As filed with the Securities and Exchange Commission on December 29, 2023.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Lafayette Energy Corp

(Exact Name of Registrant as Specified in Its Charter)

Delaware

1311

88-1178200

(State or Other Jurisdiction of

Incorporation or Organization)

(Primary Standard Industrial

Classification Code Number)

(I.R.S. Employer

Identification Number)

3450 N. Triumph Blvd., Suite 102,

Lehi, Utah 84043

(303) 625 6709

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Mr. Michael L. Peterson, Chief Executive Officer

3450 N. Triumph Blvd., Suite 102,

Lehi, Utah 84043

(303) 625 6709

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

David M. Loev, Esq.

Ross D. Carmel, Esq.

John S. Gillies, Esq.

Barry P. Biggar, Esq.

The Loev Law Firm, PC

Sichenzia Ross Ference Carmel LLP

6300 West Loop South

1185 Avenue of the Americas, 31st floor

Suite 280

New York, New York 10036

Bellaire, Texas 77401

Telephone: (212) 930-9700

Telephone: (713) 524-4110

rcarmel@srfc.law

dloev@loevlaw.com

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer

☐

Accelerated filer

☐

Non-accelerated filer

☒

Smaller reporting company

☒

Emerging growth company

☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This Registration Statement contains two prospectuses, as set forth below.

·

Public Offering Prospectus. A prospectus to be used for the public offering of 1,200,000 shares of common stock of the registrant (not including shares of common stock issuable upon exercise of the underwriter’s over-allotment option) (the “Public Offering Prospectus”) through the underwriter named on the cover page of the Public Offering Prospectus.

·

Resale Prospectus. A prospectus to be used for the resale by the selling stockholders set forth therein of 3,152,220 shares of common stock of the registrant (the “Resale Prospectus”).

The Resale Prospectus is substantially identical to the Public Offering Prospectus, except for the following principal points:

·

they contain different front cover pages and back cover pages;

·

all references in the Public Offering Prospectus to “this offering” or “this initial public offering” will be changed to “our initial public offering” and/or “the IPO,” defined as the underwritten initial public offering of our common stock, in the Resale Prospectus;

·

all references in the Public Offering Prospectus to “underwriter” will be changed to “underwriter of the IPO” in the Resale Prospectus;

·

they contain different “The Offering” sections;

·

the number of issued and outstanding shares disclosed throughout the Resale Prospectus and the percentage ownership held by certain stockholders disclosed throughout the Resale Prospectus, will be updated to the total the number of issued and outstanding shares of common stock of the Company and applicable percentages of total outstanding shares held, immediately following the completion of the IPO;

·

the Resale Prospectus includes a separate “Private Placement Offerings” section;

·

the section “Shares Eligible For Future Sale—Selling Stockholder Resale Prospectus” from the Public Offering Prospectus is deleted from the Resale Prospectus;

·

the “Underwriting” section from the Public Offering Prospectus is deleted from the Resale Prospectus and a “Plan of Distribution” section is inserted in its place;

·

the “Capitalization” and “Dilution” sections are deleted from the Resale Prospectus;

·

a “Selling Stockholders” section is included in the Resale Prospectus; and

·

the “Legal Matters” section in the Resale Prospectus deletes the reference to counsel for the underwriter.

The registrant has included in this registration statement a set of alternate pages after the outside back cover page of the Public Offering Prospectus, which we refer to as the Alternate Pages, to reflect the foregoing differences in the Resale Prospectus as compared to the Public Offering Prospectus. The Public Offering Prospectus will exclude the Alternate Pages and will be used for the public offering by the registrant. The Resale Prospectus will be substantially identical to the Public Offering Prospectus except for the addition or substitution of the Alternate Pages and will be used for the resale offering by the selling stockholders (it being understood that none of the shares being registered for resale by the selling stockholders in the Resale Prospectus may be sold prior to the closing of our initial public offering under the Public Offering Prospectus, and only then in compliance with applicable laws, rules and regulations).

i

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities nor may we accept offers to buy these securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

SUBJECT TO COMPLETION, DATED DECEMBER 29, 2023

1,200,000 shares

Lafayette Energy Corp

Common Stock

This is a firm commitment initial public offering of shares of common stock of Lafayette Energy Corp.

Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price per share will be between $4.00 and $5.00. We intend to list the common stock for trading on The Nasdaq Capital Market under the symbol “LEC.” If our common stock is not approved for listing on The Nasdaq Capital Market, we will not consummate this offering.

At the same time as the offering set forth in this prospectus (the “Public Offering Prospectus”), we are registering the resale of 3,152,220 shares of common stock, the prospectus of which was filed as part of the same registration statement of which this prospectus forms a part (the “Resale Prospectus”).

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, and, as such, may elect to comply with certain reduced public company reporting requirements for future filings. This prospectus complies with the requirements that apply to an issuer that is an emerging growth company.

Per Share

Total

Initial public offering price

$

$

Underwriting discounts and commissions(1)

$

$

Proceeds to us, before expenses

$

$

(1)

Please refer to the section entitled “Underwriting” for additional information regarding total underwriter compensation. We have agreed to pay the underwriter a non-accountable expense allowance equal to 1% of gross proceeds and reimburse the underwriter for its reasonable out-of-pocket expenses, including legal fees, up to $125,000.

We have granted the underwriter an option for a period of 45 days after the date of this prospectus to purchase up to 15% of the total number of our shares of common stock to be offered by us pursuant to this offering (excluding shares of common stock subject to this option), solely for the purpose of covering over-allotments, at the initial public offering price less the underwriting discounts and commissions.

An investment in our common stock involves a high degree of risk. You should carefully consider the risk factors set forth under “Risk Factors,” beginning on page 29 of this prospectus before you make your decision to invest in our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The Underwriter expects to deliver the shares of common stock against payment as set forth under “Underwriting,” on or about ___________, 2023.

Through and including ___________, 2024 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

No dealer, salesperson or other individual has been authorized to give any information or to make any representation other than those contained in this prospectus in connection with the offer made by this prospectus and, if given or made, such information or representations must not be relied upon as having been authorized by us. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which such an offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so, or to any person to whom it is unlawful to make such offer or solicitation. Neither the delivery of this prospectus nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in our affairs or that information contained herein is correct as of any time subsequent to the date hereof.

The following are abbreviations, acronyms and definitions of certain terms used in this document, which are commonly used in our industry:

2-D seismic. The method by which a cross-section of the earth’s subsurface is created through the interpretation of reflecting seismic data collected along a single source profile.

3-D seismic. The method by which a three-dimensional image of the earth’s subsurface is created through the interpretation of reflection seismic data collected over a surface grid. 3-D seismic surveys allow for a more detailed understanding of the subsurface than do 2-D seismic surveys and contribute significantly to field appraisal, exploitation, and production.

AFE or Authorization for Expenditures. A document that lays out proposed expenses for a particular project and authorizes an individual or group to spend a certain amount of money for that project.

