Explanatory Note

The Registrant is filing this amendment to its Form N-CSR for the period ended

December 31, 2021, originally filed with the Securities and Exchange Commission on March 4, 2022 (Accession Number 0001683863-22-001418). The purpose of this filing is to include Management's Discussion of Fund Performance, A Look at Performance, and more expansive discussion of Investment Objective, Principal Investment Strategies, and Principal Risks, in Item 1 of this filing.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-23620

John Hancock GA Senior Loan Trust

(Exact name of registrant as specified in charter)

197 Clarendon Street, Boston, Massachusetts 02116 (Address of principal executive offices) (Zip code)

Heidi Knapp

Treasurer

197 Clarendon Street

Boston, Massachusetts 02116

(Name and address of agent for service) Registrant's telephone number, including area code: 617-378-1870

Date of fiscal year end: | December 31 |

Date of reporting period: | December 31, 2021 |

ITEM 1. REPORTS TO STOCKHOLDERS

John Hancock GA Senior Loan Trust

Annual Report

December 31, 2021

John Hancock GA Senior Loan Trust

December 31, 2021

Table of Contents | |

Management's discussion of fund performance ..................................................................................... | 2 |

A look at performance ......................................................................................................................... | 3 |

Portfolio summary................................................................................................................................ | 5 |

Portfolio of investments ........................................................................................................................ | 6 |

Statement of assets and liabilities ......................................................................................................... | 9 |

Statement of operations ....................................................................................................................... | 10 |

Statement of changes in net assets ...................................................................................................... | 11 |

Statement of cash flows ....................................................................................................................... | 12 |

Financial highlights............................................................................................................................... | 13 |

Notes to financial statements ................................................................................................................ | 14 |

Report of the Independent Auditors....................................................................................................... | 22 |

Tax information .................................................................................................................................... | 23 |

Investment objective, principal investment strategies, and principal risks .................................................. | 24 |

Trustees and Officers ........................................................................................................................... | 27 |

More information.................................................................................................................................. | 29 |

John Hancock GA Senior Loan Trust

Management's discussion of fund performance

MANAGED BY

Michael A. Foreman, Long Hoang, Daniel A. Walker, Henry Wong, and Ying Yi

By the end of 2021, COVID vaccinations and boosters became widely available, and although the Omicron variant caused a significant increase in cases, it was generally considered to be a milder strain than previous variants. Economic growth was impacted by supply chain and labor market constraints. After nearly two years of near-zero interest rates, Federal Reserve officials indicated their intent for rate hikes in 2022. Within limits, rate increases can be a net positive for the floating rate senior loan product.

The fund returned 5.15% for the year ended December 31, 2021. The return was mainly attributed to revenue streams, which generated an income return of approximately 4.2%, in addition to capital appreciation of 0.9%.

Total syndicated and direct lending markets hit a record in 2021, topping the prior 2018 high. General market M&A (mergers and acquisitions) and financing activity surged in the third and fourth quarters of 2021 to meet growing capital inflows. In the fourth quarter, sponsored middle market direct lending volume surged above the prior high set in the third quarter of 2021.

Elevated middle market LBO (leverage buyouts) continue to require historically high equity contributions. The combination of healthy equity contributions along with low interest rates have resulted in a continuation of solid interest coverage ratios. While downward pressure on middle market all-in yields continues, spreads and relative value remain favorable as rate floors protect the absolute return profile of the asset class. Middle market loan yields produced premiums above the comparable liquid loan and liquid bond markets.

The views expressed in this report are exclusively those of Manulife Investment Management Private Markets (US) LLC, and are subject to change. They are not meant as investment advice. Please note that the holdings discussed in this report, if any, may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund's investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

John Hancock GA Senior Loan Trust

A look at performance

TOTAL RETURNS FOR THE PERIOD ENDED DECEMBER 31, 2021

| | | Cumulative |

| | | total |

| | | returns |

| Average annual total returns (%) | (%) |

| | Since fund | Since fund |

| 1-Year | inception1 | inception1 |

At Net asset value | 5.15 | 5.68 | 6.62 |

| | | |

S&P/LSTA U.S. B Ratings Loan Index | 5.22 | 7.57 | 8.84 |

| | | |

1From 11-3-20.

Performance figures assume all distributions have been reinvested.

The returns reflect past results and should not be considered indicative of future performance. Investment returns and principal value will fluctuate and a shareholder may sustain losses. Current month-end performance may be higher or lower than the performance cited.

The performance table above and the chart on the next page do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the sale of fund shares. The fund's performance results reflect any applicable fee waivers or expense reductions, without which the expenses would increase and results would have been less favorable.

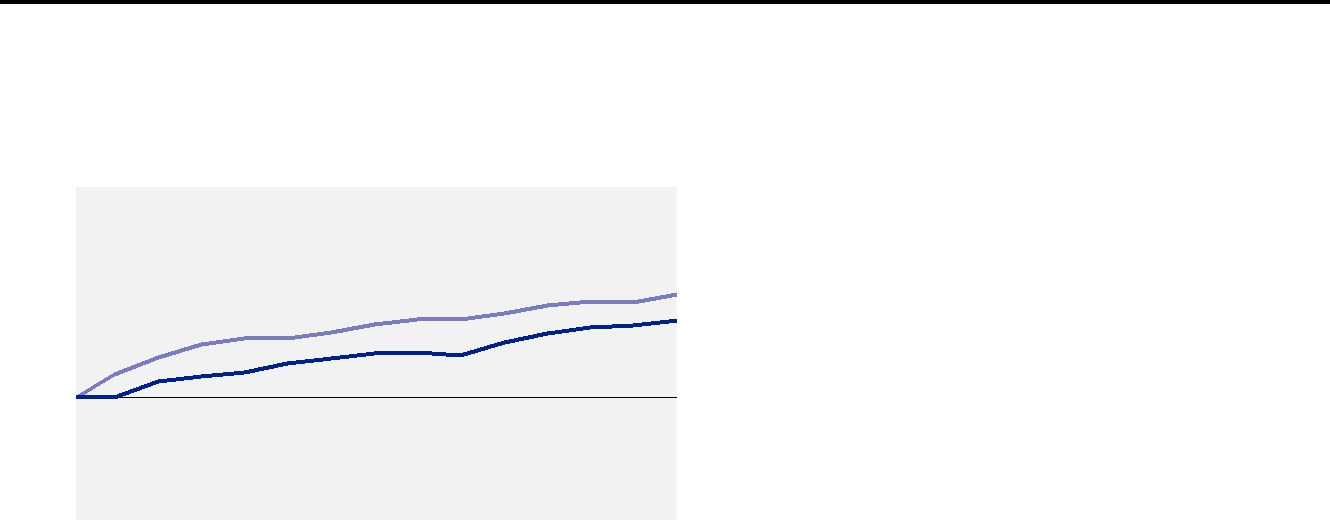

John Hancock GA Senior Loan Trust

A look at performance

This chart shows what happened to a hypothetical $10,000 investment in John Hancock GA Senior Loan Trust for the periods indicated, assuming all distributions were reinvested. For comparison, we've shown the same investment in the S&P/LSTA U.S. B Ratings Loan Index.

At net asset value

At net asset value

S&P/LSTA U.S. B Ratings Loan Index

S&P/LSTA U.S. B Ratings Loan Index

Ending values 12-31-21

9,000 | | | | | |

11-3-20 | 12-20 | 3-21 | 6-21 | 9-21 | 12-31-21 |

The S&P/LSTA U.S. B Ratings Loan Index tracks the performance of U.S. leveraged loans in the B rated category.

It is not possible to invest directly in an index. Index figures do not reflect expenses, which would result in lower returns.

The returns reflect past results and should not be considered indicative of future performance.

John Hancock GA Senior Loan Trust

Portfolio summary 12-31-21

Portfolio Composition as of 12-31-21 (% of net assets)

Senior loans | 88.5 |

Short-term investments and other | 11.5 |

Top 10 Issuers as of 12-31-21 (% of net assets) | |

Walnut Parent, Inc. | 3.3 |

MB2 Dental Solutions LLC | 3.3 |

BHI Investments LLC | 3.3 |

Octo Consulting Group LLC | 3.3 |

Apex Service Partners LLC | 3.3 |

Nxgen Buyer, Inc. | 3.2 |

GSM Acquisition Corp. | 3.1 |

Cerity Partners LLC | 3.1 |

Simplicity Financial Marketing Holdings, Inc. | 3.1 |

Oakbridge Insurance Agency LLC | 3.1 |

TOTAL | 32.1 |

Cash and cash equivalents are not included.

