UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

☐ Preliminary Proxy Statement

☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2))

☐ Definitive Proxy Statement

☒ Definitive Additional Materials

☐ Soliciting Material Pursuant to §240.14a-12

Nuveen Core Plus Impact Fund

(Exact Name of Registrant as Specified in its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

☒ No fee required.

☐ Fee paid previously with preliminary materials.

☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

Nuveen Real Asset Income and Growth Fund (JRI) Nuveen Multi-Asset Income Fund (NMAI)

Nuveen Variable Rate Preferred and Income Fund (NPFD) Nuveen Core Plus Impact Fund (NPCT)

April 23, 2024 Institutional Shareholder Services Presentation

NUVEEN CLOSED-END FUNDS

Our approach and mindset

Nuveen’s closed-end funds (CEFs) are designed to be long-term investments that help shareholders, primarily retirees or individuals nearing retirement, plan for their financial future by providing consistent, attractive income throughout multiple market cycles.

The Funds offer a broad opportunity for diversification and exposure to asset classes and strategies that retail shareholders normally would not be able to access.

CEFs are designed to provide shareholders an investment structure that can deliver enhanced income and returns over time with liquidity provided through an exchange listing.

Market factors and investor sentiment can turn negative for CEFs impacting secondary market prices, even as funds successfully deliver on their primary investment objective.

For CEF investors, attractive and reliable distributions are what matter.

Volatile market conditions, like equity and fixed income markets in 2022 which had historical negative performance, can cause CEFs to trade at deeper discounts, yet these strategies perform over the life of the fund.

When it comes to governance, there is no substitute for experience–the best way to protect the long-term interests of all CEF shareholders is by nominating a competent, knowledgeable board with CEF-specific experience.

2

GUIDING QUESTIONS

1. Is change warranted?

2. If change is warranted, who is best to effect change?

3

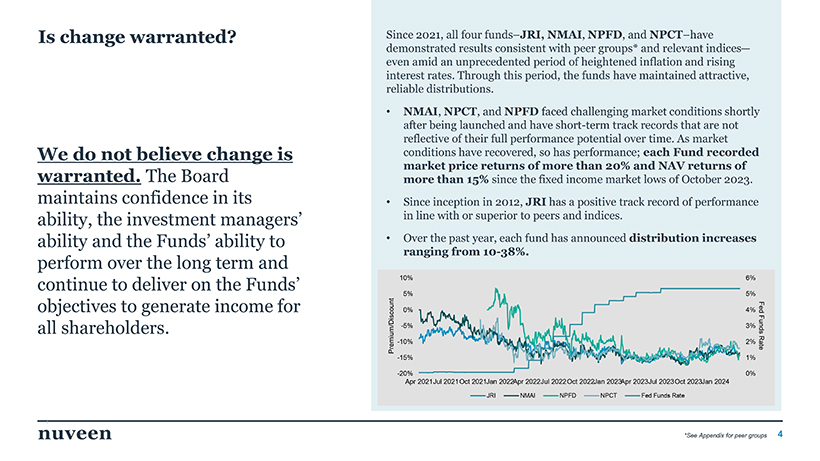

Is change warranted?

We do not believe change is warranted. The Board maintains confidence in its ability, the investment managers’ ability and the Funds’ ability to perform over the long term and continue to deliver on the Funds’ objectives to generate income for all shareholders.

Since 2021, all four funds–JRI, NMAI, NPFD, and NPCT–have demonstrated results consistent with peer groups* and relevant indices—even amid an unprecedented period of heightened inflation and rising interest rates. Through this period, the funds have maintained attractive, reliable distributions.

• NMAI, NPCT, and NPFD faced challenging market conditions shortly after being launched and have short-term track records that are not reflective of their full performance potential over time. As market conditions have recovered, so has performance; each Fund recorded market price returns of more than 20% and NAV returns of more than 15% since the fixed income market lows of October 2023.

• Since inception in 2012, JRI has a positive track record of performance in line with or superior to peers and indices.

• Over the past year, each fund has announced distribution increases ranging from 10-38%.

*See Appendix for peer groups 4

Nuveen Board Nominees are fiduciaries seeking to deliver long-term value to all shareholders and have a record of taking thoughtful actions to enhance shareholder outcomes.

Since 2012, the Board has:

• Authorized 58 CEF mergers, producing highly scaled funds in respective asset classes with:

• Lower fees (breakpoint pricing methodology)

• Enhanced trading efficiencies

• Tightened bid/ask spreads in the secondary market

• Dissident opposed recent proposed fund mergers that would provide benefits to all shareholders;

• Authorized liquidations, mandate adjustments, and mergers into open-end funds;

• Approved a dividend management program to support secondary market trading through enhanced cash flows to shareholders:

• Recent distribution increases across the entire Nuveen fund complex have spurred secondary market trading and added momentum to discount narrowing already underway;

• Approved complex-wide share repurchase program:

• Shares repurchased when there are material supply/demand imbalances

• Bids layered in below market to show depth to the book which can impact supply/demand without share repurchases;

• Established a robust and dedicated IR program to increase awareness, engagement, and advocacy for CEFs.

5

If change is warranted, who is best to effect change?

We do not believe change is warranted.

Incumbent trustees all have deep CEF, investment management, and/or business

leadership experience and are best prepared to protect and advance the

interest of all shareholders by working to achieve investment objectives,

drive long-term performance and deliver consistent, reliable income.

The board’s nominees possess decades of experience in senior executive roles at leading global corporations, asset managers, governmental and legal entities, including:

• Barclays • Morgan Stanley

• BlackRock • Putnam Investments

• Commodity Future Trading Commission • The White House

• FedEx • Invesco

• Janus Capital Group • Verizon Communications

The incumbent trustees are experienced, prepared, and engaged:

19+

Years of Closed-End Fund Experience

23+

Avg. Years of Relevant Business Leadership Experience

~ 100%

Attendance at Board Meetings

6

Jason Chen is inexperienced and unqualified

Jason Chen has zero (0) years of closed-end or other U.S. fund experience and has never served on the board of a publicly listed investment fund, or any public company at all.

Mr. Chen’s recent experience is primarily with smaller firms with negligible AUM and are all based outside of the U.S. Mr. Chen has never served in a senior leadership role at a major corporation, asset manager, or governmental or legal entity.

His lack of relevant experience renders him unqualified to contribute to performance, oversight, and/or corporate governance matters.

Mr. Chen disclosed that his relationship with Saba Capital began after responding to an X (formerly

Twitter) post from Boaz Weinstein soliciting director candidates. Mr. Chen’s nomination did not originate from a rigorous search process, but rather an open-forum social media discussion.

Members of Nuveen’s Nominating and Governance Committee interviewed Mr. Chen as part of the standardized candidate evaluation process that all current Nuveen directors participated in.

• The Board determined that the incumbent set of Trustees possess more direct and relevant experience and would better serve all Fund shareholders.

• Voting for Saba’s nominee on the gold proxy card disenfranchises shareholders because it does not allow them to vote for a full slate of trustee nominees.

