Table of Contents

As filed with the U.S. Securities and Exchange Commission on September 4, 2020.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Mission Produce, Inc.

(Exact name of registrant as specified in its charter)

| California | 0723 | 95-3847744 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

2500 E. Vineyard Avenue, Suite 300

Oxnard, California 93036

(805) 981-3650

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Stephen J. Barnard

President and Chief Executive Officer

2500 E. Vineyard Avenue, Suite 300

Oxnard, California 93036

(805) 981-3650

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Steven B. Stokdyk, Esq. Brent T. Epstein, Esq. Latham & Watkins LLP | Richard D. Truesdell, Jr., Esq. Yasin Keshvargar, Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| ||||

| Title of Each Class of Securities to be Registered | Proposed Maximum | Amount of Registration Fee | ||

Common Stock, par value $0.001 per share | $100,000,000 | $12,980 | ||

| ||||

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have the option to purchase from the registrant. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

SUBJECT TO COMPLETION, DATED SEPTEMBER 4, 2020 the jurisdiction PRELIMINARY PROSPECTUS with Shares filed any in statement securities these Mission Produce, Inc. registration buy Common Stock the to until offer an This is the initial public offering of shares of common stock of Mission Produce, Inc. We are sold seek offering shares of our common stock and the selling stockholders are offering shares. We will be not receive any proceeds from the sale of the shares by the selling stockholders. We estimate that the initial it not public offering price per share will be between $ and $ . For a detailed description of our may does common stock, see the section entitled “Description of Capital Stock”. nor Immediately prior to this offering, there has been no public market for our common stock. We have sell applied to list our common stock on the Nasdaq Global Select Market (“Nasdaq”) under the symbol “AVO”. securities to offer Investing in our common stock involves risks. See “Risk Factors” beginning on page 17. These an . not Per Share Total is changed Initial Public Offering Price $ $ Underwriting Discount(1) $ $ be Proceeds Before Expenses to Us(1) $ $ may prospectus Proceeds Before Expenses to the Selling Stockholders(1) ... $ $ and (1) See “Underwriting” preliminary We have granted the underwriters an option for a period of 30 days following the date of this complete prospectus to purchase up to an additional shares of common stock solely to cover over-allotments at This the initial public offering price, less the underwriting discount not is Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus Any effective representation to the contrary is a criminal offense prospectus is The underwriters expect to deliver the shares to purchasers on or about , 2020 through the permitted book-entry facilities of The Depository Trust Company preliminary Commission not is Active Bookrunners this sale BofA Securities J.P Morgan Citigroup in Exchange or Co-Managers and offer Roth Capital Partners Stephens Inc D A Davidson & Co information the The Securities where Prospectus dated , 2020

Table of Contents

Mission world’s finest avocados

Table of Contents

Mission world’s finest avocados $6 BILLION U.S. MARKET Y-2018 %9 CAGR Y-2008-2018 $14 BILLION GLOBAL AVOCADO MARKET Y-2018 OVER 35 YEARS OF EXCELLENCE IN OVER 25 COUNTRIES 4 PACKING HOUSES 11 DISTRIBUTION CENTERS AVOCADO PUREPLAY GLOBAL LEADER VERTICAL INTEGRATION WITH OVER 10,000 ACRES 2009-2019 CAGR (1)(2) Revenue 14%, Volume 12% Revenue ($mm) Volume (mm lbs.) Note: Fiscal year ends October 31. Revenue reflects Mission Produce only. (1) 2009 to 2012, revenues include asparagus sales (average of -$16mm of sales per year) (2) 2018, 2019, and LTM revenues include International Farming segment revenues $299 172 2009 $265 233 2010 $377 227 2011 $401 331 2012 $445 389 2013 $490 381 2014 $544 450 2015 $600 487 2016 $853 503 2017 $868 640 2018 $883 559 2019 $934 575 LTM Q2’20

Table of Contents

| 1 | ||||

| 11 | ||||

| 13 | ||||

| 17 | ||||

| 34 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 39 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 40 | |||

| 58 | ||||

| 70 | ||||

| 78 | ||||

| 89 | ||||

| 91 | ||||

| 92 | ||||

| 96 | ||||

MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR COMMON STOCK | 98 | |||

| 102 | ||||

| 110 | ||||

| 110 | ||||

| 110 | ||||

| F-i |

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only under circumstances and in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. Our business, financial condition, results of operations and prospectus may have changed since that date.

For investors outside the U.S., we have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this offering in any jurisdiction where action for that purpose is required, other than in the U.S. Persons outside the U.S. who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the U.S. See “Underwriting.”

Trademarks, Trade Names and Service Marks

This prospectus includes our trademarks, trade names and service marks, such as “Mission Produce,” which are protected under applicable intellectual property laws and are our property. This prospectus also contains trademarks, trade names and service marks of other companies, which are the property of their

i

Table of Contents

respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights to these trademarks, trade names and service marks. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

Explanatory Note

Mission Produce, Inc., the registrant whose name appears on the cover page of this registration statement, is a California corporation. Prior to the sale and issuance of any shares of our common stock subject to this registration statement, Mission Produce, Inc. will reincorporate as a Delaware corporation and will retain its current name, Mission Produce, Inc.

Market, Industry and Other Data

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate, including our general expectations and market position, market opportunity and market size, is based on reports from various sources, including those set forth below. Because this information involves a number of assumptions and limitations, you are cautioned not to give undue weight to such information.

| • | Hass Avocado Board, 2018 Market Review: World (September / October 2018); Avocado Volume, Consumption and Production Area Analysis and Projection 2010-2025 (January 2020); Global Trade Reports; Hispanic Avocado Shopper Trends (2018); Millennial Avocado Shopper Trends (2019); Avocado Shopper Insights: Regional Demographics and Purchase Trends (2018) |

| • | United States Department of Agriculture, Economic Research Service (October 2019) |

| • | California Avocado Commission, Foodservice Represents a Golden Opportunity for California Avocados (Winter 2018) |

| • | Korea Customs Service, Import/export by Commodity (August 2020) |

| • | South African Avocado Growers Association, Overview of SA Avocado Industry (January 2019) |

| • | Food and Agriculture Organization of the United States, Major Tropical Fruits Market Review 2018 (2018); Major Tropical Fruits Preliminary Market Results 2019 (2019), Major Tropical Fruits Preliminary Market Results 2019 (2019) |

| • | Transparency Market Research, Global Avocado Market to Reach US $21.56 bn by 2026, Increasing Health Consciousness Among People to Promote Growth (March 2019) |

| • | The World Bank, World Development Indicators (July 2020) |

In addition, projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section captioned “Risk Factors” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in the estimates made by third parties and by us.

ii

Table of Contents

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes included elsewhere in this prospectus before making an investment decision. Unless the context otherwise requires, the terms “Mission,” “the Company,” “we,” “us” and “our” refer to Mission Produce, Inc. and its consolidated subsidiaries. Our fiscal year ends on October 31. Accordingly, references to fiscal 2019 refer to the year ended October 31, 2019.

