring ✓ Accommodation ✓ Midstream support Source: SEACOR Marine Holdings Inc., Clarksons Research Services Ltd., Clarksons Securities AS. seacormarine.com 14

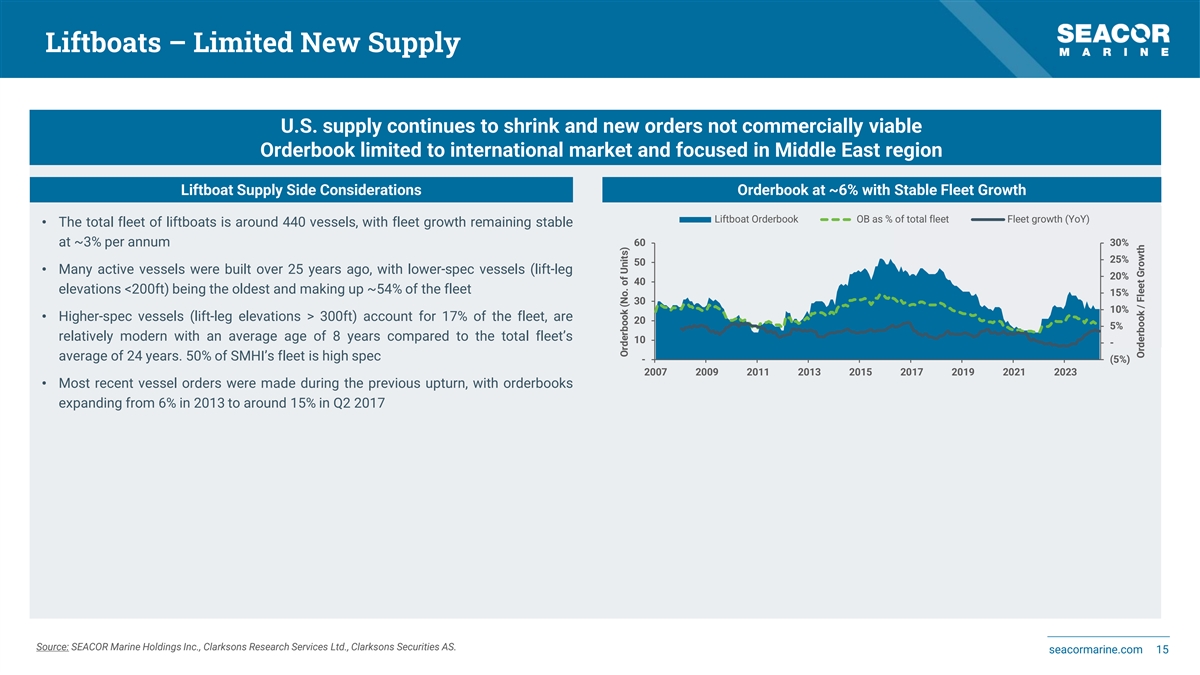

Liftboats – Limited New Supply U.S. supply continues to shrink and new orders not commercially viable Orderbook limited to international market and focused in Middle East region Liftboat Supply Side Considerations Orderbook at ~6% with Stable Fleet Growth Liftboat Orderbook OB as % of total fleet Fleet growth (YoY) • The total fleet of liftboats is around 440 vessels, with fleet growth remaining stable at ~3% per annum 60 30% 25% 50 • Many active vessels were built over 25 years ago, with lower-spec vessels (lift-leg 20% 40 elevations <200ft) being the oldest and making up ~54% of the fleet 15% 30 10% • Higher-spec vessels (lift-leg elevations > 300ft) account for 17% of the fleet, are 20 5% relatively modern with an average age of 8 years compared to the total fleet’s 10 - average of 24 years. 50% of SMHI’s fleet is high spec - (5%) 2007 2009 2011 2013 2015 2017 2019 2021 2023 • Most recent vessel orders were made during the previous upturn, with orderbooks expanding from 6% in 2013 to around 15% in Q2 2017 Source: SEACOR Marine Holdings Inc., Clarksons Research Services Ltd., Clarksons Securities AS. seacormarine.com 15 Orderbook (No. of Units) Orderbook / Fleet Growth

