Filed by Aurous Resources

Pursuant to Rule 425 under the Securities Act of 1933

Subject Company: Rigel Resources Acquisition Corp.

Commission File No. 333-280972

Gold Producer with Industry - Leading Growth Transforming into a Multi - Asset Operation September 2024

Disclaimer 1 Information Subject to Change The information contained herein has not been finalized and is subject to change (together with oral statements made in connection therewith, this “Presentation”) . This Presentation is provided for informational purposes only and has been prepared to assist interested parties in making their own evaluation with respect to a business combination (the “Business Combination”) pursuant to that certain business combination agreement (the “Business Combination Agreement”), dated March 11 , 2024 , between, among others, Rigel Resource Acquisition Corp (“Rigel”), Aurous Resources (f/k/a RRAC Newco), Blyvoor Gold Resources Proprietary Limited (“Aurous Gold”) and Blyvoor Gold Operations Proprietary Limited (“Gauta Tailings”, together with Aurous Gold, the “Target Companies”) . Any further distribution or reproduction of this presentation, in whole or in part, or the divulgence of any of its contents, is unauthorized . By accepting the presentation, each recipient agrees to maintain the confidentiality of the information contained herein . To the fullest extent permitted by law, in no circumstances will the Target Companies, Aurous Resources or Rigel or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this presentation, its contents, its omissions, reliance on the information contained within it or on opinions communicated in relation thereto or otherwise arising in connection therewith . The information contained herein is only preliminary and indicative and does not purport to contain any information that would be required to evaluate the Target Companies, Aurous Resources and Rigel, their respective financial position, the Business Combination and/or any investment decision . In furnishing this presentation, each of the Target Companies, Aurous Resources, and Rigel expressly disclaims any obligation to update any information contained herein or to correct any omissions, inaccuracies or errors . In addition, this presentation does not purport to be all - inclusive or to contain all of the information that may be required to make a full analysis of the Target Companies, Aurous Resources, Rigel or the Business Combination, and none of Target Companies, Aurous Resources, Rigel or their respective affiliates or representatives makes any representation or warranty, express or implied, as to the accuracy, completeness or reliability of the information contained in this presentation, and the recipient disclaims any such representation or warranty . Viewers of this presentation should each make their own evaluation of the Target Companies, Aurous Resources and Rigel and of the relevance and adequacy of the information and should make such other investigations as they deem necessary . By reviewing or reading this Presentation, you will be deemed to have agreed to the obligations and restrictions set out below . No Offer or Solicitation This presentation does not constitute a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Business Combination, and any such solicitation will be conducted only pursuant to a proxy statement or Registration Statement (as defined below) filed by the Target Companies, Aurous Resources, Rigel and/or their respective affiliates with the U . S . Securities and Exchange Commission (the “SEC”), as required by law . In addition, this presentation does not constitute an offer to sell, a solicitation of an offer to buy, or a recommendation to purchase any security of the Target Companies, Aurous Resources, Rigel or any of their respective affiliates, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction . Any offer of securities, if made, may be made only through definitive offering documents, including, but not limited to a subscription agreement . The information contained herein is qualified in its entirety by reference to the definitive offering documents . You should not construe the contents of this presentation as legal, tax, accounting or investment advice or a recommendation . You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, and, by accepting this presentation, you confirm that you are not relying upon the information contained herein to make any decision . This presentation is not a prospectus and investors should not subscribe for or purchase any securities solely on the basis of this presentation and before you invest you should undertake your own diligence regarding the Target Companies, Aurous Resources, Rigel and the Business Combination. The securities to be offered in the private placement to which this presentation relates have not been registered under the Securities Act of 1933 , as amended (the “Securities Act”) or applicable state or foreign securities laws . The securities may not be offered or sold in the United States absent a registration statement or an applicable exemption from the registration requirements of the Securities Act . It is currently expected that the securities of Aurous Resources will be offered and sold in reliance on the exemption from the registration requirements provided by Section 4 (a)( 2 ) of the Securities Act . The securities of Aurous Resources have not been approved or disapproved by the Securities and Exchange Commission, any state securities commission or other United States or foreign regulatory authority . This presentation does not constitute or form part of and should not be construed as any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares, nor shall any part of it nor the fact of its distribution form part of or be relied on in connection with any contract or investment decision relating thereto, nor does it constitute a recommendation regarding the securities . This presentation is supplied to you solely for your information . Nothing contained in the presentation, nor the fact of its distribution, shall form the basis of any contract or commitment whatsoever . In particular, in South Africa, this presentation is only for distribution to persons (i) falling within the exemptions set out in section 96 ( 1 )(a) or (b) of the South African Companies Act No . 71 of 2008 (as amended) (the “South African Companies Act”) or (ii) who are persons who subscribe, as principal, for the shares at a minimum placing price of R 1 , 000 , 000 (one million Rand), as envisaged in section 96 ( 1 )(b) of the South African Companies Act and to whom this presentation will be specifically addressed (the “South African Qualifying Investors”) . As such, in South Africa, this Presentation does not constitute an offer for the sale of or subscription for, or the solicitation of an offer to buy and/or to subscribe for the shares to the public as defined in the South African Companies Act and will not be distributed to any person in South Africa in any manner which could be construed as an offer to the public in terms of the South African Companies Act . Should any person in South Africa who is not a South African Qualifying Investor receive this presentation, they should not and will not be entitled to acquire any shares or otherwise act thereon . This presentation does not, nor is it intended to, constitute a prospectus prepared and registered under the South African Companies Act . Accordingly, this presentation does not comply with the substance and form requirements for prospectuses set out in the South African Companies Act and the South African Companies Act Regulations of 2011 (as amended) and has not been approved by, and/or registered with, the South African Companies and Intellectual Property Commission, or any other South African authority . Any offer or sale of the any securities shall be subject to compliance with South African exchange control regulations as may be applicable to the relevant South African Qualifying Investors . The information contained in this presentation constitutes factual information as contemplated in section 1 ( 3 )(a) of the South African Financial Advisory and Intermediary Services Act No . 37 of 2002 (as amended) (the “FAIS Act”) and does not constitute the furnishing of, any “advice” as defined in section 1 ( 1 ) of the FAIS Act . The presenters and their respective entities which they represent are not Financial Services Providers (as defined in the FAIS Act) and are neither licensed nor registered as such under the FAIS Act . The information contained in this presentation should not be construed as an express or implied recommendation, guidance or proposal that any particular transaction is appropriate to the particular investment objectives, financial situations or needs of a prospective investor, and nothing in this presentation should be construed as constituting the canvassing for, or marketing or advertising of, financial services in South Africa . If you require financial and/or investment advice, please engage the services of an independent financial adviser . Forward - Looking Statements This presentation contains “forward - looking statements, terms and expressions” within the meaning of the securities laws of certain jurisdictions, including U . S . securities laws . Forward - looking statements include statements about the Target Companies’, Aurous Resources’ and Rigel’s future business prospects, revenues and income, information relating to new or ongoing development projects, all - in - sustaining costs, all - in costs, expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts . In some cases, these forward - looking statements can be identified by the use of forward - looking terminology . Additionally, forward - looking statements include, without limitation, any estimates, forecasts, forward - looking information derived from reports prepared or obtained by the Target Companies, including by market researchers, market respondents, independent professional organizations and other external sources from compiling data, market sampling, and/or exercising subjective judgments that may be cited in this presentation . Words or phrases such as “aim,” “anticipate,” “believe,” “continue,” “can,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “objective,” “ongoing,” “plan,” “potential,” “predict,” “project,” “target,” “seek,” “pursue,” “shall,” “should,” “will” and “would,” or similar words or phrases, or, in each case, their negative or other variations or comparable terminology or by the discussions of strategies, plans, objectives, targets, goals, future events or intentions, may identify forward - looking statements, but these are not the exclusive means of identifying forward - looking statements and the absence of these words and phrases does not necessarily mean that a statement is not forward - looking . These forward - looking statements are based upon estimates and assumptions that, while considered reasonable by Rigel and its management, Aurous and its management, and the Target Companies and their management, as the case may be, are inherently uncertain . Such forward - looking statements involve known and unknown risks, uncertainties and other important factors that could cause actual results to be materially different from future results, performance or achievements expressed or implied by such forward - looking statements . Factors that may cause actual results to differ materially from current expectations include, but are not limited to : ( 1 ) the occurrence of any event, change or other circumstances that could give rise to the termination of the Business Combination ; ( 2 ) the outcome of any legal proceedings that may be instituted against Rigel, Aurous Resources, the Target Companies or others following the announcement of the Business Combination and any definitive agreements with respect thereto ; ( 3 ) the inability to complete the Business Combination due to the failure to obtain approval of the shareholders of Rigel, Aurous Resources, or the Target Companies, to obtain financing to complete the Business Combination or to satisfy other conditions to closing under the Business Combination Agreement ; ( 4 ) changes to the proposed structure of the Business Combination that may be required or appropriate as a result of applicable laws or regulations or as a condition to obtaining regulatory approval of the Business Combination ; ( 5 ) the ability to meet the listing standards of the New York Stock Exchange or NASDAQ following the consummation of the Business Combination ; ( 6 ) the risk that the Business Combination disrupts current plans and operations of the Target Companies as a result of the announcement and consummation of the Business Combination ; ( 7 ) the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the Target Companies to grow and manage growth profitably, maintain relationships with customers and suppliers and retain their management and key employees ; ( 8 ) transaction costs related to the Business Combination ; ( 9 ) changes in applicable laws or regulations ; ( 10 ) the possibility that the Target Companies may be adversely affected by other economic, business and/or competitive factors ; ( 11 ) the Target Companies’ estimates of their financial performance ; ( 12 ) the possibility that the assumptions and estimates used in the S - K 1300 Technical Reports may be different than the actual results ; and ( 13 ) other risks and uncertainties set forth in the sections entitled “Risk Factors” in the Registration Statement and the section entitled “Risk Factors” in Rigel’s Annual Report on Form 10 - K for the fiscal year ended December 31 , 2023 . In addition, forward - looking statements reflect the Target Companies’, Aurous Resources’ or Rigel’s expectations, plans or forecasts of future events and views as of the date of this presentation . The Target Companies, Aurous Resources and Rigel anticipate that subsequent events and developments will cause these assessments to change . However, while the Target Companies and/or Rigel and/or Aurous Resources may elect to update these forward - looking statements at some point in the future, each of the Target Companies, Aurous Resources, and Rigel specifically disclaim any obligation to do so . These forward - looking statements should not be relied upon as representing the Target Companies’, Aurous Resources’, nor Rigel’s assessments as of any date subsequent to the date of this presentation .

