Filed pursuant to Rule 424(b)(3)

Registration No. 333-233363

Prospectus Supplement No. 7

(To Prospectus dated September 29, 2020)

INX LIMITED

130,000,000 INX Tokens

This is a supplement (“Prospectus Supplement”) to the prospectus, dated September 29, 2020 (the “Prospectus”) of INX Limited (the “Company”), which forms a part of the Company’s Registration Statement on Form F-1 (Registration Nos. 333-233363).

This Prospectus Supplement updates and should be read in conjunction with, and delivered with, the Prospectus. To the extent there is a discrepancy between the information contained herein and the information in the Prospectus, the information contained herein supersedes and replaces such conflicting information.

This prospectus supplement consists of the Report on Form 6-K filed with the Securities and Exchange Commission on February 25, 2021 as set forth below.

This Prospectus Supplement is not complete without, and may not be delivered or utilized except in connection with, the Prospectus, including any amendments or supplements to it.

Purchasing INX Tokens involves a high degree of risk. See “Risk Factors” beginning on page 15 of the Prospectus.

None of the United States Securities and Exchange Commission, the Gibraltar Financial Services Commission, or any state securities commission or other jurisdiction has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this Prospectus Supplement No. 7 is February 25, 2021.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16

Under the Securities Exchange Act of 1934

For the Month of February 2021

333-233363

(Commission File Number)

INX LIMITED

(Exact name of Registrant as specified in its charter)

Unit 1.02, 1st Floor

6 Bayside Road

Gibraltar, GX11 1AA

Tel: +350 200 79000

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ____

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ____

Exhibit Index

| Exhibit No. | Description | |

| 99.1 | Investment Overview dated February 25, 2021 |

1

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| INX Limited | ||

| Date: February 25, 2021 | By: | /s/ Shy Datika |

| Shy Datika | ||

2

Investment Overview

Legal Disclaimer This presentation contains proprietary, non - public information regarding the business and operations of INX Limited (the “Company”) and is based upon information provided by the Company and other sources and is intended solely for use by prospective investors in the Company . This presentation is not all - inclusive and may not contain all of the information that the recipient requires to evaluate an investment in the Company (the “Proposed Offering”) . In all cases, the recipient should conduct its own investigation and analysis of the Proposed Offering and the data and financial information set forth in this presentation and should rely solely on its own judgment, review and analysis in evaluating the Proposed Offering . While the information contained in this presentation is believed to be accurate and reliable, the information in this presentation (including any statements, estimates or financial information provided by the Company) has not been independently verified by a third party . Such statements, estimates and financial information reflect various subjective assumptions by management concerning anticipated results, which assumptions are inherently subject to significant uncertainties and contingencies and may or may not prove to be correct . No representation, warranty or undertaking, expressed or implied, is or will be made, and no responsibility or liability is or will be accepted by the Company, its affiliates or any of their directors, officers, employees, agents, shareholders or advisors (“Representatives”) as to, or in relation to, the accuracy or completeness of the information contained in this presentation, the assumptions and projections incorporated therein, or any other information (whether communicated in written or oral form) transmitted or made available to the recipient, or errors therein or omissions therefrom . This presentation contains forward - looking statements . In some cases, the recipient can identify forward - looking statements by terms such as ‘may,’ ‘will,’ ‘should,’ ‘could,’ ‘would,’ ‘expects,’ ‘plans,’ ‘anticipates,’ ‘believes,’ ‘estimates,’ ‘projects,’ ‘predicts,’ ‘potential’ or ‘continue’ or the negative of those forms or other comparable terms . The Company’s forward - looking statements involve known and unknown risks, uncertainties and other factors which may cause the Company’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward - looking statements . Because of these uncertainties, the recipient should not place any reliance on the Company’s forward - looking statements . The Company does not intend to update (nor does the Company have any duty to update) any of these factors or to publicly announce the result of any revisions to any of the Company’s forward - looking statements contained in this presentation, whether as a result of new information, any future event or otherwise . The Company expressly disclaims any and all liability which may be based on any assumptions contained in this presentation or forward - looking statements derived from such assumptions or any other information contained in this presentation, errors therein or omissions therefrom . This presentation presents information with respect to the Company as of the date hereof, and none of the Company or any of its Representatives undertakes to update or otherwise revise or correct any inaccuracies which become apparent in this presentation or other information supplied . In furnishing this presentation, the Company reserve the right to amend or replace this presentation at any time and undertakes no obligation to provide any recipient with access to any additional information . Only information and representations and warranties specifically contained or referred to in a definitive written securities purchase agreement, if any, and subject to such limitations and restrictions as may be contained or made in such agreement, when, as and if executed, will have any legal effect . No person has been authorized to provide any information with respect to the Company or the Proposed Offering except the information contained in this presentation . This presentation also contains market data and certain industry forecasts which were obtained from the Company’s internal analysis, market research, publicly available information and industry publications . Industry publications generally provide that the information contained therein has been obtain from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed . Similarly, internal surveys, industry forecasts and market research, while believed to be reliable, have not been independently verified by the Company and the Company makes no representation as to the accuracy of this information .

Legal Disclaimer (Continued) This presentation does not constitute an offer to sell, or a solicitation of any offer to buy, any of the securities offered hereby, by any person in any jurisdiction in which it is unlawful for such person to make an offering or a solicitation . The securities offered hereby have not been registered under the Securities Act of 1933 , as amended, or applicable state securities laws . The securities offered hereby have not been approved or disapproved, nor has the accuracy or adequacy of this presentation or any other offering materials been endorsed by, the U . S . Securities and Exchange Commission or any state securities commission or regulatory authority, and any representation to the contrary is unlawful . This presentation may be used only for information purposes relating to the Proposed Offering and may not be photocopied, reproduced or distributed, in whole or in parts, to any other person at any time . By accepting this presentation, the recipient agrees to keep this presentation and the information contained therein confidential and further agrees that this presentation and the information contained therein and in all related and ancillary documents is not to be used for any purpose other than in connection with its consideration of the Proposed Offering . If upon request by the Company, the recipient will return or destroy this presentation and all copies thereof, including analysis based on this presentation, in whole or in part . By accepting this presentation, the recipient also acknowledges that : (i) it is not relying on (to make any decision, either for investment or otherwise) the guidance, advice or representation (whether written or oral) of the Company, (ii) the Company has not provided (directly or indirectly by any person) any form of assurance or guarantee as to the merits (whether legal, financial, tax, accounting, regulatory compliance, credit, or other) of any information described in this presentation and is not relying on the Company in any manner in connection with its review of this presentation or the Proposed Offering ; and (iii) it is an investor that is qualified, experienced and sophisticated and thereby waives any protection that an investor not qualified may have . The preparation and distribution of this presentation does not constitute a form of commitment or recommendation relating to the Proposed Offering . Neither the information contained in this presentation nor any further information made available by the Company in connection with the Proposed Offering will form the basis of or be construed as a contract . By receiving this presentation, the recipient declares that it agrees to be bound by all the terms stated above . Recipients of this presentation who do not wish to participate in the Proposed Offering are required to return it immediately to the Company .