Introduction

We are a world leader in sourcing, producing and distributing fresh avocados, serving retail, wholesale and foodservice customers in over 25 countries. We source, produce, pack and distribute avocados to our customers and provide value-added services including ripening, bagging, custom packing and logistical management. In addition, we provide our customers with merchandising and promotional support, insights on market trends and training designed to increase their retail avocado sales. Our operations consist of four packing facilities in the United States, Mexico and Peru, 11 distribution and ripening centers across the U.S., Canada, China and the Netherlands, as well as three sales offices in the U.S., China and the Netherlands. We own over 10,000 acres in Peru, of which over 8,300 acres are currently producing primarily avocados, and the remaining are greenfields that we intend to plant and harvest over the next few years. Since our founding in 1983, we have focused on long-term growth, innovation and strategic investments in our business, and reliable execution in our commitments to suppliers and customers. We operate within a strong and growing avocado industry and have played a major role in many of the industry’s innovations over the last 30 years. For example, we believe we were the first U.S. company to import avocados from Mexico, Peru and Chile, and were the first to incorporate ripening centers in to the distribution process.

We source and pack avocados primarily from Mexico, California and Peru, in addition to Colombia, Guatemala and Chile. By utilizing our own land and our relationships with thousands of third-party growers, we have access to complementary growing seasons, and are thus able to provide our customers with year-round supply. Our diversified sourcing also mitigates the impact of periodic, geographically-specific disruptions. Our packing facilities are among the largest in the world, both in terms of square footage and volume processed, and have advanced systems such as optical grading and sorting technology that analyzes and grades each piece of fruit and enables us to select fruit for our customers based on specifications. These facilities also enable us to control local supply logistics in the areas from which we source avocados.

We have developed a sophisticated global distribution network to transport avocados efficiently from our packing facilities to our customers around the world. We have invested in and manage the cold chain and other key logistics to ensure the fruit arrives to the customer in the optimal condition and level of ripeness. The U.S. is our largest market, where our ripening and distribution centers enable us to store and ripen avocados in close proximity to our highest volume customers nationwide. As a result, we are able to quickly fill our customers’ orders and adapt to their volume and ripeness preferences. Our dependability in delivering high quality avocados has led to long-term relationships with retail and foodservice customers. All of our top 10 customers in fiscal 2019 have been customers for at least 10 years and the majority have been customers for over 20 years.

For over 35 years, we have invested in people, state-of-the-art technology and avocado-specific infrastructure to better serve our customers and suppliers. Throughout our history, we have focused on conducting our business with honesty, respect and loyalty. Whether it be through water conservation, increasing

1

Table of Contents

use of renewable energy sources, providing meals, transportation and on-site healthcare to our employees in Peru or sponsoring higher-level education for our employees in the U.S., we are committed to operating in a socially responsible and environmentally sustainable manner. Our corporate culture embodies these values and, as a result, we believe we have a highly motivated and skilled work force that is committed to our business.

We have experienced strong growth in volumes and sales over the last 10 years. The charts below show the increases in our volumes and revenues during that period. To continue our growth, we intend to expand our diversified sourcing across third-party growers and our own farms and enhance our distribution network, as we believe the demand for our avocados will continue to grow globally.

Industry Overview

The avocado industry is comprised of several types of avocados that vary by size and shape of fruit, size of seed, texture of skin, color, taste and availability throughout the year. The Hass avocado dominates the market, representing approximately 95% of the consumed avocados in the U.S. and approximately 80% globally in 2019 according to Avocados from Mexico.

U.S. Avocado Industry

The U.S. Hass avocado industry had a total market value of $6.5 billion in 2019. According to the U.S. Department of Agriculture, total avocado consumption has steadily grown from 1.1 billion pounds in 2008 to 2.6 billion pounds in 2018, representing a compound annual growth rate, or CAGR, of 9.4%. This growth has been driven in part by a significant increase in per capita consumption, growing from 3.5 pounds in 2008 to 8.0 pounds in 2018. In 2017, over half of U.S. households purchased avocados according to Hass Avocado Board. Most avocados sold in the U.S. are imported from other countries. In 2018, California accounted for 96% of U.S. production, however, 76% of national avocado consumption was imported from Mexico.

U.S. retail avocado prices tend to fluctuate over time. In 2019, the average retail price per pound of Hass avocados was $2.57, an increase of 6% from the 2018 average retail price per pound of $2.42. Fluctuations are primarily driven by supply dynamics, which can be impacted by adverse weather and growing conditions, pest and disease problems, government regulations and other supply chain factors.

2

Table of Contents

The following table sets forth historical U.S. Hass avocado volumes, retail prices and implied total market value for the indicated years:

U.S. Hass Avocado Industry—Historicals | 2015 | 2016 | 2017 | 2018 | 2019 | |||||||||||||||

Volume (lbs in millions) | 2,142 | 2,189 | 2,074 | 2,477 | 2,509 | |||||||||||||||

Retail Price | $ | 2.30 | $ | 2.45 | $ | 2.83 | $ | 2.42 | $ | 2.57 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Market Value ($ in millions) | $ | 4,927 | $ | 5,363 | $ | 5,869 | $ | 5,994 | $ | 6,458 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Source: Hass Avocado Board—Avocado volume, consumption and production area analysis and projection 2010-2025

The following table sets forth total U.S. avocado sales by product origin, in millions of pounds, for the years indicated:

U.S. Total Avocado Sales by Product Origin | 2015 | 2016 | 2017 | 2018 | ||||||||||||

Domestic Production | 346 | 458 | 265 | 371 | ||||||||||||

Imports | 1,912 | 1,895 | 1,985 | 2,289 | ||||||||||||

Less: Exports | (18 | ) | (28 | ) | (17 | ) | (37 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total | 2,240 | 2,325 | 2,233 | 2,623 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Source: United States Department of Agriculture—Economic Research Service

The following table sets forth total U.S. imports of fresh avocados by country of origin, in millions of pounds, for the years indicated:

U.S. Avocado Imports by Country of Origin | 2015 | 2016 | 2017 | 2018 | ||||||||||||

Mexico | 1,773 | 1,731 | 1,708 | 1,993 | ||||||||||||

Peru | 102 | 70 | 142 | 181 | ||||||||||||

Chile | 17 | 58 | 82 | 57 | ||||||||||||

Dominican Republic | 21 | 37 | 53 | 58 | ||||||||||||

Colombia | — | — | <1 | 1 | ||||||||||||

Other | <1 | <1 | <1 | <1 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | 1,912 | 1,895 | 1,985 | 2,289 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Source: United States Department of Agriculture—Economic Research Service

The U.S. Hass avocado market is expected to continue at a 5.5% CAGR from 2019 to 2023, with the industry reaching more than $8.0 billion in revenues in 2023 according to Hass Avocado Board. There are multiple factors contributing to the industry growth. One driver is the growing interest in healthy eating and focus on nutrient-dense foods. Avocados contain nearly twenty vitamins and minerals as well as mono-unsaturated fats (commonly referred to as “good” fats), which can help the body absorb nutrients like Vitamin A, D, K and E. Avocado is also considered to be a superfood given its superior nutritional quality and functional benefits. In addition to health and wellness trends, the accessibility of year-round, ready-to-eat avocados has also been a significant growth driver, brought on by improvement in global sourcing and ripening programs. Finally, favorable demographic shifts have contributed to growth in U.S. avocado consumption. Within the growing Hispanic population in the U.S., avocado consumption is 45% higher than non-Hispanic household consumption. The millennial generation is also embracing foods from other countries and is open to new diets. In 2018, 60.1% of millennial households purchased avocados versus 51.3% of non-millennial households. The increasing consumption of avocados has also led restaurants to introduce avocado-focused items that are in high demand. In the past 10 years, the use of avocados in the foodservice channel has increased 26%.