Disclaimer (Cont’d) 2 Nothing in this presentation should be regarded as a representation by any person that the forward - looking statements set forth herein will be achieved or that any of the contemplated results of such forward - looking statements will be achieved . You should not place undue reliance on forward - looking statements, which speak only as of the date they are made . Neither the Target Companies, Aurous Resources nor Rigel undertake any duty to update these forward - looking statements, whether as a result of new information, future events or otherwise unless required to do so by applicable law or regulation . Use of Projections This presentation contains projected financial information with respect to the Target Companies, based on the S - K 1300 technical reports, or Rigel . Such projected financial information constitutes forward - looking information, and is for illustrative purposes only and should not be relied upon as necessarily being indicative of future results . The Target Companies’ independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, they did not express an opinion or provide any other form of assurance with respect thereto for the purpose of this presentation . The assumptions and estimates underlying such financial forecast information are inherently uncertain and are subject to a wide variety of significant business, economic, competitive and other risks and uncertainties . Actual results may differ materially from the results contemplated by the financial forecast information contained in this presentation, and the inclusion of such information in this presentation is not intended, and should not be regarded, as a representation by any person that the results reflected in such forecasts will be achieved . See “Forward - Looking Statements” above . Historical Financial Information; Non - GAAP or non - IFRS Financial Measures This presentation includes certain historical and forecasted non - GAAP and non - IFRS financial measures, including, among others, EBITDA, direct cash costs, all - in sustaining costs (“AISC”) and free cash flow or unlevered free cash flow . Rigel, Aurous Resources, and the Target Companies believe that these non - GAAP and non - IFRS measures provide useful information to management and investors regarding certain financial and business trends relating to Rigel, Aurous Resources, and the Target Companies’ financial condition and results of operations . These non - GAAP or non - IFRS financial measures are subject to inherent limitations as they reflect the exercise of judgments by management about which expense and income are excluded or included in determining these non - GAAP or non - IFRS financial measures . Rigel’s, Aurous Resources’, and Target Companies’ management do not consider these non - GAAP and non - IFRS measures in isolation or as an alternative to financial measures determined in accordance with GAAP or IFRS . Other companies may calculate non - GAAP and non - IFRS measures differently, and therefore the non - GAAP and non - IFRS measures of Aurous Resources or the Target Companies included in this presentation may not be directly comparable to similarly titled measures of other companies . Rigel, Aurous Resources, and the Target Companies are unable to quantify certain amounts that would be required to be included in the most directly comparable GAAP or IFRS financial measures without unreasonable effort . Consequently, no disclosure of estimated comparable GAAP or IFRS measures is included and no reconciliation of forward - looking non - GAAP or non - IFRS financial measures is included . Certain monetary amounts, percentages and other figures included in this presentation have been subject to rounding adjustments . Certain other amounts that appear in this presentation may not sum due to rounding . Cautionary Note Regarding Mineral Resources and Reserves Estimates of “measured”, “indicated” and “inferred” mineral resources as well as “proven” and “probable” mineral reserves shown in this presentation with regard to the properties of the Target Companies are defined in Subpart 1300 of Regulation S - K promulgated by the SEC (“S - K 1300 ”) . The estimation of measured resources and indicated resources involves greater uncertainty as to their existence and economic feasibility than the estimation of proven and probable mineral reserves . The estimation of inferred resources involves far greater uncertainty as to their existence and economic viability than the estimation of other categories of resources . Investors are cautioned not to assume that any or all of the mineral resources are economically or legally mineable or that these mineral resources will ever be converted into mineral reserves . In this Presentation, mineral resources are often reported as inclusive of mineral reserves, identified as such or with phrases such as “contained . ” You are cautioned that mineral resources do not have demonstrated economic viability . Industry and Market Data; Trademarks and Trade Names Industry and market data used in this presentation have been obtained from third - party industry publications and sources as well as from research reports prepared for other purposes. Neither the Target Companies, Aurous Resources, nor Rigel have independently verified the data obtained from these sources and cannot assure you of the data’s accuracy or completeness. This data is subject to change. This presentation contains trademarks, service marks, trade names and copyrights of Rigel, Aurous Resources, the Target Companies and other companies which are the property of their respective owners. Rigel has commissioned AME Mineral Economics Pty Ltd (AME) to provide certain information for inclusion in this document . Information provided by AME is referred to in this document as ‘AME’ . This document uses market data, statistics and third - party estimates, projections and forecasts relating to the industries, segments and end markets in which Rigel and the Target Companies operate . Such information includes, but is not limited to statements, statistics and data relating to product segment and market share, estimated historical and forecast market growth, market sizes and trends, and Rigel and the Target Companies’ estimated market share and its industry position . Rigel and the Target Companies have obtained significant portions of the market data, statistics and other information from databases and research prepared by third parties, including reports and information prepared by the AME and other third parties, and other sources . AME has advised that (i) information in their databases is derived from their estimates, subjective judgements, and third - party sources, (ii) the information in the databases of other coal industry data collection agencies will differ from the information in their databases, and (iii) that forecast information is highly speculative and no reliance may be placed on this data . In the compilation of the AME statistical and graphical information will be unreliable, inaccurate and will contain errors of fact and judgement . It is subject to full validation and the provision of such information requires investors to make appropriate further enquiries . Investors should note that market data and statistics are inherently predictive, subject to uncertainty and not necessarily reflective of actual market conditions . There is no assurance that any of the third - party estimates or projections contained in this information, including information provided by AME, will be achieved . Rigel and the Target Companies have not independently verified and cannot give any assurances to the accuracy or completeness of, these market and third - party estimates and projections . Estimates involve risks and uncertainties and are subject to change based on various known and unknown risks, uncertainties, and other factors . The data and information provided by Wood Mackenzie should not be interpreted as advice and you should not rely on it for any purpose . You may not copy or use this data and information except as expressly permitted by Wood Mackenzie in writing . To the fullest extent permitted by law, Wood Mackenzie accepts no responsibility for your use of this data and information except as specified in a written agreement you may have entered into with Wood Mackenzie for the provision of such data and information . Additional Information about the Business Combination and Where to Find It In connection with the Business Combination, Aurous Resources, a wholly - owned subsidiary of Rigel, has filed with the SEC a registration statement on Form F - 4 (the “Registration Statement”), which includes a preliminary proxy statement of Rigel and a preliminary prospectus of Aurous Resources, and after the Registration Statement is declared effective, Rigel will mail the definitive proxy statement/prospectus relating to the Business Combination to its shareholders and public warrant holders as of the respective record date to be established for voting at the meeting of its shareholders (the “Rigel Shareholders Meeting”) to be held in connection with the Business Combination . The Registration Statement, including the definitive proxy statement/prospectus contained therein, will contain important information about the Business Combination and the other matters to be voted upon at the Rigel Shareholders Meeting . This Presentation does not contain all the information that should be considered concerning the Business Combination and other matters and is not intended to provide the basis for any investment decision or any other decision in respect of such matters . The Target Companies, Aurous Resources and Rigel may also file other documents with the SEC regarding the Business Combination . Rigel’s shareholders, public warrant holders and other interested persons are advised to read the Registration Statement, including the preliminary proxy statement/prospectus contained therein, the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the Business Combination, as these materials will contain important information about the Target Companies, Aurous Resources, Rigel and the Business Combination . Stockholders will also be able to obtain copies of the preliminary proxy statement, the definitive proxy statement and other documents filed with the SEC, without charge, once available, at the SEC’s website at www . sec . gov . Participants in the Solicitation Rigel, Aurous Resources, and the Target Companies and their respective directors, executive officers, other members of management, and employees, under SEC rules, may be deemed to be participants in the solicitation of proxies of Rigel’s stockholders in connection with the Business Combination . Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of Rigel’s stockholders in connection with the Business Combination will be set forth in the Registration Statement, including a proxy statement/prospectus, filed with the SEC . Investors and security holders may obtain more detailed information regarding the names and interests in the Business Combination of Rigel’s directors and officers in Rigel’s filings with the SEC and such information will also be in the registration statement filed with the SEC by Rigel and Aurous Resources, which will include the proxy statement/prospectus of Rigel for the Business Combination . This Presentation is not a substitute for the Registration Statement or for any other document that Rigel, the Target Companies, or Aurous Resources may file with the SEC in connection with the potential Business Combination . INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DOCUMENTS FILED WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION . Investors and security holders may obtain free copies of other documents filed with the SEC by Rigel, the Target Companies, and Aurous Resources through the website maintained by the SEC at www . sec . gov .