Equity Raise (Subscription Receipts) : $ 25 M CAD Offering Price : $ 1 . 25 CAD Pre - Money Valuation : $ 225 M CAD Anticipating : Q 2 2021 Closing The Offering Investment Offering R&D S&M G&A M&A Use of Proceeds $XX $XX $XX $XX Total $25,000,000 CAD Use Total Class INX Shares and Warrants ESOP RTO Financing RTO Financing Warrants Public Vehicle Warrants to Underwriters Capitalization 74.58% 10% 8.52%% 4.26% 2.13% 0.51% Total Post - Listing 100% Price Shares % 234,666,667 175,000,000 23,466,667 20,000,000 10,000,000 5,000,000 1,200,000 $1.25 CAD $1.88 CAD

INX intends to list on the TSXV for added credibility, leveraging on public reporting and transparency for the purpose of attracting Fortune 500 strategic partnerships and institutional investors . The Offering INX at a Glance INX launched the world ’ s first SEC registered security token IPO aimed at establishing an evolutionary, fully regulated financial trading market and to become a prime trading and listing arena for blockchain digital assets . The Company Founded in 2017 , INX has invested over $ 7 million in building a fully - regulated digital asset trading ecosystem for listing and trading cryptocurrencies, security tokens and their derivatives by both institutional and retail investors . Anticipated revenues streams include : Cryptocurrency trading fees, security token listing and trading fees . The Business Proceeds from the offering will be utilized for the commercial launch of the trading platform and its continued development and operation . working capital alongside targeted M&A opportunities . Use of Proceeds Current and Estimated Timeline Token offering INX Launch Regulated Cryptocurrency trading revenues Security token Listing & Trading Sep 2020 Q 2 2021 Q 2 2021 Q 3 2021 F 1 filed with the SEC Jan 2018 Trading platform stage A developed Dec 2019 MT License Cleared in 7 states Q 3 2019

INX The origins • The genesis of INX followed 2017 ’ s wave of ICO irrational exuberance that was conducted with little consideration for securities laws • INX recognized that digital assets were the future • Built a strong foundation by assembling the right team with years of experience in the capital markets and blockchain arenas • Developed proprietary state - of - the - art technology • Invested in strong industry standard and future public company infrastructure • Registered the INX Token with the SEC and spent 24 months building technology and solving the challenges of fully regulated digital asset securities registration and trading SEC EDGAR Registration Statement

Unifying capital markets and blockchain experience Ex Vice Chairman of NASDAQ Ex CEO Toronto Stock Exchange Ex CEO Ameritrade Ex HSBC Brokerage USA Ex TP - ICAP Ex Morgan Stanley Ex Standard Chartered Ex GE Capital Ex American Express Ex Société Générale Fox News analyst and co - host Ex eToro Top cyber specialists Blockchain experts Crypto key opinion leaders We have assembled a team from two worlds

Leadership Exceptionally experienced management with proven track record in regulated trading and capital markets Shy Datika Co - founder & President Founder of the largest leading interbank broker in Israel and Chairman of the Investment Committee for Israel’s largest pension fund. A serial entrepreneur who played significant roles in the adoption of electronic trading in the global OTC Forex market. Alan Silbert Executive Managing Director Alan has more than 20 years of experience at top financial institutions, most recently as a Senior Vice President of Capital One Commercial Banking. At Capital One, and previously at GE Capital, he underwrote and managed portfolios of senior debt to middle market companies. Douglas Borthwick CMO Douglas brings 25 years of experience with top global financial institutions, heading FX derivatives trading desks at Morgan Stanley, Merrill Lynch and Standard Chartered. He most recently created and built the deliverable FX ECN and trading platform for TP - ICAP. Jonathan Azeroual VP Blockchain Asset Strategy Jon has over 9 years of broad financial background working for banks, hedge funds, brokerage firms in various analytical, operational or executive positions, co - founder of Bsave Ltd., a UK company which operates a Bitcoin savings platform since 2015 Maia Naor VP Product Maia was responsible for the creation and execution of company road maps at major fin - tech operations, seeing ideas through from early stages to actual operational products. She has extensive experience in managing large operations, leading teams to deliver complex projects, Oran Mordechai CFO Oran has been working for 13 years in Ernst & Young Israel and held several key financial positions with multinational and publicly traded companies. Oran ’ s business experience includes corporate finance, international corporate tax, mergers and acquisitions, and initial public offerings. Paz Diamant Paz has more than 25 years of experience in the banking and financial technology industry. Formerly a Managing Director of R&D in eToro, He holds a (cum laude) BS in Physics from the Technion - Israel Institute of Technology and an MBA in Finance from Bar - Ilan University. CTO

Board Members David Weild Board Member Ex - NASDAQ David is a former Vice Chairman and executive committee member of The NASDAQ Stock Market and spent years running Wall Street investment banking and equity capital markets businesses. He is Founder, Chairman and CEO of Weild & Co. Nicholas Thadaney Board Member Ex - Toronto Stock Exchange Nick was most recently President and Chief Executive Officer, Global Equity Capital Markets, TMXGroup (Toronto Stock Exchange) as well as a Member of ITG’s Global Executive Committee, Director of Sales & Trading of ITG Canada’s Institutional Equities business. Haim Ashar Board Member Haim served as Head of Business Development at Wayra Germany, Telefonica ’ s startup accelerator and Change Manager at We call 4 U UG, Berlin with responsibilities for marketing, brand, public relations and partnerships. Tom Lewis Board Member Ex - Ameritrade Tom has served as CEO of Ameritrade and four companies, including The Green Exchange (a federally regulated futures and options exchange in New York and London, invested in by the CME Group, Goldman Sachs, Morgan Stanley, JPMorgan, Credit Suisse and many others). James Crossley Board Member James is a strategic advisor to enterprises, Director of Flo Live Group, a mobile IoT connectivity provider, and held various senior positions at Ascarii, Titan GS Europe, Intalec, and m - Wise

The What Digital Asset trading and listing Bonds Equities Security Tokens INX is a trading platform

INX Blockchain Asset Trading Platform • Over $ 7 million invested in building a digital assets trading platform for regulated trading and listing of security tokens • Buy/Sell crypto (BTC, ETH, LTC, ZEC, BCH) and security tokens and their derivatives • Support main order types (Market, Limit, Stop) • Trade confirmation and reporting tools to continually monitor and manage blotter, positions • Technical analysis tools for pre - trading purposes • API interface for broker dealers, corporate finance, traders and market makers • Industry standard reporting to regulators • Blockchain oriented, built for digital asset listing and trading See “ Product Roadmap ” section in the Prospectus

New institutional grade product Corporate finance packaging for differentiated securities, with versatile utility functions (e.g. index pegging, dividend payments, conditional trading, self - regulation and more…) • Full listing tech and service support • API interface for broker - dealers, corporate finance, traders, and market makers • Websocket and trading API to access real - time market data or develop secure programmatic trading bots

Robust and proprietary trading solution The INX platform for cryptocurrencies consists of the following proprietary layers : • Trading core – Matching Engine – Risk Management – Balance checks - socket - based API and designed to connect multiple traders to the trading platform . • Trading platform – Back end that exposes logic and capabilities for administrating the trading core . • User front end - Web application that exposes the User Interface (UI) to INX clients and allows them to sign up, login, trade, view market data, and manage their profile and portfolio . Asset managers Family offices Retail investors Market makers Hedge funds Algo traders Compliance officer Risk manager Data analyst Web UI Websocket API Back office Web UI Amazon Web Services Audit Infrastructure (Elastic Search) Common Packages Data Layer Trade History Funding Data KYC Data Users Data Balance Data Whitelisting Data 3 rd party services Bitgo Mailgun Zendesk Cloudflare Proprietary technology 3 rd party services End - user clients INX Employees Core Services (KYC, Funding … ) Back office services Matching Engine MongoDB Atlas Redis Cache • All INX Software components were developed in house based on micro service architecture in order to support a large - scale operation • Our team built the application from the ground up with Low latency and Security in mind • Two main user interfaces : Web UI and WebSocket API • All INX Services is hosted on AWS account • Database services are based on MongoDB Atlas that host their services on AWS and give us backups, auto - scaling and high - performance database • Audit logs for every event in the system are saved and monitored using Elastic Cloud services