John Hancock GA Senior Loan Trust

Portfolio of investments 12-31-21

| Rate (%) Maturity date | Par value^ | Value |

| | | | |

Senior loans (A)(B) 88.5% | | | | $193,539,769 |

(Cost $191,323,762) | | | | |

Consumer staples 1.3% | | | | 2,962,312 |

Fresh Holdco, Inc., Term Loan (3 month LIBOR + 5.500%) | 6.500 | 01-23-26 | 2,962,312 | 2,962,312 |

Energy 1.8% | | | | 4,019,167 |

| | | | |

Andretti Buyer LLC, Term Loan (3 month LIBOR + 4.750%) | 5.750 | 06-30-26 | 4,051,225 | 4,019,167 |

Financials 19.4% | | | | 42,347,729 |

| | | | |

Cerity Partners LLC, Delayed Draw Term Loan (3 month LIBOR + | | | | |

6.750%) | 7.750 | 12-31-25 | 1,537,879 | 1,557,652 |

Cerity Partners LLC, Term Loan (3 month LIBOR + 6.750%) | 7.750 | 12-31-25 | 5,233,182 | 5,285,514 |

GC Waves Holdings, Inc., 2021 Replacing Term Loan (3 month | | | | |

LIBOR + 5.250%) | 5.474 | 08-13-26 | 4,081,067 | 4,081,067 |

Insignia Finance Merge Sub LLC, Term Loan (1 month LIBOR + | | | | |

5.000%) | 6.000 | 12-23-27 | 5,576,923 | 5,504,423 |

MC Group Ventures Corp., 2021 Delayed Draw Term Loan (3 | | | | |

month LIBOR + 5.500%) | 6.500 | 06-30-27 | 1,368,891 | 1,367,014 |

MC Group Ventures Corp., 2021 Revolver (1 month LIBOR + | | | | |

5.500%) | 6.500 | 06-30-27 | 181,250 | 180,874 |

MC Group Ventures Corp., 2021 Term Loan (3 month LIBOR + | | | | |

5.500%) | 6.500 | 06-30-27 | 4,122,143 | 4,119,150 |

Oakbridge Insurance Agency LLC, Delayed Draw Term Loan (1 | | | | |

and 3 month LIBOR + 5.250%) | 6.250 | 12-31-26 | 3,264,257 | 3,264,257 |

Oakbridge Insurance Agency LLC, Revolver (3 month LIBOR + | | | | |

5.250%) | 6.250 | 12-31-26 | 228,604 | 228,604 |

Oakbridge Insurance Agency LLC, Term Loan A (3 month LIBOR | | | | |

+ 5.250%) | 6.250 | 12-31-26 | 3,297,770 | 3,297,770 |

Simplicity Financial Marketing Holdings, Inc., Delayed Draw Term | | | | |

Loan (3 month LIBOR + 5.500%) | 6.500 | 12-02-26 | 2,061,870 | 2,082,489 |

Simplicity Financial Marketing Holdings, Inc., Term Loan (3 month | | | | |

LIBOR + 5.500%) | 6.500 | 12-02-26 | 4,667,885 | 4,719,172 |

World Insurance Associates LLC, 2021 Delayed Draw Term Loan | | | | |

Tranche 4 (3 month LIBOR + 5.750%) | 6.750 | 04-01-26 | 4,857,229 | 4,813,375 |

World Insurance Associates LLC, 2021 Revolver (1 month LIBOR | | | | |

+ 5.750%) | 6.750 | 04-01-26 | 40,578 | 35,709 |

World Insurance Associates LLC, 2021 Term Loan (3 month | | | | |

LIBOR + 5.750%) | 6.750 | 04-01-26 | 1,827,156 | 1,810,659 |

Health care 12.1% | | | | 26,473,067 |

Amerivet Partners Management, Inc., Delayed Draw Term Loan | | | | |

(1 and 3 month LIBOR + 4.750%) | 5.750 | 06-05-24 | 3,362,898 | 3,308,070 |

Avante Health Solutions, Revolver (Prime rate + 3.500%) | 6.750 | 07-15-27 | 114,715 | 114,715 |

Avante Health Solutions, Term Loan (3 month LIBOR + 4.500%) | 5.500 | 07-15-27 | 5,273,343 | 5,273,343 |

Health Management Associates, Inc., 2021 Term Loan (3 month | | | | |

LIBOR + 5.000%) | 6.000 | 09-24-26 | 5,982,961 | 5,959,511 |

MB2 Dental Solutions LLC, 2021 Delayed Draw Term Loan (Prime | | | | |

rate + 5.000% and 3 month LIBOR + 6.000%) | 7.132 | 01-29-27 | 1,908,251 | 1,908,251 |

MB2 Dental Solutions LLC, 2021 Term Loan (3 month LIBOR + | | | | |

6.000%) | 7.000 | 01-29-27 | 5,292,528 | 5,292,528 |

Therapeutic Research Center LLC, Term Loan (3 month LIBOR + | | | | |

4.750%) | 5.750 | 03-21-26 | 4,649,833 | 4,616,649 |

The accompanying notes are an integral part of the financial statements.

John Hancock GA Senior Loan Trust

Portfolio of investments 12-31-21

| Rate (%) Maturity date | Par value^ | Value |

Industrials 31.0% | | | | $67,687,751 |

| | | | |

Apex Service Partners LLC, 2019 Term Loan (3 month LIBOR + | | | | |

5.250%) | 6.250 | 07-31-25 | 4,937,003 | 4,937,003 |

Apex Service Partners LLC, 2020 1st Lien Delayed Draw Term | | | | |

Loan (Prime rate + 4.500% and 3 month LIBOR + 5.500%) | 6.715 | 07-31-25 | 456,686 | 450,795 |

Apex Service Partners LLC, 2020 Term Loan (3 month LIBOR + | | | | |

5.500%) | 6.500 | 07-31-25 | 1,725,028 | 1,702,775 |

BHI Investments LLC, 1st Lien Term Loan (3 month LIBOR + | | | | |

4.250%) | 5.250 | 08-28-24 | 7,189,261 | 7,189,261 |

BlueHalo Financing Holdings LLC, Revolver (1 month LIBOR + | | | | |

6.000%) | 7.000 | 10-31-25 | 357,685 | 354,706 |

BlueHalo Financing Holdings LLC, Term Loan A (3 month LIBOR | | | | |

+ 6.000%) | 7.000 | 10-31-25 | 5,827,449 | 5,788,987 |

CLS Management Services, Inc., Term Loan (3 month LIBOR + | | | | |

4.500%) | 5.500 | 05-31-27 | 3,819,044 | 3,761,645 |

GSM Acquisition Corp., Delayed Draw Term Loan (6 month | | | | |

LIBOR + 5.000%) | 6.000 | 11-16-26 | 909,870 | 909,870 |

GSM Acquisition Corp., Revolver (3 month LIBOR + 5.000%) | 6.000 | 11-16-26 | 513,924 | 513,924 |

GSM Acquisition Corp., Term Loan (3 and 6 month LIBOR + | | | | |

5.000%) | 5.271 | 11-16-26 | 5,451,208 | 5,451,208 |

ISS Compressors Industries, Inc., 2020 Term Loan (3 month | | | | |

LIBOR + 5.500%) | 6.500 | 02-05-26 | 2,701,758 | 2,701,649 |

Management Consulting & Research LLC, Term Loan (3 month | | | | |

LIBOR + 6.000%) | 7.000 | 08-16-27 | 6,340,502 | 6,231,752 |

Octo Consulting Group LLC, Term Loan (1 month LIBOR + | | | | |

5.000%) | 5.750 | 04-30-25 | 7,149,309 | 7,149,309 |

Orion Group HoldCo LLC, Delayed Draw Term Loan (3 month | | | | |

LIBOR + 5.000%) | 6.000 | 03-19-27 | 3,352,789 | 3,303,933 |

Orion Group HoldCo LLC, Revolver (3 month LIBOR + 5.000%) | 6.000 | 03-19-27 | 68,808 | 59,026 |

Orion Group HoldCo LLC, Term Loan (3 month LIBOR + 5.000%) | 6.000 | 03-19-27 | 3,214,167 | 3,167,331 |