3

Table of Contents

Global Avocado Industry

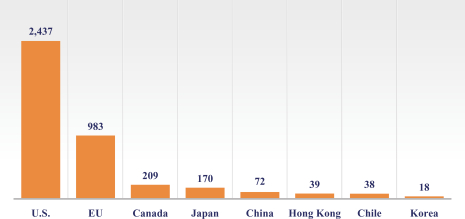

Similar to the U.S., global avocado consumption is exhibiting strong growth dynamics. Global production reached 13.9 billion pounds in 2018, representing a 6.7% increase from 2017. The overall market size reached $13.5 billion of revenues in 2018 and is expected to grow at a 5.9% CAGR between 2018 and 2026 according to Transparency Market Research. The U.S. and the EU hold the largest shares of the import markets, representing 52% and 28% of volumes in 2018. Key export countries include Mexico, Peru and Chile, representing 60%, 13% and 8% of volumes in 2018.

The following table sets forth per-capita avocado consumption in 2018, for the countries indicated:

Mexico | U.S. | Canada | EU | Japan | Korea | |||||||||||||||||||

2018 Per-Capita Avocado Consumption (in lbs) | 14.9 | 8.0 | 5.5 | 2.3 | 1.1 | 0.5 | ||||||||||||||||||

Source: Hass Avocado Board, Korea Customs Service, The World Bank, United States Department of Agriculture—Economic Research Service. Korea per capita consumption based on total imported volume over total population.

Avocado consumption in international markets has also grown, and we believe these markets are primed for continued expansion. The EU, the second largest import market globally, grew imports at a 16.5% CAGR from 2016 to 2018. Avocado consumption increased accordingly over that time period, reaching annual per capita consumption of 2.3 pounds in 2018. In 2019, extraordinary market disruptions led to a 26.1% decline in avocado imports to the EU. Peru, a key export market to the EU, experienced heavy rainfall in the first quarter of the year which damaged crops and hindered access to some farms. These supply constraints impacted the volume of fruit available and reduced overall exports from Peru by 35.8%, following record volumes in 2018. Although this dynamic had an outsized impact on EU imports, we believe that the EU avocado market will experience robust growth in the future. We also believe that the current low levels of consumption in China, Japan and Korea will drive future growth in these markets.

The following chart sets forth import volume of Hass avocados by top importing markets, in millions of pounds, in 2019:

Source: Hass Avocado Board, Korea Customs Service

Several trends are contributing to the increased consumption of avocados globally. Similar to the U.S. market, the global market has been driven by an increased focus on healthy food consumption. In addition, a growing global middle class and higher disposable incomes enable healthier diets. The avocado is also a highly versatile product. There are several uses for avocados beyond guacamole, across cuisines and times of day for both savory and sweet dishes.

4

Table of Contents

Supply and Demand Dynamics

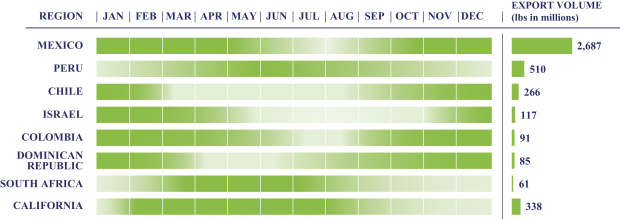

Due to the rapidly increasing demand for avocados globally, the overall market tends to be dictated by supply dynamics. A majority of global avocado supply comes from Latin America. Mexico’s production accounted for more than one-third of global output in 2018. Supply dynamics and seasonality for the avocado fruit has also changed significantly over time. While growing seasons vary widely by region, improvements in sourcing and distribution have led to a year-round availability of avocados. Each market has a highly fragmented grower base. We estimate that California has more than 5,000 growers while Mexico has over 25,000.

The following chart sets forth Hass avocado growing seasons for top exporting countries and export volume, as well as the California growing season and production, in millions of pounds, for 2019:

Source: Hass Avocado Board, South African Avocado Growers Association, and United States Department of Agriculture—Economic Research Service. Given the lack of avocado exports from the U.S., California volume denotes 2018 production volume rather than export volume.

Technology and innovations to supply chain management have enabled distributors to extend and better maintain the fresh life cycle of the fruit. With these enhancements, distributors are able to more efficiently respond to changing needs of their customers in real time.

Ready-to-eat avocados have become a key market driver. This product requires capabilities in ripening, packing and distribution to ensure freshness, quality and consistency. Serving global customers across retail and foodservice channels also requires a strong distribution network. Due to these dynamics, avocado distribution is a fragmented market as very few companies have all of these capabilities. We believe we are well-positioned to benefit from industry characteristics and trends and build upon our leading market share in the U.S.

Competitive Strengths

Established Market Leader with Scale in Large and Growing Market

We produce, source and distribute avocados globally with leading market share in the highly fragmented U.S. market and an expanding presence in other countries. In fiscal 2019, we distributed 559 million pounds of avocados, which is 58% more than our closest competitor in terms of volume. We are well-positioned to continue to capture growth from the attractive U.S. market, which is projected to grow to over $8 billion of sales in 2023. We have a large and global footprint with locations in eight countries, which positions us to serve customers in a variety of markets. We supply national grocers and foodservice customers through our sourcing and distribution network, and with our global platform we are able to grow with our existing customer base as well as expand into

5

Table of Contents

new markets. Additionally, as a result of the large volumes we sell, we are able to achieve economies of scale throughout the value chain, including reduced transportation costs. We believe our leadership position built over the last four decades, in an otherwise fragmented market, will continue to drive sales.

Diverse Global Sourcing with Year-Round Supply and Well-Established Relationships with Growers

We source and pack from what we believe are the best avocado growing regions in North and South America. We source from thousands of growers, primarily in Mexico, California, and Peru, and have developed relationships with growers in other Latin American countries such as Colombia, Chile and Guatemala. We have a minimum of two countries of origin available throughout the year to meet demand. Throughout our history, we have found new locations around the world to source fruit in order to meet the growing global demand. For example, we were the first major avocado distributor in the U.S. to import from Mexico, Peru and Chile. The track record we have developed of delivering on our commitments to growers since our founding in 1983 has enabled us to develop additional sourcing relationships with new growers in diverse geographies. We believe our diverse sourcing capability will continue to drive sales growth by reducing potential interruptions in the supply of avocados to market and differentiating our reliability and reputation to our retail and foodservice customers.