The next step in capital markets A blockchain based security token , issued and traded under securities laws. A novel alternative for public capital raising Equity Debt Security Tokens 2020 1602 2000 BC Dutch East India INX Limited Introduction of Security Token Public Offerings to both institutional and retail investors alongside legacy financial products

Digital assets trading is a proven business • The business validation for digital asset trading platforms was proven during the past two years • As one example, in approx. 3 years, Binance went from zero to an estimated $1 Billion accumulated profit per year and from $15 million to $42 billion BNB token market cap. Coinmarketcap Feb 2021 CNBC Feb 2019 BraveNewCoin.com theblockcrypto.com 2020

All that remains is regulation … Decrypt Apr 2020 Telegram has offered to refund investors after its scheduled release of the Gram token failed – again – due to regulatory complications. Bitcoin.com May 2020

Why go digital? Security tokens are programmable securities, enabling higher flexibility and novel functionality of asset listings, trading and governance such as: • New capital market financial instruments • Floating of fractional and illiquid assets • 24 x 7 x 365 cross - border trading • Increased liquidity due to simultaneous multiple listings • Direct access to trading, reducing intermediaries • Reduced trading costs as a result of efficient processes • Increased transparency and privacy • Automated KYC/AML compliance • Instant settlement • Automated cap table management

The evolution of securities to digital Equity Shares Holder Represent ownership in a company Company Before: The Legacy Equity World Digital Security Tokens Holder Represent ownership in an asset Company Intellectual property A project in a company Art / real estate / talent Any other assets of value After: The Digital Assets World

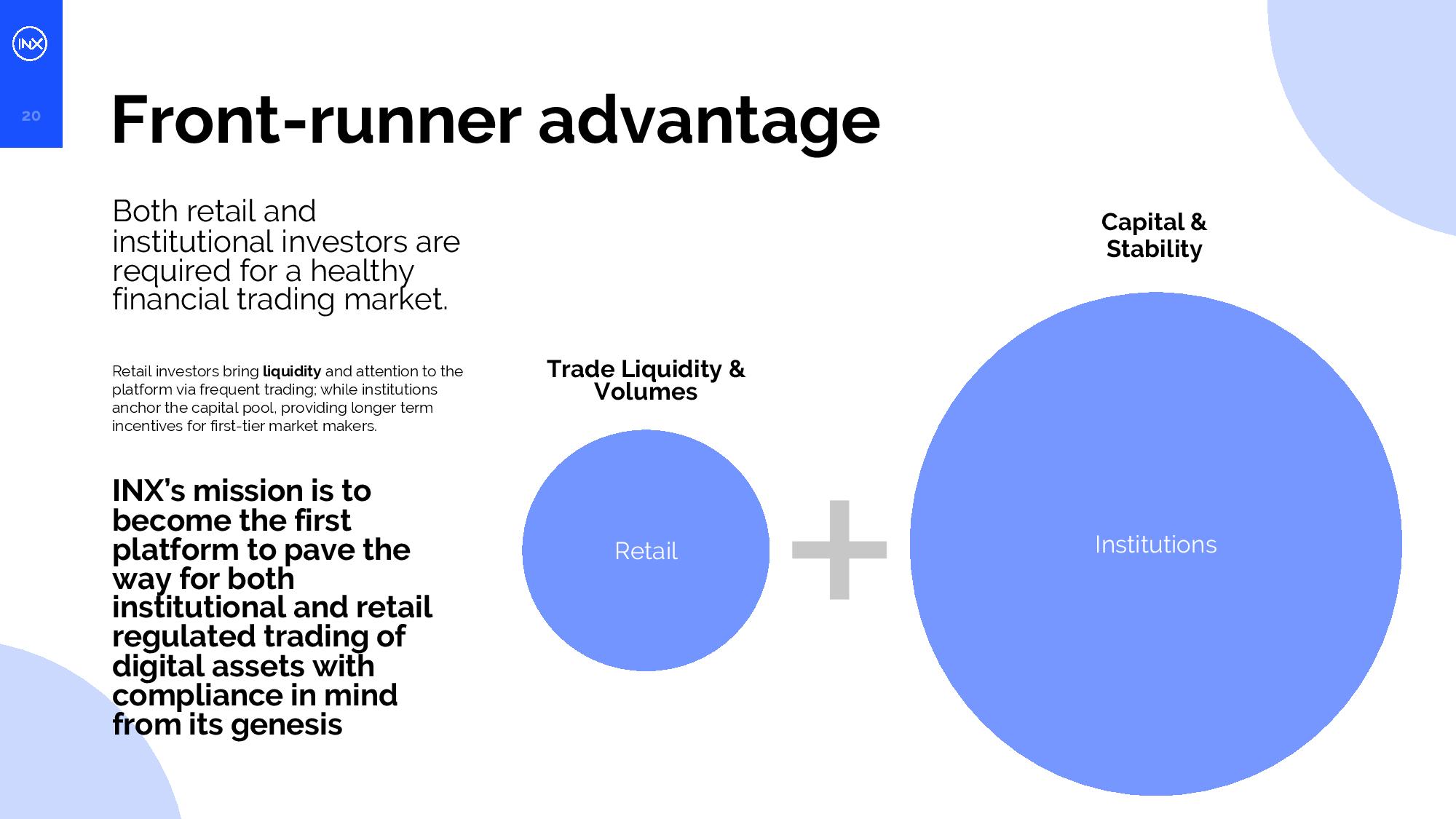

Front - runner advantage Both retail and institutional investors are required for a healthy financial trading market. Retail investors bring liquidity and attention to the platform via frequent trading; while institutions anchor the capital pool, providing longer term incentives for first - tier market makers. INX ’ s mission is to become the first platform to pave the way for both institutional and retail regulated trading of digital assets with compliance in mind from its genesis Institutions Retail Trade Liquidity & Volumes Capital & Stability

Opportunity for growth INX opens up the cryptocurrency and security token market to the entire investment community Qualified accredited investors for security tokens before INX Institutional and general public investors worldwide Source Investment Company Institute, 2017 Investment Fact Book 57 th Edition

INX Positioning Institutional Retail Cryptocurrency Security Tokens Accredited Investors Derivatives Innovative & unproven Mature & proven

INX Positioning Institutional Retail Cryptocurrency Security Tokens Accredited Investors Derivatives Innovative & unproven Mature & proven