Liftboats – U.S. Delayed Activity = Pent Up Demand Legacy Oil & Natural Gas Market U.S. Offshore Wind and Other New Markets • Multi-year deferrals in Decommissioning and Plug & Abandonment activity in • Increased focus on methane emissions lead to additional maintenance the US GOM should translate into much higher levels of activity. and repair work • Customer base in the US is financially resilient again, with IOC’s or stronger • Liftboats should participate in upcoming carbon capture and storage independents taking over assets and willing to address asset removal projects obligations • Liftboats business should indirectly benefit from legislative incentives in the Inflation Reduction Act U.S. Offshore Wind Forecast Almost 1/3 of 53% of U.S. fixed structures 35 2,500 ~60% of 334 structures 32 in the U.S. GoM offshore wells are abandoned with submitted 30 are located in 2,000 wells are decommissioning permanently 25 terminated 21 unplugged applications abandoned 1,500 20 17 17 leases 13 15 1,000 10 10 7 500 4 4 5 2 0 0 Active US Wind Farms (LHS) Active US Turbines (RHS) Source: Bureau of Ocean Energy Management, Bureau of Safety and Environmental Enforcement, U.S. Government Accountability Office. seacormarine.com 16 # of Active US Wind Farms # of Active US Turbines

3. Financial & Operational Highlights seacormarine.com 17

Financial Highlights FY 2023 LTM (through Q2 2024) FY 2022 (1) Fleet Count / Average Age 60 / 8.6 years 58 / 9.4 years 56 / 10.1 years Fleet Average Utilization 75% 69% 75% $12,673 $18,530 Fleet Average Day Rate $16,375 $282.6M Revenues $217.3M $279.5M (2) Direct Vessel Profit $101.6M $45.3M $119.9M (3) Adjusted EBITDA $0.6M $67.9M $52.6M Q2 2024 saw continued repricing of the fleet at significantly improved day rates while working through a period of lower utilization, driven by planned drydockings and major repairs (1) Fleet Count and Average Age includes 2 managed vessels and 3 leased-in vessels in 2022, 3 managed vessels and 1 leased-in vessel in 2023, 1 managed vessel and 1 leased-in vessel as of June 30, 2024. (2) Direct Vessel Profit is a non-GAAP financial measure. See Slide 2 for a discussion of Direct Vessel Profit and the Appendix to this presentation for a reconciliation to GAAP. seacormarine.com 18 (3) Adjusted EBITDA is a non-GAAP financial measure. See Slide 2 for a discussion of Adjusted EBITDA and the Appendix to this presentation for a reconciliation to GAAP.

Sustained Growth in Total Revenue and Direct Vessel Profit (1) Total Revenue, DVP & DVP Margin Comments 50% • Improving day rates and utilization leading to sustained revenue growth over the last $280M 43% four years 36% $240M 40% 36% $200M 30% 25% $160M• DVP growth exceeding 150% year-on-year from 2022 to 2023, and establishing a $283M $280M baseline over LTM through Q2 2024 despite lower activity during the winter months $120M 20% 21% $217M $171M $80M $142M $120M 10% $102M $40M • DVP margin impacted in H1 2024 due to increased drydocking activity $51M $44M $45M $0M 0% 2020 2021 2022 2023 LTM through Q2 2024 • Continued deleveraging of the balance sheet, coupled with a comfortable liquidity position Total Revenue DVP DVP Margin Total Debt, Cash & Cash Equivalents & Equity Ratio• Maintaining adequate capitalization with an equity ratio of 47% in Q2 2024 $600M 60% 49% 48% Direct Vessel Profit (“DVP”) is defined as operating revenues less operating costs and 47% 47% $500M 50% expenses (including major repairs and drydocking expenses) and is a critical financial 39% $400M 40% measure used by SMHI to analyze and compare the operating performance of its business segments without regard to financing (Adjusted EBITDA is DVP less SG&A and Lease $300M 30% $522M Expenses). $200M 20% $401M $364M $353M $339M $84M $100M 10% $43M $43M $41M $36M Contrary to most peer companies, SMHI fully expenses maintenance and drydocking costs, $0M 0% 2020 2021 2022 2023 Q2 2024 resulting in reduced DVP and Adjusted EBITDA figures. Total Debt Cash & Cash Equivalents Equity Ratio (1) Direct Vessel Profit is a non-GAAP financial measure. See Slide 2 for a discussion of Direct Vessel Profit and the Appendix to this presentation for a reconciliation to GAAP. seacormarine.com 19