ARO. Asset retirement obligation, which is a legal obligation associated with the retirement of an oil or gas well, where the owner is responsible for removing equipment, plugging the well and/or cleaning up hazardous materials at some future date.

Bbl. One stock tank barrel, or 42 U.S. gallons liquid volume, used in this Annual Report in reference to crude oil or other liquid hydrocarbons.

Bcf. An abbreviation for billion cubic feet. Unit used to measure large quantities of gas, approximately equal to 1 trillion Btu.

Bitumen. Is an immensely viscous constituent of petroleum. Depending on its exact composition it can be a sticky, black liquid or an apparently solid mass that behaves as a liquid over very large time scales. Bitumen is defined by the U.S. Geological Survey as an extra-heavy oil with an API gravity less than 10° and a viscosity greater than 10,000 centipoise. At the temperatures normally encountered in natural deposits, bitumen will not flow; in order to be moved through a pipe, it must be heated and, in some cases, diluted with a lighter oil.

Boe. Barrels of oil equivalent, determined using the ratio of one Bbl of crude oil, condensate or natural gas liquids, to six Mcf of natural gas.

Boepd. Barrels of oil equivalent per day.

Bopd. Barrels of oil per day.

Btu or British thermal unit. The quantity of heat required to raise the temperature of one pound of water by one degree Fahrenheit.

Completion. The operations required to establish production of oil or natural gas from a wellbore, usually involving perforations, stimulation and/or installation of permanent equipment in the well or, in the case of a dry hole, the reporting of abandonment to the appropriate agency.

Condensate. Liquid hydrocarbons associated with the production of a primarily natural gas reserve.

Conventional resources. Natural gas or oil that is produced by a well drilled into a geologic formation in which the reservoir and fluid characteristics permit the natural gas or oil to readily flow to the wellbore.

Cushing/WTI. Means the price of West Texas Intermediate oil at the hub located in Cushing, Oklahoma.

Developed acreage. The number of acres that are allocated or assignable to productive wells.

Developed oil and natural gas reserves. Reserves of any category that can be expected to be recovered (i) through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well and (ii) through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well.

Development well. A well drilled into a proved oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

Electric submersible pump or ESP. Is an artificial-lift method for lifting moderate to high volumes of fluids from wellbores.

Estimated ultimate recovery or EUR. Estimated ultimate recovery is the sum of reserves remaining as of a given date and cumulative production as of that date.

Exploratory well. A well drilled to find and produce oil or natural gas reserves not classified as proved, to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir or to extend a known reservoir.

Frac or fracking. A short name for hydraulic fracturing, a method for extracting oil and natural gas.

Farmin or farmout. An agreement under which the owner of a working interest in an oil or natural gas lease assigns the working interest or a portion of the working interest to another party who desires to drill on the leased acreage. Generally, the assignee is required to drill one or more wells in order to earn its interest in the acreage. The assignor usually retains a royalty or reversionary interest in the lease. The interest received by an assignee is a “farmin” while the interest transferred by the assignor is a “farmout.”

FERC. Federal Energy Regulatory Commission.

Field. An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition.

GHG. Greenhouse gases, which are gases that absorb and emit radiant energy within the thermal infrared range, causing the greenhouse effect.

Gross acres or gross wells. The total acres or wells in which a working interest is owned.

Henry Hub. A natural gas pipeline located in Erath, Louisiana that serves as the official delivery location for futures contracts on the NYMEX. The settlement prices at the Henry Hub are used as benchmarks for the entire North American natural gas market.

Held by production. An oil and natural gas property under lease in which the lease continues to be in force after the primary term of the lease in accordance with its terms as a result of production from the property.

Horizontal drilling or well. A drilling operation in which a portion of the well is drilled horizontally within a productive or potentially productive formation. This operation typically yields a horizontal well that has the ability to produce higher volumes than a vertical well drilled in the same formation. A horizontal well is designed to replace multiple vertical wells, resulting in lower capital expenditures for draining like acreage and limiting surface disruption.

Hydraulic Fracturing. Means the forcing open of fissures in subterranean rocks by introducing liquid at high pressure, especially to extract oil or gas.

Initial Development Opportunities. Means the development of the Asphalt Ridge Option assets.

IP30. Means the production of a well for the first full calendar month of production.

Liquids. Liquids, or natural gas liquids, are marketable liquid products including ethane, propane, butane, and pentane resulting from the further processing of liquefiable hydrocarbons separated from raw natural gas by a natural gas processing facility.

LOE or Lease operating expenses. The costs of maintaining and operating property and equipment on a producing oil and gas lease.

MBbl or MBbls. One thousand barrels of crude oil or other liquid hydrocarbons.

MBbl/d. One thousand barrels of crude oil or other liquid hydrocarbons per day.

MBoe. Thousand barrels of oil equivalent.

MBoe/d. Thousand barrels of oil equivalent per day.

Mcf. One thousand cubic feet of natural gas.

Mcfgpd. Thousands of cubic feet of natural gas per day.

MMcf. One million cubic feet of natural gas.

MMBtu. One million British thermal units.

MMBoe. Million barrels of oil equivalent.

Net acres or net wells. The sum of the fractional working interest owned in gross acres or wells.

Net revenue interest. The interest that defines the percentage of revenue that an owner of a well receives from the sale of oil, natural gas and/or natural gas liquids that are produced from the well.

NGL. Natural gas liquids.

NYMEX. New York Mercantile Exchange.

Permeability. A reference to the ability of oil and/or natural gas to flow through a reservoir.

Petrophysical analysis. The interpretation of well log measurements, obtained from a string of electronic tools inserted into the borehole, and from core measurements, in which rock samples are retrieved from the subsurface, then combining these measurements with other relevant geological and geophysical information to describe the reservoir rock properties.

Play. A set of known or postulated oil and/or natural gas accumulations sharing similar geologic, geographic, and temporal properties, such as source rock, migration pathways, timing, trapping mechanism and hydrocarbon type.

Plugging and abandonment. Refers to the sealing off of fluids in the strata penetrated by a well so that the fluids from one stratum will not escape into another or to the surface. State regulations require generally plugging of abandoned wells.

Possible reserves. Additional reserves that are less certain to be recognized than probable reserves.

Present value of future net revenues (“PV-10”). The present value of estimated future revenues to be generated from the production of proved reserves, before income taxes, calculated in accordance with SEC guidelines, net of estimated production and future development costs, using prices and costs as of the date of estimation without future escalation and without giving effect to hedging activities, non-property related expenses such as general and administrative expenses, debt service and depreciation, depletion and amortization. PV-10 is calculated using an annual discount rate of 10%.

Probable reserves. Additional reserves that are less certain to be recognized than proved reserves but which, in sum with proved reserves, are as likely as not to be recovered.

Producing well, production well or productive well. A well that is found to be capable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of the well’s production exceed production-related expenses and taxes.

Production costs. Costs incurred to operate and maintain wells and related equipment and facilities, including depreciation and applicable operating costs of support equipment and facilities and other costs of operating and maintaining those wells and related equipment and facilities that become part of the cost of oil, natural gas and NGL produced.