Dissident nominee

Jason Chen’s experience:

0

Years of Closed-End Fund Experience

0

Years of U.S. Mutual Fund Experience

0

Relevant Board Director Experiences

0

Shareholder-Focused Experiences

7

Saba’s actions and resulting performance does not benefit all shareholders

BRW DISCOUNT POST-TAKEOVER

SABA DISCOUNT POST-TAKEOVER

Saba Capital Income & Opportunities Fund (BRW)

Since Saba’s 2021 takeover and overhaul of the fund’s investment mandate, BRW trades at a wider, persistent discount to NAV. Under Saba, BRW has significantly underperformed peers and indices compared to the pre-takeover investment strategy1. Shareholders would have been materially better off under Voya’s strategy.

Saba Capital Income & Opportunities Fund II (SABA)

Since Saba’s January 2024 takeover, the fund never declassified its board, a proposal once advocated for by Saba, and the fund has traded at its widest discount. The hedge fund also removed guardrails which protected the fund from trading in risky assets. The fund is now managed with higher fees after the addition of an administrative fee.

Saba’s tender offer failed to allow all shareholders who wanted to exit the fund to do so, trapping retail shareholders in a fund with an inherently riskier investment strategy and with an investment objective that has changed.

Since takeover, Saba has not taken any of the corporate governance actions it advocated for, nor has it lowered fees or stuck to the funds’ stated investment objectives, instead replicating its own hedge fund strategy and vastly underperforming peers. CHANGE IS NOT WARRANTED.

1See Appendix for BRW performance 8

Corporate Governance

The Board has established various committees designed for deeper engagement by trustees in certain oversight functions, all with independent trustees and chairs. Committees include:

Closed-End Funds and Open-End Funds: Each meets quarterly and is responsible for assisting the Board in the oversight and monitoring of the Nuveen Funds that are registered as either closed-end and open-end management investment companies.

Dividend: Meets quarterly and authorizes distributions for the Nuveen Funds’ shares, including, but not limited to, regular and special dividends, capital gains and ordinary income distributions.

Investment: Meets monthly and is responsible for the oversight of Nuveen Fund performance, investment risk management and other portfolio-related matters affecting the Nuveen Funds which are not otherwise the jurisdiction of the other Board committees.

Nominating and Governance: Responsible for seeking, identifying and recommending to the Board qualified candidates for election or appointment to the Board.

Executive: Meets between regular meetings of the Board and is authorized to exercise all the powers of the Board.

Audit: Meets monthly and assists the Board in the oversight and monitoring of the accounting and reporting policies, processes and practices of the Nuveen Funds, and the audits of the financial statements of the Nuveen Funds.

Compliance, Risk Management and Regulatory Oversight: Responsible for the oversight of compliance issues, risk management and other regulatory matters affecting the Nuveen Funds that are not otherwise the jurisdiction of the other committees.

9

ISS Five Factor Framework

Distributions

Total Shareholder Return NAV Premium / Discount Fees & Expenses Corporate Governance

10

Five Factor Framework: Distributions

Summary

Nuveen CEF shareholders seek attractive and reliable distributions from their investment in the Funds.

• Each Fund has delivered attractive and reliable distributions since inception.

• Each Fund has competitive distribution rates on both NAV and market price.

• Approved an enhanced distribution management program across the Nuveen CEF complex, designed to provide investors with incremental cash flows during a challenging market environment while helping support secondary market prices.

• As part of this program each Fund increased distributions over the last six months, ranging from 10.2% to 38.2%.

• Each Fund’s distribution increases were greater than peer averages, contributing to better relative secondary market price performance since the increases were implemented.

• Enhanced distribution levels were set in a thoughtful manner, balancing current earnings with an appropriate level of capital included in the overall distribution.

11

Five Factor Framework: Distributions JRI

KEY DISTRIBUTION METRICS

NAV Distribution Rate

8 .91% 8.88%

JRI PEER AVG.

As of March 31, 2024

Market Price Distribution Rate

10 .12% 9.91%

JRI PEER AVG.

As of March 31, 2024

1-Year Distribution Change

+14 .9% -1.8%

JRI PEER AVG.

As of March 31, 2024

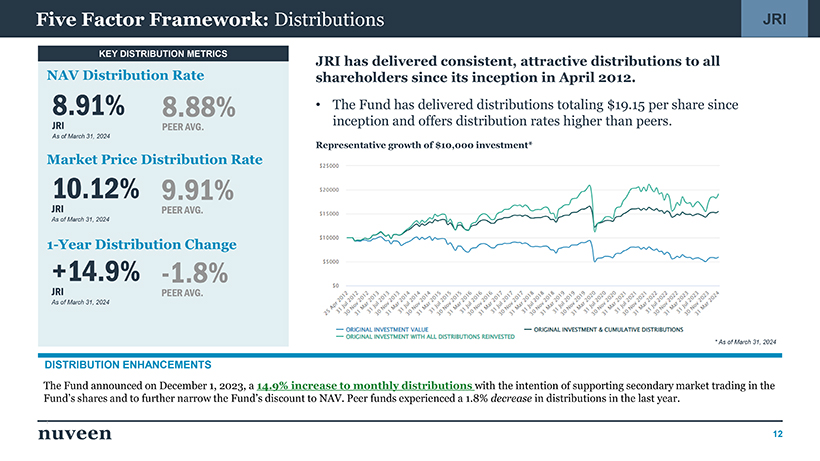

JRI has delivered consistent, attractive distributions to all shareholders since its inception in April 2012.

• The Fund has delivered distributions totaling $19.15 per share since inception and offers distribution rates higher than peers.

Representative growth of $10,000 investment*

DISTRIBUTION ENHANCEMENTS

The Fund announced on December 1, 2023, a 14.9% increase to monthly distributions with the intention of supporting secondary market trading in the

Fund’s shares and to further narrow the Fund’s discount to NAV. Peer funds experienced a 1.8% decrease in distributions in the last year.

12

Five Factor Framework: Distributions NMAI

KEY DISTRIBUTION METRICS

NAV Distribution Rate

11 .59% 9.45%

NMAI PEER AVG.

As of March 31, 2024

Market Price Distribution Rate

12 .86% 10.65%

NMAI PEER AVG.

As of March 31, 2024

1-Year Distribution Change

+33 .3% -7.1%

NMAI PEER AVG.

As of March 31, 2024

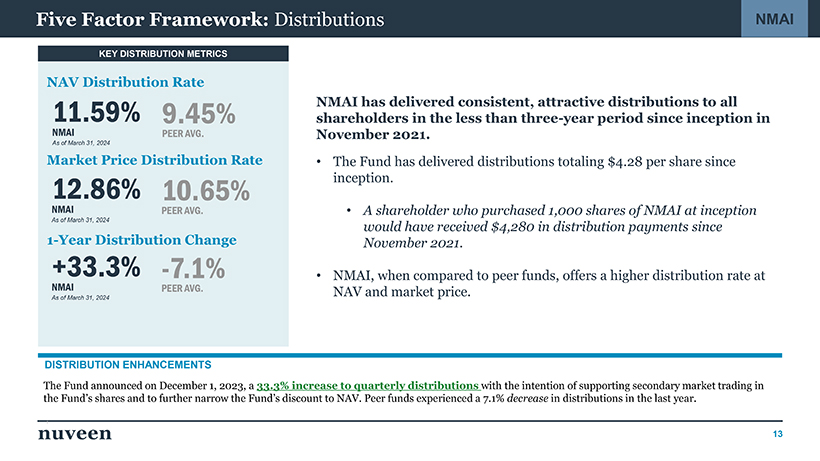

NMAI has delivered consistent, attractive distributions to all shareholders in the less than three-year period since inception in November 2021.