Paint Intermediate III LLC, 1st Lien Term Loan (3 month LIBOR + | | | | |

4.250%) | 5.250 | 06-14-24 | 2,949,904 | 2,949,904 |

The S2 HR Group LLC, Revolver (3 month LIBOR + 4.250%) | 5.250 | 05-30-25 | 594,404 | 504,439 |

The S2 HR Group LLC, Term Loan (3 month LIBOR + 4.250%) | 5.250 | 05-30-25 | 4,093,565 | 4,093,565 |

WilliamsMarston LLC, Term Loan (1 month LIBOR + 5.250%) | 6.250 | 07-01-25 | 6,539,006 | 6,466,669 |

Information technology 10.4% | | | | 22,769,101 |

| | | | |

Drilling Info, Inc., 2018 Term Loan (1 month LIBOR + 4.250%) | 4.354 | 07-30-25 | 4,936,273 | 4,936,273 |

MRI Software LLC, 2020 Term Loan B (3 month LIBOR + 5.500%) | 6.500 | 02-10-26 | 4,624,331 | 4,673,911 |

Nxgen Buyer, Inc., Term Loan (1 month LIBOR + 4.500% and 3 | | | | |

month LIBOR + 4.750%)) | 5.578 | 10-31-25 | 7,187,028 | 7,042,028 |

Omni Intermediate Holdings LLC, 2021 Delayed Draw Term Loan | | | | |

1 (1 month LIBOR + 5.000%) | 6.000 | 11-30-27 | 578,639 | 567,066 |

Omni Intermediate Holdings LLC, 2021 Delayed Draw Term Loan | | | | |

2 (1 month LIBOR + 5.000%) | 6.000 | 11-30-27 | 34,038 | 27,570 |

Omni Intermediate Holdings LLC, 2021 Revolver (1 month LIBOR | | | | |

+ 5.000%) | 6.000 | 11-30-26 | 136,150 | 130,704 |

Omni Intermediate Holdings LLC, Term Loan (Prime rate + | | | | |

4.000% and 1 month LIBOR + 5.000%) | 6.003 | 12-30-26 | 5,446,009 | 5,391,549 |

Materials 12.5% | | | | 27,280,642 |

| | | | |

Comar Holding Company LLC, 2018 Term Loan (6 month LIBOR | | | | |

+ 5.750%) | 6.750 | 06-18-24 | 1,736,690 | 1,736,690 |

The accompanying notes are an integral part of the financial statements.

John Hancock GA Senior Loan Trust

Portfolio of investments 12-31-21

| Rate (%) Maturity date | Par value^ | Value |

Materials (continued) | | | | |

| | | | |

Comar Holding Company LLC, 2nd Amendment Delayed Draw | | | | |

Term Loan (1 month LIBOR + 6.250%) | 7.250 | 06-18-24 | 737,957 | $737,957 |

Comar Holding Company LLC, Delayed Draw Term Loan (1 and 3 | | | | |

month LIBOR + 5.750%) | 6.750 | 06-18-24 | 614,028 | 614,028 |

Comar Holding Company LLC, First Amendment Term Loan (1 | | | | |

month LIBOR + 5.750%) | 6.750 | 06-18-24 | 1,582,996 | 1,582,996 |

DCG Acquisition Corp., Second Lien Term Loan (3 month LIBOR | | | | |

+ 8.500%) | 8.599 | 09-30-27 | 5,000,000 | 5,000,000 |

Liqui-Box Holdings, Inc., Term Loan B (3 month LIBOR + 4.500%) | 5.500 | 02-26-27 | 2,962,406 | 2,962,406 |

Polymer Solutions Group LLC, 2019 Term Loan (3 month LIBOR | | | | |

+ 4.750%) | 5.750 | 11-26-26 | 1,893,720 | 1,893,720 |

Tilley Chemical Company, Inc., Revolver (Prime rate + 5.000%) | 8.250 | 12-31-26 | 260,256 | 255,919 |

Tilley Chemical Company, Inc., Term Loan A (3 month LIBOR + | | | | |

6.000%) | 7.000 | 12-31-26 | 5,315,679 | 5,247,651 |

Walnut Parent, Inc., Term Loan (1 month LIBOR + 5.500%) | 6.500 | 11-09-27 | 7,177,500 | 7,249,275 |

| | Yield (%) | Shares | Value |

| | | | |

Short-term investments 14.5% | | | | $31,710,128 |

(Cost $31,710,128) | | | | |

Short-term funds 14.5% | | | | 31,710,128 |

| | | |

State Street Institutional U.S. Government Money Market Fund, Premier Class | 0.0250(C) | 31,710,128 | 31,710,128 |

| | | | |

Total investments (Cost $223,033,890) 103.0% | | | | $225,249,897 |

Other assets and liabilities, net (3.0%) | | | | (6,617,553) |

Total net assets 100.0% | | | | $218,632,344 |

| | | | |

The percentage shown for each investment category is the total value of the category as a percentage of the net assets of the fund unless otherwise indicated.

^All par values are denominated in U.S. dollars unless otherwise indicated.

Security Abbreviations and Legend

LIBOR London Interbank Offered Rate

(A)Securities are valued using significant unobservable inputs and are classified as Level 3 in the fair value hierarchy. Refer to Note 2 to the financial statements.

(B)Senior loans are variable rate obligations. The coupon rate shown represents the rate at period end.

(C)The rate shown is the annualized seven-day yield as of 12-31-21.

At 12-31-21, the aggregate cost of investments for federal income tax purposes was $223,033,890. Net unrealized appreciation aggregated to $2,216,007, of which $2,396,092 related to gross unrealized appreciation and $180,085 related to gross unrealized depreciation.

The accompanying notes are an integral part of the financial statements.

Financial statements

John Hancock GA Senior Loan Trust

Statement of assets and liabilities 12-31-21

Assets | |

Unaffiliated investments, at value (Cost $223,033,890) | $225,249,897 |

Interest receivable | 710,933 |

Total assets | 225,960,830 |

| |

Liabilities | |

Due to custodian | 1,692,038 |

Distributions payable | 3,910,558 |

Payable for investments purchased | 686 |

Payable to affiliates | |

Investment management fees | 284,054 |

Performance fees | 880,357 |

Accounting and legal services fees | 19,046 |

Other liabilities and accrued expenses | 541,747 |

Total liabilities | 7,328,486 |

Net assets | $218,632,344 |

| |

Net assets consist of | |

Paid-in capital | $220,684,421 |

Total distributable earnings | (2,052,077) |

Net assets | $218,632,344 |

Net asset value per share | |

Based on 13,524,791 shares of beneficial interest outstanding - unlimited number of shares authorized with no | |

par value | $16.17 |

The accompanying notes are an integral part of the financial statements.

9

John Hancock GA Senior Loan Trust

Statement of operations for the year ended 12-31-21

Investment income | |

Interest | $11,132,852 |

| |

Expenses | |

Investment management fees | 1,043,925 |

Performance fees | 943,079 |

Accounting and legal services fees | 86,114 |

Transfer agent fees | 31,416 |

Trustees' fees | 66,931 |

Custodian fees | 140,118 |

Professional fees | 246,468 |

Offering costs | 236,587 |

Other | 129,309 |

Total expenses | 2,923,947 |

Net investment income | 8,208,905 |

| |

Realized and unrealized gain (loss) | |

Net realized gain (loss) on | |

Unaffiliated investments | 671,988 |

| 671,988 |

Change in net unrealized appreciation (depreciation) of | |

Unaffiliated investments | 373,501 |

| 373,501 |

Net realized and unrealized gain | 1,045,489 |

Increase in net assets from operations | $9,254,394 |

The accompanying notes are an integral part of the financial statements.

John Hancock GA Senior Loan Trust

Statement of changes in net assets

| Year ended | Period ended |

| 12-31-21 | 12-31-201 |

| | |

Increase (decrease) in net assets | | |

From operations | | |

Net investment income | $8,208,905 | $499,717 |

Net realized gain | 671,988 | 58,741 |

Change in net unrealized appreciation (depreciation) | 373,501 | 1,842,506 |

Increase in net assets resulting from operations | 9,254,394 | 2,400,964 |

Distributions to shareholders | | |

From net investment income and net realized gain | (12,669,417) | (843,880) |

From tax return of capital | (36,709,717) | — |

Total distributions | (49,379,134) | (843,880) |

From fund share transactions | | |

Fund shares issued | 69,200,000 | 188,000,000 |

Total increase | 29,075,260 | 189,557,084 |

Net assets | | |

Beginning of year | 189,557,084 | — |

End of year | $218,632,344 | $189,557,084 |

| | |

Share activity | | |

Shares outstanding | | |

Beginning of year | 9,392,193 | — |

Shares issued | 4,132,598 | 9,392,193 |

End of year | 13,524,791 | 9,392,193 |

1 Period from 11-3-20 (commencement of operations) to 12-31-20.

The accompanying notes are an integral part of the financial statements.