Properties. Natural gas and oil wells, production and related equipment and facilities and natural gas, oil or other mineral fee, leasehold, and related interests.

Prospect. A specific geographic area which, based on supporting geological, geophysical, or other data and also preliminary economic analysis using reasonably anticipated prices and costs, is considered to have potential for the discovery of commercial hydrocarbons.

Proved developed reserves. Proved reserves that can be expected to be recovered through existing wells and facilities and by existing operating methods.

Proved reserves. Reserves of oil and natural gas that have been proved to a high degree of certainty by analysis of the producing history of a reservoir and/or by volumetric analysis of adequate geological and engineering data.

Proved undeveloped reserves or PUDs. Proved reserves that are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion.

Repeatability. The potential ability to drill multiple wells within a prospect or trend.

Reserves. Estimated remaining quantities of oil, natural gas and NGL and related substances anticipated to be economically producible by application of development projects to known accumulations. In addition, there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil, natural gas and NGL or related substances to market, and all permits and financing required to implement the project. Reserves should not be assigned to adjacent reservoirs isolated by major, potentially sealing, faults until those reservoirs are penetrated and evaluated as economically producible. Reserves should not be assigned to areas that are clearly separated from a known accumulation by a non-productive reservoir (i.e., absence of reservoir, structurally low reservoir, or negative test results). Such areas may contain prospective resources (i.e., potentially recoverable resources from undiscovered accumulations).

Reservoir. A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

Royalty interest. An interest in an oil and natural gas lease that gives the owner of the interest the right to receive a portion of the production from the leased acreage (or of the proceeds of the sale thereof), but generally does not require the owner to pay any portion of the costs of drilling or operating the wells on the leased acreage. Royalties may be either landowner’s royalties, which are reserved by the owner of the leased acreage at the time the lease is granted, or overriding royalties, which are usually reserved by an owner of the leasehold in connection with a transfer to a subsequent owner.

Salt Water Disposal Well or SWD. A salt water disposal (SWD) well is a disposal site for water produced as a result of the oil and gas extraction process.

Spud. Spudding is the process of beginning to drill a well in the oil and gas industry.

Standardized measure or standardized measure of discounted future net cash flows. The present value of estimated future cash inflows from proved oil, natural gas and NGL reserves, less future development and production costs and future income tax expenses, discounted at 10% per annum to reflect timing of future cash flows and using the same pricing assumptions as were used to calculate PV-10. Standardized Measure differs from PV-10 because standardized measure includes the effect of future income taxes on future net revenues.

Step-out well. A well drilled near a proven well, but located in an unproven area, that determines the boundaries of the producing formation.

Transition Zone. The Transition Zone usually produces both oil and water at different ratios depending on the height above the Free Water Level (“FWL”). In normal conditions wells that are drilled in the Transition Zone will produce at some water cut.

Trend. A region of oil and/or natural gas production, the geographic limits of which have not been fully defined, having geological characteristics that have been ascertained through supporting geological, geophysical, or other data to contain the potential for oil and/or natural gas reserves in a particular formation or series of formations.

Unconventional resource play. A set of known or postulated oil and or natural gas resources or reserves warranting further exploration which are extracted from (a) low-permeability sandstone and shale formations and (b) coalbed methane. These plays require the application of advanced technology to extract the oil and natural gas resources.

Undeveloped acreage. Lease acreage on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil and natural gas, regardless of whether such acreage contains proved reserves. Undeveloped acreage is usually considered to be all acreage that is not allocated or assignable to productive wells.

Unproved and unevaluated properties. Refers to properties where no drilling or other actions have been undertaken that permit such property to be classified as proved.

Updip well. A well located higher in the structure.

USACE. United States Army Corps of Engineers.

Vertical well. A hole drilled vertically into the earth from which oil, natural gas or water flows is pumped.

Volumetric reserve analysis. A technique used to estimate the amount of recoverable oil and natural gas. It involves calculating the volume of reservoir rock and adjusting that volume for the rock porosity, hydrocarbon saturation, formation volume factor and recovery factor.

Wellbore. The hole made by a well.

WTI or West Texas Intermediate. A grade of crude oil used as a benchmark in oil pricing. This grade is described as light because of its relatively low density, and sweet because of its low sulfur content.

Working interest. The operating interest that gives the owner the right to drill, produce and conduct operating activities on the property and receive a share of production.

No dealer, salesperson or other individual has been authorized to give any information or to make any representation other than those contained in this prospectus in connection with the offer made by this prospectus and, if given or made, such information or representations must not be relied upon as having been authorized by us. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which such an offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so, or to any person to whom it is unlawful to make such offer or solicitation. Neither the delivery of this prospectus nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in our affairs or that information contained herein is correct as of any time subsequent to the date hereof.

For investors outside the United States: We and the underwriter have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves, and observe any restrictions relating to, the offering of the shares of our common stock and the distribution of this prospectus outside the United States.

Our logo and some of our trademarks and tradenames are used in this prospectus. This prospectus also includes trademarks, tradenames and service marks that are the property of others. Solely for convenience, trademarks, tradenames, and service marks referred to in this prospectus may appear without the ®, ™ and SM symbols. References to our trademarks, tradenames and service marks are not intended to indicate in any way that we will not assert to the fullest extent under applicable law our rights or the rights of the applicable licensors if any, nor that respective owners to other intellectual property rights will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend the use or display of other companies’ trademarks and trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, reports by market research firms or other independent sources that we believe to be reliable sources; however, we have not commissioned any of the market or survey data that is presented in this prospectus. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. We are responsible for all of the disclosures contained in this prospectus, and we believe these industry publications and third-party research, surveys and studies are reliable. While we are not aware of any misstatements regarding any third-party information presented in this prospectus, their estimates, in particular, as they relate to projections, involve numerous assumptions, are subject to risks and uncertainties, and are subject to change based on various factors, including those discussed under the section entitled “Risk Factors” beginning on page 29 of this prospectus. These and other factors could cause our future performance to differ materially from our assumptions and estimates. Some market and other data included herein, as well as the data of competitors as they relate to Lafayette Energy Corp, is also based on our good faith estimates.

Unless the context otherwise requires, references in this prospectus to “we,” “us,” “our,” the “Registrant”, the “Company,” “Lafayette” and “Lafayette Energy Corp” refer to Lafayette Energy Corp

In addition:

●

“Exchange Act” refers to the Securities Exchange Act of 1934, as amended;

●

“Nasdaq” means the Nasdaq Capital Market;

●

“SEC” or the “Commission” refers to the United States Securities and Exchange Commission; and

●

“Securities Act” refers to the Securities Act of 1933, as amended.