• The Fund has delivered distributions totaling $4.28 per share since inception.

• A shareholder who purchased 1,000 shares of NMAI at inception would have received $4,280 in distribution payments since November 2021.

• NMAI, when compared to peer funds, offers a higher distribution rate at NAV and market price.

DISTRIBUTION ENHANCEMENTS

The Fund announced on December 1, 2023, a 33.3% increase to quarterly distributions with the intention of supporting secondary market trading in the Fund’s shares and to further narrow the Fund’s discount to NAV. Peer funds experienced a 7.1% decrease in distributions in the last year.

13

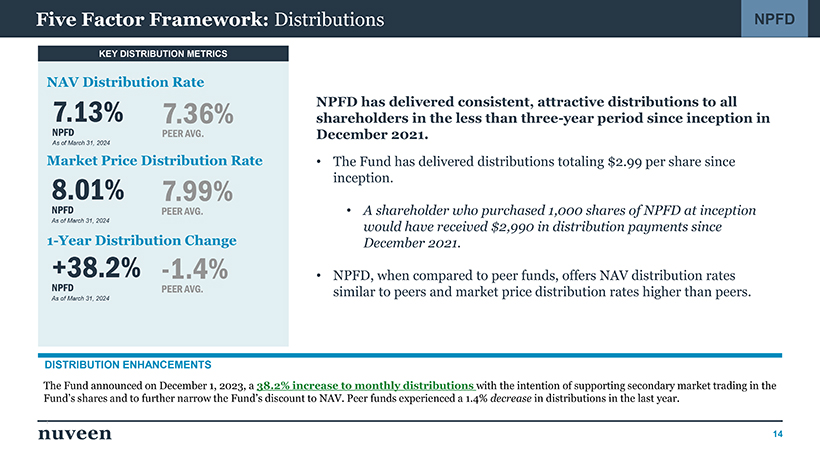

Five Factor Framework: Distributions NPFD

KEY DISTRIBUTION METRICS

NAV Distribution Rate

7.13% 7.36%

NPFD PEER AVG.

As of March 31, 2024

Market Price Distribution Rate

8. 01% 7.99%

NPFD PEER AVG.

As of March 31, 2024

1-Year Distribution Change

+38 .2% -1.4%

NPFD PEER AVG.

As of March 31, 2024

NPFD has delivered consistent, attractive distributions to all shareholders in the less than three-year period since inception in December 2021.

• The Fund has delivered distributions totaling $2.99 per share since inception.

• A shareholder who purchased 1,000 shares of NPFD at inception would have received $2,990 in distribution payments since December 2021.

• NPFD, when compared to peer funds, offers NAV distribution rates similar to peers and market price distribution rates higher than peers.

DISTRIBUTION ENHANCEMENTS

The Fund announced on December 1, 2023, a 38.2% increase to monthly distributions with the intention of supporting secondary market trading in the

Fund’s shares and to further narrow the Fund’s discount to NAV. Peer funds experienced a 1.4% decrease in distributions in the last year.

14

Five Factor Framework: Distributions NPCT

KEY DISTRIBUTION METRICS

NAV Distribution Rate

9. 15% 11.45%

NPCT PEER AVG.

As of March 31, 2024

Market Price Distribution Rate

10 .61% 10.93%

NPCT PEER AVG.

As of March 31, 2024

1-Year Distribution Change

+10 .2% +3.7%

NPCT PEER AVG.

As of March 31, 2024

NPCT has delivered consistent, attractive distributions to all shareholders in the less than three-year period since inception in April 2021.

• The Fund has delivered distributions totaling $3.35 per share since inception.

• A shareholder who purchased 1,000 shares of NPCT at inception would have received $3,350 in distribution payments since December 2021.

• NPCT, when compared to peer funds, offers comparable distribution rates at NAV and market price.

DISTRIBUTION ENHANCEMENTS

The Fund announced on December 1, 2023, a 10.2% increase to monthly distributions with the intention of supporting secondary market trading in the Fund’s shares and to further narrow the Fund’s discount to NAV. Peer funds experienced only a 3.7% increase in distributions in the last year.

15

Nuveen CEFs are designed to perform over the life of the fund by offering shareholders investment strategies and structures that are harder to access.

The Funds offer a broad

Five Factor Framework: Total Shareholder Returns Summary

• Each Fund has a distinct mandate with investment objectives and policies intended to provide shareholders access to a clear investment strategy and consistent fund structure.

• Each Fund’s portfolio and structure were challenged in

2022 with unprecedented market volatility, but Nuveen CEFs are designed to perform over the long-term and through market cycles.

• Each Fund has recovered significantly on a market price and NAV-basis along with broad market indices.

TOTAL RETURNS (as of 3/31/2024)

16

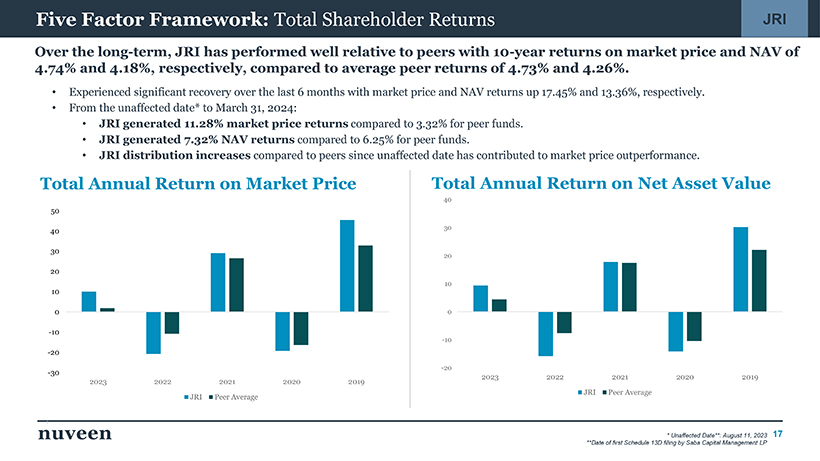

Five Factor Framework: Total Shareholder Returns JRI

Over the long-term, JRI has performed well relative to peers with 10-year returns on market price and NAV of

4.74% and 4.18%, respectively, compared to average peer returns of 4.73% and 4.26%.

• Experienced significant recovery over the last 6 months with market price and NAV returns up 17.45% and 13.36%, respectively.

• From the unaffected date* to March 31, 2024:

• JRI generated 11.28% market price returns compared to 3.32% for peer funds.

• JRI generated 7.32% NAV returns compared to 6.25% for peer funds.

• JRI distribution increases compared to peers since unaffected date has contributed to market price outperformance.