• “ More millennials hold a bitcoin - tied investment product in their investment portfolios than Netflix stock, according to a recent report from brokerage giant Charles Schwab ” – The Block, Dec 6 , 2019 • While equities have taken a few hundred years to become central to investor portfolios, digital assets have achieved the same in just 11 years . As more assets are digitized, the market cap will grow exponentially . Overview of Global Exchanges and Asset Classes Blockchain assets are growing in popularity SOURCE: SIFMA, Deutsche Bank, money.visualcapitalist.com, Worldbank, Commodity.com SOURCE :Coinmarketcap.com The blockchain asset class market reached $ 160 B in daily volume while operating with limited institutional investment and within limited retail geographies Market Cap Countries Exchanges Fee Structure Listing Method $ 100 Trillion 195 countries OTC Markets Mark - Up / Commission No Listing $85 Trillion 56 countries 60 exchanges, including: Application fee Annual membership fee Monthly trading fee IPO Direct Listing $ 20 Trillion 195 countries Mark - Up / Commission Establishment of contracts $ 6 Trillion 195 countries OTC Markets Mark - Up / Commission No Listing $ 1.5 Trillion 68 countries 322 exchanges, including: Percentage of notional amount per trade ICO – Initial Coin Offering IEO – Initial Exchange Offering STO – Security Token Offering Free listing (for highly popular coins to build momentum) Fixed Income Equity Commodity Forex Blockchain Assets

Our competitive advantage Digital assets are likely to follow traditional securities exchanges ’ evolution There are multiple securities exchanges operating globally in parallel Traditional Exchanges TODAY Digital Asset Trading Platforms IN 5 YEARS 60 exchanges worldwide, top 16 in the trillion - dollar club Hence, our view of the future competitive landscape INX is a front - runner amongst comparable digital assets trading platforms: We have been regulation focused from day one for both institutional and retail trading. We have an exceptional execution team that has vast experience in: • Running trading platforms • Marketing and onboarding professional & retail traders • Securities and derivatives compliance • Multibillion - dollar asset management in global capital markets

Why now? History repeats itself Merchant ship owners issue stock ownerships raising capital against share participation in their commercial voyages Amsterdam and England lead the new asset class. 1600 ’ s 1971 Equity Trading Blockchain Asset Trading 2017 2020 1711 South Sea Company fails to pay dividends causing a market crash. Investors loose massively. British government bans shares till 1825 . 1773 1792 LSE was formed but crippled by the ban on shares. Age of public corporate finance takes flight. 2020 Modern day computerized share trading is corporate finance global standard Over 60 exchanges trading Trillions of US dollars in shares every year Inception No Regulation Ban Regulation Mass Adoption ICO campaigns have raised almost $ 6.5 B offering blockchain digital tokens against investments ICOs raise $21B more. Multiple ICOs feature scams, “Pumps & Dumps” and investors lose massively. 2018 2019 Regulated trading platforms start to form with limited offerings and abilities. SEC issues hundreds of subpoenas prosecuting companies for non - regulated ICOs. ICOs come to a halt. Regulated offerings – nascent growth in STOs (Security Token Offerings) under Reg D and Reg A. INX becomes the first ever fully - registered Security Token IPO Over 300 blockchain trading platforms, trading over 3,000 digital assets. None of them registered. 2018

Inception No Regulation Ban Regulation Mass Adoption Adaptation Why now? History repeats itself Blockchain digital assets industry is here

We believe INX is well positioned to potentially take significant market share as one of the top ten regulated trading platforms in the next 5 years

Timeline & Revenue generation Staged expansion of trading and listing Q 3 Phase II Security token listings Security token trading FINRA/BD/ATS licenses are expected to be assigned from OpenFinance acquisition during 2021 Expansion of MT License to 40 states + Worldwide expansion Licenses Q 1 An SEC Cleared INX Token offering 2021 2021 INX Launch Cryptocurrency trading MT Licenses obtained in 25 states Phase II REVENUE DRIVERS Start of revenue generation Q 4 Q 2 Revenue generation 1. Cryptocurrency trading fees – the main revenue source ( 100 %) at launch, until other activities are operational and changing the revenue mix over time 2. Security token trading fees – will commence upon receipt of the BD/ATS license 3. Security token listing fees – will commence upon receipt of the BD/ATS license

• Openfinance Securities LLC, a registered U.S. broker - dealer operating a registered FINRA/SIPC member, with an alternative trading system (ATS) and one of the pioneers of digital assets regulated trading platforms • INX signed a definitive agreement to acquire Openfinance's broker - dealer and ATS business including its systems, digital asset listings, client base and licenses • The closing of this transaction is subject to regulatory approval. Acquisition of Open Finance Strategic Advancements & Partnerships Additional Partners

• Seeking to raise $ 25 million CAD at $ 225 million CAD pre - money valuation against issuance of ordinary shares • All new money into the company • 5 % shareholders and shareholders who are directors and officers of the Company will undertake to share sale lock - up USE OF PROCEEDS INX will use the funds primarily for 1. commercial launch of the trading platform ( 20 %), 2. ongoing operational and marketing development of the business ( 60 %) and 3. leveraging on potential targeted acquisitions ( 20 %) Round & Use of proceeds

Summary • Building a prime trading and listing arena for digital assets • First SEC - registered security token public offering • Introducing a first - of - its - kind corporate finance asset class • Exceptionally experienced team with demonstrated success in the industry • A multi - trillion - dollar potential market • Planning to fuel revenue growth and profitability via a $ 25 m CAD offering on TSXV INX strongly believes that the time we spent building our strong foundation is a necessity for long - term success . 1. Strong adherence to laws and regulations from inception 2. Robust, proprietary technology built with security and regulation in mind ground - up 3. Strong management with proven track record in multi - national capital markets and related execution While many trading platforms exist today with one or more of the stated prerequisites for success, only INX has been built with all 3 in mind . We work with regulators ; we do not run from them . We built our own technology ; we do not license it . Our management has top - line experience on Wall Street and the digital space . We believe a strong, healthy community of token holders is preferred to only a few institutional token holders . We believe to be well positioned to take significant market share in this multitrillion dollar opportunity .

Risk Factors Investing in INX involves a high degree of risk . You should carefully consider the risks we describe below, along with all of the other information set forth in this presentation, including the section entitled “ Legal Disclaimers ” . The risks and uncertainties described below are those significant risk factors, currently known and specific to us, that we believe are relevant to an investment in INX Tokens . If any of these risks materialize, our business, results of operations or financial condition could suffer, the price of INX Tokens could decline substantially, and you could lose part or all of your investment . Additional risks and uncertainties not currently known to us or that we now deem immaterial may also harm us and adversely affect your investment in INX Tokens . • You may lose the entirety of your investment . • You should consult legal, financial, tax and other professional advisors or experts for further guidance before participating in the offering . • We have no operating history . Even if this offering is successful, we may need to raise additional capital in the future to continue operations, which may not be available on acceptable terms, or at all . • Our ability to develop the INX Platform faces operational, technological and regulatory challenges and we may not be able to develop the INX Platform as contemplated or at all . • The regulatory regimes governing blockchain technologies, blockchain assets and the purchase and sale of blockchain assets are uncertain, and new regulations or policies may materially adversely affect the development of blockchain networks and the use of blockchain assets . • The INX Platform depends upon security tokens being transferred to and held by a custodian before being traded on our INX Platform ; however, we have been unsuccessful in identifying a custodian relationship that the SEC has determined will satisfy our obligations under Rule 15 c 3 - 3 of the Exchange Act with regard to providing custodial services for security tokens . • We expect to face intense competition from other companies . • Failure to keep up with rapid changes in industry - leading technology, products and services could negatively impact our results of operations . • The extent to which blockchain assets are used to fund criminal or terrorist enterprises or launder the proceeds of illegal activities could materially impact our business . • Our securities business and related clearing operations expose us to material default and liquidity risk . • There can be no assurance that we will obtain liability insurance with adequate coverage to cover our liabilities . • We may experience systems failures or capacity constraints that could materially harm our ability to conduct our operations and execute our business strategy, including with respect to compliance and risk management matters . • The open - source structure of blockchain software means that blockchain networks may be susceptible to malicious cyber - attacks or may contain exploitable flaws, which may result in security breaches and the loss or theft of blockchain assets . • The loss of key personnel, particularly Mr . Shy Datika, our President, could have a material adverse effect on us . • Our business will be adversely affected if we are unable to attract and retain talented employees, including sales, technology, operations and development professionals . • As a financial services provider, we will be subject to significant litigation risk and potential commodity and securities law liability . • Our operations of businesses outside of the United States and our acceptance of currencies other than the U . S . Dollar will subject us to currency risk . • We, as well as many of our potential customers, depend on third party suppliers and service providers for a number of services that are important . An interruption or cessation of an important supply or service by any third party could have a material adverse effect on our business, including revenues derived from our customers ’ trading activity . • Our revenues and profits will be substantially dependent on the trading volume in our markets, which in turn are impacted by volatile prices of blockchain assets . Our revenues and profits would be adversely affected if we are unable to develop and continually increase our trading volume once the INX Platform becomes operational . • We intend to explore acquisitions, other investments and strategic alliances . We may not be successful in identifying opportunities or in integrating the acquired businesses and such transaction may not produce the results we anticipate . • Our business may be adversely affected by the impact of coronavirus . • Blockchain is a nascent and rapidly changing technology and there remains relatively small use of blockchain networks and blockchain assets in the retail and commercial marketplace . The slowing or stopping of the development or acceptance of blockchain networks may adversely affect an investment in our Company .