Global Distribution Network Delivering Avocados to Diverse and Long-Standing Customer Base

The people, processes, facilities and relationships that allow us to source and deliver avocados to customers around the world to their specifications of ripeness and volume represent a competitive advantage that we have built over decades. Our global footprint of 18 facilities, including four packing facilities, 11 distribution and ripening centers and three sales offices, provides proximity to key growers and customers. Proximity to growers enables us to develop stronger relationships, control the logistics of the supply chain from tree to packing, and export fruit from the country of origin faster. Proximity to customers allows us to better provide the fruit on time and to specification, and to adapt to changing customer volume and ripeness needs. We have built high-quality, diverse and long-standing customer relationships due to our consistent execution across our global distribution network. All of our top 10 customers in fiscal 2019 have been customers for over 10 years and the majority have been customers for over 20 years. As customer demand changes, our distribution network is able to adapt quickly and efficiently to meet that demand through our full service capabilities. The strength of our global distribution network and relationships with customers enables us to be more competitive in obtaining additional supply from third-party growers, which in turn facilitates our ability to meet customer demand. Our distribution network and customer relationships are competitive advantages that we believe will be difficult for others to replicate.

Extensive Infrastructure With State-of-the-Art Facilities

We have state-of-the-art facilities and strive to be on the leading edge of industry innovations. For example, we introduced the use of hydrocoolers immediately after picking to extend shelf life and market reach. At the same time, we also use ripening centers to prepare avocados for tailored end-market consumption preferences. We have a dedicated research and development department whose sole focus is to optimize our operations through innovation. For example, we believe we were the first to incorporate the role of ripening centers into the distribution process, and we continuously review and analyze methods to extend shelf life after ripening. Our packing facilities provide the processing and storage capacity necessary to optimize the sourcing process and meet customer demand at scale. Our packing facility in Peru has approximately 250,000 square feet of space, which we believe is the largest in the world, and can pack three million pounds of avocados per day. Our two packing facilities in Mexico have leading technology and efficiency and can pack 1.9 million pounds of avocados per day. We also have the technology of advanced optical grading and sorting at our facilities that analyzes and grades each piece of fruit, allowing us to select fruit that is tailored to the customer’s specifications. The infrastructure investments that we have made across our distribution network enable us to meet the needs of customers and foster innovation, which we believe will continue to drive sales.

6

Table of Contents

International Farming and Vertical Integration

In addition to buying avocados from third-party growers, we grow avocados on the land we own or lease. This vertical integration results in greater control over our supply chain and product quality, and allows us to earn a higher gross margin relative to the third-party avocados we sell. We have made significant investments in Peru, which we expect to enhance our margins as trees mature and greenfields come online. In 2019, we produced approximately 11% of the avocados we sold, and we expect the volume of avocados that we grow to increase as our trees mature. Owning and farming our own avocado orchards also helps to mitigate potential disruptions across our third-party grower supply relationships. We forecast avocado sourcing costs for the season for our own production, which enables us to enter into fixed price contracts with customers for a season without bearing pricing risk from spot market purchases. We believe this is a significant competitive advantage. Fixed prices across a season provide our customers with accurate forecasts and inventory in a commodity-based industry. In fiscal 2019, approximately 65% of our total Peru volume, which was primarily sourced from Mission-grown orchards, was sold into fixed price contracts. This seasonal fixed price offering strengthens our relationships with customers and differentiates our products and services. We believe this vertical integration drives sales, increases margins, and positions us well to meet increasing demand across the industry.

Experienced Leadership Who Nurture a Culture of Innovation and Growth

We are led by an experienced management team with significant industry experience. Five members of our management team have each been with us for over thirty years. Our team has transformed a small business into a leading avocado sourcer, producer, and distributor with a global network and leading market share. Our founder, Steve Barnard, is a well-known industry pioneer and veteran, and he continues to lead us with an entrepreneurial culture that is focused on innovation and growth. Our operations management brings sophisticated experience across the regions we operate. In particular, our leaders in Peru and Mexico have extensive experience with expanding our operations in those countries. Our broader management team consists of a deep bench of experienced professionals with expertise in sales, finance, and other critical areas, which we believe positions us to execute on our long-term strategy.

Our Growth Strategies

Capitalize on strong growth trends in our core U.S. market by expanding our nationwide distribution network

We plan to capitalize on the continued strong growth trends in the U.S. by expanding our distribution network and overall supply chain capabilities. As the leading avocado company in the market, we believe we are well positioned to grow with our existing customer base and build relationships with new retailers and foodservice partners. We plan to supplement our current nationwide distribution capabilities and enhance our supply chain by opening new facilities to improve our throughput. For example, we currently have plans to open a new distribution and ripening center in Texas in 2021, which is an important entry point for channeling Mexican avocado supply into the U.S. and Canada. This facility will enable us not only to reduce our dependence on third parties for importing and distributing produce, but also to increase our ability to provide value-added services. We will continue to invest in our U.S. distribution capabilities and evaluate opportunities to capitalize on the growing U.S. demand for avocados. We are focused on deploying capital towards facilities and forward distribution centers in order to better service our customers and drive future sales.

7

Table of Contents

Leverage our global supply chain and distribution capabilities to continue developing international markets

We believe there is a significant opportunity to leverage our global supply chain and distribution capabilities to continue developing international markets and support growing global avocado consumption trends, particularly in Europe, Asia and other markets.

| • | Europe: We plan to expand our distribution capabilities throughout Europe to support new direct retail relationships. We will also increase our exports from Peru, Guatemala, Colombia and other regions to provide balance to our year-round supply and to capitalize on the growing demand for avocados throughout Europe. In addition, we believe our seasonal customer programs will help us continue to build our existing relationships and attract new customers across Europe. As we continue to expand throughout the region, we believe our growing scale will enable us to make more direct, ripe and bulk deliveries of our avocado produce to retail customers. |

| • | Asia: We have a longstanding presence in Asia, with over 35 years in Japan, and over 5 years in China and Korea. We expect to maintain and strengthen our relationships with distributors in Japan and Korea and we believe our existing Chinese distribution facilities will serve as a platform upon which we can continue to build out our avocado distribution network. |

| • | Other markets: We will continue to evaluate opportunities to capitalize on growing demand in other international markets, with a focus to expand our operations in South America. We believe Chile represents an attractive opportunity for growth as one of the world’s top avocado consuming countries, and we believe we are well-positioned to be a long-term provider of avocados in the region. |

Diversify sourcing to enhance our global market-leading position and year-round supply position

We plan to continue to expand our avocado supply relationships and build our global infrastructure in order to diversify our sourcing, strengthen our year-round supply and capitalize on the growing avocado demand. We currently have the ability to source our avocados across three primary countries to optimize our produce selection across various seasons and climates. We will continue to evaluate opportunities to build sourcing relationships in new growing regions such as Colombia, Guatemala and South Africa, which we believe will continue to drive growth and allow us to provide our customers with the best avocado supply across all seasons. Our strong relationships with growers provide us with continued access to avocado supply, which enables us to expand our footprint and strengthen our position as one of the world’s leading avocado sourcers, producers and distributors.