Total Annual Return on Market Price Total Annual Return on Net Asset Value

* Unaffected Date**: August 11, 2023 17 **Date of first Schedule 13D filing by Saba Capital Management LP

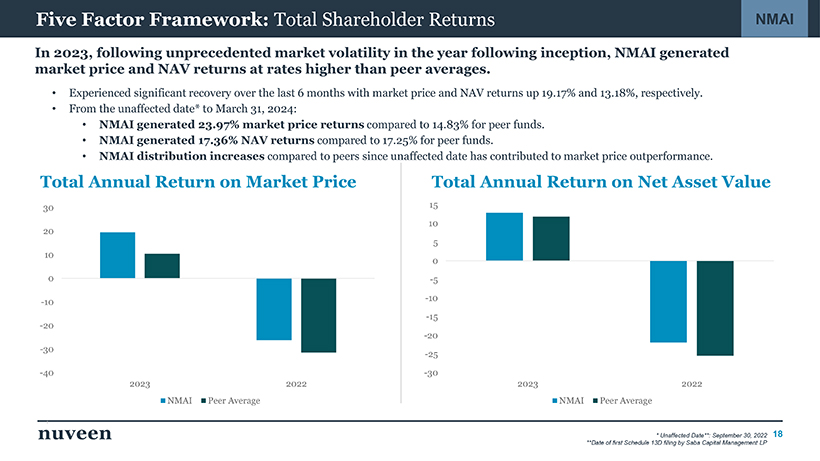

Five Factor Framework: Total Shareholder Returns NMAI

In 2023, following unprecedented market volatility in the year following inception, NMAI generated market price and NAV returns at rates higher than peer averages.

• Experienced significant recovery over the last 6 months with market price and NAV returns up 19.17% and 13.18%, respectively.

• From the unaffected date* to March 31, 2024:

• NMAI generated 23.97% market price returns compared to 14.83% for peer funds.

• NMAI generated 17.36% NAV returns compared to 17.25% for peer funds.

• NMAI distribution increases compared to peers since unaffected date has contributed to market price outperformance.

Total Annual Return on Market Price Total Annual Return on Net Asset Value

30 15 10 20 5 10 0

0 -5 -10 -10 -15 -20 -20 -30 -25

-40 -30

2023 2022 2023 2022 NMAI Peer Average NMAI Peer Average

* Unaffected Date**: September 30, 2022 18 **Date of first Schedule 13D filing by Saba Capital Management LP

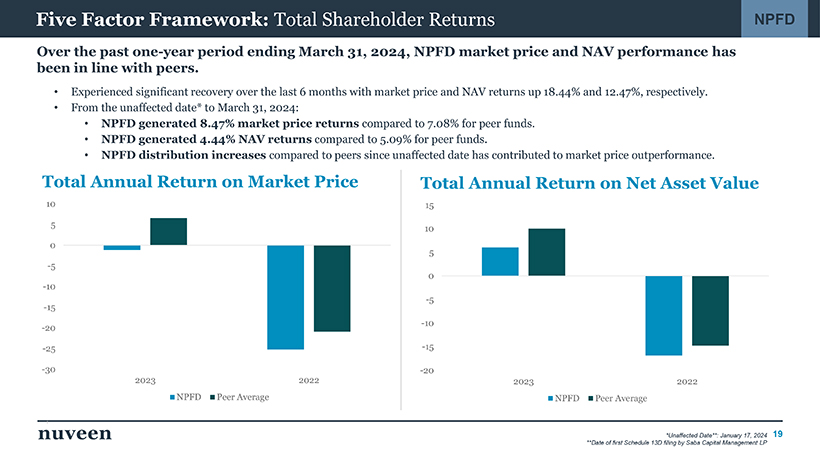

Five Factor Framework: Total Shareholder Returns NPFD

Over the past one-year period ending March 31, 2024, NPFD market price and NAV performance has been in line with peers.

• Experienced significant recovery over the last 6 months with market price and NAV returns up 18.44% and 12.47%, respectively.

• From the unaffected date* to March 31, 2024:

• NPFD generated 8.47% market price returns compared to 7.08% for peer funds.

• NPFD generated 4.44% NAV returns compared to 5.09% for peer funds.

• NPFD distribution increases compared to peers since unaffected date has contributed to market price outperformance.

Total Annual Return on Market Price Total Annual Return on Net Asset Value

10 15

5 10 0 5 -5 0 -10 -5 -15 -10 -20

-25 -15 -30 -20

2023 2022 2023 2022 NPFD Peer Average NPFD Peer Average

*Unaffected Date**: January 17, 2024 19 **Date of first Schedule 13D filing by Saba Capital Management LP

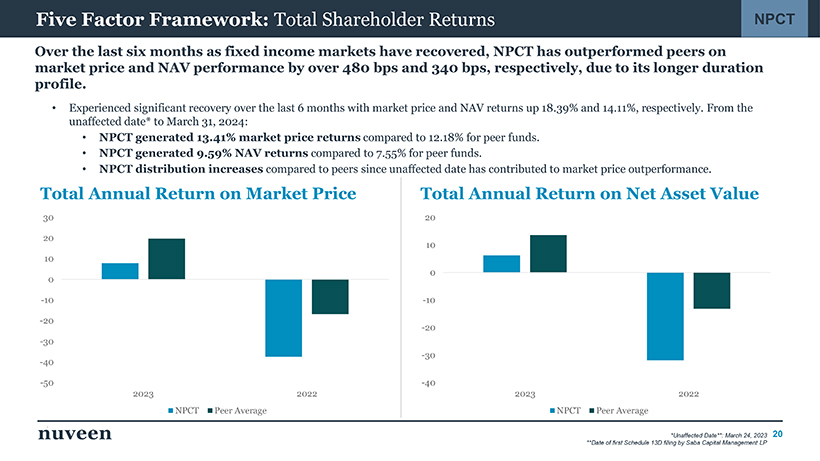

Five Factor Framework: Total Shareholder Returns NPCT

Over the last six months as fixed income markets have recovered, NPCT has outperformed peers on market price and NAV performance by over 480 bps and 340 bps, respectively, due to its longer duration profile.

• Experienced significant recovery over the last 6 months with market price and NAV returns up 18.39% and 14.11%, respectively. From the unaffected date* to March 31, 2024:

• NPCT generated 13.41% market price returns compared to 12.18% for peer funds.

• NPCT generated 9.59% NAV returns compared to 7.55% for peer funds.

• NPCT distribution increases compared to peers since unaffected date has contributed to market price outperformance.