PURCHASERS ’ RIGHTS OF ACTION • Securities legislation in certain of the provinces of Canada provides purchasers of resciswith rights sion or damages, or both, where an offering memorandum or any amendment to it contains a misrepresentation . A “ misrepresentation ” is an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make any statement not misleading or false in the light of the circumstances in which it was made . • These remedies must be commenced by the purchaser within the time limits prescribed and are subject to the defences contained in the applicable securities legislation . Each purchaser should refer to the provisions of the applicable securities laws for the particulars of these rights or consult with a legal advisor . • The following rights are in addition to and without derogation from any other right or remedy which purchasers may have at law and are intended to correspond to the provisions of the relevant securities laws and are subject to the defences contained therein . The following summaries are subject to the express provisions of the applicable securities statutes and instruments in the below - referenced provinces and the regulations, rules and policy statements thereunder and reference is made thereto for the complete text of such provisions . Ontario Investors • Under Ontario securities legislation, certain purchasers who purchase securities offered by an offering memorandum during the period of distribution will have a statutory right of action for damages, or while still the owner of the securities, for rescission against the issuer or any selling security holder if the offering memorandum contains a misrepresentation without regard to whether the purchasers relied on the misrepresentation . The right of action for damages is exercisable not later than the earlier of 180 days from the date the purchaser first had knowledge of the facts giving rise to the cause of action and three years from the date on which payment is made for the securities . The right of action for rescission is exercisable not later than 180 days from the date on which payment is made for the securities . If a purchaser elects to exercise the right of action for rescission, the purchaser will have no right of action for damages against the issuer or any selling security holder . In no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser and if the purchaser is shown to have purchased the securities with knowledge of the misrepresentation, the issuer and any selling security holder will have no liability . In the case of an action for damages, the issuer and any selling security holder will not be liable for all or any portion of the damages that are proven to not represent the depreciation in value of the securities as a result of the misrepresentation relied upon . • These rights are not available for a purchaser that is (a) a Canadian financial institution or a Schedule III Bank (each as defined in National Instrument 45 - 106 – Prospectus Exemptions), (b) the Business Development Bank of Canada incorporated under the Business Development Bank of Canada Act (Canada), or (c) a subsidiary of any person referred to in paragraphs (a) and (b), if the person owns all of the voting securities of the subsidiary, except the voting securities required by law to be owned by directors of that subsidiary . • These rights are in addition to, and without derogation from, any other rights or remedies available at law to an Ontario purchaser . The foregoing is a summary of the rights available to an Ontario purchaser . Not all defences upon which an issuer, selling security holder or others may rely are described herein . Ontario purchasers should refer to the complete text of the relevant statutory provisions . Alberta, British Columbia and Quebec • By purchasing Subscription Receipts of the company, purchasers in Alberta, British Columbia and Quebec are not entitled to the statutory rights described above . In consideration of their purchase of the Subscription Receipts and upon accepting a purchase confirmation in respect thereof, these purchasers are hereby granted a contractual right of action for damages or rescission that is substantially the same as the statutory right of action provided to residents of Ontario who purchase Subscription Receipts . Saskatchewan Investors Under Saskatchewan securities legislation, certain purchasers who purchase securities offered by an offering memorandum during the period of distribution will have a statutory right of action for damages against the issuer, every director and promoter of the issuer or any selling security holder as of the date of the offering memorandum, every person or company whose consent has been filed under the offering memorandum, every person or company that signed the offering memorandum or the amendment to the offering memorandum and every person or company who sells the securities on behalf of the issuer or selling security holder under the offering memorandum, or while still the owner of the securities, for rescission against the issuer or selling security holder if the offering memorandum contains a misrepresentation without regard to whether the purchasers relied on the misrepresentation . The right of action for damages is exercisable not later than the earlier of one year from the date the purchaser first had knowledge of the facts giving rise to the cause of action and six years from the date on which payment is made for the securities . The right of action for rescission is exercisable not later than 180 days from the date on which payment is made for the securities . If a purchaser elects to exercise the right of action for rescission, the purchaser will have no right of action for damages against the issuer or the others listed above . In no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser and if the purchaser is shown to have purchased the securities with knowledge of the misrepresentation, the issuer and the others listed above will have no liability . In the case of an action for damages, the issuer and the others listed above will not be liable for all or any portion of the damages that are proven to not represent the depreciation in value of the securities as a result of the misrepresentation relied upon .