Illustrative Operating Leverage – Adjusted EBITDA Sensitivity The following information represents potential Annual Revenue and Adjusted EBITDA outcomes under different average fleet day rate and/or utilization environments, calculated assuming for these purposes: (i) our LTM through Q2 2024 Average Fleet Utilization of 69% and illustrative Fleet Utilization of 80%; (ii) our FY 2023 Bareboat Charter and Other Marine Services of $28.1M; (iii) our FY 2023 General & Administrative and Lease Expenses of $51.9M; and (iv) our FY 2023 Operating Expenses (including Major Repairs and Drydocking Expenses) of $159.7M. The following does not represent SEACOR Marine’s guidance or projections for potential results for 2024 or any other period and should not be relied on as such. Actual FY 2024 financial results may materially differ from prior periods and the information set forth below. Annual Revenue (in $M) 280 299 304 311 318 325 332 339 346 353 (1) Net Debt / Adjusted EBITDA 4.3x 3.4x 3.2x 3.0x 2.8x 2.6x 2.5x 2.3x 2.2x 2.1x $220M 194 ~10% increase in Day Rates from Q2 2024 $200M 185 177 $180M 169 161 153 $160M 144 142 69% Fleet Utilization 136 135 $140M 130 128 (LTM through Q2 2024) 121 114 $120M 106 99 80% Fleet Utilization 92 $100M 87 85 (Illustrative) $80M 68 Adjusted EBITDA 2023 $60M (75% Fleet Utilization) $40M $20M $0M (2) $16,375 $19,141 $19,500 $20,000 $20,500 $21,000 $21,500 $22,000 $22,500 $23,000 Average Fleet Day Rate High operating leverage for any incremental percentage in fleet utilization and/or growth in day rates Note: Based on an average fleet of 56 vessels. (1) Net Debt and Adjusted EBITDA are non-GAAP financial measures. See Slide 2 for a discussion of Net Debt and Adjusted EBITDA and the Appendix to this presentation for a reconciliation to GAAP. seacormarine.com 20 (2) Average Fleet Day Rate in FY 2023. Annual EBITDA

Sound Capital Structure (1) Total Debt Maturity Profile Existing Debt Facilities $160M $152M SEACOR Marine Foreign Holdings Inc. - due September 2028 • Amount Outstanding: $112.9M • Security: 27x OSVs (8x PSVs, 15x FSVs, 2x Liftboat, 2x AHTSs) $140M $35M • Pricing: 11.75% p.a. $120M SEACOR Alpine LLC - due June 2028 $110M • Amount Outstanding: $23.9M • Security: 3x PSVs $100M • Pricing: 10.25% p.a. SEACOR Delta Shipyard Financing - due 2028/2029 $80M • Amount Outstanding: $64.2M • Security: 8x PSVs $90M • Pricing: LIBOR + 4.00% p.a. $98M $60M Sea-Cat Crewzer III - due July 2029 • Amount Outstanding: $13.0M $40M • Security: 2x FSVs • Pricing: 2.76% p.a. $20M $6M $28M $29M $27M $27M $12M $0M Guaranteed Notes - due July 2026 2024 2025 2026 2027 2028 2029 • Amount Outstanding: $90.0M • Security: Unsecured, Negative Pledge on 1x Liftboat (LB Robert) Principal Instalments Balloon Guaranteed Notes Convertible Notes• Pricing: 8.00% Cash or 9.50% Hybrid (4.25% Cash + 5.25% PIK) Convertible Notes - due July 2026 • Amount Outstanding: $35.0M Fiscal Year End 2023 2024 2025 2026 2027 2028 2029 • Security: Unsecured • Pricing: 4.25% p.a. (Conversion price of $11.75 per share) Total Debt Outstanding ($M) 353.0 324.7 296.1 143.6 116.5 6.2 0.0 (1) Amounts outstanding under the various debt facilities as of June 30, 2024. seacormarine.com 21 Unsecured Debt Secured Debt