Additional Cautionary Notes 3 Certain information in this Presentation is presented according to the customs outlined below for comparative purposes across the Target Companies’ industry. Investors are additionally cautioned about the following: ▪ This Presentation includes information on mineral reserves and mineral resources prepared in accordance with S - K 1300 . In most instances mineral resources are presented inclusive of mineral reserves, and data based on, or derived from, mineral reserves and resources may be on an “inclusive” or “contained” basis . Consequently, mineral grades reported on an “inclusive” or “contained” basis may not be reflective of individual grades of underlying mineral reserves or mineral resources . Mineral resources do not have demonstrated economic viability and a number of uncertainties may affect mineral reserve and mineral resource estimation . You are urged to read the S - K 1300 Technical Report Summary on the Blyvoor Gold Mine (available on EDGAR ) and the S - K 1300 Technical Report Summary on the Gauta Tailings Project (available on EDGAR ) . ▪ Certain information on mineral reserves and mineral resources for the Blyvoor Gold Mine and calculations derived therefrom are presented on a 100 % basis, for comparative purposes . Only 74 % is attributable to Aurous Gold, given its 74 % ownership percentage in the Blyvoor Gold Mine . ▪ Certain information about the net present value, denoted as “NPV”, of the Blyvoor Gold Mine and the Gauta Tailings Project in this Presentation is calculated based on an assumed 5 % discount rate . This information is derived from the S - K 1300 Technical Report Summaries . The best estimated discount rate used by the qualified person preparing the S - K 1300 Technical Report Summaries is 11 . 9 % .

Aurous Resources & Rigel Teams Izak Marais Chief Operating Officer • Previously served as COO at Gold One for 9+ years and as CEO at fluorspar miner Sallies for ~2 years • Also served as Manager Benchmarking for Goldfields, and as Operations Manager for the ultra - deep Kloof Gold Mine Jon Lamb Chief Executive Officer • Current Portfolio Manager at Orion, with extensive investment experience across precious / base metals • Previously worked as an Investment Manager at Red Kite and at Deutsche Bank in metals & mining advisory Alan Smith Executive Chairman • 27+ years with Anglo / DeBeers, including serving as General Manager at the Finsch diamond mine in South Africa • Thereafter, joined AngloGold SA as CEO, leading the entity during its time as the largest production unit of AngloGold Richard Floyd Founder and Chief Executive Officer • Prior to Aurous, spent 6+ years at gold mining operations associated with East Daggafontein and Galaxy Gold • Also served as Director at Raven Mining and Galaxy Gold Stratocorp Investments Nate Abebe President • Founded industrials - focused investment firm Rockpoint Capital in 2018, serving as Managing Partner • Previously worked as an Investment Manager at Orion Resource Partners and in commodities trading at Lehman and Barclays Oskar Lewnowski Chairman • Founder and Chief Investment Officer of Orion Resource Partners, an $8bn+ AUM metals and mining private equity firm • Previously founded Red Kite Group, a leading hedge fund in the metals space 4

Aurous Resources Snapshot ESG and HSE - focused management team Upside through clear organic growth and potential regional consolidation Proven, low - cost gold producer in the first quartile of the cost curve (1) with a strong track - record Top - tier production growth and a gold resource that ranks in the top - 20 globally (2) Approximately US$1.0bn replacement value for the existing mine and infrastructure Sources: CapitalIQ, Wood Mackenzie Notes: (1) The foregoing information was obtained from Metals Cost Curves , a product of Wood Mackenzie. (2) Based on contained reserve and resource (inclusive) size. Excludes mines with <25kozpa production between 2023 - 2025. Shown on a 100% basis. 5

Aurous is a Proven Gold Producer Transforming into a Multi - Asset Operation Blyvoor Gold Mine (Producing) 74% Owned, Shown on a 100% Basis (1,2) Low - cost, producing mine with substantial near - term growth Gauta Gold Project (Development) 100% Owned (2,3) A heavily de - risked source of incremental organic production Sources: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. Notes: (1) Aurous owns 74% of the Blyvoor Gold Mine; however, figures shown on a 100% basis. (2) Long term ZAR/USD of 19.08 for Blyvoor and 19.09 for Gauta per S - K 1300 reports. Assumed long term gold price of $1,900/oz. (3) BEE partnership not required for Gauta Gold Project. (4) Shown on a 100% basis. Mineral resources inclusive of mineral reserves. (5) Calculated as the overall resource grade for total mineral resources (measured, indicated and inferred) inclusive of mineral reserves. (6) Non - IFRS measure, which should not be considered in isolation or as substitute to IFRS measures. Please refer to section “Non - IFRS Disclosure” on page 36. (7) Consists of ~US$72m plant infrastructure costs, ~US$20m mining costs and ~US$2m spent on other infrastructure spend. NPV 5% of US$1,275m ~143koz average annual gold production ~US$145m average annual EBITDA (6) >30 - year remaining mine life 5.1Moz (4) of contained gold reserves (@ 5.5g/t Au) and 22.5Moz (4) of contained gold resource (@ 5.4g/t Au (5) ) ~US$665m of LOM total capex ~US$905/oz average annual all - in - sustaining cost (6) NPV 5% of US$115m ~30koz average annual gold production ~US$27m average annual EBITDA (6) 15 - year mine life ~US$94m (7) of pre - production capex 0.8Moz of contained gold reserves and 0.5Moz of contained gold resource (both @ 0.3g/t Au) ~US$982/oz average annual all - in - sustaining cost (6) ~US$87m average annual free cash flow (6) ~US$13m average annual free cash flow (6) 6

2.0 4.0 6.0 8.0 10.0 0 50 100 150 200 250 Y1 4,000 3,500 3,000 2,500 2,000 1,500 1,000 500 0 ▪ Established underground mine with a proven operating track record Produced first gold in 1942 and has a 75+ year operating history with >50 million ounces of historical gold production Restarted production in fiscal year 2022 ▪ Planned capital spending (~US$665m over LOM) is focused and leverages existing infrastructure Recent investment to re - open the Peter Skeat Shaft (previously known as the No. 5 Shaft) PIPE proceeds and cash remaining in the SPAC trust account expected to be used to refurbish underground and surface infrastructure as well as increase mill throughput ▪ Benchmarks well versus other gold producers Plots in the first quartile of the global gold cost curve ▪ Exceptionally high - grade resource base of 5.4g/t Au (1) offers material upside Current mine plan assumes just 23% (2) of total contained reserves and resources (on a 100% basis) is recovered over the life of mine Overview Blyvoor is a Well - Invested Producing Gold Mine with a First Quartile Cost Position Gold Production Cost Curve by Company (3) (100% basis) (AISC US$/oz Au) (4)(5) Spot Gold Price: US$2,323 / oz Au 18,000 54,000 72,000 Sources: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. FactSet. Market data as of 31 st May 2024. Notes: Aurous’ fiscal year ends on 28 Feb. (1) Shown on a 100% basis. Calculated on 22.5Moz of contained gold resource. Mineral resources inclusive of mineral reserves. (2) Based on mineral reserves as a proportion of total inclusive mineral resources. Based on a 5km radius mining area. (3) The foregoing chart was obtained from Metals Cost Curves , a product of Wood Mackenzie. (4) Net of by - product credits. (5) Non - IFRS measure, which should not be considered in isolation or as substitute to IFRS measures. Please refer to section “Non - IFRS Disclosure” on page 36. (6) LOM All in Sustaining Cost. Total gold recovered ~5.0 million ounces Production (koz) Recovered Grade (g/t) S - K 1300 Life - of - Mine Production Profile (100% basis) AISC (US$ / oz Au) 36,000 Paid Gold (koz Au) Y4 Y7 Y10 Gold Production (koz) Y13 Y16 Y19 Y22 Y25 Y28 Y31 Y34 Recovered Grade (g/t) Average Grade (g/t) Average Recovered Grade: 5.2 g/t Modelled LT Gold Price: US$1,900 / oz Au Blyvoor Gold Mine (US$905/oz) (6) 7