PURCHASERS ’ RIGHTS OF ACTION ( Continued) • Other defences in Saskatchewan legislation include that no person or company, other than the issuer, will be liable if the person or company proves that (a) the offering memorandum or any amendment to it was sent or delivered without the person ’ s or company ’ s knowledge or consent and that, on becoming aware of it being sent or delivered, that person or company immediately gave reasonable general notice that it was so sent or delivered, or (b) with respect to any part of the offering memorandum or any amendment to it purporting to be made on the authority of an expert, or purporting to be a copy of, or an extract from, a report, an opinion or a statement of an expert, that person or company had no reasonable grounds to believe and did not believe that there had been a misrepresentation, the part of the offering memorandum or any amendment to it did not fairly represent the report, opinion or statement of the expert . • No person or company, other than the issuer, is liable for any part of the offering memorandum or the amendment to the offering memorandum not purporting to be made on the authority of an expert and not purporting to be a copy of or an extract from a report, opinion or statement of an expert, unless the person or company (a) failed to conduct a reasonable investigation sufficient to provide reasonable grounds for a belief that there had been no misrepresentation, or (b) believed there had been a misrepresentation . Similar rights of action for damages and rescission are provided in Saskatchewan legislation in respect of a misrepresentation in advertising and sales literature disseminated in connection with an offering of securities . Saskatchewan legislation also provides that where an individual makes a verbal statement to a prospective purchaser that contains a misrepresentation relating to the security purchased and the verbal statement is made either before or contemporaneously with the purchase of the security, the purchaser has, without regard to whether the purchaser relied on the misrepresentation, a right of action for damages against the individual who made the verbal statement . • No person or company, other than the issuer, is liable for any part of the offering memorandum or the amendment to the offering memorandum not purporting to be made on the authority of an expert and not purporting to be a copy of or an extract from a report, opinion or statement of an expert, unless the person or company (a) failed to conduct a reasonable investigation sufficient to provide reasonable grounds for a belief that there had been no misrepresentation, or (b) believed there had been a misrepresentation . Similar rights of action for damages and rescission are provided in Saskatchewan legislation in respect of a misrepresentation in advertising and sales literature disseminated in connection with an offering of securities . Saskatchewan legislation also provides that where an individual makes a verbal statement to a prospective purchaser that contains a misrepresentation relating to the security purchased and the verbal statement is made either before or contemporaneously with the purchase of the security, the purchaser has, without regard to whether the purchaser relied on the misrepresentation, a right of action for damages against the individual who made the verbal statement . • In addition, Saskatchewan legislation provides a purchaser with the right to void the purchase agreement and to recover all money and other consideration paid by the purchaser for the securities if the securities are sold by a vendor who is trading in Saskatchewan in contravention of Saskatchewan securities legislation, regulations or a decision of the Financial and Consumer Affairs Authority of Saskatchewan . • The Saskatchewan legislation also provides a right of action for rescission or damages to a purchaser of securities to whom an offering memorandum or any amendment to it was not sent or delivered prior to or at the same time as the purchaser enters into an agreement to purchase the securities, as required by the Saskatchewan legislation . • A purchaser who receives an amended offering memorandum has the right to withdraw from the agreement to purchase the securities by delivering a notice to the issuer or selling security holder within two business days of receiving the amended offering memorandum . • These rights are in addition to, and without derogation from, any other rights or remedies available at law to a Saskatchewan purchaser . The foregoing is a summary of the rights available to a Saskatchewan purchaser . Not all defences upon which an issuer or others may rely are described herein . Saskatchewan purchasers should refer to the complete text of the relevant statutory provisions . Manitoba Investors If an offering memorandum or any amendment thereto, sent or delivered to a purchaser contains a misrepresentation, the purchaser who purchases the security is deemed to have relied on the misrepresentation if it was a misrepresentation at the time of the purchase and has a statutory right of action for damages against the issuer, every director of the issuer at the date of the offering memorandum, and every person or company who signed the offering memorandum . Alternatively, the purchaser may elect to exercise a statutory right of rescission against the issuer, in which case the purchaser will have no right of action for damages against any of the aforementioned persons . No action shall be commenced to enforce any of the foregoing rights more than : (a) in the case of an action for rescission, 180 days from the date of the transaction that gave rise to the cause of action, or (b) in the case of an action for damages, the earlier of (i) 180 days after the purchaser first had knowledge of the facts giving rise to the cause of action, or (ii) two years after the date of the transaction that gave rise to the cause of action . Securities legislation in Manitoba provides a number of limitations and defences to such actions, including : a) in an action for rescission or damages, no person or company will be liable if it proves that the purchaser purchased the securities with knowledge of the misrepresentation ; b) in an action for damages, no person or company will be liable for all or any portion of the damages that it proves do not represent the depreciation in value of the securities as a result of the misrepresentation relied upon ; and c) in no case will the amount recoverable under the right of action described above exceed the price at which the securities were offered under the offering memorandum .

PURCHASERS ’ RIGHTS OF ACTION ( Continued) New Brunswick Investors • Under New Brunswick securities legislation, certain purchasers who purchase securities offered by an offering memorandum during the period of distribution will have a statutory right of action for damages, or while still the owner of the securities, for rescission against the issuer and any selling security holder in the event that the offering memorandum, or a document incorporated by reference in or deemed incorporated into the offering memorandum, contains a misrepresentation without regard to whether the purchasers relied on the misrepresentation . The right of action for damages is exercisable not later than the earlier of one year from the date the purchaser first had knowledge of the facts giving rise to the cause of action and six years from the date on which payment is made for the securities . The right of action for rescission is exercisable not later than 180 days from the date on which payment is made for the securities . If a purchaser elects to exercise the right of action for rescission, the purchaser will have no right of action for damages against the issuer or any selling security holder . In no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser and if the purchaser is shown to have purchased the securities with knowledge of the misrepresentation, the issuer and any selling security holder will have no liability . In the case of an action for damages, the issuer and any selling security holder will not be liable for all or any portion of the damages that are proven to not represent the depreciation in value of the securities as a result of the misrepresentation relied upon . • These rights are in addition to, and without derogation from, any other rights or remedies available at law to a New Brunswick purchaser . The foregoing is a summary of the rights available to a New Brunswick purchaser . Not all defences upon which an issuer, selling security holder or others may rely are described herein . New Brunswick purchasers should refer to the complete text of the relevant statutory provisions . Nova Scotia Investors • Under Nova Scotia securities legislation, certain purchasers who purchase securities offered by an offering memorandum during the period of distribution will have a statutory right of action for damages against the issuer or other seller and the directors of the issuer as of the date the offering memorandum, or while still the owner of the securities, for rescission against the issuer or other seller if the offering memorandum, or a document incorporated by reference in or deemed incorporated into the offering memorandum, contains a misrepresentation without regard to whether the purchasers relied on the misrepresentation . The right of action for damages or rescission is exercisable not later than 120 days from the date on which payment is made for the securities or after the date on which the initial payment for the securities was made where payments subsequent to the initial payment are made pursuant to a contractual commitment assumed prior to, or concurrently with, the initial payment . If a purchaser elects to exercise the right of action for rescission, the purchaser will have no right of action for damages against the issuer or other seller or the directors of the issuer . In no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser and if the purchaser is shown to have purchased the securities with knowledge of the misrepresentation, the issuer or other seller and the directors of the issuer will have no liability . In the case of an action for damages, the issuer or other seller and the directors of the issuer will not be liable for all or any portion of the damages that are proven to not represent the depreciation in value of the securities as a result of the misrepresentation relied upon . • In addition, a person or company, other than the issuer, is not liable with respect to any part of the offering memorandum or any amendment to the offering memorandum not purporting (a) to be made on the authority of an expert or (b) to be a copy of, or an extract from, a report, opinion or statement of an expert, unless the person or company (i) failed to conduct a reasonable investigation to provide reasonable grounds for a belief that there had been no misrepresentation or (ii) believed that there had been a misrepresentation . • A person or company, other than the issuer, will not be liable if that person or company proves that (a) the offering memorandum or any amendment to the offering memorandum was sent or delivered to the purchaser without the person ’ s or company ’ s knowledge or consent and that, on becoming aware of its delivery, the person or company gave reasonable general notice that it was delivered without the person ’ s or company ’ s knowledge or consent, (b) after delivery of the offering memorandum or any amendment to the offering memorandum and before the purchase of the securities by the purchaser, on becoming aware of any misrepresentation in the offering memorandum or any amendment to the offering memorandum, the person or company withdrew the person ’ s or company ’ s consent to the offering memorandum or any amendment to the offering memorandum, and gave reasonable general notice of the withdrawal and the reason for it, or (c) with respect to any part of the offering memorandum or any amendment to the offering memorandum purporting (i) to be made on the authority of an expert, or (ii) to be a copy of, or an extract from, a report, an opinion or a statement of an expert, the person or company had no reasonable grounds to believe and did not believe that (A) there had been a misrepresentation, or (B) the relevant part of the offering memorandum or any amendment to the offering memorandum did not fairly represent the report, opinion or statement of the expert, or was not a fair copy of, or an extract from, the report, opinion or statement of the expert . • These rights are in addition to, and without derogation from, any other rights or remedies available at law to a Nova Scotia purchaser . The foregoing is a summary of the rights available to a Nova Scotia purchaser . Not all defences upon which an issuer or other seller or others may rely are described herein . Nova Scotia purchasers should refer to the complete text of the relevant statutory provisions . Prince Edward Island Investors • If an offering memorandum, together with any amendment thereto, is delivered to a purchaser and the offering memorandum, or any amendment thereto, contains a misrepresentation, a purchaser has, without regard to whether the purchaser relied on the misrepresentation, a statutory right of action for damages against (a) the issuer, (b) subject to certain additional defences, against every director of the issuer at the date of the offering memorandum and (c) every person or company who signed the offering memorandum, but may elect to exercise the right of rescission against the issuer (in which case the purchaser shall have no right of action for damages against the aforementioned persons or company) .