Continue to vertically integrate our supply chain

We believe there is an opportunity to strengthen our customer relationships and increase our overall profitability by vertically integrating our supply chain. We have deployed a significant amount of capital expenditures in recent years towards strategically integrating our operations. We plan on continuing to invest in new farming operations, and expect to increase the volume of Mission-grown avocados that we sell, which typically have a higher gross margin than avocados sourced from third-party growers. We also believe our vertically-integrated farming operations and recent avocado farm investments in Peru and other geographies will allow us to grow our global scale and market-leading position through season-long customer programs that provide our customers stable pricing and help ensure access to quality fruit throughout the season. As we continue our efforts to gain more control over and visibility into the quality of our fruit throughout our supply chain, we can continue to provide seasonal customer programs that we believe are a key differentiator compared to our competition.

8

Table of Contents

Summary Risk Factors

Our business is subject to numerous risks and uncertainties, including those in the section entitled ���Risk Factors” and elsewhere in this prospectus. These risks include, but are not limited to, the following:

| • | Our ability to generate revenues is limited by the annual supply of avocados and our ability to purchase or grow additional avocados. |

| • | A significant portion of our revenues are derived from a relatively small number of customers. |

| • | Mexican and Peruvian economic, political and societal conditions may have an adverse impact on our business. |

| • | Our business and earnings are sensitive to seasonal factors and fluctuations in market prices of avocados. |

| • | We and our growers are subject to the risks that are inherent in farming, including weather and price fluctuations. |

| • | Food safety events, including instances of food-borne illness involving avocados, could create negative publicity for our customers and adversely affect sales and operating results. |

| • | We are subject to United States Department of Agriculture and Food and Drug Administration regulations that govern the importation of foreign avocados into the United States. |

| • | Changes to U.S. trade policy, tariff and import/export regulations may adversely affect our operating results. |

| • | We are subject to domestic and international health and safety laws, which may restrict our operations, result in operational delays or increase our operating costs and adversely affect our financial results of operations. |

| • | Compliance with environmental laws and regulations, including laws pertaining to the use of herbicides, fertilizers and pesticides or climate change, or liabilities thereunder, could result in significant costs that adversely impact our business, results of operations, financial position, cash flows and reputation. |

| • | We depend on our infrastructure to have sufficient capacity to handle our business needs, and failure to optimize our supply chain or disruption of our supply chain could have an adverse effect on our business, financial condition and results of operations. |

Corporate Information

We are a California corporation and commenced our principal operations in 1983. Our principal executive offices are located at 2500 E. Vineyard Avenue, Suite 300, in Oxnard, California 93036, and our telephone number is (805) 981-3650. Our website address is www.worldsfinestavocados.com. The information on or that can be accessed through our website is not incorporated by reference into this prospectus, and you should not consider any such information as part of this prospectus or in deciding whether to purchase our common stock.

9

Table of Contents

Implications of being an emerging growth company and smaller reporting company

As a company with less than $1.07 billion of revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. We may remain an emerging growth company for up to five years, or until such earlier time as we have more than $1.07 billion in annual revenue, the market value of our stock held by non-affiliates is more than $700 million (and we have been a public company for at least 12 months and have filed one annual report on Form 10-K with the Securities and Exchange Commission, or the SEC) or we issue more than $1 billion of non-convertible debt over a three-year period. For so long as we remain an emerging growth company, we are permitted and intend to rely on exemptions from disclosure and other requirements that are applicable to other public companies that are not emerging growth companies. These provisions include:

| • | reduced disclosure about our executive compensation arrangements; |

| • | exemption from the non-binding stockholder advisory votes on executive compensation or golden parachute arrangements; |

| • | exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting; and |

| • | reduced disclosure of financial information in this prospectus, such as being permitted to include only two years of audited financial information and two years of selected financial information in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure. |

We have taken advantage of some reduced reporting burdens in this prospectus. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock. In addition, the JOBS Act permits an emerging growth company to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies until those standards would otherwise apply to private companies. We have irrevocably elected to avail ourselves of this exemption and, as a result, our financial statements may not be comparable to companies that comply with public company effective dates.

10

Table of Contents

Common stock offered by us | shares | |

Common stock outstanding after this offering | shares | |

Common stock offered by the selling stockholders | shares | |

Underwriters’ option to purchase additional shares of common stock from us | shares | |

Use of proceeds | We estimate that the net proceeds to us from the sale of shares of our common stock in this offering will be approximately $ million based upon the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders. | |

| The principal purposes of this offering are to increase our capitalization and financial flexibility, create a public market for our common stock and thereby enable access to the public equity markets for us and our shareholders. We intend to use the net proceeds to us from this offering for working capital and other general corporate purposes and to fund future acquisitions (if any). See the section captioned “Use of Proceeds” for a more complete description of the intended use of proceeds from this offering. | ||

Proposed trading symbol | “AVO”. | |

Risk factors | Investing in our common stock involves a high degree of risk. See the section titled “Risk Factors” beginning on page 17 and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. | |

Reserved share program | At our request, the underwriters have reserved for sale, at the initial public offering price, up to % of the shares offered by this prospectus to some of our directors, officers, employees and related persons through a reserved share program. If these persons purchase reserved shares, this will reduce the number of shares available for sale to the general public. Any reserved shares that are not so purchased will be offered by the underwriters to the general public on the same terms as the other shares offered by this prospectus. Shares purchased by our directors and officers in the reserved share program | |

11

Table of Contents

| will be subject to lock-up restrictions described in this prospectus. See the section titled “Underwriting—Reserved Share Program” for additional information. |

The number of shares of our common stock that will be outstanding after this offering is based on shares of our common stock outstanding as of , 2020 and excludes:

| • | shares authorized pursuant to our 2020 Incentive Award Plan (the “2020 Plan”), which number does not include any future annual evergreen increases pursuant to the terms of the 2020 Plan; and |

| • | outstanding options to purchase shares under our Amended and Restated 2003 Stock Incentive Plan (the “2003 Plan”) at a weighted average price of $ . |

Except as otherwise indicated, all information in this prospectus assumes:

| • | a -for- stock split; |

| • | no exercise of outstanding options to purchase shares of common stock; and |

| • | no exercise by the underwriters of their right to purchase up to an additional shares of common stock from us to cover overallotments, if any. |

12

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables present consolidated financial and other data. The consolidated balance sheet, income, and cash flow data as of and for the fiscal years ended October 31, 2018 and October 31, 2019 are derived from our audited consolidated financial statements included elsewhere in this prospectus. We have derived the consolidated balance sheet, income, and cash flow data as of and for the six months ended April 30, 2019 and 2020 from our unaudited interim condensed consolidated financial statements included elsewhere in this prospectus. We have prepared the unaudited interim condensed consolidated financial statements on the same basis as the audited consolidated financial statements and have included, in our opinion, all adjustments, consisting only of normal recurring adjustments that we consider necessary for a fair statement of the interim condensed consolidated financial statements.