0 10 20 30 40 50 60 1937 1946 1951 1956 1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011 2016 2021 Paid Gold (million ounces) Blyvoor and Gauta Tailings Project S - K 1300 reports completed Underground mining operations restarted from the Peter Skeat Shaft commenced ramping up Updated technical report on Blyvoor and the Gauta Tailings Project Environmental authorisation granted for both Blyvoor and the Gauta Tailings Project Aurous Resources purchased Blyvoor and the Gauta Tailings Project VMR went into bankruptcy due to broader financial difficulty – Blyvoor mothballed Blyvoor sold to Village Main Reef Limited (“VMR”) Purchase of Blyvoor by DRDGOLD First production at Blyvooruitzicht Gold Mine (“Blyvoor”) Cumulative Historical Production Extensive Operational Track Record 1942 1997 2011 2013 2014 - 2016 2020 2021 Sources: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. Blyvoor Corporate Presentation Q1 2023. 2022 2024 x The Blyvoor Gold Mine has been historically profitable x However, Village Main Reef’s (VMR’s) marginal mines did not fare well during the gold price downturn in 2012 and resulted in the stoppage of all its mines, including Blyvoor x This provided a unique opportunity for Aurous Resources to acquire the Blyvoor Gold Mine and Gauta Gold Project and prepare a highly - economic, long - term business plan, without assuming certain legacy liabilities x The current Aurous management team has successfully repositioned the mine into a top - tier asset and has established a strong operational track record over the past few years The Blyvoor Gold Mine has produced over 50Moz of gold historically 8

61 34 26 24 17 16 14 14 14 South Deep (Gold Fields) Evander (Pan African) Mponeng (Harmony) Obuasi (AGA) Kibali (AGA) Kloof (Sibanye) Loulo (Barrick) Syama (Resolute) Free State (Harmony) 2024E AISC (3)(4) 1,252 907 1,189 1,014 834 1,180 938 1,409 1,351 43% 23% 19% 19% 17% 15% 11% 9% Bombore (Orezone) Bibiani (Asante) Twangiza (Baiyin) Kloof (Sibanye) Driefontein (Sibanye) Beatrix (Sibanye) Buckreef (TRX) Obuasi (AGA) Asanko (Galiano) Large, High - Grade Resource Base & Superior Growth vs. Peers Sources : S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29 , 2024 , CapitalIQ, Wood Mackenzie (Q 4 , 2023 ) . Screen based on CapitalIQ database (criteria primary commodity gold assets, active status, preproduction / operating / expansion stage) . Notes : ( 1 ) Blyvoor Gold Mine standalone figures based on S - K 1300 report . ( 2 ) Aurous production figures based on fiscal years ending 28 Feb . Fiscal year 2022 production has been annualised, based on 9 months of production . 2026 production figure from S - K 1300 . ( 3 ) AISC for peers based on Wood Mackenzie defined TCPS (Total Cash + Sustaining Cost), used as a proxy for AISC . The foregoing information was obtained from Metals Cost Curves , a product of Wood Mackenzie . ( 4 ) Non - IFRS measure, which should not be considered in isolation or as substitute to IFRS measures . Please refer to section “Non - IFRS Disclosure” on page 36 . ( 5 ) LOM All in Sustaining Costs . ( 6 ) Inclusive reserve and resource for Blyvoor Gold Mine on 100 % basis . Contained Gold Reserve & Resource Base (Moz Au, Capital IQ) (100% basis) 1 st in Africa 2 nd Globally 5 th in Africa 16 th Globally (1) (US$/oz) The Blyvoor Gold Mine (1) Ranks Favourably Across Gold Mines in Africa, with Further Upside from Gauta 2022 - 2026 Production CAGR (%, Capital IQ) (100% basis) (2) 62% 52% (6) 23 905 (5) (1) 9

Heavily - Invested Infrastructure Already in Place Brownfield Site Enables Quick Production Ramp Up ▪ Past - producing operation offered significant in - place infrastructure upon Aurous Resources’ acquisition of the Blyvoor Gold Mine including the Peter Skeat Shaft (formerly No . 5 Shaft) and Gauta Tailings Project - Circa US$141m has been invested by current owners (including Orion) into surface and underground infrastructure over the past 4 years - Most significant investments since 2015 have been on the treatment plant, Eskom yard, refurbishment of No . 5 Shaft infrastructure, and five vertical shaft winders ▪ Remaining infrastructure to be built includes re - opening of various underground workings and mill and processing upgrades ▪ Site is fed by two independent 132 kV overhead lines (Eskom) and 40 MVA substation with full redundancy (e.g. standby diesel generation capability under construction) ▪ In terms of a signed agreement, a 3 rd party has undertaken to build a 40 MW solar generation project on Aurous land - Once built, this is expected to reduce energy costs for the Aurous operations by ~9% or ~US$11/oz (1) Overview of Underground Mine Infrastructure 1 OF 4 UNDERGROUND WINDER CHAMBERS CLOSE UP VIEW OF 1 OF 4 UNDERGROUND WINDERS INSTALLED NEW MAN AND MATERIALS CAGE BEING INSTALLED IN THE PETER SKEAT SUB - VERTICAL SHAFT $2 $1 $2 $14 $49 $32 $28 $4 $4 $5 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 Investment Timeline of Current Owners (US$m) (2) Total invested: ~US$141m (3) Sources: Company information, Company Corporate Presentation Q1 2023, Company Audited Financial Statements. Notes: (1) Using Blyvoor’s actual electricity consumption for October 2022 to September 2023, and assuming an exchange rate of ZAR19/US$, annualised production of 30koz and 25% daylight hours. (2) Fiscal year basis, fiscal years ending 28 Feb. (3) Includes capitalised expenses. 10

Details of Near Term Capital Requirements at Blyvoor Gold Mine (1) Total LOM (6) (US$m) Total Y1 & Y2 (US$m) Y2 as per S - K 1300 (US$m) Y1 as per S - K 1300 (US$m) Historical Capex Spent (FY15 - FY24) Project 207.9 61.9 36.5 25.4 126.4 Underground Expansion 36.1 11.0 4.0 6.9 31.6 Opening - Up and Development 29.7 10.5 6.7 3.8 24.5 Establishing Production Faces 11.9 2.7 1.6 1.1 23.8 Engineering and Equipping 46.3 20.0 11.8 8.2 19.9 Shaft Infrastructure 47.7 10.5 7.9 2.6 11.1 Technical Services - - - - - - - - 15.5 Surface Assets 36.2 7.3 4.5 2.8 - - Contingency 389.0 4.6 2.2 2.4 - - Underground “Stay in Business” 67.2 6.1 5.5 0.6 15.1 Processing Plant Capex (5) (expansion + contingency) 664.7 72.6 44.2 28.4 (2) 141.5 Total Capital Requirement Clear Capital Deployment Plan to Enable Production Growth Sources: Company information and S - K 1300 Technical Report on the Blyvoor Gold Mine, with an effective date of February 29, 2024. Notes: Financials shown on fiscal year basis. Fiscal year ending 28 Feb. (1) Total capex in line with capex outlined in S - K 1300 Technical Reports on the Blyvoor Gold Mine. Categorisation varies as compared to the S - K 1300 report, and is pursuant to the Company’s internal accounting. (2) Peak capex of US$29m to be funded from PIPE proceeds and remainder to be funded via operating cash flows. (3) Consists of ~US$72m plant infrastructure costs, ~US$20m mining costs and ~US$2m spent on other infrastructure spend. (4) Total Gauta capital spend in Y2 of ~US$89m, includes ~US$16m of contingency capital. (5) Expansion, stay in business and contingency capital. (6) Excluding Historical Capex Spent ▪ Actual results may differ based on actual amounts of funding received, as well as timing of consummation of de - SPAC transactions ▪ PIPE proceeds are expected to be used to fund the expansion of the Blyvoor Mine and associated processing plant ▪ A portion of the funding for this expansion is expected to also come from existing operations ▪ Aurous is also in advanced discussions regarding a debt facility which it expects to be able to draw on, as needed ▪ Operating cash flow of US$6.9m and US$38.1m expected to be generated in Y1 and Y2, respectively (per SK1300 technical reports) - Assumes gold prices of US$2,078/oz and $2,016/oz, respectively ▪ Pre - production capex for Gauta of US$94m (3) required (~$89m (4) to be spent in Y2) - Debt financing anticipated for Gauta 11

$29 $44 $42 $41 $43 $28 $21 $14 $10 $5 $19 $20 Strong Resulting Near - Term Cash Flow Profile from Assets EBITDA (2) (US$m) Y2 Y3 Payable Gold Production (koz Au) Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. Notes: Financials shown on fiscal year basis. Fiscal year ending 28 Feb. (1) Blyvoor Mine shown on 100% basis. (2) Non - IFRS measure, which should not be considered in isolation or as substitute to IFRS measures. Please refer to section “Non - IFRS Disclosure” on page 36.. Blyvoor Mine (1) Full Year SK - 1300 Projections (US$m) Unlevered FCF (2) (US$m) Capex (US$m) $5 $38 $77 $72 $120 $145 $167 $161 $192 $200 $208 $163 ($22) ($6) $35 $33 $66 $81 $102 $102 $125 $135 $130 $100 25koz 50koz 81koz 87koz 145koz 125koz 165koz 163koz 180koz 186koz 190koz 164koz Y1 Y4 Y5 Y6 Y7 Y8 Y9 Y10 Y11 Y12 12