Effective on January 24, 2023, our Board of Directors, and on January 26, 2023, stockholders holding a majority of our outstanding voting shares, approved resolutions approving and authorizing the filing of a Second Amended and Restated Certificate of Incorporation of the Company, which affected a two-for-three reverse stock split of the outstanding shares of our common stock (the “Reverse Stock Split”), without any corresponding change in the number of authorized shares of common stock of the Company. On January 31, 2023, the Second Amended and Restated Certificate of Incorporation of the Company was filed with the Secretary of Delaware, and at the same time, the Reverse Stock Split became effective. Except as otherwise indicated and except in our financial statements and the notes thereto, all references to our common stock, share data, per share data and related information retroactively depict and reflect the Reverse Stock Split. The Reverse Stock Split combined each three shares of our outstanding common stock into two shares of common stock, without any change in the par value per share, and the Reverse Stock Split correspondingly adjusted, among other things, the number of shares of common stock available for awards under our equity compensation plans. No fractional shares were issued in connection with the Reverse Stock Split, and any fractional shares resulting from the Reverse Stock Split were rounded up to the nearest whole share on a per stockholder basis.

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before deciding to invest in our common stock. You should read this entire prospectus carefully, including the “Risk Factors” section, our historical financial statements, and the notes thereto, each included elsewhere in this prospectus.

Overview

We are an oil and gas exploration and production company headquartered in Lehi, Utah. The Company was incorporated on February 7, 2022 under the laws of Delaware, with the goal of acquiring, funding and developing, primarily natural gas exploration and development. The Company plans to initially focus its attention on certain oil and gas assets located in Eastern Utah, pursuant to the Asphalt Ridge Option (defined and discussed below), and use anticipated cash flow from those operations to fund development of the Imperial Parish Fields (defined and discussed below). We currently hold options to lease an additional approximately 960 acres in the Uinta Basin, Utah and options to purchase leases covering approximately 1,487 gross mineral acres in Imperial Parish, Louisiana, and options. We have no revenue-generating operations as of the date of this prospectus and will need to raise funding to exercise our lease options and complete successful oil and gas exploration and development activities before we can generate revenues.

Asphalt Ridge Option (Utah)

On November 13, 2023, the Company entered into a Leasehold Acquisition and Development Option Agreement (the “Asphalt Ridge Option Agreement”) with Heavy Sweet Oil, LLC (“Heavy Sweet”). Pursuant to the Asphalt Ridge Option Agreement, we purchased an option to acquire up to a 30% production share in certain leases in long-developed oil and gas area of eastern Utah, southwest of Vernal, Utah, totaling 960 acres. Heavy Sweet holds the right to such leases below 500 ft depth from surface (the “Asphalt Ridge Leases”) and we have the option to participate in Heavy Sweet’s initial 960 acre drilling and production program on such Asphalt Ridge Leases (the “Asphalt Ridge Option”).

The Asphalt Ridge Option has a term of nine months, through June 28, 2024. Pursuant to the Asphalt Ridge Option, we have the exclusive right, but not the obligation, to acquire up to a 30% interest in the Asphalt Ridge Leases for $3,000,000, which may be invested in tranches, provided that the initial tranche closing occurs during the Asphalt Ridge Option period and subsequent tranches occurring as soon thereafter as practical, with each tranche providing the Company a portion of the ownership of the Asphalt Ridge Leases equal to 30% multiplied by a fraction, the numerator of which is the total consideration paid by the Company, and denominator of which is $3,000,000. Upon receipt of any funding from the Company pursuant to the Asphalt Ridge Option, Heavy Sweet is required to pay that amount to the named operator of the properties, to pay for engineering, procurement, operations, sales, and logistics activities on the properties. The Asphalt Ridge Option Agreement provides that additional development capital is expected to be secured by Heavy Sweet, and made available for the Company’s participation, by way of a reserve base lending facility (RBL), provided that if such RBL cannot be obtained or does not cover all subsequent capital costs, Heavy Sweet agreed to fund a maximum of $5,000,000 of the first funding required for the development program, with the parties splitting any costs thereafter according to their ownership interests. The initial target is three wells, with an estimated cost of $5,000,000 for roads, pads, drilling, and above ground steam and storage facilities, and thereafter the parties anticipate working together to fund further well development based on their proportionate ownership thereof.

As consideration for agreeing to the Asphalt Ridge Option, we issued Heavy Sweet 2,688,000 shares of the Company’s restricted common stock, equal to approximately 19.9% of the Company’s then-issued and outstanding shares of common stock (the “Option Shares”). The Option Shares are subject to the terms of a Restricted Stock Agreement and provide that in the event (i) the Company does not fund the Asphalt Ridge Option by November 13, 2024, or (ii) the Asphalt Ridge Option is funded by November 13, 2024, but the leases fail to achieve a 30-day average net production rate of at least 200 barrels per day in post-development operations as set forth in the development plan, by November 13, 2025, the Option Shares will be cancelled and forfeited by Heavy Sweet. Until vested in full, the Option Shares are held in escrow by the Company and only released to Heavy Sweet upon vesting. While held in escrow, Heavy Sweet has the right to vote such Option Shares, and the right to any cash dividends which are paid on such Option Shares, but does not have the right to transfer such Option Shares until vested.

On or around the date the parties entered into the Asphalt Ridge Option Agreement, Heavy Sweet entered into a Leasehold Acquisition and Development Option Agreement with Trio Petroleum Corp. (“Trio”), of which Michael Peterson, the Chief Executive Officer and director of the Company, is also the Chief Executive Officer and director, and Frank C. Ingriselli, our Chairman, is also the Vice Chairman and director (the “Trio Option”). The Trio Option has similar terms as the Asphalt Ridge Option Agreement, except that it allows Trio to obtain a 20% interest in the Asphalt Ridge Leases, and did not require Trio to pay any equity compensation.

The Parties hereto agree that, to the extent Trio does not fully exercise the Trio Option, the Company has the right to acquire up to all 20% of the right set forth in the Trio Option (or such letter amount which Trio has not exercised), from Heavy Sweet, for $2,000,000 cash.

The exercise of the Asphalt Ridge Option is contingent upon the following: (a) Heavy Sweet providing the Company the statements of revenues and direct operating expenses for the prior two years for the asset and the unaudited stub period for 2023, through the date of closing; (b) satisfactory due diligence review by the Company of Heavy Sweet, the leases, the property and other information; (c) the negotiating of a mutually-acceptable joint operations agreement (“JOA”) or other development and operations agreement(s) as agreed by the parties; and (d) Heavy Sweet providing the Company an updated independent reserves report including proved undeveloped reserves (PUDs) and an estimate of gross valuation and discounted net present values, and indicating best estimate original oil-in-place (OOIP) volumes and gross (100%) contingent oil resources, as of a date no earlier than August 31, 2023, for discoveries located in Northwest Asphalt Ridge, Uinta Basin, Utah.

A Reserve Report covering the Asphalt Ridge Leases was issued by Netherland Sewel to Heavy Sweet on November 17, 2023 (as of October 31, 2023), which estimated total oil resources of 58,390,200 barrels (bbls) of oil, with an estimated total net cash flow of $1.947 billion and a PV(10) discounted cash flow value of $1.027 billion.

Asphalt Ridge Asset

The initial development of the tar-sand assets controlled by Heavy Sweet Oil will be the Asphalt Ridge Asset. The Company would receive a 30% production share, non-operating interest, assuming the Asphalt Ridge Option is exercised.