You should read this data together with our audited consolidated financial statements and related notes, as well as the information under the captions “Selected Consolidated Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. Our historical results are not necessarily indicative of our future results, and results for any interim period below are not necessarily indicative of results for the full year.

Fiscal Year Ended | Six Months Ended | |||||||||||||||

(U.S. dollars in thousands) | October 31, 2018 | October 31, 2019 | April 30, 2019 | April 30, 2020 | ||||||||||||

Statement of Comprehensive Income Data: | ||||||||||||||||

Net sales | $ | 859,887 | $ | 883,301 | $ | 368,040 | $ | 419,100 | ||||||||

Cost of sales | 805,931 | 728,626 | 305,611 | 378,240 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Gross profit | 53,956 | 154,675 | 62,429 | 40,860 | ||||||||||||

Selling, general and administrative expenses | 35,235 | 48,168 | 25,296 | 25,862 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Operating income | 18,721 | 106,507 | 37,133 | 14,998 | ||||||||||||

Interest expense | (5,396 | ) | (10,320 | ) | (5,207 | ) | (4,397 | ) | ||||||||

Equity method income | 12,433 | 3,359 | 1 | 438 | ||||||||||||

Impairment of equity method investment | — | — | — | (21,164 | ) | |||||||||||

Remeasurement gain on acquisition of equity method investee | 62,020 | — | — | — | ||||||||||||

Other income (expense), net | 908 | (3,549 | ) | (880 | ) | 950 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

Income (loss) before income tax expense | 88,686 | 95,997 | 31,047 | (9,175 | ) | |||||||||||

Income tax expense | 16,245 | 24,298 | 7,838 | 4,212 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net income (loss) | $ | 72,441 | $ | 71,699 | $ | 23,209 | $ | (13,387 | ) | |||||||

|

|

|

|

|

|

|

| |||||||||

Net income per share | ||||||||||||||||

Basic | $ | $ | $ | $ | ||||||||||||

Diluted | $ | $ | $ | $ | ||||||||||||

Fiscal Year Ended | Six Months Ended | |||||||||||||||

(U.S. dollars in thousands) | October 31, 2018 | October 31, 2019 | April 30, 2019 | April 30, 2020 | ||||||||||||

Other Information: | ||||||||||||||||

Adjusted Net Income(1) | $ | 23,218 | $ | 75,384 | $ | 24,968 | $ | 8,653 | ||||||||

Combined Adjusted Net Income(1) | $ | 33,701 | $ | 75,384 | $ | 24,968 | $ | 8,653 | ||||||||

Adjusted EBITDA(2) | $ | 43,104 | $ | 122,973 | $ | 43,506 | $ | 22,816 | ||||||||

Combined Adjusted EBITDA(2) | $ | 58,038 | $ | 122,973 | $ | 43,506 | $ | 22,816 | ||||||||

Sales volume (million pounds) | 640 | 559 | 270 | 286 | ||||||||||||

Average sales price per pound(3) | $ | 1.34 | $ | 1.58 | $ | 1.36 | $ | 1.47 | ||||||||

Gross profit per pound(4) | $ | 0.08 | $ | 0.28 | $ | 0.23 | $ | 0.14 | ||||||||

Combined gross profit per pound(4) | $ | 0.14 | $ | 0.28 | $ | 0.23 | $ | 0.14 | ||||||||

13

Table of Contents

As of | ||||||||||||

(U.S. dollars in thousands) | October 31, 2018 | October 31, 2019 | April 30, 2020 | |||||||||

Consolidated Balance Sheet Data: | ||||||||||||

Cash and cash equivalents | $ | 26,314 | $ | 64,008 | $ | 26,568 | ||||||

Total assets | 621,773 | 689,449 | 663,823 | |||||||||

Long-term debt, net of current portion | 192,404 | 174,034 | 174,128 | |||||||||

Capital leases, net of current portion | 2,800 | 4,561 | 4,170 | |||||||||

Total shareholders’ equity | 313,451 | 379,033 | 354,900 | |||||||||

| (1) | The following table presents a reconciliation of net income to Adjusted Net Income and Combined Adjusted Net Income: |

Fiscal Year Ended | Six Months Ended | |||||||||||||||

(U.S. dollars in thousands) | October 31, 2018 | October 31, 2019 | April 30, 2019 | April 30, 2020 | ||||||||||||

Net income (loss) | $ | 72,441 | $ | 71,699 | $ | 23,209 | $ | (13,387 | ) | |||||||

Share-based compensation | 9 | — | — | 686 | ||||||||||||

Unrealized loss on derivative financial instruments | — | 3,669 | 1,006 | 3,445 | ||||||||||||

Remeasurement gain on acquisition of equity method investee | (62,020 | ) | — | — | — | |||||||||||

Impairment of equity method investment | — | — | — | 21,164 | ||||||||||||

Foreign currency gains and (losses) | (1,452 | ) | 1,273 | 1,418 | (3,245 | ) | ||||||||||

Debt extinguishment costs | 920 | — | — | — | ||||||||||||

Tax effects of pre-tax adjustments to net income(a) | 13,320 | (1,257 | ) | (665 | ) | (10 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Adjusted Net Income | $ | 23,218 | $ | 75,384 | $ | 24,968 | $ | 8,653 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Pre-acquisition International Farming Segment Adjusted Net Income, net of tax effects(b) | $ | 10,483 | — | — | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Combined Adjusted Net Income | $ | 33,701 | $ | 75,384 | $ | 24,968 | $ | 8,653 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (a) | The adjustments to calculate Adjusted Net Income are pre-tax adjustments. As such, this adjustment is to eliminate the income tax expense or benefit included in net income related to the pre-tax adjustments and is calculated based on the rate that is applicable to the taxable jurisdiction that the adjustment relates to. |

| (b) | Represents the Adjusted Net Income of Grupo Arato Holdings SAC (“Grupo Arato”) from November 1, 2017 through September 20, 2018 that is not already included in Adjusted Net Income. The Adjusted Net Income for Grupo Arato for the period from November 1, 2017 through September 20, 2018 was calculated by taking 50% of Grupo Arato’s net income from the period from November 1, 2017 through September 20, 2018 which was $8,422 thousand, plus the foreign exchange loss, net of the related income tax benefit, included in Grupo Arato’s net income for the period of $124 thousand. This amount was further increased by $1,937 thousand to eliminate the income tax expense recorded by the Company on its outside basis difference in Grupo Arato while it was being accounted for as an equity method investee. Had the entity been combined as of November 1, 2017, the outside basis difference tax expense would have not been recognized. |

Adjusted Net Income is calculated by adding share-based compensation expense, adding the unrealized loss on derivative financial instruments, subtracting remeasurement gain on acquisition of equity method investees, adding impairment of equity method investment, subtracting foreign currency gains, adding foreign currency losses, adding debt extinguishment costs, and adjusting for the tax effects of these items. Combined

14

Table of Contents

Adjusted Net Income represents Adjusted Net Income further adjusted to include 100% of Grupo Arato’s Adjusted Net Income.