Blyvoor Maintains Strong Relationships with Key Stakeholders Black Economic Empowerment (BEE) • Unique ownership opportunity for community and employees to be direct equity participants through the broad - based BEE structure • Employee and community trusts set up to directly benefit the local communities and employees through the BEE structure • BEE 26% ownership of the Blyvoor Gold Mine is split as follows: - 20% Blyvoor Workers Trust (1) - 3% Blyvoor Community Trust - 3% SPV - focused on black entrepreneurs Union Relationships • Employees formed a new union in 2018 called the Blyvoor Workers Union (BWU) (2) • This union is not affiliated with larger unions such as National Union of Mineworkers (NUM) or Association of Mineworkers and Construction Union (AMCU), nor is it affiliated with any trade union federation • Highly collaborative management/union relationship, with wage increases and other matters of mutual interest negotiated periodically as agreed • Union members benefit from Blyvoor Workers Trust distributions • Anticipate new tailings employees to be hired under similar unionised workforce structure Source: Company Management. Notes: (1) In April 2023 , Blyvoor made a first payment to the workforce as part of profit - sharing arrangement. (2) Labour relations act allows for a closed shop agreement – in effect the Closed Shop Agreement at the Blyvoor Gold Mine provides for all employees to be part of the Blyvoor Workers Union and compels all new employees joining the company to join this union. The union represent all employees at Blyvoor except senior management. 13

Source: Company Management. Aurous Resources Capital Environmental Policy. Notes: (1) Environmental Authorisation was obtained following submission of the EMPR and the EIA by the Company. Both the underground operation and its treatment plant are fully permitted, and the tailings operation has environmental authorisation to build the tailings treatment plant, mine TSF no.7 and deposit residues onto TSF No. 6. The tailings operation will require additional permitting to allow for deposition on the footprint of TSF No.7 . This authorisation process will commence once the project implementation phase commences. (2) Aurous works closely with Harmony Gold on water issues; the surface and groundwater monitoring programs are currently managed by Harmony Gold. Aurous has an ESG - Focused Management Team Environmental Assessment granted in February 2020 for Blyvoor Gold Mine and for Gauta Tailings Project (1) Environmental Compliance Water Quality Ongoing monitoring of surface and groundwater (2) as well as an onsite plant to treat sewage Renewable Energy Agreement signed with 3 rd party to build a 40 MW solar generation plant on Aurous land and enter into a long - term power purchase agreement Local Employment US$41m invested via employment in the local economy over the 6 - year period ending February 2024 Strong Governance Majority independent board planned; stringent compliance controls in place across the organisation Mining Rehabilitation Initial costs assessed and insurance in place; funding of revised rehabilitation costs being explored 14

Lost Time Injury Frequency Rate per 1 Million Hours (LTIFR) (1) Deep Commitment to Improving Safety Track Record Source : Company information . Notes : ( 1 ) Calculated as : number of LTI’s / total hours worked x 1 , 000 , 000 hours . A Lost Time Injury (“LTI”) is an injury to an employee which causes the employee not to be able to report to work on the day following the injury . The calculation for the statistic divides the number of LTIs which occur in one month by the number of manhours worked in that month and then multiplies the result by 1 , 000 , 000 man hours . Initiatives to Improve Safety x Leading by example in commitment to health and safety and pursuing harm - free mining x Implementation of ISO 45001 (Occupational Health and Safety) is underway to continually improve health and safety at the mine x Adjustments to mining sequence and support characteristics to reduce the potency of seismic incidents x Focus on improving pre - conditioning of mining faces and face shapes to reduce seismicity x Closer scrutiny and more vigorous investigation into seismic incidents x Established a messaging line for reporting incidents and at - risk situations Total Injuries 12 - Month Moving Average 3 15 2 3 0 5 1 4 8 0 1 3 3 5 6 1 1 5 7.3 7.0 6.3 5.9 6.6 6.6 7.0 8.5 8.1 8.2 8.3 8.5 8.9 9.8 9.2 9.4 9.5 Sep - 22 Oct - 22 Nov - 22 Dec - 22 Jan - 23 Feb - 23 Mar - 23 Apr - 23 May - 23 Jun - 23 Jul - 23 Aug - 23 Sep - 23 Oct - 23 Nov - 23 Dec - 23 Jan - 24

Tailings Offer a Heavily De - risked Source of Organic Production Located in Close Proximity to the Blyvoor Gold Mine S - K 1300 Life - of - Mine Production Profile (100% basis) Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. Notes: (1) Legacy entity Goldfields South Africa (GFSA). (2) Cumulative Reserves and Resources figure for all TSFs. (3) Water use license has expired; the Company is renewing the license. (4) Long term ZAR/USD exchange rate of 19.15 per S - K 1300 reports. (5) Consists of ~US$72m plant infrastructure costs, ~US$20m mining costs and ~US$2m spent on other infrastructure spend. Overview ▪ Gauta represents a natural, nearby source of gold for retreatment Aurous wholly - owns Gauta which owns the six tailings deposits created from historical Blyvooruitzicht (Rand Mines Ltd) and Doornfontein (Goldfields Ltd (1) ) mine production (TSF 6 is currently in use) Incremental ~30koz of average annual gold production at an estimated all - in - sustaining - cost of ~US$982/oz Au over the life - of - mine 1.3Moz of contained reserves and resources (2) , on a 100% basis Adjacent to further tailings deposits from the Savuka mine (Harmony) and Driefontein mine (Sibanye) ▪ De - risked path to production provides low - cost organic growth Key permitting in place for plant construction and subsequent re - mining / processing (3) First production expected in 3 years, with tailings converted into slurry through high - pressure water monitoring before being transported via pipeline to a new processing plant Typical plant flowsheet with thickening, leaching and carbon treatment ▪ Highly economic project with an NPV5% of US$115m Pre - production capex is ~US$94m (4)(5) and there is potential for upside from both inferred resource conversion, if proven to be economically viable, and acquisition of adjacent TSFs Flexibility in mine plan allows for tailings to be processed in a manner such that economics are maximised Production (koz) Recovered Grade (g/t) Blyvoor TSF 1 Doornfontein TSF 1 Doornfontein TSF 2 Doornfontein TSF 3 Blyvoor TSF 6 Blyvoor TSF 7 Blyvoor Gold Plant 5km Peter Skeat Shaft 0.0 0.1 0.2 0.3 0.4 50 40 30 20 10 0 Y3 Y5 Y7 Y9 Gold Production (koz) Y11 Y13 Y15 Recovered Grade Y17 16

115 109 99 76 74 53 35 31 30 14 Australia Canada Russia South Africa USA Indonesia Brazil PNG Mexico Chile Prolific Gold Production Region ▪ South Africa contains the 4 th largest gold resource base in the world and the Witwatersrand is one of the most prolific regions Aurous is located within the Carletonville Goldfield, one of the most significant historical gold deposits that contains some of the largest underground mines in the world With an improved gold price outlook, some of the region’s historical underground operations have received a new lease on life Witwatersrand has produced ~50m ounces of gold since 1995 and represents ~3% of global annual gold production today ▪ Plenty of high - quality assets indicative of consolidation potential Notable gold mines located in close proximity include Kusasalethu and Mponeng (Harmony) and Driefontein (Sibanye) Sources: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. AME. Wood Mackenzie. Notes: (1) The foregoing chart was obtained from Global Gold Mine Supply Summary , a product of Wood Mackenzie. (2) Based on latest Wood Mackenzie data for year end 2022. Aurous Sits in One of the Most Prolific Gold Mining Jurisdictions Top Countries by Contained Gold Resources (1) Contained gold resource by country today (2) , Moz Au N Blyvoor Kloof Consolidated Leeudoorn South Deep Mponeng Kusasalethu Driefontein Consolidated West Wits Surface Cooke West Rand Tailings Wilwatersrand Basin Johannesburg Development Stage Operating Developing / Exploration Aurous Located Amongst World - Class Gold Mines 17

Transaction Details

Key Elements of the Proposed Transaction x The transaction values Aurous Resources at a pre - money equity value of US$362m (US$350m (1) for Aurous’ ownership in the Blyvoor Mine and US$12m for Gauta Tailings) x The transaction contemplates raising a minimum US$50m PIPE of which US$7.5m has already been committed from leading institutional and strategic investors x Net proceeds will be used to accelerate production growth x Orion currently owns ~20% of Aurous Resources’ 74% ownership of the Blyvoor Mine 63% 13% 1% 13% 10% Illustrative Transaction Overview Pro Forma Valuation & Ownership at Close (3) Illustrative Sources & Uses (5) Existing Blyvoor Shareholders Existing Gauta Shareholders RRAC Public Shareholders RRAC Founder Shares (Orion) PIPE Investors (4) Notes: (1) Equates to Aurous Resources’ existing 74% ownership of the Blyvoor Mine. (2) Includes Aurous Resources’ existing net commercial debt as at end of Fiscal Year 2024 (ending 29 Feb 2024), adjusted for transaction impacts. Pro - forma commercial debt is US$4.2m. (3) Pro forma valuation and pro forma ownership at $10.00 per share. Excludes the dilutive impact of SPAC public warrants and Sponsor warrants with an $11.50 exercise price. Excludes the impact of the new, to - be - established equity incentive plan, seller and management earnout, and deferred share consideration. (4) Represents an effective net purchase price of $6.67 per share. (5) Assumes $50m of PIPE proceeds; as of this date $7.5m of PIPE proceeds have been committed. (6) Redemption percentage based on current Rigel redemption status as of August 13, 2024. (7) Excludes approximately US$1m of shares transferred to committed PIPE investors. (8) Assumes a redemption price of $11.40 per share at close. Non - redeeming public shareholders to receive a cash consideration to the extent cash in trust at close exceeds $10.00 per share. Redemptions (%) (6) Sources (US$m) $81 RRAC Cash in Trust 50 Third Party PIPE Proceeds 349 Blyvoor Equity Rollover (7) 6 Gauta Equity Rollover $487 Total Sources Uses (US$m) $98 Cash to Balance Sheet 6 Cash Proceeds to Gauta 10 Cash Proceeds to Non - Redeeming Public Shareholders (8) 349 6 Blyvoor Equity Rollover Gauta Equity Rollover 17 Illustrative Fees & Expenses $487 Total Uses ~71% (US$m) Illustrative Share Price $10.00 (x) Pro Forma Shares Outstanding 55.2 Pro Forma Equity Value $552 ( - ) Pro Forma Cash (98) (+) Pro Forma Debt (2) 4 Pro Forma Enterprise Value $458