11

John Hancock GA Senior Loan Trust

Statement of cash flows for the year ended 12-31-21

Cash flows from operating activities

Net increase in net assets from operations | $9,254,394 |

Adjustments to reconcile net increase in net assets from operations to net cash used in operating activities: | | |

Long-term investments purchased | (106,792,190) |

Long-term investments sold | 58,072,639 |

Net purchases and sales in short-term investments | 3,278,845 |

Net amortization of premium (discount) | (522,731) |

(Increase) Decrease in assets: | | |

Interest receivable | (250,542) |

Receivable for investments sold | 7,673 |

Other assets | 255,835 |

Increase (Decrease) in liabilities: | | |

Payable for investments purchased | (135) |

Payable to affiliates | 908,425 |

Other liabilities and accrued expenses | 160,714 |

Net change in unrealized (appreciation) depreciation on: | | |

Unaffiliated investments | (373,501) |

Net realized (gain) loss on: | | |

Unaffiliated investments | (671,988) |

Net cash used in operating activities | $(36,672,562) |

| | |

Cash flows provided by (used in) financing activities | | |

Distributions to shareholders | $(46,312,456) |

Increase (Decrease) in due to custodian | (1,214,982) |

Fund shares issued | 84,200,000 |

Net cash flows provided by financing activities | $36,672,562 |

Cash at beginning of year | $— |

Cash at end of year | $— |

The accompanying notes are an integral part of the financial statements.

John Hancock GA Senior Loan Trust

Financial highlights

Period ended | 12-31-21 | 12-31-201 |

| | | | |

Per share operating performance | | | | |

Net asset value, beginning of period | $20.18 | $20.00 |

Net investment income2 | | 0.79 | | 0.06 |

Net realized and unrealized gain (loss) on | | | | |

investments | | 0.13 | | 0.22 |

Total from investment operations | | 0.92 | | 0.28 |

Less distributions | | | | |

From net investment income | | (1.15) | | (0.10) |

From net realized gain | | (0.04) | | — |

From tax return of capital | | (3.74) | | — |

Total distributions | | (4.93) | | (0.10) |

Net asset value, end of period | $16.17 | $20.18 |

Total return (%) | | 5.15 | | 1.403 |

Ratios and supplemental data | | | | |

Net assets, end of period (in millions) | $ | 219 | $ | 190 |

Ratios (as a percentage of average net | | | | |

assets): | | | | |

Expenses | | 1.54 | | 1.694 |

Net investment income | | 4.32 | | 3.444 |

Portfolio turnover (%) | | 37 | | 6 |

1Period from 11-3-20 (commencement of operations) to 12-31-20.

2Based on average daily shares outstanding.

3Not annualized.

4Annualized. Certain expenses are presented unannualized.

The accompanying notes are an integral part of the financial statements.

13

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

1. Organization

John Hancock GA Senior Loan Trust (the fund) is a Delaware statutory trust that is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as a closed-end, non-diversified management investment company. The investment objective of the fund is to generate current income.

The fund is only offered to "accredited investors" within the meaning of Regulation D under the Securities Act of 1933 (the 1933 Act), non-U.S. investors within the meaning of Regulation S under the 1933 Act, and other investors eligible to invest in a private placement.

2. Significant accounting policies

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (US GAAP), which require management to make certain estimates and assumptions as of the date of the financial statements. Actual results could differ from those estimates and those differences could be significant. The fund qualifies as an investment company under Topic 946 of Accounting Standards Codification of US GAAP.

Events or transactions occurring after the end of the fiscal period through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the fund:

Security valuation. Investments are valued at the end of each month at a minimum. The fund invests primarily in senior loans. The Board of Trustees oversees the process of the fund's valuation of its portfolio securities, assisted by the fund's Pricing Committee (composed of officers of the Trust), which calculates fair value determinations pursuant to procedures adopted by the Board. Assets that are not publicly traded or whose market prices are not readily available are valued at fair value as determined in good faith by the fund's Pricing Committee following procedures established by the Board of Trustees. In connection with that determination, portfolio valuations are prepared in accordance with the fund's valuation policy using valuation obtained from independent valuation firms and/or proprietary models.

Valuation techniques include discounted cash flow models, comparison with similar instruments for which observable market prices exist and other valuation models. Assumptions and inputs used in valuation techniques include risk-free and benchmark interest rates, credit spreads and other inputs used in estimating discount rates. For senior loans, the fund uses valuations from independent valuation firms, which are based on models developed from recognized US GAAP valuation approaches under ASC 820. Some or all of the significant inputs into these models may be unobservable and are derived either from observable market prices or rates or are estimated based on unobservable assumptions. Valuation models that employ significant unobservable inputs require a higher degree of management judgment and estimation in the determination of fair value. Judgment and estimation are usually required for the selection of the appropriate valuation model to be used, determination of expected future cash flows on the financial instrument being valued, determination of the probability of counterparty default and prepayments and selection of appropriate discount rates.

The fund uses a three-tier hierarchy to prioritize the pricing assumptions, referred to as inputs, used in valuation techniques to measure fair value. Level 1 includes securities valued using quoted prices in active markets for identical securities. Level 2 includes securities valued using other significant observable inputs. Observable inputs may include quoted prices for similar securities, interest rates, prepayment speeds and credit risk. Prices for securities valued using these inputs are received from independent pricing vendors and brokers and are based on an evaluation of the inputs described. Level 3 includes securities valued using significant unobservable inputs when market prices are not readily available or reliable, including the fund's own assumptions in determining the fair value of investments. Factors used in determining value may include market or issuer specific events or trends, changes in interest rates and credit quality. The inputs or

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. Changes in valuation techniques and related inputs may result in transfers into or out of an assigned level within the disclosure hierarchy.

Senior loan investments are measured at fair value based on the present value of the expected cash flows of the loans. There are no quoted prices in active markets. Assumptions and inputs used in the valuation of senior loan investments include prepayment estimates, determination of the discount rate based on the risk-free interest rate adjusted for credit risk (including estimation of probability of default), liquidity and any other adjustments that the independent valuation firm believes that a third-party market participant would take into account in pricing a transaction. Senior loan investment valuations rely primarily on the use of significant unobservable inputs, including credit assumptions, which require significant judgment and, accordingly, are classified as Level 3.

Other debt obligations are typically valued based on the evaluated prices provided by an independent pricing vendor. Independent pricing vendors utilize matrix pricing which takes into account factors such as institutional-size trading in similar groups of securities, yield, quality, coupon rate, maturity, type of issue, trading characteristics and other market data, as well as broker supplied prices. Other debt obligations are generally classified as Level 2.

Investments in open-end mutual funds are valued at their respective net asset values each business day and are generally classified as Level 1.

The following is a summary of the values by input classification of the fund's investments as of December 31, 2021 by major security category or type:

| | | Level 2 | Level 3 |

| Total | | Significant | Significant |

| value at | Level 1 | observable | unobservable |

| 12-31-21 | quoted price | inputs | inputs |

Investments in securities: | | | | |

Assets | | | | |

Senior loans | $193,539,769 | — | — | $193,539,769 |

Short-term investments | 31,710,128 | $31,710,128 | — | — |

Total investments in securities | $225,249,897 | $31,710,128 | — | $193,539,769 |

The following is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value. There were no transfers into or out of Level 3 during the period.

Investments in securities | | Senior loans |

Balance as of 12-31-20 | $143,251,998 |

Purchases | | 106,792,190 |

Sales | | (58,072,639) |

Realized gain (loss) | | 671,988 |

Net amortization of (premium) discount | | 522,731 |

Change in unrealized appreciation (depreciation) | | 373,501 |

Balance as of 12-31-21 | $193,539,769 |

Change in unrealized appreciation (depreciation) at period end* | $ | 799,069 |

*Change in unrealized appreciation (depreciation) attributable to Level 3 securities held at the period end.