The location of the Asphalt Ridge Leases is shown in the graphics below:

The graphic below shows proposed drilling locations in the Asphalt Ridge Asset:

Heavy Sweet has identified a minimum 16 standard 40-acre spaced wells and 119 wells on 2.5-acre wells under a unitization agreement. Phase 1 is planned to consist of developing Section 22 and the western half of Section 23 of T4S R20E with development drilling and advanced cyclic steam production techniques planned to exploit the heavy oil resources thought to reside in the Rimrock and Asphalt Ridge sandstone reservoirs.

The Company’s $3 million capital investment, paid upon exercise of the Asphalt Ridge Option, together with the $2 million expected to be funded by Trio, or if not funded by Trio, by the Company by stepping into Trio’s ownership rights, as discussed above, is expected to provide the anticipated costs needed to produce roads, drilling pads, and the cost of drilling and completion of three wells. Thereafter, all additional capital costs are expected to be funded by a reserve base lending facility (RBL) that Heavy Sweet expects to be able to secure based on their previous negotiations though the securing of this RBL is not guaranteed nor in the Company’s control, provided that if such RBL cannot be obtained or does not cover all subsequent capital costs, Heavy Sweet agreed to fund a maximum of $5,000,000 of the first funding required for the development program, with the parties splitting any costs thereafter according to their ownership interests.

According to the website of the American Geological Society, the largest tar sand deposits of in the world are found in Alberta (Canada) and Venezuela. However, according to Utah Geological Society (“UGS”), Utah’s measured tar sand resource is the largest in the United States (Energy News: Taking Another Look at Utah’s Tar Sand Resources, J. Wallace Gwynn (2007) Survey Notes, v. 39 no. 1, January 2007). The UGS estimates that Utah’s tar sand deposits contain between 14 to 15 billion barrels of measured in-place oil, with an additional estimated resource of 23 to 28 billion barrels. Analysis of bitumen extracted from samples show that bitumen is low-sulfur and high-gravity.

The UGS (Tar-Sand Resources of the Uinta Basis, Utah, Catalog of Deposits, compiled by Robert E. Blackett, dated May 1996), reported that three independent reserve analyses of the Asphalt Ridge formation made in 1930, 1966, and 1979, estimated that the formation contained proven reserves of nearly 900 million barrels, 700 million barrels, and 1,048 million barrels of bitumen, respectively.

While these reports and analysis are just projections, we believe they do indicate that there is a high probability of a significant addressable resource tar-sand/oil targeted structure in this area.

Drilling Plan (Utah)

The drilling program is planned to be completed using conventional drilling techniques and followed up with Conventional Steam & CO2 Flood (“Huff and Puff”)(discussed below). These are proven methods used in Utah and worldwide.

“A Review of Steam Soak Operations in California”, Babson and Burns, January 1969.

B)

“Extraction of petroleum”, Wikimedia Foundation, last modified November 4, 2023, 15:05, https://en.wikipedia.org/wiki/Extraction_of_petroleum.

C)

“Huff-n-puff gas injection or gas flooding in tight oil reservoirs”, Journal of Petroleum Science and Engineering, Tang & Sheng, January 2022.

D)

“Quantitative study of C02 huff-n-puff enhanced oil recovery in tight formations using online NMR technology”, Liu, Li, Tan, Liu, Zhao, and Wang, Journal of Petroleum Science and Engineering (July 2022).

Field Geology Description

According to the Tar-Sand Resources of the Unita Basin, Utah, complied by Robert E. Blackett, May 1996, the Asphalt Ridge is situated along the northeast edge of the Unita Basin physiographic subprovince, with the Marginal Benches/Uinta Mountains subprovince of the Middle Rocky Mountains lying less than 10 miles to the north. The Asphalt Ridge forms the southwest limit to the low-lying farm lands of Ashley Valley. The Green River, which flows southwestward through the Uinta Basin, flows through the southeast extension of Asphalt Ridge. The Asphalt Ridge is a northwest-southeast trending cuesta, where Cretasceous and Terriary formations dip to the southwest. Bitumen-saturated outcrops extend for approximately 12 miles northwest-southeast along the strike of the outcrops.

The town of Vernal, Utah is approximately 4 miles to the northeast in the Ashley Valley, where elevations range between 5,200 and 5,500 feet. the Asphalt Ridge rises from 500 to 1,000 feet above Ashley Valley. The highest point on the Asphalt Ridge, located near the northwest end, is approximately 6,400 feet in elevation.

Reserves and Production

A Reserve Report covering the Asphalt Ridge Leases was issued by Netherland Sewel to Heavy Sweet on November 17, 2023 (as of October 31, 2023), which estimated total oil resources of 58,390,200 barrels (bbls) of oil, with an estimated total net cash flow of $1.947 billion and a PV(10) discounted cash flow value of $1.027 billion. The Reserve Report estimates the average per-well gross estimated ultimate recovery (EUR) for the 119 potential locations to be approximately 491 thousand barrels (MBBL) of oil.

Market Opportunity

The Company believes that the Utah Asphalt Ridge Option opportunity provides a very attractive option to participate in a project that, if successful, should provide an attractive cash flow to the Company, beginning six months after successful completion of the first three wells. The project is ready to begin the development phase and we believe the wells could be drilled within a few months. The Company also believes that Utah is a good location for this type of development for many reasons, including existing paths to multiple markets, and attractive Utah State costs and development attributes, especially as compared to other national resource plays. These advantages include low state royalties, low transportation costs, access to rail, low cost of approximately $500,000 to drill and complete wells due to shallow drill depths of approximately 1,200 feet, and favorable state regulations.

We believe that the Asphalt Ridge Asset offers attractive deployment attributes:

·

Low state royalty rate;

·

Low transportation costs;

·

Shallow wells, which result in less costly drilling expenses; and

·

Attractive stimulation costs using steam vs. fracturing processes.

Set forth below is information regarding the average well cost, well depth, state royalty rate, transportation cost and simulation cost for wells drilled in Utah’s Rimrock sandstone, North Dakota’s Bakken Formation and Texas’ Permian Basin.

“Midland County, TX Oil & Gas Activity - MineralAnswers.com”.

c)

“Drillnomics Analysis of the Bakken Shale– Mountrail County, ND”, March 2016 (https://www.drillnomics.com/drillnomics-analysis-of-the-bakken-shale-mountrail-county-nd/).

d)

REPORT ON THE FEDERAL OIL AND GAS LEASING PROGRAM U.S. Department of the Interior November 2021.

e)

Crude oil pipeline constraints: A tale of two shales - ScienceDirect, January 2023.

f)

Who Wins as Oil Price Differentials Widen in the Permian Basin_- TX transportation costs https://finance.yahoo.com/news/wins-oil-price-differentials-widen-204854624.html, June 2018.

The three Asphalt Ridge Option wells are expected to be drilled and completed by Valkor Oil & Gas LLC, a related party to Heavy Sweet, whose principals have extensive experience in oil and gas. The Company anticipates that the drilling will be commenced within the first quarter following the successful closing of this offering.