81 3,264 1,811 1,303 1,197 854 - - - - 529 498 497 395 395 388 367 366 364 358 347 345 315 301 275 227 208 204 189 161 130 120 112 107 92 75 70 Westgold Ramelius Karora Wesdome Calibre New Gold Endeavour Silver Lake Tietto IAMGOLD Galiano Perseus G Mining Hummingbird B2Gold Centamin Shanta Gold Ascot Gold Fields Aura Minerals Asante Gold Harmony Resolute West African Orezone Argonaut Aris Mining Caledonia Osino Resources DRD Gold OreCorp Pan African McEwen St Barbara 2.6x 2.0x 1.9x 1.7x 0.4x 0.3x 0.0x 1.3x 1.3x 1.3x 1.2x 1.2x 1.2x 1.1x 1.1x 1.0x 1.0x 1.0x 1.0x 1.0x 0.9x 0.9x 0.8x 0.7x 0.7x 0.7x 0.6x 0.6x 0.6x 0.5x 0.5x 0.5x 0.4x 0.4x Harmony Galiano Gold Fields Tietto New Gold Centamin Ramelius Wesdome Silver Lake Westgold Pan African OreCorp Perseus West African Resolute G Mining IAMGOLD Endeavour Calibre Karora B2Gold Ascot Shanta Gold Osino Resources McEwen Caledonia St Barbara Aura Minerals Hummingbird Argonaut Asante Gold Aris Mining Orezone DRD Gold EV / Attributable Reserves ($ / oz) (Blyvoor Gold Mine 74% basis) Attractively Priced Transaction vs. Public Gold Producers Price / NAV (Broker Consensus) (x) (Blyvoor Gold Mine 74% basis) (1) 0.3x Sources: FactSet, SNL CapitalIQ, company filings, SK1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings Project, with an effective date of February 29, 2024. Market data as of 31 May 2024. Notes: Reserves and Resources data for Blyvoor Gold Mine and Gauta Tailings Project as of 29 February 2024, for other companies in composite Reserves and Resources data as of November 2023. Represents select African and Global producers only. (1) Based on NAV at 5% discount rate. Calculated as US$362m pre - money equity value divided by attributable NAV of US$1,047m (sum of 74% of US$1,275m in Blyvoor and 100% of US$115m in Gauta adjusted for net commercial debt at Blyvoor Gold Mine (US$4.2m) and Gauta Tailings (US$6m). Net debt as at end of Fiscal Year 2024 (ending 29 Feb 2024). South African Median: $150/oz African Multi - Asset Median: $358/oz South African Median: 1.5x African Multi - Asset Median: 0.7x African Single - Asset Median: 1.2x Global Multi - Asset Median: 0.9x Global Gold Developers Median: $211/oz Global Gold Developers Median: 0.8x African Single - Asset Median: $268/oz Global Multi - Asset Median: $497/oz 19

Post - Deal Organizational Structure Pre - & Post - Transaction Organizational Structures Pre - Deal Organizational Structure Note: (1) Rigel will be renamed as Aurous Resources post transaction. Orion Mine Finance Fund II L.P. (Bermuda) Avaya (Mauritius) Stratocorp Blyvoor Gold Blyvoor Resources Blyvoor Operations (Tailings) Black Economic Empowerment Partners Blyvoor Gold Capital & Subsidiaries Mining Rights SPAC Shareholders SPAC (Cayman Islands) 40% 60% 19.95% 80.05% 100% 100% 74% 26% PIPE Investors SPAC Shareholders SPAC Sponsor (Orion) Aurous Shareholders Gauta Shareholders Aurous Resources (1) Gauta Tailings (Blyvoor Operations) (Tailings Project) Black Economic Empowerment Partners Blyvoor Gold Capital & Subsidiaries Mining Rights 26% 74% 100% Aurous Gold 20

Combination Benefits for Investors US - listed vehicle Highly attractive listing jurisdiction enabling future consolidation and growth Backed by Orion, a leading, global metals & mining alternative investment firm Orion manages over US$8bn and has extensive South African and precious metals experience Attractive valuation Transaction implies an Aurous P/NAV of 0.3x Low cost, high margin operations st 1 quartile cost position (2) with Blyvoor mine all - in - sustaining cost (3) of ~US$905/oz $ ESG - focused management Management team is laser - focused on improving safety and maintaining a collaborative and productive relationship with the workforce Top production growth 62 % production growth between FY 2022 - FY 2026 ( 1 ) (including establishment of Gauta) Heavily de - risked Simple operations & fully permitted, with approximately US$1.0bn worth of infrastructure in place (in terms of replacement value) Sources: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. CapitalIQ. Wood Mackenzie. Notes: (1) As per S - K 1300. Fiscal year ending 28 Feb. Fiscal year 2022 production has been annualised, based on 9 months of production. 2026 production figure from S - K 1300. (2) The foregoing information was obtained from Metals Cost Curves , a product of Wood Mackenzie. (3) Non - IFRS measure, which should not be considered in isolation or as substitute to IFRS measures. Please refer to section “Non - IFRS Disclosure” on page 36. 21

Appendix 1 – Rigel Information

Orion & Rigel Resource Acquisition Corp Rigel Management Team Key Focus Areas & Select Orion Investments “Green” Metals • “Green” base metals (copper, nickel, zinc) • Other battery metals (lithium, cobalt, vanadium) • “Green” precious / PGMs ▪ Founder and CEO of Orion Resource Partners ▪ Founding Partner of the Red Kite Group and the Chief Investment Officer of the Mine Finance business ▪ Previously Director for Corporate Development at Varomet, a metals processor and merchant firm of >$1bn revenues Oskar Lewnowski Chairman ▪ Portfolio Manager at Orion ▪ Prior to Orion, Investment Manager for Red Kite’s Mine Finance business ▪ Previously worked in Deutsche Bank's Metals & Mining Investment Banking group Jon Lamb CEO ▪ Founder and Managing Partner of Rockpoint Capital ▪ Previously worked as an Investment Manager at Orion ▪ Previously a commodities trading analyst at Lehman Bros, Barclays Capital and LAMCO Nate Abebe President Precious Metals • “High value” metals including gold, silver, palladium, rhodium, etc. South Africa Exposure (Platreef) Overview ▪ Rigel Resource Acquisition Corp is a SPAC sponsored by Orion Resource Partners (“Orion”), that listed on the NYSE in a $300mm IPO in Nov 2021 (1) ▪ The SPAC received shareholder approval for an extension to it’s business combination deadline in August 2023, resulting in an extension to February 2025 and is transitioning to a listing on the NASDAQ ▪ Orion was founded in 2012 and is a global, asset management firm with an AUM of over $8bn (2) that focuses on investments in and financial solutions for metals and mineral companies ▪ Orion operates five complementary business lines: □ Orion Mine Finance: Late - stage private equity providing capital to base and precious meta mining companies □ Orion Mineral Royalty Fund: Royalties on lower - cost mines in geopolitically stable regions □ Orion Commodities Fund : Sector - specific hedge fund employing a discretionary investment style □ Orion Merchant Services: Trading, hedging, insuring and delivering physical metals worldwide □ Orion Industrial Ventures: Venture capital focused on technology companies that aim to decarbonize industry and enable the economic supply of the minerals and energy required for sustainable growth ▪ Portfolio Companies / Investments: 70+ ▪ Employees: ~70+ ▪ Offices: New York (HQ), Denver, London & Sydney Sources: Orion Resource Partners company website - https:// www.orionrp.com/ Notes: (1) Total proceeds of $306m raised including Greenshoe and private placement. (2) As of March 2024.