The valuation techniques and significant amounts of unobservable inputs used in the fair value measurement of the fund's Level 3 securities are outlined in the table below.

| Fair Value | | Significant | | |

| at 12-31-21 | Valuation technique | unobservable inputs | Input range | Input weighted average* |

| | | | | |

Senior Loans | $193,539,769 | Discounted cash flow | Discount rate | 3.18% - 9.01% | 6.32% |

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

*A weighted average is an average in which each input in the grouping is assigned a weighting before summing to a single average value. The weighting of the input is determined based on a security's fair value as a percentage of the total fair value.

A change to unobservable inputs of the fund's Level 3 securities as of December 31, 2021 could have resulted in changes to the fair value measurement, as follows:

| Impact to Valuation | Impact to Valuation |

Significant Unobservable Input | if input had increased | if input had decreased |

| | |

Discount rate | Decrease | Increase |

Due to the inherent uncertainty of determining the fair value of Level 3 investments, the fair value of the investments may differ significantly from the values that would have been used had a ready market for such securities existed and may differ materially from the values that may ultimately be received or settled. Further, such investments will generally be subject to legal and other restrictions, or otherwise will be less liquid than publicly traded instruments. If the fund is required to liquidate a portfolio investment in a forced or liquidation sale, the fund might realize significantly less than the value at which such investment will have been previously been recorded. The fund's investments will be subject to market risk. Market risk is the potential for changes in the value due to market changes. Market risk is directly impacted by the volatility and liquidity in the markets in which the investments are traded.

Senior loans. The fund invests in senior loans. Senior loans include first and second lien term loans, delayed draw term loans, and revolving credit facilities. The fund will only invest in loans and commitments that are determined to be below investment-grade. The fund's investment policies are based on credit quality at the time of purchase. Credit quality is determined by the Advisor. The fund may invest in loans with a maturity of up to nine years from the closing date of the loan. The Advisor typically expects to employ a buy-and-hold strategy. The fund may invest in loans either by transacting directly at the initial funding date or acquiring loans in secondary market transactions. The fund may invest in loans secured by substantially all of the assets of the borrower and the other loan parties, subject to customary exceptions, including a pledge of the equity of the borrower and its subsidiaries.

The fund may be subject to greater levels of credit risk, call (or "prepayment") risk, settlement risk and liquidity risk than funds that do not invest in senior loans. Senior loans are considered predominantly speculative with respect to an issuer's continuing ability to make principal and interest payments, and may be more volatile than other types of securities. An economic downturn or individual corporate developments could adversely affect the market for these instruments and reduce the fund's ability to sell these instruments at an advantageous time or price. An economic downturn would generally lead to a higher non-payment rate and a senior loan may lose significant value before a default occurs. The fund may also be subject to greater levels of liquidity risk than funds that do not invest in senior loans. In addition, the senior loans in which the fund invests may not be listed on any exchange and a secondary market for such loans may be comparatively less liquid relative to markets for other more liquid fixed income securities. Consequently, transactions in senior loans may involve greater costs than transactions in more actively traded securities. Restrictions on transfers in loan agreements, a lack of publicly-available information, irregular trading activity and wide bid/ask spreads among other factors, may, in certain circumstances, make senior loans difficult to value accurately or sell at an advantageous time or price than other types of securities or instruments. These factors may result in the fund being unable to realize full value for the senior loans and/or may result in the fund not receiving the proceeds from a sale of a senior loan for an extended period after such sale, each of which could result in losses to the fund. Senior loans may have extended trade settlement periods which may result in cash not being immediately available to the fund. If an issuer of a senior loan prepays or redeems the loan prior to maturity, the fund may have to reinvest the proceeds in other senior loans or similar instruments that may pay lower interest rates. Senior loans in which the fund invests may or may not be collateralized, although the loans may not be fully collateralized and the collateral may be unavailable or insufficient to meet the obligations of the borrower. The fund may have limited rights

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

to exercise remedies against such collateral or a borrower, and loan agreements may impose certain procedures that delay receipt of the proceeds of collateral or require the fund to act collectively with other creditors to exercise its rights with respect to a senior loan. Because of the risks involved in investing in senior loans, an investment in the fund should be considered speculative. Junior loans, which are secured and unsecured subordinated loans, second lien loans and subordinate bridge loans, involve a higher degree of overall risk than senior loans of the same borrower due to the junior loan's lower place in the borrower's capital structure and, in some cases, their unsecured status.

The fund may also enter into, or acquire participations in, delayed funding loans and revolving credit facilities, in which a bank or other lender agrees to make loans up to a maximum amount upon demand by the borrower during a specified term. These commitments may have the effect of requiring the fund to increase its investment in a company at a time when it might not be desirable to do so (including at a time when the company's financial condition makes it unlikely that such amounts will be repaid). Delayed funding loans and revolving credit facilities are subject to credit, interest rate and liquidity risk and the risks of being a lender. Unfunded loan commitments are marked to market in accordance with the fund's valuation policies. Any related unrealized appreciation (depreciation) on unfunded commitments is included in unaffiliated investments, at value in the Statement of assets and liabilities and change in net unrealized appreciation (depreciation) in the Statement of operations. As of December 31, 2021, the fund had the following unfunded commitments outstanding.

| | | Unrealized |

| | | Appreciation |

Unfunded Term Loan | Principal on Delayed Draw Term Loan | Principal on Revolver | (Depreciation) |

| | | |

Amerivet Partners Management, Inc. | $3,886,000 | — | ($29,391) |

Andretti Buyer LLC | — | $897,364 | (5,813) |

Avante Health Solutions | 1,376,582 | 458,861 | — |

BlueHalo Financing Holdings LLC | — | 1,045,541 | (2,220) |

Cerity Partners LLC | — | 439,394 | 4,394 |

CLS Management Services, Inc. | 2,132,353 | 1,279,412 | (27,083) |

Comar Holding Company LLC | — | 276,184 | — |

GC Waves Holdings, Inc. | — | 867,298 | — |

GSM Acquisition Corp. | — | 312,025 | — |

Health Management Associates, Inc. | 760,224 | 506,816 | (4,098) |

Insignia Finance Merger SUB LLC | — | 1,673,077 | (16,731) |

ISS Compressors Industries, Inc. | — | 251,151 | (9) |

Management Consulting & Research LLC | — | 909,498 | (13,642) |

MC Group Ventures Corp. | 1,216,964 | 336,607 | (1,127) |

MRI Software LLC | — | 318,037 | 3,190 |

Oakbridge Insurance Agency LLC | — | 424,550 | — |

Omni Intermediate Holdings LLC | 408,451 | 612,676 | (10,212) |

Orion Group HoldCo LLC | — | 602,488 | (8,779) |

Polymer Solutions Group LLC | — | 463,768 | — |

Roofing Buyer LLC | 6,868,349 | 381,651 | (145,000) |

Simplicity Financial Marketing Holdings, Inc. | — | 460,903 | 4,609 |

The S2 HR Group LLC | — | 2,377,617 | (71,972) |

Therapeutic Research Center LLC | — | 303,131 | (2,031) |

Tilley Chemical Company, Inc. | 1,487,179 | 173,504 | (16,606) |

WilliamsMarston LLC | 694,606 | — | (6,946) |

World Insurance Associates LLC | — | 500,466 | (4,504) |

Total | $18,830,708 | $15,872,019 | $(353,971) |

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

Security transactions and related investment income. Investment security transactions are accounted for on a trade date plus one basis for NAV calculations. However, for financial reporting purposes, investment transactions are reported on trade date. Interest income is accrued as earned. Interest income includes coupon interest and amortization/accretion of premiums/discounts on debt securities. Debt obligations may be placed in a non-accrual status and related interest income may be reduced by stopping current accruals and writing off interest receivable when the collection of all or a portion of interest has become doubtful. Gains and losses on securities sold are determined on the basis of identified cost and may include proceeds from litigation.

Overdrafts. Pursuant to the custodian agreement, the fund's custodian may, in its discretion, advance funds to the fund to make properly authorized payments. When such payments result in an overdraft, the fund is obligated to repay the custodian for any overdraft, including any costs or expenses associated with the overdraft. The custodian may have a lien, security interest or security entitlement in any fund property that is not otherwise segregated or pledged, to the maximum extent permitted by law, to the extent of any overdraft.