3. Appendix seacormarine.com 22

Fleet Maintenance and Capital Expenditures Historical Major Repairs and Drydocking Expenses SMHI Fleet Age Profile $25M Near-term increased level of Major Repairs and Drydocking Expenses given the fleet’s age profile 5-year, 10-year and 15-year surveys due in 2024 8 8 result in higher than usual maintenance activity 7 $20M 5 5 5 $15M 4 $10M 20 17 2 2 2 2 11 $5M 1 1 1 1 1 1 8 8 7 5 $0M 2018 2019 2020 2021 2022 2023 H1 2024 Capital Expenditures for Vessel Upgrades as of June 30, 2024 Unfunded Capital Commitments H2 2024 2025 Deferred Hybrid battery power systems – 4x PSVs $6.1M $4.0M - DP-2 upgrade – 1x Liftboat $0.3M $1.3M - Miscellaneous Equipment $0.5M - - New construction – 1x FSV (deferred indefinitely) - - $9.2M Total $6.9M 5.3M $9.2M seacormarine.com 23

Financials – Income and Loss Statement Income & Loss Statement (in $ thousands) H1 2024 FY 2023 FY 2022 Operating Revenues 132,637 279,511 217,325 Costs and Expenses: Operating 97,619 159,650 171,985 Administrative and General 22,806 49,183 40,911 Lease Expense 967 2,748 3,869 Depreciation and Amortization 25,821 53,821 55,957 147,213 265,402 272,722 Gains (Losses) on Asset Dispositions and Impairments, Net 36 21,409 1,398 Operating Income (Loss) (14,540) 35,518 (53,999) Other Income (Expense): Interest Income 1,038 1,444 784 Interest Expense (20,499) (37,504) (29,706) Gain on Debt Extinguishment - (2,004) 10,429 Derivative Gains, Net (439) 608 - Foreign Currency Losses, Net (640) (2,133) 1,659 Gain (Loss) from Return of Investments in 50% or Less Owned Companies and Other, Net (95) - 755 (20,635) (39,589) (16,079) Income (Loss) from Continuing Operations Before Tax Expense (Benefit) and Equity in Earnings (Losses) of 50% or Less Owned Companies (35,175) (4,071) (70,078) Income Tax Expense (Benefit): Current 5,878 13,860 8,485 Deferred (5,635) (5,061) 97 (243) 8,799 8,582 Income (Loss) Before Equity in Earnings (Losses) of 50% or Less Owned Companies (35,418) (12,870) (78,660) Equity in Earnings (Losses) of 50% or Less Owned Companies, Net of Tax (134) 3,556 7,011 Income (Loss) (35,552) (9,314) (71,649) Net Income (Loss) Attributable to Noncontrolling Interests in Subsidiaries - - (1) Net Income (Loss) attributable to SEACOR Marine Holdings Inc. (35,552) (9,314) (71,650) Source: Company filings. seacormarine.com 24