Orion’s Expertise in Gold & South Africa Commitment to Aurous ▪ Orion holds a 19.95% stake in the Blyvoor Gold Mine through its Mine Finance Fund II LP ▪ Orion has been a committed partner to Aurous since August 2018 as the principal investor in restarting the Blyvoor Mine, when Orion acquired a participation through a stream and an offtake (for US$37m) and an equity stake (for a subscription price of US$23m) ▪ Additionally, Orion has demonstrated continued support of Aurous during the ramp - up of the Blyvoor Mine by investing a further US$5m in Q4 2021 to expand production at the mine ▪ Orion has significant experience partnering with, investing in and supporting mining operations in South Africa ▪ In July 2022, Orion invested US$100m in Sedibelo Resources to expand production at Sedibelo’s Pilansberg Platinum Mines located in South Africa ▪ In December 2020, Orion invested US$65m in Bushveld Minerals to expand production of Bushveld’s Vametco Mine located in South Africa ▪ In October 2019 , Orion invested in Allied Gold Corp (TSX : AAUC) to support Allied’s acquisition of the Agbaou Gold Mine located in Cote d’Ivoire from Endeavour Mining ▪ In December 2016 , Orion invested in Alufer Mining to support the construction and commence production of the Bel Air Mine in Guinea US$153m Loan, Equity, Warrants and Offtake Victoria Gold Corp April 2018 Loan, Stream, Equity and Offtake Allied Gold Mining plc October 2019 US$225m Prepay, Stream, Equity and Offtake Lundin Gold Inc. May 2017 Select Other Precious Metals Investments by Orion US$268m Equity Nomad Royalty Company May 2020 ▪ Publicly - listed precious metals royalty company formerly listed on the TSX (before Sandstorm acquisition) ▪ Owned 10 precious metals royalties, including one on the Blyvoor Mine Precious Metals Royalties ▪ Privately owned gold producer going through growth phase ▪ Owns a number of producing and development assets in West Africa African Gold Producer ▪ Publicly - listed gold exploration and production company ▪ Owns the Eagle Gold Mine in Canada that Orion helped finance into production Gold Producer ▪ Owns the Fruta del Norte gold mine in Ecuador ▪ Commenced operations in 2019 as one of the highest - grade gold mines in the world Gold Producer

Timothy Keating Independent Director Kelvin Dushnisky Independent Director Christine Coignard Independent Director Peter O’Hagan Independent Director Jeff Feeley Chief Financial Officer Nathaneal Abebe President Jonathan Lamb Chief Executive Officer Oskar Lewnowski Chairman • Most recently served as the Head of Mining Investment Private Equity at the Oman Investment Authority • Extensive metals and mining experience gained at African Nickel Ltd, Anglo American and Investec Bank • Most recently served as Chief Executive Officer and an Executive Director of AngloGold Ashanti • Prior to AngloGold Ashanti, had a 16 - year career with Barrick Gold, ultimately serving as President and a member of its Board of Directors • Senior Advisor in metals and mining sector • Extensive banking, investing, management and board experience built during a career at the Royal Bank of Canada, Société Générale, and Citi • Previously worked for Norilsk Nickel, one of the world’s largest producers of palladium • 30 years experience in commodities and natural resources investing and operations • Former head of Goldman Sachs’ Global Commodities business • Founding CEO of GS Bank USA • Former MD at Carlyle Group • Former Operating Advisor at KKR • Chief Financial Officer at Orion Resource Partners • Former Director of Finance for the Global Equities division of Citadel LLC • Prior to Citadel, spent over 13 years as a Controller at Goldman Sachs • Founder and Managing Partner of Rockpoint Capital, an investment vehicle via the search fund model • Formerly an Investment Manager at Orion Resource Partners • Spent time as a Commodities analyst at Lehman Brothers, Barclays Capital, and LAMCO • Portfolio Manager at Orion Resource Partners • Formerly an Investment Manager for the Red Kite Group’s Mine Finance business • Also worked for Deutsche Bank in their Metals & Mining group • Founder and Chief Investment Officer of Orion Resource Partners, a private equity firm within the metals and mining sector with over $8bn in AUM • Founding Partner of the Red Kite Group, one of the world’s leading hedge funds in the metals space • Spent time at Credit Suisse and Varomet Rigel Resource Acquisition Corp Management & Board of Directors Source: Rigel company website - https:// www.rigelresource.com/team.

Appendix 2 – Further Aurous Detail

Motsumi Tlhapi Chief Safety Officer João Mahumana Mine Manager Pieter du Preez Chief Financial Officer Izak Marais Chief Operating Officer Alan Smith Executive Chairman Richard Floyd Chief Executive Officer Safety Practitioner with over 28 years experience Prior experience includes: CSO of Lanxess Chrome Mine Rustenburg, Maseve Platinum Mine Rustenburg and Samancor Limpopo Member of the South African Institute of Occupational Safety And Health (SAIOSH) Mining Engineer with over 35 years experience Prior experience includes operations manager at Beatrix, Burnstone trackless mining and Blyvooruitzicht Mine, projects manager for DRDGOLD corporate office, Underground Manager at Driefontein, Elandsrand and Natalspruit in the Free State Corporate finance executive with over 25 years of experience Prior experience includes being CFO of Taung Gold, Group Economist at Gold Fields and Corporate Finance Executive at Touchstone Capital and Sasfin Capital where he worked on capital raisings, mergers and acquisitions and deal origination CFA Charterholder Mining engineer with over 30 years of experience Prior experience includes being CEO of fluorspar - miner Sallies (JSE), COO of Gold One Group (ASX/JSE), Benchmarking Manager for Gold Fields and Operations Manager for the ultra - deep Kloof Gold Mine Mining engineer with over 45 years experience Prior experience includes being CEO of AngloGold Ashanti South Africa, CEO of FreeGold Ltd and GM of De Beers’ Central Mines (Kimberley, Finsch and Koffiefontein) Member of the Association of Mine Managers South Africa Cofounder and shareholder responsible for Aurous’ revival Successfully raised c. $100m to build new infrastructure and ramping up production Prior decade as gold mining exec at Galaxy/Galane Gold (TSX), East Daggafontein Mines Ltd (ex Anglo), Raven Mining Zimbabwe Member of the Association of Mine Managers South Africa Aurous Resources Management Team Sources: Blyvoor Corporate Presentation Q1 2023, Company Management. Stratocorp Investments

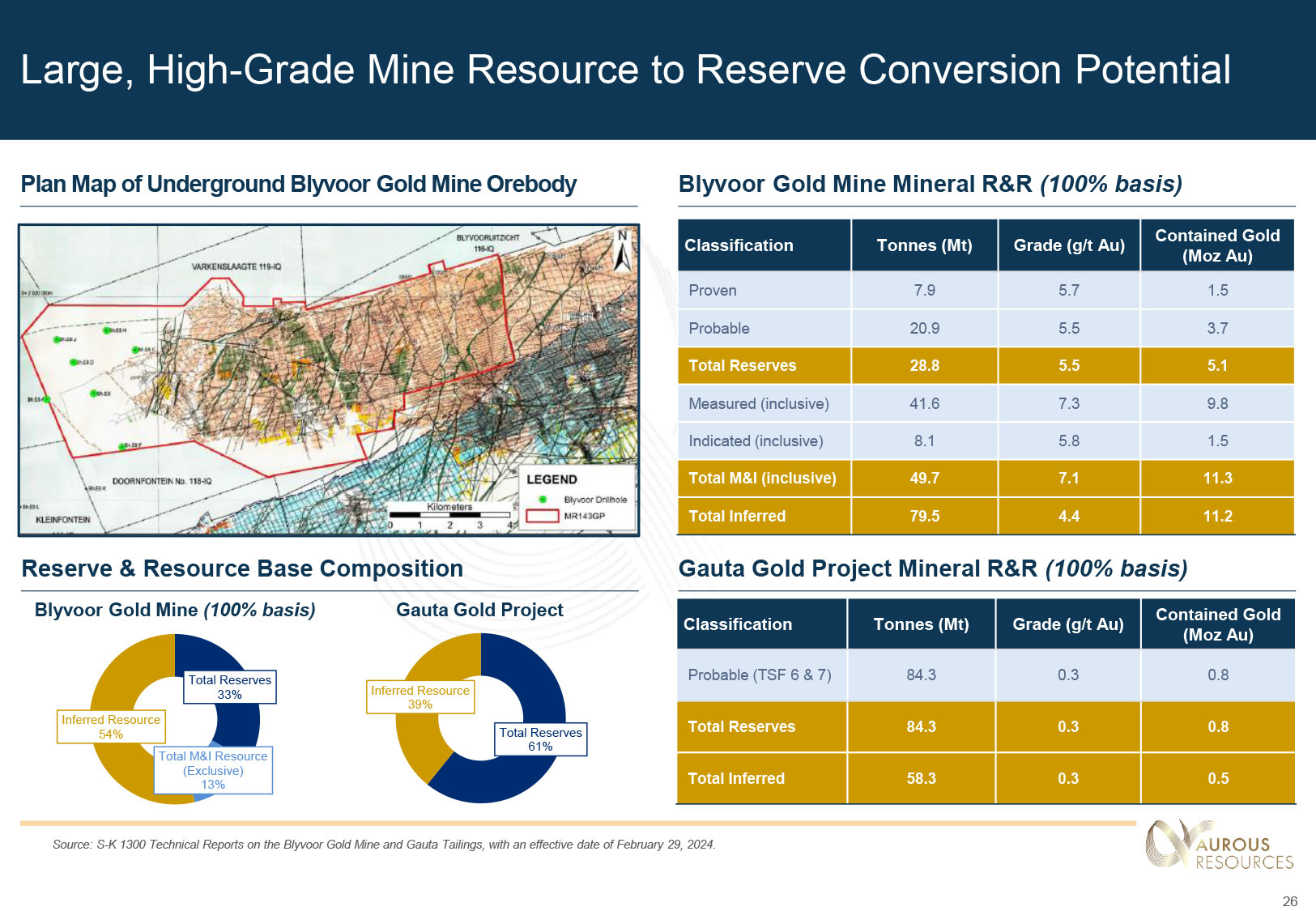

Total Reserves 33% Total M&I Resource (Exclusive) 13% Inferred Resource 54% Blyvoor Gold Mine Mineral R&R (100% basis) Plan Map of Underground Blyvoor Gold Mine Orebody Large, High - Grade Mine Resource to Reserve Conversion Potential Contained Gold (Moz Au) Grade (g/t Au) Tonnes (Mt) Classification 1.5 5.7 7.9 Proven 3.7 5.5 20.9 Probable 5.1 5.5 28.8 Total Reserves 9.8 7.3 41.6 Measured (inclusive) 1.5 5.8 8.1 Indicated (inclusive) 11.3 7.1 49.7 Total M&I (inclusive) 11.2 4.4 79.5 Total Inferred Gauta Gold Project Mineral R&R (100% basis) Total Reserves 61% Inferred Resource 39% Reserve & Resource Base Composition Blyvoor Gold Mine (100% basis) Gauta Gold Project Contained Gold (Moz Au) Grade (g/t Au) Tonnes (Mt) Classification 0.8 0.3 84.3 Probable (TSF 6 & 7) 0.8 0.3 84.3 Total Reserves 0.5 0.3 58.3 Total Inferred Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024.