Adjusted Net Income and Combined Adjusted Net Income is included in this prospectus because it is used by management and our board of directors to assess our financial performance. Adjusted Net Income is frequently used by analysts, investors and other interested parties to evaluate companies in our industry. Adjusted Net Income and Combined Adjusted Net Income are not a GAAP measure of our financial performance or liquidity and should not be considered as an alternative to net income, as measures of financial performance, or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP. Adjusted Net Income and Combined Adjusted Net Income should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Additionally, Adjusted Net Income and Combined Adjusted Net Income are not intended to be a measure of free cash flow for management’s discretionary use, as it does not reflect tax payments, debt service requirements, capital expenditures and other cash costs that may recur in the future, including, among other things, cash requirements for working capital needs and cash costs to replace assets being depreciated and amortized. Management compensates for these limitations by relying on our GAAP results in addition to using Adjusted Net Income and Combined Adjusted Net Income supplementally. Our measure of Adjusted Net Income and Combined Adjusted Net Income is not necessarily comparable to similarly titled captions of other companies due to different methods of calculation.

| (2) | The following table presents a reconciliation of net income to Adjusted EBITDA and Combined Adjusted EBITDA: |

Fiscal Year Ended | Six Months Ended | |||||||||||||||

(U.S. dollars in thousands) | October 31, 2018 | October 31, 2019 | April 30, 2019 | April 30, 2020 | ||||||||||||

Net income | $ | 72,441 | $ | 71,699 | $ | 23,209 | $ | (13,387 | ) | |||||||

Interest expense | 5,396 | 10,320 | 5,207 | 4,397 | ||||||||||||

Income tax expense | 16,245 | 24,298 | 7,838 | 4,212 | ||||||||||||

Depreciation and amortization | 9,440 | 16,466 | 6,373 | 7,132 | ||||||||||||

Equity method income(a) | (12,433 | ) | (3,359 | ) | (1 | ) | (438 | ) | ||||||||

Remeasurement gain on acquisition of equity method investee | (62,020 | ) | — | — | — | |||||||||||

Impairment of equity method investment | — | — | — | 21,164 | ||||||||||||

Other income (expense), net | (908 | ) | 3,549 | 880 | (950 | ) | ||||||||||

Share-based compensation | 9 | — | — | 686 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 28,170 | 122,973 | 43,506 | 22,816 | |||||||||||||

International Farming Segment Adjusted EBITDA(a) | 14,934 | — | — | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Adjusted EBITDA | $ | 43,104 | $ | 122,973 | $ | 43,506 | $ | 22,816 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Pre-acquisition International Farming Segment Adjusted EBITDA(b) | 14,934 | — | — | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Combined Adjusted EBITDA | $ | 58,038 | $ | 122,973 | $ | 43,506 | $ | 22,816 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (a) | Includes 50% of Grupo Arato’s Adjusted EBITDA from November 1, 2017 through September 20, 2018, prior to our acquisition of the remaining 50% of this subsidiary. |

| (b) | Represents the remaining 50% of Grupo Arato’s Adjusted EBITDA from November 1, 2017 through September 20, 2018 that is not already included in Adjusted EBITDA. |

15

Table of Contents

Adjusted earnings before interest expense, income tax expense and depreciation and amortization (“Adjusted EBITDA”) is calculated by adding interest expense, income tax expense, depreciation and amortization, subtracting equity method income, subtracting remeasurement gain on acquisition of equity method investee, adding impairment of equity method investment, subtracting or adding other income (expense), net, and adding share-based compensation to net income. Combined Adjusted EBITDA represents Adjusted EBITDA which is further adjusted to include 100% of Grupo Arato’s Adjusted EBITDA as if Grupo Arato was acquired on November 1, 2017. Adjusted EBITDA and Combined Adjusted EBITDA are included in this prospectus because these measures are used by management and our board of directors to assess our financial performance. Adjusted EBITDA is frequently used by analysts, investors and other interested parties to evaluate companies in our industry. Adjusted EBITDA and Combined Adjusted EBITDA are not a GAAP measures of our financial performance or liquidity and should not be considered as an alternative to net income as a measure of financial performance or cash flows from operations as measures of liquidity, or any other performance measure derived in accordance with GAAP. Adjusted EBITDA and Combined Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Additionally, Adjusted EBITDA is not intended to be a measure of free cash flow for management’s discretionary use, as it does not reflect tax payments, debt service requirements, capital expenditures and other cash costs that may recur in the future, including, among other things, cash requirements for working capital needs and cash costs to replace assets being depreciated and amortized. Management compensates for these limitations by relying on our GAAP results in addition to using Adjusted EBITDA and Combined Adjusted EBITDA supplementally. Adjusted EBITDA and Combined Adjusted EBITDA are not necessarily comparable to similarly titled captions of other companies due to different methods of calculation.

| (3) | Calculated by dividing net sales by the total sales volume in the stated period. |

| (4) | Gross profit per pound is calculated by dividing gross profit by the total sales volume in the stated period. Combined gross profit per pound is calculated by dividing gross profit plus the gross profit of Grupo Arato from the period from November 1, 2017 through September 20, 2018 that is not already included in gross profit per pound, divided by the total sales volume in the stated period. |

16

Table of Contents

Risks Related to Our Business

Our ability to generate revenues is limited by the annual supply of avocados and our ability to purchase or grow additional avocados.

Our ability to distribute avocados is currently limited by our ability to acquire supply from third-party growers and to produce on our own farms. With a limited number of avocado trees on our farms and on the farms from which we purchase, our ability to replace supply from third parties and adapt to any changes in demand of our product may be limited. If we are unable to purchase sufficient volumes from third-party growers or demand for our products were to increase in the future, we would need additional production capacity, which may take time, whether by purchasing additional products from third-party suppliers or by waiting for our younger avocado trees to bear fruit. These purchases may expose us to increases in short-term costs and additional production may expose us to additional long-term operating costs. If supply were to decrease dramatically in the future, whether as a result of damage to farms, inclement weather, drought or labor problems, we may not be able to purchase sufficient fruit or the prices would dramatically increase. The impact of the limited supply could decrease our revenues or increase our costs of goods sold, which would harm our business and financial results.

The loss of one or more of our largest customers, or a reduction in the level of purchases made by these customers, could negatively impact our sales and profits.

Sales to our top 10 largest customers amounted to approximately 65% of our total sales in the six months ended April 30, 2020, with our top customer, Kroger (including its affiliates), accounting for approximately 14% of our total sales in the same period. We expect that a significant portion of our revenues will continue to be derived from a relatively small number of customers. We believe these customers make purchase decisions based on a combination of price, product quality, consumer demand, customer service performance, desired inventory levels and other factors that may be important to them at the time the purchase decisions are made. Changes in our customers’ strategies or purchasing patterns, including a reduction in the number of suppliers from which they purchase, may adversely affect our sales. Additionally, our customers may face financial or other difficulties which may impact their operations and cause them to reduce their level of purchases from us, which could adversely affect our results of operations. Customers also may respond to any price increase that we may implement by reducing their purchases from us, resulting in reduced sales of our products. If sales of our products to one or more of our largest customers are reduced, this reduction may have a material adverse effect on our business, financial condition, and results of operations. Any bankruptcy or other business disruption involving one of our significant customers also could adversely affect our results of operations.