Total Annual Return on Market Price Total Annual Return on Net Asset Value

30 20

20

10 10 0 0

-10 -10

-20

-20 -30 -30 -40

-50 -40

2023 2022 2023 2022 NPCT Peer Average NPCT Peer Average

*Unaffected Date**: March 24, 2023 20 **Date of first Schedule 13D filing by Saba Capital Management LP

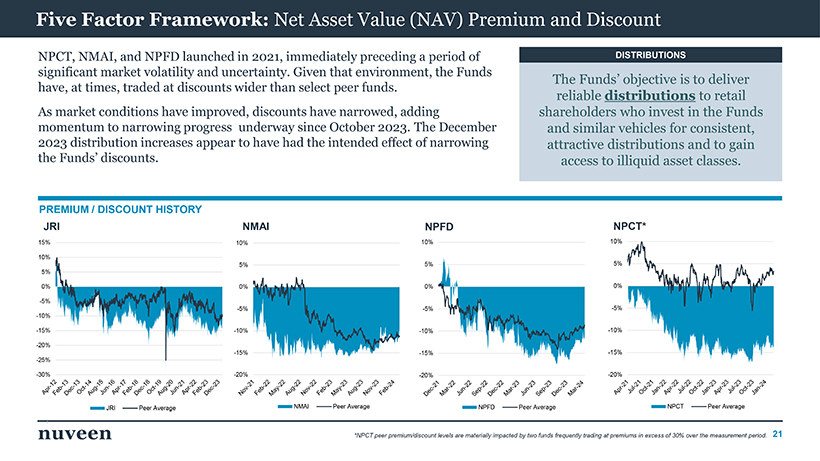

Five Factor Framework: Net Asset Value (NAV) Premium and Discount

NPCT, NMAI, and NPFD launched in 2021, immediately preceding a period of DISTRIBUTIONS significant market volatility and uncertainty. Given that environment, the Funds

The Funds’ objective is to deliver have, at times, traded at discounts wider than select peer funds. reliable distributions to retail

As market conditions have improved, discounts have narrowed, adding shareholders who invest in the Funds momentum to narrowing progress underway since October 2023. The December and similar vehicles for consistent, 2023 distribution increases appear to have had the intended effect of narrowing attractive distributions and to gain the Funds’ discounts. access to illiquid asset classes.

PREMIUM / DISCOUNT HISTORY

JRI NMAI NPFD NPCT*

15% 10% 10% 10%

10%

5% 5% 5% 5%

0% 0% 0% 0%

-5%

-5% -5% -5% -10%

-15% -10% -10% -10%

-20%

-15% -15% -15% -25%

-30% -20% -20% -20%

JRI Peer Average NMAI Peer Average NPFD Peer Average NPCT Peer Average

*NPCT peer premium/discount levels are materially impacted by two funds frequently trading at premiums in excess of 30% over the measurement period. 21

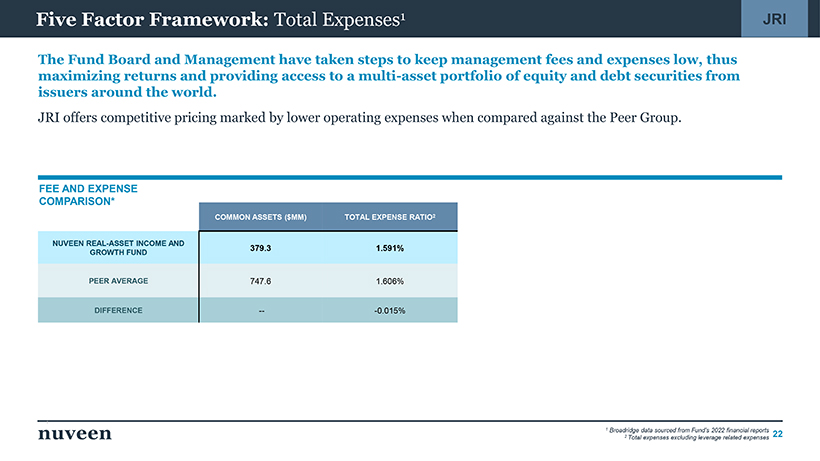

Five Factor Framework: Total Expenses1 JRI

The Fund Board and Management have taken steps to keep management fees and expenses low, thus maximizing returns and providing access to a multi-asset portfolio of equity and debt securities from issuers around the world.

JRI offers competitive pricing marked by lower operating expenses when compared against the Peer Group.

FEE AND EXPENSE COMPARISON*

COMMON ASSETS ($MM) TOTAL EXPENSE RATIO2

NUVEEN REAL-ASSET INCOME AND

379.3 1.591%

GROWTH FUND

PEER AVERAGE 747.6 1.606%

DIFFERENCE -- -0.015%

1 Broadridge data sourced from Fund’s 2022 financial reports

2 Total expenses excluding leverage related expenses 22

Five Factor Framework: Total Expenses1 NMAI

The Fund Board and Management have taken steps to keep management fees and expenses low, thus maximizing returns and providing access to a multi-asset portfolio of equity and debt securities from issuers around the world.

NMAI offers competitive pricing marked by lower operating expenses when compared against the Peer Group.

FEE AND EXPENSE COMPARISON*

COMMON ASSETS ($MM) TOTAL EXPENSE RATIO2

NUVEEN MULTI-ASSET INCOME FUND 459.7 1.493%

PEER AVERAGE 281.1 1.831%

DIFFERENCE -- -0.338%

1 Broadridge data sourced from Fund’s 2022 financial reports

2 Total expenses excluding leverage related expenses 23

Five Factor Framework: Total Expenses1 NPFD

The Fund Board and Management have taken steps to keep management fees and expenses low, thus maximizing returns and providing access to a multi-asset portfolio of equity and debt securities from issuers around the world.

NPFD offers competitive pricing marked by comparable operating expenses when compared against the Peer Group.

FEE AND EXPENSE COMPARISON*

COMMON ASSETS ($MM) TOTAL EXPENSE RATIO2

NUVEEN VARIABLE RATE PREFERRED

441.9 1.393%

AND INCOME FUND

PEER AVERAGE 537.0 1.377%

DIFFERENCE -- 0.016%

1 Broadridge data sourced from Fund’s 2022 financial reports

2 Total expenses excluding leverage related expenses 24

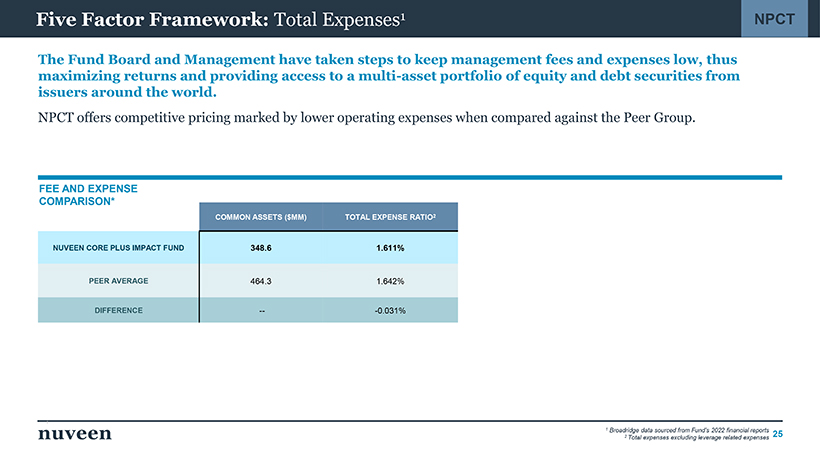

Five Factor Framework: Total Expenses1 NPCT

The Fund Board and Management have taken steps to keep management fees and expenses low, thus maximizing returns and providing access to a multi-asset portfolio of equity and debt securities from issuers around the world.