Planned Development Activities

We currently anticipate the following three stages of development with Stage 1 using anticipated proceeds of this offering and Stages 2 and 3 using anticipated cash flow from our Stage 1 investment.

Stage

Description

Estimated Timing

Estimated Cost*

1

Invest in Initial Development Opportunities that are planned to be drilled within one quarter following the close of this offering

February 2024

$3,000,000

2

Acquire an additional 27,800 of optioned acreage in the Imperial Parish Fields (discussed below)

*We anticipate funding the first stage through cash raised in this offering (See “Use of Proceeds”) and future stages from projected cash flow from operations.

As described above and discussed below, subsequent to investing in the Initial Development Opportunities, we plan to use anticipated cash flow to develop the Imperial Parish Fields asset (discussed below) by first securing rights to perform 3-D seismic imaging and develop up to approximately 30,000 acres in the Imperial Parish Fields, second to perform 3-D seismic imaging on the acreage we successfully option, and then to drill and complete wells in the most prospective areas we have optioned. Through our agreement with Saur Minerals (discussed below), we plan to acquire acreage within the Imperial Parish Fields through options that include (1) the right to perform a 3-D seismic shoot on the property; and (2) an option to purchase a mineral lease with rights to drill oil and gas wells on the property. For most options the Company has paid $12.50 to $25.00 per acre for the seismic right and has entered into an option to pay $75.00 per acre for the mineral and drilling rights for those acres the Company chooses to develop.

On March 8, 2022, the Company entered into a letter agreement (the “Letter Agreement”) with Saur Minerals LLC (“Saur Minerals”) which is based in Lafayette, Louisiana. Saur Minerals is owned and controlled by Louis E. Bernard, Jr. and Michael L. Schilling, Jr., beneficial owners of an aggregate of less than 1% and 10.0% of the Company’s outstanding common stock as of the date of this prospectus, respectively. Pursuant to the Letter Agreement, Saur Minerals caused its affiliated entity, Two Pearl Energy LLC (“Two Pearl”), to assign approximately 1,487 net acres of oil and gas leasehold interests (the “Subject Leases”) and related assets located within St. Landry Parish, Louisiana to the Company in exchange for (a) $300,000 of cash consideration paid by the Company to Saur Minerals on March 8, 2022, (b) $100,000 cash consideration payable by the Company to Saur Minerals within five days after the closing of the acquisition, which amount has been paid in full, and (c) $200,000 of cash consideration payable by the Company to Saur Minerals within thirty days after the closing of the acquisition, which amount has been paid in full. In addition, the parties agreed that Two Pearl would reserve and retain an overriding royalty interest (“ORRI”) with respect to each Subject Lease in a percentage equal to the positive difference between the royalty interest of the lessor under each Subject Lease and 25%, if the lessor reserves a royalty less than 25%, and 2% if the lessor reserves a royalty interest equal to or greater than 25%.

As part of our diligence into the Imperial Parish Fields, the Company evaluated potential target zones and offset well results, and identified potential well locations and produced an estimate (the “Resource Estimate”) of the resource opportunity of the Imperial Parish Fields, noting that “resource” estimates are not consistent with “proved reserves” as defined by the SEC, and that we do not currently have, and may not have in the future, either proved reserves or production of oil or natural gas in commercial quantities or at all. Based on our Resource Estimate, we believe single well economics in the area on which we hold our options would be robust in today’s commodity price environment.

In connection with the closing of the transactions contemplated by the Letter Agreement, the Company and Saur Minerals entered into an Acquisition and Development Agreement, dated March 8, 2022, as amended June 16, 2022 (the “Development Agreement”), pursuant to which Saur Minerals agreed to seek and pursue opportunities to acquire certain interests for the benefit of the Company and subsequently reconveyed to the Company, or directly acquire on behalf of the Company such interests, within St. Landry Parish, Louisiana (the “Development Area”), on an exclusive basis for a term of five years expiring March 8, 2027, subject to extension by the Company for three additional periods of one year each, and subject to satisfaction of certain pre-authorized economic terms, prices and conditions as set forth therein, the acquisition of which interests are to be reimbursed to Saur Minerals, or paid directly, by the Company.

In addition, in connection with the closing of the transactions contemplated by the Letter Agreement, on March 8, 2022, the Company and Saur Minerals entered into a Seismic License Agreement, pursuant to which, Saur Minerals, as licensor of certain seismic data covering the Subject Leases and other mineral interests or leasehold interests within the Development Area, agreed to license such seismic data, on a perpetual, irrevocable, non-exclusive, transferable, sublicensable, royalty-free and fully-paid up basis. The seismic license was granted in connection was the closing of the transactions contemplated under the Letter Agreement, Development Agreement and related transactions, with no additional consideration, royalty or license fee due or owing by the Company to Saur Minerals.

We project that seismic and lease options on an additional 27,800 targeted acres in Phase 1 (the “Targeted Acres”) will cost approximately $860,000, which is anticipated to be funded by a portion of funds raised in this offering or anticipated cash flow from the development of our Asphalt Ridge (see “Use of Proceeds”). Additionally, we plan to use anticipated future cash flow of $1.5 million of the proceeds to prepare a 3-D seismic survey on the optioned acreage in Phase 1 to analyze three targeted zones – the Frio, Cockfield and Sparta zones. These zones have been proven in offset acreage not held by the Company by companies such as Exxon Mobil, Texaco (Chevron USA Inc.), Halbouty Reserve and Hunt Oil Company, and several smaller independents such as Lynal, Inc., Lyons Petroleum, Inc., and others. All national US Army Corp of Engineer permits are in place to shoot 3-D seismic data for our optioned property. The timeline for shooting and analyzing the 3-D data is anticipated to be six months (the “3-D Seismic Phase”), which we anticipate beginning immediately after acquiring the Phase 1 acreage. In tandem during the 3-D Seismic Phase, we plan to put out a request for proposal (a “RFP”) for drilling contracts with locally identified drilling contractors.