Line of credit. The fund has entered into a revolving promissory note agreement with John Hancock Funding Company, LLC ("JH Funding") and a Line of Credit agreement with John Hancock Life Insurance Company ("JHUSA"). The aggregate outstanding borrowings under the agreements with JHUSA and JH Funding for the fund will not exceed $50 million. Any borrowings will be first drawn from JHUSA subject to certain conditions as specified in the agreement; otherwise, the borrowings will be drawn from JH Funding. There were no upfront fees or commitment fees paid by the fund in connection with these line of credit agreements. The borrowings under these agreements are designed to be short-term to satisfy intermittent delayed draws and will not be used to originate new loans or for investment leverage.

Expenses. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known. The fund incurred estimated offering costs of $290,000 upon commencement of operations. Offering costs were amortized over the fund's first year of operations. $236,587 of offering costs were expensed during the year ended December 31, 2021.

Statement of cash flows. A Statement of cash flows is presented when a certain percentage of the fund's investments is classified as Level 3 in the fair value hierarchy. Information on financial transactions that have been settled through the receipt and disbursement of cash is presented in the Statement of cash flows. The cash amount shown in the Statement of cash flows is the amount included in the fund's Statement of assets and liabilities and represents the cash on hand at the fund's custodian and does not include any short-term investments.

Federal income taxes. The fund intends to continue to qualify as a regulated investment company by complying with the applicable provisions of the Internal Revenue Code and will not be subject to federal income tax on taxable income that is distributed to shareholders. Therefore, no federal income tax provision is required.

As of December 31, 2021, the fund had no uncertain tax positions that would require financial statement recognition, derecognition or disclosure. The fund's federal tax returns are subject to examination by the Internal Revenue Service for a period of three years.

Distribution of income and gains. Distributions to shareholders from net investment income and net realized gains, if any, are recorded on the ex-date. The fund generally declares and pays dividends at least quarterly. Capital gain distributions, if any, are typically distributed annually.

The tax character of distributions for the year ended December 31, 2021 and the period ended December 31, 2020 was as follows:

| December 31, 2021 | December 31, 2020 |

Ordinary Income | $12,566,611 | $843,880 |

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

| December 31, 2021 | December 31, 2020 |

Long-term capital gains | 102,806 | — |

Tax Return of Capital | 36,709,717 | — |

Total | $49,379,134 | $843,880 |

As of December 31, 2021, there were no distributable earnings on a tax basis.

Such distributions and distributable earnings, on a tax basis, are determined in conformity with income tax regulations, which may differ from US GAAP. Distributions in excess of tax basis earnings and profits, if any, are reported in the fund's financial statements as a return of capital.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Temporary book-tax differences, if any, will reverse in a subsequent period. Book-tax differences are primarily attributable to organizational cost and distributions payable.

3. Guarantees and indemnifications

Under the fund's organizational documents, its Officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the fund. Additionally, in the normal course of business, the fund enters into contracts with service providers that contain general indemnification clauses. The fund's maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the fund that have not yet occurred. The risk of material loss from such claims is considered remote.

4. Fees and transactions with affiliates

Manulife Investment Management Private Markets (US) LLC (the Advisor) serves as investment advisor for the fund. The fund does not have a principal underwriter. The fund has entered into a Placement Agency Agreement with John Hancock Distributors, LLC (the Distributor), an affiliate of the Advisor, to offer to sell shares of the fund. The Advisor and Distributor are wholly owned subsidiaries of Manulife Financial Corporation (MFC).

Management fee. The fund has an investment management agreement with the Advisor under which the fund pays an annual fee rate of 0.55% of average net assets.

Performance fee. The fund has an agreement with the Advisor under which the fund pays a performance fee at annual rate of 10% of the fund's net profits, if any, over the high water mark provided that the performance fee shall be due only if (and, to the extent necessary, shall be reduced by an amount so that), after deducting such performance fee the fund's net profits as of the end of the applicable quarter will at least equal a defined preferred return. For the purposes of calculating the performance fee, net profits will be determined by taking into account net realized gain or loss (including realized gain that has been distributed to shareholders during a fiscal quarter and net of fund expenses, including the management fee) and the net change in unrealized appreciation or depreciation of securities positions, as well as dividends, interest and other income. No performance fee will be payable for any fiscal quarter unless losses and depreciation from prior fiscal quarters (the "cumulative loss") have been recovered by the fund, which is referred to as a "high water mark" calculation. The cumulative loss to be recovered before payment of performance fees will be reduced in the event of withdrawals by shareholders. The Advisor is under no obligation to repay any performance fees previously paid by the fund. Thus, the payment of performance fee for a fiscal quarter will not be reversed by the subsequent decline of the fund's net asset value in any subsequent fiscal quarter.

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

The preferred return as of the end of the applicable fiscal quarter is an amount equal to (a) 1.25% (the "Preferred Return Rate") multiplied by (b) the fund's net asset value as of the beginning of the fiscal quarter, adjusted to reflect additions to the fund's net asset value resulting from new share purchases during the fiscal quarter and reductions to the fund resulting from withdrawals by, or distributions to, shareholders during the fiscal quarter (the "Preferred Return Base"). The performance fee will not be payable for any fiscal quarter unless losses and depreciation from prior fiscal quarters have been recovered by the fund. The performance fee is accrued monthly and paid quarterly.

Accounting and legal services. Pursuant to a service agreement, the fund reimburses the Advisor for all expenses associated with providing the administrative, financial, legal, compliance, accounting and recordkeeping services to the fund, including the preparation of all tax returns, periodic reports to shareholders and regulatory reports, among other services. These accounting and legal services fees incurred for the year ended December 31, 2021 amounted to an annual rate of 0.05% of the fund's average net assets.

Trustee expenses. The fund compensates each Trustee who is not an employee of the Advisor or its affiliates.

Co-investment. Pursuant to an Exemptive Order issued by the SEC, the fund is permitted to negotiate certain investments with entities with which it would be restricted from doing so under the 1940 Act, such as the Advisor and its affiliates. The fund is permitted to co-invest with affiliates if certain conditions are met. For example, the Advisor makes an independent determination of the appropriateness of the investment for the fund. Also, a "required majority" (as defined in the 1940 Act) of the fund's independent trustees make certain conclusions in connection with a co-investment transaction as set forth in the order, including that (1) the terms of the transactions, including the consideration to be paid, are reasonable and fair to the fund and shareholders and do not involve overreaching by the fund or shareholders on the part of any person concerned and (2) the transaction is consistent with the interests of shareholders and is consistent with the fund's investment objective and strategies. During the year ended December 31, 2021, commitments entered into by the fund pursuant to the exemptive order amounted to $127,381,135, including unfunded commitments of $48,270,606.

5. Fund share transactions

Affiliates of the fund owned 100% of shares of the fund on December 31, 2021.

6. Purchase and sale of securities

Purchases and sales of securities, other than short-term investments, amounted to $106,792,190 and $58,072,639, respectively, for the year ended December 31, 2021.

7. Coronavirus (COVID-19) pandemic

The novel COVID-19 disease has resulted in significant disruptions to global business activity. A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, which may lead to less liquidity in certain instruments, industries, sectors or the markets generally, and may ultimately affect fund performance.

8. LIBOR discontinuation risk

LIBOR (London Interbank Offered Rate) is a measure of the average interest rate at which major global banks can borrow from one another. Following allegations of rate manipulation and concerns regarding its thin liquidity, in July 2017, the U.K. Financial Conduct Authority, which regulates LIBOR, announced that it will stop encouraging banks to provide the quotations needed to sustain LIBOR. As market participants transition away from LIBOR, LIBOR's usefulness may deteriorate. The transition process may lead to

John Hancock GA Senior Loan Trust

Notes to financial statements 12-31-21

increased volatility and illiquidity in markets that currently rely on LIBOR to determine interest rates. LIBOR's deterioration may adversely affect the liquidity and/or market value of securities that use LIBOR as a benchmark interest rate.

The ICE Benchmark Administration Limited, the administrator of LIBOR, ceased publishing most LIBOR maturities, including some US LIBOR maturities, on December 31, 2021, and is expected to cease publishing the remaining and most liquid US LIBOR maturities on June 30, 2023. It is expected that market participants will transition to the use of alternative reference or benchmark rates prior to the applicable LIBOR publication cessation date. However, although regulators have encouraged the development and adoption of alternative rates such as the Secured Overnight Financing Rate (SOFR), the future utilization of LIBOR or of any particular replacement rate remains uncertain.