PURCHASERS ’ RIGHTS OF ACTION ( Continued) • No action shall be commenced to enforce the right of action discussed above more than : (a) in the case of an action for rescission, 180 days after the date of the transaction that gave rise to the cause of action ; or (b) in the case of any action for damages, the earlier of : (i) 180 days after the purchaser first had knowledge of the facts giving rise to the cause of action ; or (ii) three years after the date of the transaction that gave rise to the cause of action . • Securities legislation in Prince Edward Island provides a number of limitations and defences to such actions, including : a) no person or company will be liable if it proves that the purchaser purchased the securities with knowledge of the misrepresentation ; b) in an action for damages, the defendant is not liable for all or any portion of the damages that it proves does not represent the depreciation in value of the securities as a result of the misrepresentation relied upon ; and c) in no case shall the amount recoverable under the right of action described herein exceed the price at which the securities were offered under the offering memorandum, or any amendment thereto . Newfoundland and Labrador Purchasers • If an offering memorandum, together with any amendment thereto, contains a misrepresentation, a purchaser has, without regard to whether the purchaser relied on the misrepresentation, a statutory right of action for damages against (a) the issuer, (b) subject to certain additional defences, against every director of the issuer at the date of the offering memorandum and (c) every person who signed the offering memorandum, but may elect to exercise the right of rescission against the issuer (in which case the purchaser shall have no right of action for damages against the aforementioned persons) . No action shall be commenced to enforce the right of action discussed above more than : (a) in the case of an action for rescission, 180 days after the date of the transaction that gave rise to the cause of action ; or (b) in the case of any action for damages, the earlier of : (i) 180 days after the purchaser first had knowledge of the facts giving rise to the cause of action ; or (ii) three years after the date of the transaction that gave rise to the cause of action . Securities legislation in Newfoundland and Labrador provides a number of limitations and defences to such actions, including : a) no person will be liable if it proves that the purchaser purchased the securities with knowledge of the misrepresentation ; b) in an action for damages, the defendant is not liable for all or any portion of the damages that it proves does not represent the depreciation in value of the securities as a result of the misrepresentation relied upon ; and c) in no case shall the amount recoverable under the right of action described herein exceed the price at which the securities were offered under the offering memorandum, or any amendment thereto .

Supporting slides

What is the blockchain? An explanation of the process behind INX ’ s business Using a Digital Wallet Unlike common equity securities, blockchain assets are stored on a digital wallet held by a custodian ; whereas regular assets like stocks and bonds are held by a brokerage company . When an investor wants to purchase the INX token, they are directed through an onboarding process . This process includes KYC and AML procedures, followed by whitelisting . Whitelisting requires the purchaser to supply INX with the wallet address that will be used by the firm to deliver the tokens . Note that only investors that have passed through the firm ’ s KYC, AML and whitelisting procedures are able to transact INX tokens . Purchasing Blockchain Assets via an Exchange When an investor seeks to buy or sell a blockchain asset on an exchange there are a number of things they have to do . They need to open an account, requiring them to go through a number of KYC and AML procedures similar to opening an account at a brokerage firm . They need to link their digital asset wallets, or the bank account from which funds will be used for purchases . In addition they need to supply the wallet to which blockchain purchases will be delivered . Each blockchain asset may require a different digital wallet . For example, an investor may have a wallet for storing Bitcoin, and another for storing Ethereum . Exchange Confirmation with the Ledger The transfer of a blockchain asset is recorded on its underlying blockchain ledger when the owner of the blockchain asset wishes to withdraw it from their account . When this happens, the blockchain asset is transferred from the exchange’s respective custodian’s digital wallet to the customer’s private digital wallet . Verifying the Transaction In order for the network to complete a transfer of funds, the transaction must be confirmed and written into a block on the blockchain . A block is mined every time a miner finds a solution to a mathematical problem and broadcasts their solution to the rest of the network . In other words, the miner solves the problem and proves their work to the other machines that were trying to solve the same problem . All the machines on the network verify the solution . If the solution is true, the miner who found it is given a reward . Then, a new problem is presented, and the competition begins again . That ’ s how Proof of Work blockchains like bitcoin or ethereum function . Digital Wallet A file that houses private keys and usually contains a software client which allows access to view and create transactions on a specific blockchain network that the wallet is designed for . Blockchain Asset Assets based on a computer - generated math - based and/or cryptographic protocol that utilize blockchain ledgers to record their creation, ownership and transfer of ownership . Blockchain Exchanges Trading platforms that provide basic buy and sell services for one or more blockchain assets . Distributed Ledger A shared ledger on a blockchain network that is a continuously growing list of transaction records (called “ blocks ” ) which are linked and secured using cryptography . Smart Contracts Self - executing rules in a programmable computer language on the blockchain that are enforced by the participants of the network . The INX Token is an ERC 20 blockchain asset that is programmed using a smart contract which is compatible with the Ethereum blockchain . KEY TERMINOLOGY AND PLAYERS

Blockchain assets overview Threats • Risk of loss • Limited scaling. • Lack of applications. • Numerous bugs in the smart contract • Limited scaling • Not subject to regulatory scrutiny • No accountability • No transparency • Lack of audits • Money laundering Benefits • Cannot be counterfeited or reversed arbitrarily by the sender • Immediate Settlement • Access to everyone with an internet connection • Lower fees • Allows people to build various application that enforce complex logics via smart contracts • Right to use the network • Right to vote on decisions that direct the evolution of the network • Reducing Investment Thresholds • Enhancing Asset Liquidity • Issuance Costs • Improved Market Efficienc y • Stable value • Backed by fiat currencies • Instant settlement • Global transactions Description Cryptocurrencies are designed to work as a store of value and medium of exchange, using decentralized cryptography to secure financial transactions, control the creation of additional units, and verify the transfer of assets. The most popular cryptocurrency is Bitcoin. Protocol tokens are required to access the service that the underlying protocol provides. Usually, apps or .are created on these protocols. The most popular protocol token right now is Ethereum ʾ DApps ʾ Utility tokens are issued in order to fund project development and can be later used to purchase goods or services offered by the token issuer Security tokens can pay dividends, share profits, pay interest or invest in other tokens or assets to generate profits for the token holders. Stablecoins are pegged to and secured by an underlying asset. The most popular ‘stablecoin’ right now is Tether, a coin backed by the US Dollar Cryptocurrency Protocol Token Stablecoins Utility Token Security Token • More Expensive than Utility Tokens • Secondary Market Trading Restrictions • Investor Accreditation Limitations