The anticipated development plan for the Imperial Parish Fields Asset to the extent deployed, is to first acquire options on the Targeted Acres, then shoot 3-D seismic, and following the interpretation of the 3-D seismic data, and assuming that such 3-D seismic data provides us with reasonable validation of the prospectivity of the acreage, we plan to exercise options we hold to acquire leaseholds we deem most prospective, sign a drilling contract, and then diligently work with our contracted drilling contractor to identify optimal locations for four initial wells (the “Drilling Evaluation Process”). We anticipate each well will require approximately 500 acres to form a drilling unit. Our current options include an option that allows us to lease the acreage for $75 per acre. For acreage not under option, we anticipate a total cost of $115 per acre to source and lease. Therefore, each well would incur acreage leasing costs estimated at between $37,500 to $57,500, with the total estimated acreage leasing cost for the first four wells being between $150,000 and $230,000, which funds for such drilling we anticipate raising through a reserve based lending facility subsequent to this offering, which may not be available on favorable terms, if at all. We will also need to evaluate and source offtake contracts through the Drilling Evaluation Process. We expect the drilling evaluation process to take up to an additional two months following the 3-D Seismic Phase. The goal of these wells will be to prove up all three zones (Frio, Cockfield, and Sparta). Subject to changes in the discretion of management during the Drilling Evaluation Process, we intend to drill our first four wells in the Imperial Parish Fields in the Sparta zone with each well testing the Cockfield and Frio zones. We anticipate that the drilling and completion of the first two wells will take approximately two months to complete with hydrocarbons expected to begin flowing from the initial wells after 10 weeks. The second set of wells is anticipated to take a similar time frame. We intend to use the cash flow generated from the Initial Development Opportunities, if any, and a reserve based lending facility (an “RBL”) which we plan to seek to put into place following this offering, to drill the four wells and subsequent wells in our three year drilling plan, noting that we do not currently have, and may not have in the future, either proved reserves or production of oil or natural gas in commercial quantities or at all. Thus, we expect to have sufficient liquidity to drill further wells out of cash flow and future borrowings. Based on the well results of the first four wells, we plan to drill two additional wells each quarter with the next six wells being called the 2nd Drilling Phase (the “2nd Drilling Phase”). We expect these wells in the 2nd Drilling Phase to be able to be completed with more efficiency and the intention of establishing a type curve that can be replicated throughout the acreage position. We anticipate funds for our 2nd Drilling Phase to be raised through a reserve-based lending facility subsequent to this offering, which may not be available on favorable terms, if at all. Additionally, with the cash flow generated and anticipated borrowing capacity from the first and 2nd Drilling Phase, we may look at further exploration options on our acreage, including the deep and highly prospective Cretaceous formation which has been proved to produce commercial quantities of oil and gas by Freeport-McMoran Oil and Gas LLC, BP plc, and Pennington Oil Co.

Business Strategies

Our primary objective is to exercise our option in the Asphalt Ridge Asset with the proceeds of this offering. We then plan to use anticipated cash flow, if any, from that Asphalt Ridge operation, to acquire the Targeted Acres and develop our optioned acreage in the Imperial Parish Fields and potentially to acquire and develop other opportunities for oil and gas production in south central Louisiana. Our primary focus is first in Utah, and then in Louisiana, but we may also consider appropriately priced out-of-state oil and gas opportunities in the future.

The primary goal of our collective efforts is to grow the Company into a highly profitable, independent oil and gas company.

Competition

There are many large, medium, and small-sized oil and gas companies and third-parties that are our competitors. Some of these competitors have extensive operational histories, experienced oil and gas industry management, profitable operations, and significant reserves and funding resources.

Our ability to acquire properties and to discover reserves in the future will be dependent upon our ability to evaluate and select suitable properties and to consummate transactions in a competitive environment. In addition, because we have fewer financial and human resources than many companies in our industry, we may be at a disadvantage in eventually bidding or consummating transactions.

There is also competition between natural gas producers and other related and unrelated industries. Furthermore, competitive conditions may be substantially affected by energy legislation or regulation enacted by governments of the United States and other jurisdictions. It is not possible to predict the nature of any such legislation or regulation which may ultimately be adopted or its effects upon our future operations. Such laws and regulations may substantially increase the costs of capitalizing on oil and gas opportunities. Our larger competitors may be able to absorb the burden of existing, and any changes to governmental regulations more easily than we can, which would adversely affect our competitive position.

In the Imperial Parish Fields themselves, which currently is our secondary focus, we anticipate intense competition from other operators, especially if our 3-D seismic project identifies highly-prospective resources and we obtain and publicly disclose (as is our intention) an independent petroleum engineer reserves report detailing reserves in the area. Obtaining mineral leases in order to control development is an integral part of our strategy.

Our larger competitors may be able to absorb the existing and evolved laws and regulations more easily than we can, which would adversely affect our competitiveness. Our ability to acquire properties and to discover reserves in the future will be dependent upon our ability to evaluate and select suitable properties and to consummate transactions in a competitive environment. In addition, because we have fewer financial and human resources than many companies in our industry, we may be at a disadvantage in eventually bidding or consummating transactions.

Government Regulation

We are subject to a number of federal, state, county and local laws, regulations and other requirements relating to oil and natural gas operations. The laws and regulations that affect the oil and natural gas industry are under constant review for amendment or expansion. Some of these laws, regulations and requirements result in challenges, delays and/or obstacles in obtaining permits, and some carry substantial penalties for failure to comply. The regulatory burden on the oil and natural gas industry increases our cost of doing business, can affect and even obstruct our operations and, consequently, can affect our revenues and future ability to become profitable.

Pre-IPO Private Placement Financing

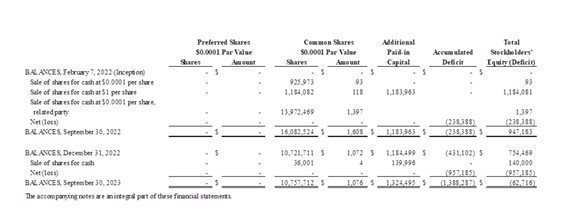

From March to May 2022, we sold an aggregate of 9,562,660 shares of restricted common stock in private transactions to 11 accredited investors, including to Frank C. Ingriselli (880,000 shares)(our Chairman); Graham Patterson (our then Chief Financial Officer)(500,000 shares, of which 100,000 shares were subsequently transferred to Gregory L. Overholtzer, our current Chief Financial Officer and Secretary for no consideration); Louis E. Bernard, Jr. (the Managing Member of Project Operations of Saur Minerals) (1,360,000 shares, of which 680,000 were subsequently transferred to Saur Minerals, LLC, and 633,333 shares were subsequently sold to four other unaffiliated investors); Michael L. Peterson (1,000,000 shares)(our Chief Executive Officer and Secretary); Michael Schilling (1,360,000 shares)(the President of Land/Legal of Saur Minerals); Adrian Beeston (1,483,334 shares, of which 133,334 shares were subsequently sold to Michael L. Peterson, our Chief Executive Officer and President, 66,667 shares were subsequently sold to an entity minority owned by Mr. Beeston, and 100,000 shares were subsequently sold to an unaffiliated investor ); and Naia Ventures, LLC (1,200,000 shares, of which 100,000 shares were subsequently sold to a third party around the time of the third party’s subscription for shares of the Company), for $0.00015 per share or $1,439 in aggregate.

From May to September 2022, we sold an aggregate of 789,386 shares of restricted common stock to 44 accredited investors for $1.50 per share, or $1,184,079 in aggregate. All but eight of those investors (36 in total), were also offered the right, at the same time, to subscribe for additional shares of common stock at $0.00015 per share, and an additional 12 investors were also offered the right to subscribe for shares of common stock at $0.0015 per share, and in total we sold 337,990 shares of restricted common stock to 51 accredited investors for an aggregate of $50.70.