NPCT offers competitive pricing marked by lower operating expenses when compared against the Peer Group.

FEE AND EXPENSE COMPARISON*

COMMON ASSETS ($MM) TOTAL EXPENSE RATIO2

NUVEEN CORE PLUS IMPACT FUND 348.6 1.611%

PEER AVERAGE 464.3 1.642%

DIFFERENCE -- -0.031%

1 Broadridge data sourced from Fund’s 2022 financial reports

2 Total expenses excluding leverage related expenses 25

Five Factor Framework: Corporate Governance

Experienced, Successful Discount- Impactful Consistently Qualified Narrowing Distribution competitive total Independent Trustees Initiatives Enhancements expenses

• Deep closed-end fund • Distribution and fee-focused • Attractive, consistent • Competitive, and often lower, expertise and relevant career programs have resulted in distributions through managed fees compared to peer averages meaningful discount programs convert long-term maximize returns by keeping experiences narrowing following period return potential into regular total expenses comparatively

• Track record of stewardship of unprecedented market- income, giving shareholders reduced advancing shareholders’ best wide turbulence the CEF benefits they invest for

• JRI, NMAI, NPFD offer interests lower total expense ratios

• NMAI and NPFD

• NMAI trades at a increased distributions when compared to

• Highly engaged individuals discount narrower than in Dec. 2023 by 33.3% respective peer averages 3 with a demonstrated history of peer group averages and 38.2% respectively, taking thoughtful governance and indices as of Jan.

1 far more than peers in actions 2024 2 the same period

1 See p. 19

2 See p. 12, 13 26

2 See p. 20, 21, 23

The Board believes its Nominees should continue to serve shareholders of JRI, NMAI, NPFD, and NPCT as Trustees, representing all shareholders in the pursuit of long-term value from their investment in the Funds.

The Board Nominees possess the qualifications, skills, and experience in overseeing closed-end funds and will continue to act in the best interests of all shareholders.

The dissident nominee has no relevant or beneficial qualifications or skills and lacks any relevant experience to complement the existing board or benefit the decision-making Is change capacities of the Board, as a whole. warranted? No. ? The diverse slate of Board Nominees are all accomplished professionals in their respective fields and bring a wide range of experience to the Fund Board, each with direct closed-end fund and mutual fund experience.

Members of the Board’s Nominating and Governance Committee interviewed Saba’s nominee, Mr. Chen, and determined that the current Trustees up for election possess more direct and relevant experience and would better serve all Fund shareholders.

27

NUVEEN REAL ASSET INCOME AND GROWTH FUND (JRI) NUVEEN MULTI-ASSET INCOME FUND (NMAI)

Independent Trustees for Election

Independent Trustees for Election

The Nominees for each Fund are independent and highly experienced, focused on delivering long-term value to all shareholders. The diverse group of Nuveen Nominees possess a broad range of leadership and board experience.

Formerly, Managing Director, Government Relations and Public Policy (2009-2020) and Senior Advisor to the Vice Chairman (2018-2020), BlackRock, Inc. (global investment management firm); formerly, Managing Director, Global Head of Government Relations and Public Policy, Barclays Group (IBIM) (investment banking, investment management and wealth management businesses)(2006-2009); formerly, Managing Director, Global General Counsel and Corporate Secretary, Barclays Global Investors (global investment management firm) (1996-2006); formerly, Partner, Orrick, Herrington & Sutcliffe LLP (law firm) (1993-1995); formerly, General Counsel, Commodity Futures Trading Commission (government agency overseeing U.S. derivatives markets) (1989-1993); formerly, Deputy Associate Director/Associate Director for Legal and Financial Affairs, Office of Presidential Personnel, The White House (1986-1989); Member of the Board of Directors, Baltic-American Freedom JOANNE T. Foundation (seeks to provide opportunities for citizens of the Baltic states to gain education and professional development through exchanges in the U.S.) (since 2019).

MEDERO

Independent Trustee since 2021

Independent Consultant/Advisor (since 2021); formerly, Vice Chair, Senior Managing Director (2020–2021), Chief Financial Officer, Senior Managing Director (2005–2020), Invesco Ltd.; Director (since 2023) and Audit Committee member (since 2024), AMG; formerly, Chair and Member of the Board of Directors (2014–2021), Georgia Leadership Institute for School Improvement (GLISI); formerly, Chair and Member of the Board of Trustees (2014–2018), Georgia Council on Economic Education (GCEE); Trustee, the College Retirement Equities Fund and Manager, TIAA Separate Account VA-1 (2022–2023).

LOREN M. STARR

Independent Trustee since 2024

29

Independent Trustees for Election

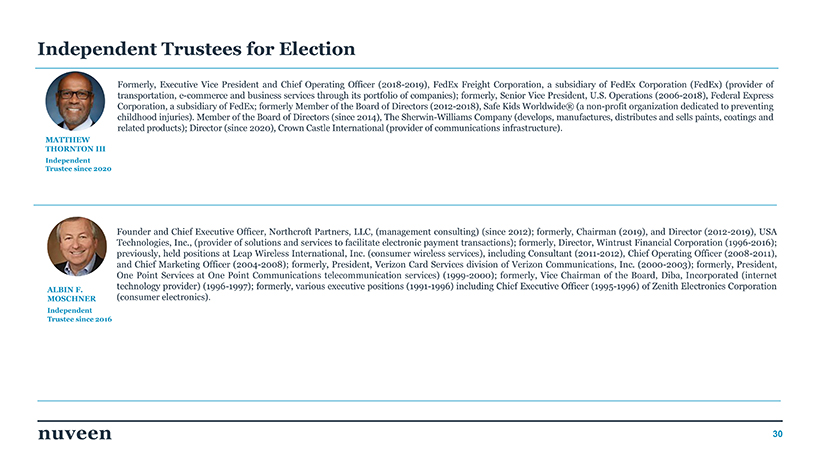

Formerly, Executive Vice President and Chief Operating Officer (2018-2019), FedEx Freight Corporation, a subsidiary of FedEx Corporation (FedEx) (provider of transportation, e-commerce and business services through its portfolio of companies); formerly, Senior Vice President, U.S. Operations (2006-2018), Federal Express Corporation, a subsidiary of FedEx; formerly Member of the Board of Directors (2012-2018), Safe Kids Worldwide® (a non-profit organization dedicated to preventing childhood injuries). Member of the Board of Directors (since 2014), The Sherwin-Williams Company (develops, manufactures, distributes and sells paints, coatings and related products); Director (since 2020), Crown Castle International (provider of communications infrastructure).

MATTHEW THORNTON III

Independent Trustee since 2020

Founder and Chief Executive Officer, Northcroft Partners, LLC, (management consulting) (since 2012); formerly, Chairman (2019), and Director (2012-2019), USA Technologies, Inc., (provider of solutions and services to facilitate electronic payment transactions); formerly, Director, Wintrust Financial Corporation (1996-2016); previously, held positions at Leap Wireless International, Inc. (consumer wireless services), including Consultant (2011-2012), Chief Operating Officer (2008-2011), and Chief Marketing Officer (2004-2008); formerly, President, Verizon Card Services division of Verizon Communications, Inc. (2000-2003); formerly, President, One Point Services at One Point Communications telecommunication services) (1999-2000); formerly, Vice Chairman of the Board, Diba, Incorporated (internet ALBIN F. technology provider) (1996-1997); formerly, various executive positions (1991-1996) including Chief Executive Officer (1995-1996) of Zenith Electronics Corporation MOSCHNER (consumer electronics).