Blockchain – historical highlights 2009 Satoshi Nakamoto launches Bitcoin 2010 The first ever cryptocurrency exchange, Bitcoin Market First trade 0.03 USD/ 1 BTC 2010 Bitcoin reaches parity with USD, GBP and EUR 2012 BitPay reports having over 1,000 merchants accepting bitcoin under its payment processing service 2013 U.S. Federal Court issues opinion that Bitcoin is a currency or form of money People ’ s Bank of China ‘ ok ’ s ’ Bitcoin Bitcoin breaks US$ 1,000 2014 Vitalik Buterin announces Ethereum Credit - card processor Stripe begins accepting Bitcoin Paypal, Zynga, Overstock.com, Expedia, Newegg, Dell, Dish Network, and Microsoft are all accepting bitcoin for payments

2015 Coinbase opens up the first U.S - based cryptocurrency exchange NASDAQ initiates blockchain trial Gemini exchange launches, founded by the Winklevoss 2016 The DAO raised US$ 150 M in an ICO CME Launches Bitcoin Price Index 2017 BlockOne begins its year - long EOS ICO, eventually raising $ 4 billion China bans ICOs CME announces Bitcoin futures Bitcoin price at $ 20,000 2018 Switzerland begins accepting tax payments in Bitcoin 80 % of all Bitcoin has been mined Cryptocurrency market cap peaks at over $ 800 billion Fidelity launches institutional platform for cryptocurrencies 90 % of banks in the US and Europe report exploration of blockchain tech 2019 United States senate holds hearings titled ‘ Examining Regulatory Frameworks for Digital Currencies and Blockchain ” Block.One fined $ 24 million by the SEC for its unregulated $ 4 billion EOS ICO Santander bank settles both sides of a $ 20 million bond on Ethereum INX filed the “ red herring ” for the first Registered Security Token IPO 435 successful ICOs raising a cumulative total of over $ 5.6 billion INX submitted the first F - 1 for a Registered Security Token IPO $ 20 billion raised in ICOs over the year New York Stock Exchange owner announces Bakkt, a federally regulated digital asset exchange Blockchain – historical highlights

Industry challenges Opportunities Obstacles Several opportunitie s exist in the blockchain asset industry : • Security tokens and cryptocurrencies are a new asset class that have the potential to greatly improve upon legacy assets and systems • The “ tokenization ” of companies and assets frees up liquidity that didn ’ t before exist, and can automate processes in ways that weren ’ t possible • The stringent and tightening KYC/AML requirements from global regulators can be programmed into security token smart contracts, automating compliance . • Blockchain asset adoption is in its infancy . We believe we are in the very early stages of the industry ’ s development and adoption • Institutional adoption of the asset class will only happen through platforms like INX that embrace regulations The threats and obsta cles that hinder the expected growth in the industry and overall adoption of blockchain assets include : • Prior thefts and cybersecurity hacks to blockchain asset platforms that have raised the risk profile of the industry and caused some investors to avoid the space • Dark market use of blockchain assets have tainted the perception of the industry • Evolving global regulations have resulted in blockchain assets becoming illegal in certain countries, and some governments have intervened and caused certain operations to shut down • Some governments view blockchain assets as a threat to their fiat currencies • The INX team engaged regulators early and engineere d a regulated security token from scratch to become the first full - registered security token in U . S . history . The INX - SEC process has created the proper path for all future registered security token offerings and listings, potentially revitalizing the security token offering space and allowing INX to become the premier platform for IPOs going forward in the space • Threats of theft and cybersecurity hacks are managed by strict adherence to sound asset management through qualified custodians, cold storage of the vast majority of assets on the platform, and multi - signature hot wallets • Fraud and dark market abuse mitigated through our platform through use of our KYC/AML policies, smart contract, and whitelisting • We have an exceptionally experienced management team bringing together regulated trading and capital markets experience from both legacy and blockchain asset worlds INX Advantages

INX Whitelisting & Registry INX Token Distributed Ledger The “ INX Token distributed ledger ” references the ledger of holdings of INX Tokens that is recorded on the Ethereum blockchain . The INX Token distributed ledger records, by design, the public wallet addresses of all Ethereum wallets that hold INX Tokens and the balance of INX Tokens in each wallet address . The distributed ledger is updated after each transfer of INX Tokens . Information from the distributed ledger can be viewed using an Ethereum network block explorer, such as Etherscan . com . The INX Token distributed ledger is not a separate internal or private blockchain independent of the Ethereum blockchain . Whitelist Database The Company maintains a Whitelist Database to validate decentralized transfers of the INX Token . The Whitelist Database is a database stored on the data section of the INX Token smart contract . The Whitelist Database contains a record of information about individuals and entities that have satisfied the KYC/AML compliance procedures and thus are eligible to hold INX Tokens . Such information includes the digital wallet address, name and a KYC Reference ID linking to KYC filing information . INX Registry The INX Registry however, is an internal list of the identities of each record holder, the digital wallets addresses they own and the amount of INX Tokens held by each record holder . Thus, the purpose of the INX Registry is to maintain a list of INX Token holders by identity, updated on an ongoing basis . For example, the Company refers to the INX Registry when it makes a pro rata distribution of the Adjusted Operating Cash Flow to holders of INX Tokens . All holders (including purchasers) of INX Tokens must be vetted via a regulatory compliant KYC/AML process . Any transfer of INX Tokens or trade of INX Tokens on the INX Securities trading platform can only occur between two parties that have each satisfied the Company ’ s KYC/AML process . Individuals or entities which satisfactorily complete the KYC/AML process may have their Ethereum wallet address added to the Whitelist Database, allowing them to receive and send INX Tokens .

Regulatory impact • The “ Howey test ” , based on a 1946 U . S . Supreme Court case, is generally used to judge whether a blockchain asset is a non - security (cryptocurrency) or a security (security token) . • Security token issuance is governed by the SEC on a federal level, and by state ‘ Blue Sky ’ regulators on a state level if securities are issued to the public . • State money transmitter authorities oversee the operations of cryptocurrency trading platforms . • The SEC and FINRA approve and regulate Alternative Trading Systems (ATSs) and broker - dealers that trade security tokens . • FinCEN, a bureau of the U . S . Department of the Treasury, collects certain KYC/AML information and suspicious activity reporting from blockchain asset trading platforms in the U . S . • The Commodity Futures Trading Commission (CFTC) regulates derivatives trading operations . • The Internal Revenue Service (IRS) governs the taxation of blockchain assets . • In general, the existing regulatory construct for securities, currencies, and commodities applies a patchwork of regulations over the blockchain asset space . In many cases where regulations aren ’ t clear, regulators are working to modify laws around blockchain assets . Applicable Regulation • The first extensive securities regulations were put into place in the early 1930 ’ s following the Great Depression to regulate the stock market and protect the public from unregulated market activity and fraud . • In the era of blockchain assets, there is a ‘ gray zone ’ in applying securities laws from the 1930 ’ s to cryptocurrencies and security tokens today . • Starting in 2013 and peaking in 2017 , many Initial Coin Offerings (ICOs) abused that gray zone and claimed to be exempt from securities regulations . • As a result, regulators came down hard on ICO offerings to protect investors and essentially levied a ‘ cease and desist ’ on further ICOs . • Additionally, many early trading platforms, hastily constructed and not regulated, were the target of large hacks, with investors losing hundreds of millions of dollars . Regulators moved in to shut down all unregulated trading activity in the U . S . Purpose of the Regulation