Blyvoor Gold Mine Employs a Simple & Highly Effective Mining Method Mining Method Employed ▪ Mining strategy is to extract both the quartz - pebble Middelvlei Reef (MV) and the carbonaceous, gold - rich Carbon Leader Reef (CL) ore utilizing the Peter Skeat Shaft (1) - Conventional stoping method implemented at No.5 shaft using hand - held hydro - powered drills to clear ore to existing ore passes ▪ No dewatering required at present as all mining will take place above water level over the next five years (2) - Planned dewatering efforts will allow for incremental mining in years beyond ▪ Significant potential efficiency upside should selective bench mining be employed - Halves the ore hauled for same gold production and increases feed grade Key Advantages of Selective Bench Mining Sources: Blyvoor Corporate Presentation Q1 2023, Company information. Notes: (1) The Carbon Leader Reef is located above the Middelvlei reef, located ~80m apart vertically. (2) The water level is ~2,370m below surface. The lowest operating level currently is located 2,291m below surface. Potential Upside Through Selective Bench Mining x Reduced dilution of reef x Better working conditions x Improved ventilation controls and lower ventilation costs x Reduced seismicity x Improved metal recovery vs. mine planning estimate (mine call factor)

Mine Assumes a Conventional Processing Flowsheet Processing Overview ▪ The plant has a current run - of - mine (ROM) feed capacity of 40 ktpm and an expansion to 80 ktpm is in process to allow for the planned increase in production ▪ The plant employs a conventional flowsheet, consisting of: - Crushed ore from the mine passes into either of two mills, to a carbon in pulp (CIP) circuit with the option of gravity concentration prior to the leach circuit - Loaded carbon from the CIP circuit is fed into the elution circuit to strip the gold off the carbon - On - site smelting to produce dore bars of approximately 85% purity on average for delivery to Rand Refinery (the world’s largest gold refinery) for further refining ▪ The mine plan contemplates a processing plant feed grade of between 4 g/t Au and 7 g/t Au depending on the mining mix ▪ Tailings are deposited onto the existing No. 6 tailings storage facility (TSF) - Will potentially form part of tailings retreatment feedstock as part of Gauta Tailings Project Process Flow Sheet Source: Blyvoor Corporate Presentation Q1 2023. Fine Surface Source RoM Coarse Surface Source RoM Silo Crushed Ore Silo Ore Milling Ore Crushing Classification Gravity Concentration Intensive CIL Conditioning and Leach CIP Elution and EW Smelting Detox Thickening TSF Dore

Current & Future Underground Infrastructure No. 2A Sub - vertical Shaft – Not to be used Surface 15 Level 17 Level 19 Level 29 Level 31 Level 33 Level Level Closed - FOG New Dewatering Column 889m Peter Skeat Shaft No . 1 A Sub - vertical Shaft – Emergency Secondary Escape 15 Level 9 Level 47 Level 43 Level Loading Station B5A Incline A5 Incline Boundary 1 Level 6 Level 12 Level 16 Level 19 Level 24 Level 34 Level B5 Incline 2566 to Surface 33 Level Dams Peter Skeat Sub - vertical Shaft 1677m to Surface 14 Level Dams Doornfontein Sect. Old Blyvooruitzicht Sect. Shaft Bottom - 3462.8 25 Level 29 Level Dams 27.5 Mid Shaft Loading 21 Level 23 Level 33 Mid Shaft Loading New Dewatering Column Existing Development & Infrastructure New Development Existing Traveling Ways New Dewatering Column Existing Ore passes Legend: Current Mining Area New Orepass System Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. 29

View of Peter Skeat Shaft Surface Infrastructure Legend Peter Skeat Shaft Lamproom and Crush Peter Skeat Shaft Offices and Admin Block Peter Skeat Shaft Surface Winderhouse Peter Skeat Shaft Distribution Substation Peter Skeat Shaft Engineering and Infrastructure Battery Limit Peter Skeat Shaft Headgear and Shaft Blyvoor Intake Yard, Sub and PFC Equipment Eskom Substation Explosives Bay Process Plant Battery Limit Sewage Plant Shaft Parking Area Shaft Silo Feed Conveyor Surface Compressor and Cooling Towers Surface Store Surface Ventilation Fans Surface Workshop Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. 30

Proven Gauta Tailings Retreatment Process Gauta Mining & Processing Overview ▪ The mining method planned to be used for the reclamation of the TSF No . 6 and TSF No . 7 is hydro - mining, which uses high - pressure water monitors (water jets) to erode the TSF - Mining will commence with targeting the high - grade areas located at the upper portion of TSF No. 6 and then move to TSF No. 7 - Aurous will seek to subsequently mine the other TSFs ▪ The planned mining strategy involves a 12 - month ramp up to 500 ktpm steady state - production over a period of 15 years ▪ Ore slurry will then be transported to the processing plant via pipeline, where 500 ktpm will be treated through two identical circuits - Subsequently, a well - tested and widely used Carbon - In - Leach (CIL) process will be used to recover the gold - An oxidation step will be utilised before cyanidation to improve leaching kinetics and lower the cyanide consumption - Average production of ~30kozpa Au is expected from the tailings retreatment project ▪ Other operations that treat similar surface stockpiles incorporate a grinding step prior to pre - oxidation and leaching - Lower grade does not warrant the additional expensive grinding step improving cost efficiencies and expected profitability Planned Gauta Processing Flow Sheet SMBS Cyanide Oxygen Lime Trash Removal Feed Thickening Pre - Oxidation Carbon - in - Leach Detox Tailings Thickening Process Water Storage Acid Wash Elution Electrowinning Smelting Carbon Regeneration Water HCI Fresh Carbon Caustic Doré Old TSF New TSF Reclaimed Tailings Stripped Carbon Loaded Carbon Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. 31

Gauta Tailings Retreatment Plant and Method Source: Company information Note: (1) Illustrations from other similar existing tailings retreatment operations on the Witwatersrand Basin. Gauta Tailings Retreatment Plant Three Dimensional Overview High Pressure Water Monitoring Anticipated Method on TSFs (1) 32

S - K 1300 Project Economics Highly Attractive Economic Profile for Blyvoor & Gauta Source: S - K 1300 Technical Reports on the Blyvoor Gold Mine and Gauta Tailings, with an effective date of February 29, 2024. Notes: Financials shown on fiscal year basis. Fiscal year ending 28 Feb. (1) Long - term gold price of US$1,900/oz. (2) Historic TSF’s are not defined as a mineral resource in the MPRDA and hence the gold produced from these is not subject to the provisions of the Royalty Act. (3) Non - IFRS measure, which should not be considered in isolation or as substitute to IFRS measures. Please refer to section “Non - IFRS Disclosure” on page 36. Blyvoor Gold Mine Cash Flow Projections as per S - K 1300 Technical Reports Mine Value (1) NPV (US$m,100% Basis) Discount Rate 1,275 5% ▪ NPV derived from post government royalties and tax, pre - debt real cash flows, and macro - economic projections ▪ Incorporates gold royalty held by Sandstorm ▪ Corporate tax ~29 - 31% with capital expenditure relief ▪ Includes government royalty Gauta Gold Project Tailings Value (1) NPV (US$m) Discount Rate 115 5% ▪ NPV derived from post tax, pre - debt real cash flows, and macro - economic projections ▪ Average tax rate ~29 - 31% with capital expenditure relief ▪ Excludes government royalty (2) US$m Tailings pre - production capital of ~US$94m consists of ~US$72m plant infrastructure costs, ~US$20m mining costs and ~US$2m spent on other infrastructure spend US$m 160 140 120 100 80 60 40 20 0 - 20 - 40 Y1 Y4 Y7 Y28 Y31 Y34 FCF (US$m) Y10 Y13 Y16 Y19 Y22 Y25 Capex (USm) 200 175 150 125 100 75 50 25 0 (25) (50) (75) (100) Y2 Y4 Y6 Y8 Y10 Y12 Y14 Y16 Y18 Cumulative FCF (US$m) FCF (US$m) Capex (USm) (3) 33 (3)