Independent Trustee since 2016

30

NUVEEN CORE PLUS IMPACT FUND (NPCT)

NUVEEN VARIABLE RATE PREFERRED AND INCOME FUND (NPFD)

Independent Trustees for Election

31

Independent Trustees for Election

The Nominees for each Fund are independent and highly experienced, focused on delivering long-term value to all shareholders. The diverse group of Nuveen Nominees possess a broad range of leadership and board experience.

Formerly, Managing Director, Government Relations and Public Policy (2009-2020) and Senior Advisor to the Vice Chairman (2018-2020), BlackRock, Inc. (global investment management firm); formerly, Managing Director, Global Head of Government Relations and Public Policy, Barclays Group (IBIM) (investment banking, investment management and wealth management businesses)(2006-2009); formerly, Managing Director, Global General Counsel and Corporate Secretary, Barclays Global Investors (global investment management firm) (1996-2006); formerly, Partner, Orrick, Herrington & Sutcliffe LLP (law firm) (1993-1995); formerly, General Counsel, Commodity Futures Trading Commission (government agency overseeing U.S. derivatives markets) (1989-1993); formerly, Deputy Associate Director/Associate Director for Legal and Financial Affairs, Office of Presidential Personnel, The White House (1986-1989); Member of the Board of Directors, Baltic-American Freedom JOANNE T. Foundation (seeks to provide opportunities for citizens of the Baltic states to gain education and professional development through exchanges in the U.S.) (since 2019).

MEDERO

Independent Trustee since 2021

Independent Consultant/Advisor (since 2021); formerly, Vice Chair, Senior Managing Director (2020–2021), Chief Financial Officer, Senior Managing Director (2005–2020), Invesco Ltd.; Director (since 2023) and Audit Committee member (since 2024), AMG; formerly, Chair and Member of the Board of Directors (2014–2021), Georgia Leadership Institute for School Improvement (GLISI); formerly, Chair and Member of the Board of Trustees (2014–2018), Georgia Council on Economic Education (GCEE); Trustee, the College Retirement Equities Fund and Manager, TIAA Separate Account VA-1 (2022–2023).

LOREN M. STARR

Independent Trustee since 2024

32

Independent Trustees for Election

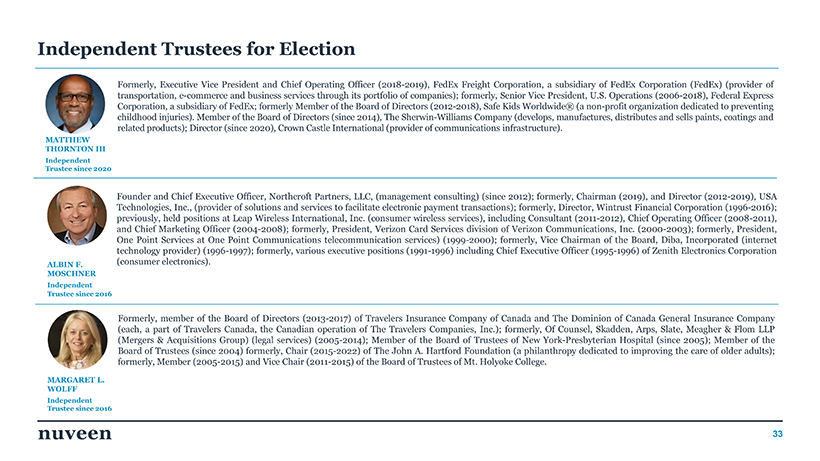

Formerly, Executive Vice President and Chief Operating Officer (2018-2019), FedEx Freight Corporation, a subsidiary of FedEx Corporation (FedEx) (provider of transportation, e-commerce and business services through its portfolio of companies); formerly, Senior Vice President, U.S. Operations (2006-2018), Federal Express Corporation, a subsidiary of FedEx; formerly Member of the Board of Directors (2012-2018), Safe Kids Worldwide® (a non-profit organization dedicated to preventing childhood injuries). Member of the Board of Directors (since 2014), The Sherwin-Williams Company (develops, manufactures, distributes and sells paints, coatings and related products); Director (since 2020), Crown Castle International (provider of communications infrastructure).

MATTHEW THORNTON III

Independent Trustee since 2020

Founder and Chief Executive Officer, Northcroft Partners, LLC, (management consulting) (since 2012); formerly, Chairman (2019), and Director (2012-2019), USA Technologies, Inc., (provider of solutions and services to facilitate electronic payment transactions); formerly, Director, Wintrust Financial Corporation (1996-2016); previously, held positions at Leap Wireless International, Inc. (consumer wireless services), including Consultant (2011-2012), Chief Operating Officer (2008-2011), and Chief Marketing Officer (2004-2008); formerly, President, Verizon Card Services division of Verizon Communications, Inc. (2000-2003); formerly, President, One Point Services at One Point Communications telecommunication services) (1999-2000); formerly, Vice Chairman of the Board, Diba, Incorporated (internet technology provider) (1996-1997); formerly, various executive positions (1991-1996) including Chief Executive Officer (1995-1996) of Zenith Electronics Corporation ALBIN F. (consumer electronics).

MOSCHNER

Independent Trustee since 2016

Formerly, member of the Board of Directors (2013-2017) of Travelers Insurance Company of Canada and The Dominion of Canada General Insurance Company (each, a part of Travelers Canada, the Canadian operation of The Travelers Companies, Inc.); formerly, Of Counsel, Skadden, Arps, Slate, Meagher & Flom LLP (Mergers & Acquisitions Group) (legal services) (2005-2014); Member of the Board of Trustees of New York-Presbyterian Hospital (since 2005); Member of the Board of Trustees (since 2004) formerly, Chair (2015-2022) of The John A. Hartford Foundation (a philanthropy dedicated to improving the care of older adults); formerly, Member (2005-2015) and Vice Chair (2011-2015) of the Board of Trustees of Mt. Holyoke College.

MARGARET L. WOLFF

Independent Trustee since 2016

33

Appendix

34

Nuveen’s corporate governance across its CEFs is designed to protect and advance the best interests of all fund shareholders.

Optimized Board Structure for CEFs

Nuveen’s Board of Directors carefully and thoughtfully determined that a classified board structure best serves fund shareholders, as it confers the following benefits:

• Promotes stability since Trustees with deep CEF experience serve at all times

• Protects against abrupt Fund management or structural changes based on short-term profit motives that may harm long term shareholders

• Over 90% of CEFs have similar classified board structures

Board Refreshment

• Nominating and Governance Committee that employs a rigorous search process with an independent nationally recognized search firm to identify and recommend qualified candidates for Board positions

• Qualifications, experience and diversity of trustee candidates are key factors in the process

• Six new independent trustees added over the last four years

Majority Vote Standard in Contested Election

• Adopted after a long and thoughtful review process with advice of outside legal experts

• Ensures that a significant number of shareholder voices are heard

• Similar standard adopted by a number of CEF complexes

• Distinct structure of CEFs provides important benefits to shareholders but leaves such funds vulnerable to opportunistic traders seeking short-term gains at the expense of long-term shareholders

• Short-term actions can destroy significant shareholder value, result in adverse tax consequences and impose substantial costs on long-term shareholders

Removal of Control Share By-Law

• The Board suspended the control share by-law in February 2022 and formally removed the by-law provision in February 2024.