Financials – Balance Sheet and Debt Overview Balance Sheet (in $ thousands) Debt Overview (as of June 30, 2024) ASSETS H1 2024 FY 2023 FY 2022 Final Principal Debt Facility Maturity Outstanding ($M) Current Assets: Cash and Cash Equivalents, including Restricted Cash 42,860 84,131 43,045 Guaranteed Notes July 2026 90.0 Other Current Assets 87,239 80,555 89,268 Total Current Assets 130,099 164,686 132,313 (1) New Convertible Notes July 2026 35.0 Property and Equipment, net of Depreciation 571,644 594,682 656,905 Unsecured Debt – Sub-Total 125.0 Construction in Progress 11,518 10,362 8,111 SEACOR Alpine Credit Facility June 2028 23.9 Net Property and Equipment 583,162 605,044 665,016 Leases and Other Assets 8,305 10,606 18,038 2023 SMFH Credit Facility September 2028 112.9 Total Assets 721,566 780,336 815,367 Sea-Cat Crewzer III Term Loan Facility July 2029 13.0 LIABILITIES AND EQUITY H1 2024 FY 2023 FY 2022 SEACOR Delta Shipyard Financing February 2029 64.2 Current Liabilities: Current Portion of Lease Liabilities 887 1,626 2,826 Secured Debt – Sub-Total 214.0 Current Portion of Long-Term Debt 28,605 28,365 61,512 Other Current Liabilities 41,585 47,095 56,824 Total Debt 339.0 Total Current Liabilities 71,077 77,086 121,162 (2) Discount / Issuance Costs (32.6) Long-Term Lease Liabilities 3,281 3,535 11,520 Total Debt net of Discount / Issuance Costs 306.4 Long-Term Debt 277,740 287,544 260,119 Other Long-Term Liabilities 31,530 37,947 43,420 Total Liabilities 383,628 406,112 436,221 Total Equity 337,938 374,224 379,146 Total Liabilities and Equity 721,566 780,336 815,367 (1) Conversion Price of $11.75 per share. (2) Debt discounts and costs incurred in connection with the issuance of debt are amortized over the life of the related debt using the effective interest rate method for term loans and straight-line method for revolving credit facilities and are included in interest expense in the accompanying consolidated statements of income (loss). seacormarine.com 25 Source: Company filings.

Financials – Cash Flow Statement (1/2) Cash Flow Statement (in $ thousands) H1 2024 FY 2023 FY 2022 Cash Flows from Continuing Operating Activities: Net Income (Loss) (35,552) (9,314) (71,649) Adjustments to Reconcile Net Income (Loss) to Net Cash Provided by (used in) Operating Activities: Depreciation and Amortization 25,821 53,821 55,957 Debt Discount and Deferred Financing Cost Amortization 4,511 8,340 6,701 Stock-based Compensation Expense 3,232 6,000 4,597 Allowance for Credit Losses 42 3,519 489 (Gains) Losses from Equipment Sales, Retirements or Impairments, Investments in 50% or Less Owned Companies (36) (21,409) (1,398) (Gain) Loss on Debt Extinguishment - 177 (12,700) Derivative (Gains) Losses 439 (608) - Interest on Finance Lease 1 202 244 Settlements on Derivative Transactions, Net 164 577 (749) Currency (Gains) Losses 640 2,133 (1,659) Deferred Income Taxes (5,635) (5,061) 97 Equity (Earnings) Losses 134 (3,556) (7,011) Dividends Received from Equity Investees 1,418 2,241 3,057 Changes in Operating Assets and Liabilities: Accounts Receivables (2,637) (17,215) (652) Other Assets (3,685) 2,288 2,559 Accounts Payable and Accrued Liabilities (8,273) (13,188) 7,501 Net Cash provided by (used in) Operating Activities (19,416) 8,947 (14,616) Cash Flows from Continuing Investing Activities: Purchases of Property and Equipment (4,074) (10,604) (462) Proceeds/Cash Impact from Disposition/Sale of Property and Equipment 86 44,730 6,734 Cash Flow related to Investments in 50% or Less Owned Companies and Equity Investees - - 66,528 Notes Due from Others - - (28,831) Principal Payments on Notes due from Others - 15,000 13,831 Net Cash provided by Investing Activities (3,988) 49,126 57,800 Source: Company filings. seacormarine.com 26