The impact on the transition away from LIBOR referenced financial instruments remains uncertain. It is expected that market participants will amend such financial instruments to include fallback provisions and other measures that contemplate the discontinuation of LIBOR. To facilitate the transition of legacy derivatives contracts referencing LIBOR, the International Swaps and Derivatives Association, Inc. launched a protocol to incorporate fallback provisions. There are obstacles to converting certain longer term securities to a new benchmark or benchmarks and the effectiveness of one versus multiple alternative reference rates has not been determined. Certain proposed replacement rates, such as SOFR, are materially different from LIBOR, and will require changes to the applicable spreads. Furthermore, the risks associated with the conversion from LIBOR may be exacerbated if an orderly transition is not completed in a timely manner.

9. New accounting pronouncement

In March 2020, the Financial Accounting Standards Board (FASB) issued an Accounting Standards Update (ASU), ASU 2020-04, which provides optional, temporary relief with respect to the financial reporting of contracts subject to certain types of modifications due to the planned discontinuation of the LIBOR and other IBOR-based reference rates as of the end of 2021. The temporary relief provided by ASU 2020-04 is effective for certain reference rate-related contract modifications that occur during the period March 12, 2020 through December 31, 2022. Management expects that the adoption of the guidance will not have a material impact to the financial statements.

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Trustees of John Hancock GA Senior Loan Trust

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of John Hancock GA Senior Loan Trust (the "Fund"), including the portfolio of investments, as of December 31, 2021, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets and the financial highlights for the year ended December 31, 2021 and the period from November 3, 2020 (commencement of operations) through December 31, 2020 and the related notes (collectively referred to as the "financial statements"). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund at December 31, 2021, the results of its operations and cash flows for the year then ended, the statements of changes in its net assets and its financial highlights for the year ended December 31, 2021 and the period from November 3, 2020 (commencement of operations) through December 31, 2020, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund's financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) ("PCAOB") and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund's internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund's internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2021, by correspondence with the custodian and others. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more John Hancock investment companies since 2019.

Boston, Massachusetts

February 18, 2022

John Hancock GA Senior Loan Trust

Tax information

Unaudited

For federal income tax purposes, the following information is furnished with respect to the distributions of the fund, if any, paid during its taxable year ended December 31, 2021.

The fund reports the maximum amount allowable as Section 163(j) Interest Dividends.

The fund paid $102,806 in long term capital gain dividends.

Qualified Interest Income ("QII") and Qualified Short-Term Capital Gain ("QSTCG")

NonResident Alien ("NRA") shareholders are normally subject to a 30% (or lower tax treaty rate depending on the country) NRA withholding tax on income and short-term capital gain dividends paid by a mutual fund, unless such dividends are designated as qualified interest income or qualified short-term capital gains, and therefore exempt from NRA withholding tax. Under the American Jobs Creation Act of 2004, the following percentages of ordinary dividends paid during the fiscal year ended December 31, 2021 are considered to be derived from "qualified interest income," as defined in Section 871(k)(1)(E) of the Code. Further, the following percentages of ordinary dividends paid during the fiscal year ended December 31, 2021 are considered to be derived from "qualified short-term capital gain," as defined in Section 871(k)(2)(D) of the Code.

John Hancock GA Senior Loan Trust | | | | |

| Q1 | Q2 | Q3 | Q4 |

QII | 100% | 98.15% | 95.69% | 97.64% |

QSTCG | — | — | — | 100% |

John Hancock GA Senior Loan Trust

Investment objective, principal investment strategies, and principal risks (unaudited)

Investment Objective

The fund's investment objective is to generate current income.

Principal Investment Strategies

Under normal market conditions, the fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in senior loans. Senior loans include first and second lien term loans, delayed draw term loans, and revolving credit facilities. Senior loans do not include commercial mortgage loans (including subordinated real estate mezzanine financing). The fund will only invest in loans and commitments that are determined to be below investment-grade. The fund's investment policies are based on credit quality at the time of purchase. Credit quality is determined by the Advisor. The fund may invest in loans with a maturity of up to nine years from the closing date of the loan. The Advisor typically expects to employ a buy-and-hold strategy. The fund may invest in loans either by transacting directly at the initial funding date or acquiring loans in secondary market transactions.

The fund may invest in loans secured by substantially all of the assets of the borrower and the other loan parties (subject to customary exceptions), including a pledge of the equity of the borrower and its subsidiaries. While real property is not a primary source of collateral, occasionally mortgages are part of the collateral package if the borrower owns particularly valuable real property. The fund may also invest in subordinated debt obligations to the extent permitted by the fund's investment restrictions.

The Advisor undertakes a comprehensive due diligence process, which includes a credit review and internal loan rating process as well as review of loan terms and collateral.

Principal Risks

An investment in the fund is subject to investment and market risks, including the possible loss of the entire principal invested.

The fund's main risks are listed below in alphabetical order, not in order of importance.

Changing distribution level & return of capital risk. There is no guarantee prior distribution levels will be maintained, and distributions may include a substantial tax return of capital. A return of capital is the return of all or a portion of a shareholder's investment in the fund.

Credit and counterparty risk. The issuer or guarantor of a fixed-income security may not make timely payments or otherwise honor its obligations. A downgrade or default affecting any of the fund's securities could affect the fund's performance.

Cybersecurity and operational risk. Cybersecurity breaches may allow an unauthorized party to gain access to fund assets, customer data, or proprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affecting issuers of a fund's securities may negatively impact performance. Operational risk may arise from human error, error by third parties, communication errors, or technology failures, among other causes.

Delayed funding loans and revolving credit facilities risk. Delayed funding loans and revolving credit facilities may have the effect of requiring the fund to increase its investment in a company at a time when it might not be desirable to do so (including at a time when the company's financial condition makes it unlikely that such amounts will be repaid). Delayed funding loans and revolving credit facilities are subject to credit, interest rate and liquidity risk and the risks of being a lender.

John Hancock GA Senior Loan Trust

Investment objective, principal investment strategies, and principal risks (unaudited)

Economic and market events risk. Events in the U.S. and global financial markets, including actions taken by the U.S. Federal Reserve or foreign central banks to stimulate or stabilize economic growth, may at times result in unusually high market volatility, which could negatively impact performance. Reduced liquidity in credit and fixed-income markets could adversely affect issuers worldwide. Banks and financial services companies could suffer losses if interest rates rise or economic conditions deteriorate.

As a result of continued political tensions and armed conflicts, including the Russian invasion of Ukraine commencing in February of 2022, the extent and ultimate result of which are unknown at this time, the United States and the European Union, along with the regulatory bodies of a number of countries, have imposed economic sanctions on certain Russian corporate entities and individuals, and certain sectors of Russia's economy, which may result in, among other things, the continued devaluation of Russian currency, a downgrade in the country's credit rating, and/or a decline in the value and liquidity of Russian securities, property or interests. These sanctions could also result in the immediate freeze of Russian securities and/or funds invested in prohibited assets, impairing the ability of a fund to buy, sell, receive or deliver those securities and/or assets. Economic sanctions and other actions against Russian institutions, companies, and individuals resulting from the ongoing conflict may also have a substantial negative impact on other economies and securities markets both regionally and globally, as well as on companies with operations in the conflict region, the extent to which is unknown at this time.

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange trading suspensions and closures, and affect fund performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future, could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the fund's performance, resulting in losses to your investment.

Fixed-income securities risk. A rise in interest rates typically causes bond prices to fall. The longer the average maturity or duration of the bonds held by a fund, the more sensitive it will likely be to interest-rate fluctuations. An issuer may not make all interest payment or repay all or any of the principal borrowed.

Changes in a security's credit quality may adversely affect fund performance. Increases in real interest rates generally cause the price of inflation-protected debt securities to decrease.

Illiquid and restricted securities risk. Illiquid and restricted securities may be difficult to value and may involve greater risks than liquid securities. Illiquidity may have an adverse impact on a particular security's market price and the fund's ability to sell the security.

LIBOR discontinuation risk. The publication of the London Interbank Offered Rate (LIBOR), which many debt securities, derivatives and other financial instruments use as the reference or benchmark rate for interest rate calculations, was discontinued for most maturities at the end of 2021, and is expected to be discontinued on June 30, 2023 for the remaining maturities. The transition process away from LIBOR may lead to increased volatility and illiquidity in markets that currently rely on LIBOR to determine interest rates, and the eventual use of an alternative reference rate may adversely affect the fund's performance. In addition, the usefulness of LIBOR may deteriorate in the period leading up to its discontinuation, which could adversely affect the liquidity or market value of securities that use LIBOR.