We are subject to the risks of doing business internationally.

We conduct a substantial amount of business with growers and customers who are located outside the United States. We purchase avocados from growers and packers in Mexico and other countries, own or lease thousands of acres and operate packing facilities in Peru, have farming joint ventures in Colombia and sell fresh avocados and processed avocado products to foreign customers. We are also subject to regulations and taxes imposed by governments of the countries in which we operate. Significant changes to these government regulations and to assessments by tax authorities can have a negative impact on our operations and operating results.

Our current international operations are subject to a number of inherent risks, including:

| • | Local economic and political conditions, including local corruption or disruptions in supply, labor, transportation and trading; |

17

Table of Contents

| • | Restrictive U.S. and foreign governmental actions, such as restrictions on transfers of funds and trade protection measures, including import/export duties and quotas and customs duties and tariffs; |

| • | Changes in legal or regulatory requirements affecting foreign investment, taxes, imports and exports; and |

| • | Currency fluctuations that could affect our results of operations. |

Moreover, our business is also impacted by the negotiation and implementation of free trade agreements between the United States and other countries, particularly in Mexico, which is the largest source of our supply of avocados. Such agreements can reduce barriers to international trade and thus the cost of conducting business internationally, including the cost of purchasing avocados. For instance, the United States recently ratified a new trilateral trade agreement with the governments of Canada and Mexico, known as the United States-Mexico-Canada Agreement (“USMCA”) to replace the North American Free Trade Agreement (“NAFTA”). If any of the three countries withdraws from the USMCA, our cost of doing business within the three countries could increase.

Mexican economic, political and societal conditions may have an adverse impact on our business.

Mexico is the largest source of our supply of avocados, and our business is affected by developments in that country. Shipments from Mexico to the United States are dependent on the border remaining open to imports, which has closed from time to time. In addition, security institutions in Mexico are under significant stress as a result of organized crime and gang and drug-related violence, which also could affect avocado production and shipments. This situation creates potential risks that could affect a large part of our sourcing in Mexico and would harm our operations if it impacts our facilities or personnel. In addition, Mexican growers strike from time to time to obtain higher prices for their avocados. We cannot provide any assurance that economic conditions or political developments, including any changes to economic policies or the adoption of other reforms proposed by existing or future administrations, in or affecting Mexico will not have a material adverse effect on market conditions or our business, results of operations or financial condition.

Peruvian economic and political conditions may have an adverse impact on our business.

A significant part of our operations are conducted in Peru. Accordingly, our business, financial condition or results of operations could be affected by changes in economic or other policies of the Peruvian government or other political, regulatory or economic developments in the country. During the past several decades, Peru has had a succession of regimes with differing policies and programs. Past governments have frequently intervened in the nation’s economy and social structure. Among other actions, past governments have imposed controls on prices, exchange rates and local and foreign investments, as well as limitations on imports, have restricted the ability of companies to dismiss employees and have prohibited the remittance of profits to foreign investors.

In 2018, Peru experienced heightened political instability derived from various currently ongoing investigations into allegations of money laundering and corruption linked to the “Operation Car Wash” investigation that was initiated by Brazilian authorities. Because we have significant operations in Peru, we cannot provide any assurance that political developments and economic conditions, including any changes to economic policies or the adoption of other reforms proposed by existing or future administrations, in Peru and/or other factors will not have a material adverse effect on market conditions, prices of our securities, our ability to obtain financing and our results of operations and financial condition.

Our earnings are sensitive to fluctuations in market prices of avocados.

The pricing of avocados depends on supply, and excess supply can lead to price competition in our industry. Growing conditions in various parts of the world, particularly weather conditions such as windstorms,

18

Table of Contents

floods, droughts, wildfires and freezes, as well as diseases and pests, are primary factors affecting market prices because of their influence on the supply and quality of product.

Pricing also depends on quality. Fresh produce is highly perishable and generally must be brought to market and sold soon after harvest. The selling price received depends on the availability and quality offered by us to customers and available in the market generally.

Pricing also depends on demand, and consumer preferences for particular food products are subject to fluctuations over time. Shifts in consumer preferences that can impact demand at any given time can result from a number of factors, including dietary trends, attention to particular nutritional aspects, concerns regarding the health effects of particular products, attention given to product sourcing practices and general public perception of food safety risks. Consumer demand for our products also may be impacted by any public commentary that consumers may make regarding our products, as well as by changes in the level of advertising or promotional support that we employ or that are employed by relevant industry groups or third parties. If consumer preferences trend negatively with respect to avocados, our sales volumes may decline as a result.

We are subject to increasing competition that may adversely affect our operating results.

The market for avocados and processed avocado products is highly competitive. Competition for the purchase of avocados from suppliers and the sale of avocados to distributors primarily comes from other avocado distributors. If we are unable to consistently pay growers a competitive price for their avocados, these growers may choose to have their avocados marketed by alternate distributors. If we are unable to offer attractive prices or consistent supply to retail and wholesale customers, they may choose to purchase from other companies. Such competition may adversely affect our volumes and prices, which would harm our business and results of operations.

We and our growers are subject to the risks that are inherent in farming.

Our results of operations may be adversely affected by numerous factors over which we have little or no control and that are inherent in farming, including reductions in the market prices for our products, adverse weather including drought, high winds, earthquakes and wildfires. Growing conditions, pest and disease problems and new government regulations regarding farming and the marketing of agricultural products.

Due to the seasonality of the business, our revenue and operating results may vary from quarter to quarter and year to year.

Our earnings may be affected by seasonal factors, including:

| • | the availability, quality and price of fruit; |

| • | the timing and effects of ripening and perishability; |

| • | the ability to process perishable raw materials in a timely manner; |

| �� | • | fixed overhead costs during off-season months at our farms; and |

| • | the slight impacts on consumer demand based on seasonal and holiday timing. |

In particular, our farming operations in Peru are affected by seasonal factors, as the harvest in Peru is generally concentrated in the third and fourth fiscal quarters.

19

Table of Contents

Our performance may be impacted by general economic conditions or an economic downturn.

An overall decline in economic activity could adversely impact our business and financial results. Economic uncertainty may reduce consumer spending as consumers make decisions on what to include in their food budgets. This could also result in a shift in consumer preference. Shifts in consumer spending could result in increased pressure from competitors or customers that may require us to increase promotional spending or reduce the prices of some of our products and/or limit our ability to increase or maintain prices, which could lower our revenue and profitability. Instability in financial markets may impact our ability, or increase the cost, to enter into new credit agreements in the future. Additionally, it may weaken the ability of our customers, suppliers, third-party distributors, banks, insurance companies and other business partners to perform their obligations in the normal course of business, which could expose us to losses or disrupt the supply of inputs we rely upon to conduct our business. If one or more of our key business partners fail to perform as expected or contracted for any reason, our business could be negatively impacted.

The ongoing COVID-19 pandemic, restrictions intended to prevent its spread and resulting worldwide economic conditions could adversely impact our business, financial condition and results of operations.