Financials – Cash Flow Statement (2/2) Cash Flow Statement (in $ thousands) H1 2024 FY 2023 FY 2022 Cash Flows from Continuing Financing Activities: Payments on Long-Term Debt (14,063) (29,165) (38,152) Payments on Debt Extinguishment - (131,604) - Payments on Debt Extinguishment Costs - (1,827) (2,271) Proceeds from issuance of Long-Term Debt, net of Issue Costs - 148,475 - Proceeds from issuance of Common Stock, net of Issue Costs - 24 - Proceeds from Exercise of Stock Options and Warrants 102 6 151 Payments on Finance Lease (18) (531) (351) Acquisition of Common Shares for Tax Withholding Obligations (3,889) (2,368) (732) Net Cash used in Financing Activities (17,868) (16,990) (41,355) Effects of Exchange Rates 1 3 (4) Net Increase (Decrease) in Cash, Cash Equivalents and Restricted Cash (41,271) 41,086 1,825 Cash, Cash Equivalents and Restricted Cash, Beginning of Period 84,131 43,045 41,220 Cash, Cash Equivalents and Restricted Cash, End of Period 42,860 84,131 43,045 Source: Company filings. seacormarine.com 27

Financial Reconciliations Adjusted EBITDA Reconciliation (in $ thousands) H1 2024 FY 2023 FY 2022 Net Income (Loss) attributable to SEACOR Marine Holdings Inc. (35,552) (9,314) (71,650) Depreciation and Amortization 25,821 53,821 55,957 Interest Expense 20,499 37,504 29,706 Interest Income (1,038) (1,444) (784) Taxes 243 8,799 8,562 Earnings before Interest, Taxes, Depreciation and Amortization (EBITDA) 9,973 89,366 21,811 (Gains) Losses on Asset Dispositions and Impairments, Net (36) (21,409) (1,398) (Gains) Losses on Debt Extinguishment - 2,004 (10,429) Derivative (Gains) Losses, Net 439 (608) - Foreign Currency (Gains) Losses, Net 640 2,133 (1,659) Other, Net 95 - (755) Equity in (Earnings) Losses Earnings of 50% or Less Owned Companies 134 (3,556) (7,011) Net Income (Loss) attributable to Noncontrolling Interests in Subsidiaries - - 1 Adjusted EBITDA 11,245 67,930 560 DVP Reconciliation (in $ thousands) H1 2024 FY 2023 FY 2022 Operating Income (Loss) (14,540) 35,518 (53,999) (Gains) Losses on Asset Dispositions and Impairments, Net (36) (21,409) (1,398) Depreciation and Amortization 25,821 53,821 55,957 Lease Expense 967 2,748 3,869 Administrative and General 22,806 49,183 40,911 Direct Vessel Profit (DVP) 35,018 119,861 45,340 Source: Company filings. seacormarine.com 28

Financial Reconciliations (continued) DVP to Adjusted EBITDA Reconciliation (in $ thousands) H1 2024 FY 2023 FY 2022 Operating Revenues 132,637 279,511 217,325 Operating Expenses 97,619 159,650 171,985 Direct Vessel Profit (DVP) 35,018 119,861 45,340 Administrative and General 22,806 49,183 40,911 Lease Expense 967 2,748 3,869 Adjusted EBITDA 11,245 67,930 560 Net Debt Reconciliation (in $ thousands) H1 2024 FY 2023 FY 2022 Current Portion of Long-Term Debt 28,605 28,365 61,512 Long-Term Debt 277,740 287,544 260,119 Discount and Issuance Costs 32,617 37,115 42,163 Total Debt 338,962 353,024 363,794 Cash and Cash Equivalents, including Restricted Cash 42,860 84,131 43,045 Net Debt 296,102 268,893 320,749 Source: Company filings. seacormarine.com 29