Liquidity risk. The extent (if at all) to which a security may be sold without negatively impacting its market value may be impaired by reduced market activity or participation, legal restrictions, or other economic and market impediments. Liquidity risk may be magnified in rising interest rate environments due to higher than normal redemption rates. Widespread selling of fixed-income securities to satisfy redemptions during periods of reduced demand may adversely impact the price or salability of such securities.

John Hancock GA Senior Loan Trust

Investment objective, principal investment strategies, and principal risks (unaudited)

Loan participations risk. Participations and assignments involve special types of risks, including credit risk, interest rate risk, liquidity risk, and the risks of being a lender. Investments in loan participations and assignments present the possibility that a fund could be held liable as a co-lender under emerging legal theories of lender liability. If a fund purchases a participation, it may only be able to enforce its rights through the lender and may assume the credit risk of the lender in addition to the borrower.

Lower-rated and high-yield fixed-income securities risk. Lower-rated and high-yield fixed-income securities (junk bonds) are subject to greater credit quality risk, risk of default, and price volatility than higher-rated fixed-income securities, may be considered speculative, and can be difficult to resell.

Senior loans risk. Senior loans may be comparatively less liquid relative to markets for other more liquid fixed income securities. Restrictions on transfers in loan agreements, a lack of publicly-available information, irregular trading activity and wide bid/ask spreads among other factors, may, in certain circumstances, make senior loans difficult to value accurately or sell at an advantageous time or price than other types of securities or instruments. Senior loans may have extended trade settlement periods which may result in cash not being immediately available. If an issuer of a senior loan prepays or redeems the loan prior to maturity, the fund may have to reinvest the proceeds in other senior loans or similar instruments that may pay lower interest rates. Senior loans in which the fund invests may or may not be collateralized, although the loans may not be fully collateralized and the collateral may be unavailable or insufficient to meet the obligations of the borrower. The fund may have limited rights to exercise remedies against such collateral or a borrower, and loan agreements may impose certain procedures that delay receipt of the proceeds of collateral or require the fund to act collectively with other creditors to exercise its rights with respect to a senior loan.

Subordinated liens on collateral risk. Certain debt investments that the fund may make will be secured on a second priority basis by the same collateral securing senior secured debt of such companies. The first priority liens on the collateral will secure the fund's obligations under any outstanding senior debt and may secure certain other future debt that may be permitted to be incurred by the fund under the agreements governing the debt. The holders of obligations secured by the first priority liens on the collateral will generally control the liquidation of and be entitled to receive proceeds from any realization of the collateral to repay their obligations in full before the fund is so entitled. There can be no assurance that the proceeds, if any, from the sale or sales of all of the collateral would be sufficient to satisfy the debt obligations secured by the second priority liens after payment in full of all obligations secured by the first priority liens on the collateral.

John Hancock GA Senior Loan Trust

Trustees and Officers

This chart provides information about the Trustees and Officers who oversee the Fund. Officers elected by the Trustees manage the day-to-day operations of the Fund and executed policies formulated by the Trustees.

| Term of Office and | Principal Occupation(s) During Past 5 | Number of Portfolios in Fund |

Name (Birth Year) | Length of Time Served1 | Years | Complex Overseen by Trustee |

Hassell H. McClellan2(1945) | Trustee and Chairperson of the | Director/Trustee, Virtus Funds | 2 |

| Board (since 2020) | (2008-2020); Director, The Barnes | |

| | Group (2010-2021); Associate | |

| | Professor, The Wallace E. Carroll | |

| | School of Management, Boston | |

| | College (retired 2013) Trustee (since | |

| | 2005) and Chairperson of the Board | |

| | (since 2017) of various trusts within | |

| | the John Hancock Fund Complex. | |

| | Trustee and Chairperson of the | |

| | Board, John Hancock GA Senior | |

| | Loan Trust (since 2020). | |

Grace K. Fey2(1946) | Trustee (since 2020) | Chief Executive Officer, Grace Fey | 2 |

| | Advisors (since 2007); Director and | |

| | Executive Vice President, Frontier | |

| | Capital Management Company | |

| | (1988–2007); Director, Fiduciary | |

| | Trust (since 2009). Trustee of | |

| | various trusts within the John | |

| | Hancock Fund Complex (since | |

| | 2008). Trustee, John Hancock GA | |

| | Senior Loan Trust (since 2020). | |

Deborah C. Jackson2(1952) | Trustee (since 2020) | President, Cambridge College, | 2 |

Cambridge, Massachusetts (since 2011); Board of Directors, Amwell Corporation (since 2020); Board of Directors, Massachusetts Women's Forum (2018-2020); Board of Directors, National Association of Corporate Directors/New England (2015-2020); Board of Directors, Association of Independent Colleges and Universities of Massachusetts (2014-2017); Chief Executive Officer, American Red Cross of Massachusetts Bay (2002–2011); Board of Directors of Eastern Bank Corporation (since 2001); Board of Directors of Eastern Bank Charitable Foundation (since 2001); Board of Directors of American Student Assistance Corporation (1996–2009); Board of Directors of Boston Stock Exchange (2002–2008); Board of Directors of Harvard Pilgrim Healthcare (health benefits company) (2007–2011) Trustee of various trusts within the John Hancock Fund Complex (since 2008). Trustee, John Hancock GA Senior Loan Trust (since 2020).

John Hancock GA Senior Loan Trust

Trustees and Officers

Principal Officers who are not Trustees | |

Name (Birth Year) | Position(s) with the Fund | Principal Occupation(s) During Past 5 Years |

| | |

Ian Roke (1969) | President (since 2020) | Vice President, Product Support & Investment Strategy, Global Asset |

| | Liability Management for John Hancock and Manulife (since 2013); |

| | President, John Hancock GA Mortgage Trust (since 2020). |

Heidi Knapp (1970) | Treasurer and Chief Financial | Vice President, John Hancock Life Insurance Company (U.S.A.), |

| Officer (since 2020) | including prior positions (since 2017); Vice President, John Hancock |

| | Life Insurance Company of New York, including prior positions (since |

| | 2017); Vice President, John Hancock Life & Health Insurance |

| | Company, including prior positions (since 2017); Vice President, |

| | Hancock Capital Investment Management, LLC, including prior |

| | positions (since 2018); Treasurer and Chief Financial Officer, John |

| | Hancock GA Mortgage Trust (since 2019). |

Jason M. Pratt (1974) | Chief Compliance Officer (since | Assistant Vice President and Senior Counsel, John Hancock Life |

| 2020) | Insurance Company (U.S.A.) (since 2011); Assistant Vice President, |

| | John Hancock Life Insurance Company of New York (since 2014); |

| | Assistant Vice President, John Hancock Life & Health Insurance |

| | Company (since 2014); Chief Compliance Officer, Hancock Capital |

| | Investment Management, LLC (since 2013); Chief Compliance |

| | Officer, Hancock Capital Management, LLC (since 2013); Chief |

| | Compliance Officer, John Hancock Funding Company, LLC (since |

| | 2018); and Chief Compliance Officer, John Hancock GA Mortgage |

| | Trust (since 2019); Vice President and Senior Counsel, John |

| | Hancock Life Insurance Company (U.S.A), John Hancock Life |

| | Insurance Company of New York, and John Hancock Life & Health |

| | Insurance Company (since 2019). |

E. David Pemstein (1967) | Secretary and Chief Legal Officer | Senior Managing Director and Chief Counsel, North American |

| (since 2020) | Investments for John Hancock and Manulife (since 2015); AVP & |

| | Senior Counsel, North American Investments for John Hancock and |

| | Manulife (since 2006), Secretary and Chief Legal Officer, John |

| | Hancock GA Mortgage Trust (since 2019). |

The business address for all Trustees and Officers is 197 Clarendon Street, Boston, Massachusetts 02116.

The Statement of Additional Information of the fund includes additional information about members of the Board of Trustees.

1Each Trustee holds office until his or her successor is elected and qualified, or until the Trustee's death, retirement, resignation, or removal.

2Member of the Audit Committee.

John Hancock GA Senior Loan Trust

More information