• In adopting the control share by-law, the Board acted in a manner consistent with the SEC Staff’s withdrawal of the Boulder Letter.

• Although in later litigation the control share by-law was determined to violate the 40 Act, the Board was neither accused of nor found guilty of any wrongdoing or any breach of fiduciary duty in adopting the by-law provision.

35

We view closed-end funds differently than operating companies, because they function differently than operating companies.

NUVEEN PROXY VOTING GUIDELINES

On Closed-End Funds:

We recognize that many exchange-listed closed-end funds (“CEFs”) have adopted particular corporate governance practices that deviate from certain policies set forth in the Guidelines. We believe that the distinctive structure of CEFs can provide important benefits to investors but leaves CEFs uniquely vulnerable to opportunistic traders seeking short-term gains at the expense of long-term shareholders.

Thus, to protect the interests of their long-term shareholders, many CEFs have adopted measures to defend against attacks from short-term oriented activist investors. As such, in light of the unique nature of CEFs and their differences in corporate governance practices from operating companies, we will consider on a case-by-case basis proposals involving the adoption of defensive measures by CEFs. This is consistent with our approach to proxy voting that recognizes the importance of case-by-case analysis to ensure alignment with investment team views and voting in accordance with the best interest of our shareholders.

VIEW FULL PROXY VOTING GUIDELINES*

*Updated as of December 18, 2023 36

Peer groups

Ticker Fund Name

JRI Nuveen Real Asset Income and Growth Fund

TEAF Ecofin Sustainable and Social Impact Term Fund

MEGI MainStay CBRE Global Infrastructure Megatrends Term Fund ASGI abrdn Global Infrastructure Income Fund ERH Allspring Utilities & High Income Fund RA Brookfield Real Assets Income Fund DNP DNP Select Income Fund PGZ Principal Real Estate Income Fund TPZ Tortoise Power & Energy Infrastructure Fund

Ticker Fund Name

NPFD Nuveen Variable Rate Preferred & Income Fund

BXSY Bexil Investment Ord

CPZ Calamos L/S Equity & Dynamic Inc Trust CSQ Calamos Strategic Total Return

DFP Flaherty & Crumrine Dynamic Preferred & Income Fund DMA Destra Multi-Alternative FFC Flaherty & Crumrine Preferred Securities Income Fund FLC Flaherty & Crumrine Total Return Fund FPF First Trust Intermediate Duration Preferred & Income Fund GUG Guggenheim Active Allocation Fund HPI John Hancock Preferred Income Fund HPF John Hancock Preferred Income Fund II

HPS John Hancock Preferred Income Fund III JPC Nuveen Pref & Income Opportunities Fund JPI Nuveen Preferred & Income Term Fund

LDP Cohen & Steers Limited Duration Preferred & Income Fund OPP RiverNorth/DoubleLine Strategic Opp Fund PDT John Hancock Premium Dividend Fund

PFD Flaherty & Crumrine Preferred and Income Fund

PFO Flaherty & Crumrine Preferred and Income Opportunity Fund PSF Cohen & Steers Select Preferred & Income Fund

PTA Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund RIV RiverNorth Opportunities SCD LMP Capital & Income TSI TCW Strategic Income

Ticker Fund Name

NMAI Nuveen Multi-Asset Income Fund

CGO Calamos Global Total Return Fund CHW Calamos Global Dynamic Income Fund GLO Clough Global Opportunities Fund GLV Clough Global Dividend and Income Fund

ZTR Virtus Total Return Fund

GUG Guggenheim Active Allocation Fund

PGP PIMCO Global StocksPLUS & Income Fund

Ticker Fund Name

NPCT Nuveen Core Plus Impact Fund

AIF Apollo Tactical Income

ARDC Ares Dynamic Credit Allocation Fund MCI Barings Corporate Investors BIT BlackRock Multi-Sector Income DBL Doubleline Opportunistic Credit GOF Guggenheim Strategic Opp Fund KIO KKR Income Opportunities PCM PCM Fund PHK PIMCO High Income PFL PIMCO Income Strategy Fund PFN PIMCO Income Strategy Fund II

37

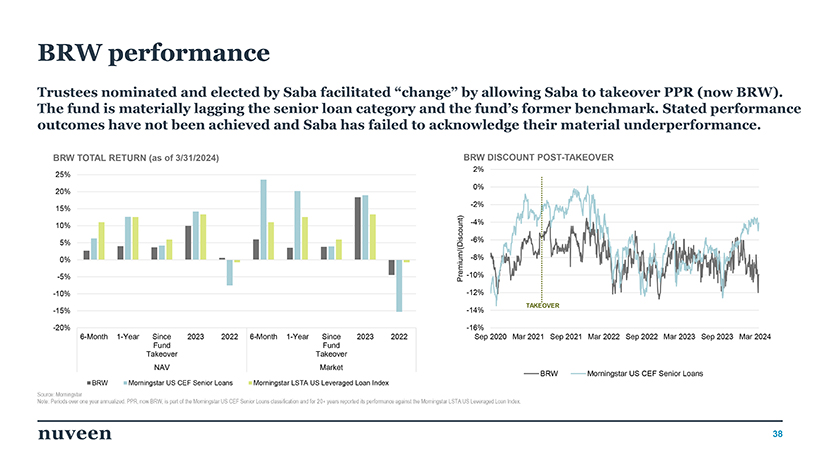

BRW performance

Trustees nominated and elected by Saba facilitated “change” by allowing Saba to takeover PPR (now BRW). The fund is materially lagging the senior loan category and the fund’s former benchmark. Stated performance outcomes have not been achieved and Saba has failed to acknowledge their material underperformance.

BRW TOTAL RETURN (as of 3/31/2024) BRW DISCOUNT POST-TAKEOVER

2%

25%

0%

20%

-2%

15%

-4%

10%

5% -6%

0% -8%

-5% Premium/(Discount) -10%

-10% -12%

TAKEOVER

-15% -14%

-20% -16%

6-Month 1-Year Since 2023 2022 6-Month 1-Year Since 2023 2022 Sep 2020 Mar 2021 Sep 2021 Mar 2022 Sep 2022 Mar 2023 Sep 2023 Mar 2024

Fund Fund

Takeover Takeover

NAV Market

BRW Morningstar US CEF Senior Loans

BRW Morningstar US CEF Senior Loans Morningstar LSTA US Leveraged Loan Index

Source: Morningstar

Note: Periods over one year annualized. PPR, now BRW, is part of the Morningstar US CEF Senior Loans classification and for 20+ years reported its performance against the Morningstar LSTA US Leveraged Loan Index.

38