Strong Commitment to ESG Our Values and Responsible Business Practices Second Sustainability Report (2022/2023) SEACOR Marine works towards aligning its goals with: • United Nations Sustainable Development Goals (“SDGs”) Local • United Nations Global Compact – Economic Decarbonizing Empowerment Operations Sustainable Ocean Principles Diversity, • Paris Climate Accord; and Anti-Corruption Equity & Inclusion • Frameworks provided by the: • Sustainability Accounting Standards Human Health and Safety Board (“SASB”) Rights • Task Force on Climate-Related Financial Disclosures (“TCFD”) Ocean Responsible Health Procurement Ethical • Global Reporting Initiative (“GRI”) Operations SEACOR Marine – Winner of the 2024 OSJ ESG Award • Recognizes the positive impact of SEACOR Marine’s environmental, social and governance (“ESG”) program Source: Company’s 2022/2023 Sustainability Report. seacormarine.com 30

Advancing Our ESG Program Notable Highlights from our 2022/2023 Sustainability Report 1 Completed pilot project implementing direct (Scope 1) emissions tracking on select vessels and data collection for indirect (Scope 2) emissions 2 Introduced a carbon intensity indicator (“CII”) metric on select vessels 3 Supported one of the largest offshore wind projects under development in the U.S. (South Fork), located off the coast of Long Island, New York 4 Completed implementation of Safe Water on Board (“SWOB”) on select vessels as part of our pilot project to reduce plastic waste 5 Published our Supplier Code of Conduct and developed our Responsible Procurement Policy 6 Published our Diversity, Equity and Inclusion (“DE&I”) Statement 7 Created sub-committees and working groups in support of sustainability and ESG oversight responsibilities of the Board of Directors 8 Continued development of our Compliance Training Program, including the addition of courses on sustainability, environmental protection and DE&I Source: Company’s 2022/2023 Sustainability Report. seacormarine.com 31

Case Study: Ongoing ESG Initiatives Across the Fleet Investments in Energy Storage Systems Cooperation with Spinergie Potential Future Projects • 7 of SMHI’s 11 most modern PSVs are now hybrid• SMHI is working marine technology firm Spinergie Carbon Capture (France) to analyze fleet data with the goal to optimize • PSV “SEACOR Yangtze” completed its upgrades in Q1 operations• SMHI is in discussion with Value Maritime (Netherlands) 2024, including: • Spinergie developed their “Smart Fleet Management” • Value Maritime has developed the “Filtree System”, an • Installation of an energy storage system platform, an AI powered and data-driven platform to onboard carbon capture system for small and medium- • Upgrade of a closed bus-tie system analyze large amounts of data in a concise manner sized vessels • Installation of a shore tie connection • DP system upgrade• SMHI currently tracks its entire fleet, and developed an • The system includes a small plug and play gas cleaning intelligent fuel and activity prediction tool for a portion of system that removes 99% of particulate matter and CO 2 • Committed to four additional energy storage systems, to its fleet which does not have granular data for reporting from the exhaust gas be installed on the last four PSVs by 2025 • SMHI has taken initial steps to engage the fleet on voyage • The system is also equipped with a filter that cleans with • Results in reduction in fuel consumption and CO and energy plant optimization to make its operation washing water and the waste product fed into the sludge 2 emission by up to 40% greener tanks • Solution can be well-suited for SMHI’s fleet of liftboats seacormarine.com 32

SEACOR Marine Safety Benchmarks (1) Year-on-Year Total Recordable Injury Rate (“TRIR”) vs. Industry Benchmarks 5-year TRIR Average (2019 - 2023) SEACOR Marine 0.210 ISOA 0.886 IMCA 1.216 1.450 1.360 1.110 1.100 1.090 1.070 0.950 0.880 0.780 0.720 0.531 0.202 0.179 0.100 0.037 2019 2020 2021 2022 2023 SEACOR Marine ISOA IMCA (1) TRIR = (Fatalities + Lost Time Incidents + Restricted Work Cases + Medical Treatment Cases) x 1,000,000 / Total Hours Worked. Source: Company, International Support Owners Association (ISOA), International Marine Contractors Association (IMCA). seacormarine.com 33

Contact: Investor Relations SMHI LISTED Email: InvestorRelations@seacormarine.com NYSE Website: www.seacormarine.com seacormarine.com 34