In January 2023, we sold an aggregate of 32,001 shares of restricted common stock to four accredited investors for $3.75 per share, or $120,000 in aggregate. At or around the same time as the sales were completed, one of our founders and one of our affiliates, Louis E. Bernard, Jr. and Saur Minerals, LLC, respectively, sold the purchasers and three other accredited investors, in a separate private transaction, an aggregate of 683,336 shares of our restricted common stock (Louis E. Bernard, Jr. (133,334 shares) and Saur Minerals, LLC (550,002 shares)), for $0.30 per share.

On February 13, 2023, our then Chief Financial Officer, Graham Patterson gifted 100,000 shares of common stock to our current Chief Financial Officer, Gregory L. Overholtzer, for no consideration.

In August 2023, we sold an aggregate of 4,000 shares of restricted common stock to an accredited investor, Adrian Beeston, for $5.00 per share or $20,000 in aggregate.

In November 2023, we sold 16,667 shares of restricted common stock to an accredited investor, for $3.00 per share, or $50,000 in aggregate. At or around the same time as the sale was completed, one of greater than 5% stockholders, Naia Ventures LLC, sold the purchaser (the Sandhya Ajjarapu revocable Trust dtd 2007), in a separate private transaction, an aggregate of 100,000 shares of our restricted common stock, for $10.

In total, from all of the private offerings described above we raised an aggregate of $1,375,511.

Selected Risks Associated with Our Company

Our business is subject to numerous risks and uncertainties, including those in the section entitled “Risk Factors” and elsewhere in this prospectus. These risks include, but are not limited to, the following:

Risks Related to our Operating History and Need for Funding

·

The fact that we have a limited operating history and have not generated any operating revenues to date and our ability to generate revenues and/or achieve profitability, our need for additional funding and the availability and terms of such funding;

·

Our ability to execute our growth strategy and scale our operations and risks associated with such growth;

·

Our need to raise additional funding to complete planned drilling and the terms of such funding, if any;

Risks Related to The U.S. and Global Economy

·

Current and future declines in economic activity and recessions, and their effect on the Company, its property, prospects and the supply and demand, and ultimate price of oil and natural gas;

·

Risks associated with inflation, recessions, and increases in interest rates;

Risks Related to the Oil, NGL and Natural Gas Industry and Our Business

·

The future price of oil, natural gas and NGL;

·

The status and availability of oil and natural gas gathering, transportation, and storage facilities owned and operated by third parties;

An increase in the differential between the NYMEX or other benchmark prices of oil and natural gas and the wellhead price we receive for our production may adversely affect our business, financial condition, and results of operations;

·

The impact of a decline in global oil and natural gas prices for an extended period of time;

·

Our ability to generate sufficient cash flow to meet any future debt service and other obligations due to events beyond our control;

·

The fact that to date we only hold options to acquire drilling and mineral rights and have not to date acquired any drilling and mineral rights, the acquisition of which will require significant additional capital;

·

The fact that all our assets and operations are located in Utah and the Saint Landry Parish located in south central Louisiana, making us vulnerable to risks associated with operating in only two geographic areas;

·

The speculative nature of our oil and gas operations, and general risks associated with the exploration for, and production of oil and gas; including accidents, equipment failures or mechanical problems which may occur while drilling or completing wells or in production activities; operational hazards and unforeseen interruptions for which we may not be adequately insured; the threat and impact of terrorist attacks, cyber-attacks or similar hostilities; declining reserves and production; and losses or costs we may incur as a result of title deficiencies or environmental issues in the properties in which we invest, any one of which may adversely impact our operations;

·

Intense competition in the oil and natural gas industry;

·

Our competitors use of superior technology and data resources that we may be unable to afford or obtain the use of;

·

Uncertainties associated with enhanced recovery methods which may result in us not realizing an acceptable return on our investments in such projects or suffering losses;

·

Requirements that we must drill on certain of acreage in order to hold such acreage by production;

��

·

Improvements in or new discoveries of alternative energy technologies that could have a material adverse effect on our financial condition and results of operations;

·

Future litigation or governmental proceedings which could result in material adverse consequences, including judgments or settlements;

·

Future material impairments of our oil and gas assets;

Risks Related to Management, Employees and Directors

·

Our dependence on the continued involvement of our present management;

·

Potential conflicts of interest that could arise for certain members of our management team and board of directors;

Our ability to comply with government regulations, changing regulations and laws, penalties associated with any non-compliance (inadvertent or otherwise), the effect of new laws or regulations, and our ability to comply with such new laws or regulations;

Risks Associated with Our Governing Documents and Delaware Law

·

Certain terms and provisions of our governing documents which may prevent a change of control, and which provide for indemnification of officers and directors, limit the liability of officers or directors, and provide for the board of director’s ability to issue blank check preferred stock;

Risks Related to Our Common stock and this Offering

·

The fact that certain recent initial public offerings of companies with public floats comparable to the anticipated public float of the Company have experienced extreme volatility that was seemingly unrelated to the underlying performance of the respective company; and the fact that we may experience similar volatility, which may make it difficult for prospective investors to assess the value of our common stock; and

·

The anticipated volatile nature of the trading prices of our common stock following this offering; dilution experienced by investors in the offering; and dilution which may be caused by future sales of securities.

Company Information and Formation

Our principal executive offices are located at 3450 N. Triumph Blvd., Suite 102 Lehi, Utah 84043. Our principal website address is www.LafayetteEnergyCorp.com. The information on or accessible through our website is not part of this prospectus.

Nasdaq Capital Market Listing

We have applied to list our common stock on The Nasdaq Capital Market under the symbol “LEC”. If our application to Nasdaq is not approved or we otherwise determine that we will not be able to secure the listing of the common stock on Nasdaq, we will not complete the offering.

Reverse Stock Split

Effective on January 24, 2023, our Board of Directors, and on January 26, 2023, stockholders holding a majority of our outstanding voting shares, approved resolutions approving and authorizing the filing of a Second Amended and Restated Certificate of Incorporation of the Company, which affected a two-for-three reverse stock split of the outstanding shares of our common stock, without any corresponding change in the number of authorized shares of common stock of the Company. On January 31, 2023, the Second Amended and Restated Certificate of Incorporation of the Company was filed with the Secretary of Delaware, and at the same time, the Reverse Stock Split became effective. Except as otherwise indicated and except in our financial statements and the notes thereto, all references to our common stock, share data, per share data and related information retroactively depict and reflect the Reverse Stock Split. The reverse Stock Split combined each three shares of our outstanding common stock into two shares of common stock, without any change in the par value per share, and the Reverse Stock Split correspondingly adjusted, among other things, the number of shares of common stock available for awards under our equity compensation plans. No fractional shares were issued in connection with the Reverse Stock Split, and any fractional shares resulting from the Reverse Stock Split were rounded up to the nearest whole share on a per stockholder basis.

Implications of Being an Emerging Growth Company

As a company with less than $1.235 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we have elected to take advantage of reduced reporting requirements and are relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company:

We may take advantage of these provisions until December 31, 2028 (the last day of the fiscal year following the fifth anniversary of our initial public offering) if we continue to be an emerging growth company. We would cease to be an emerging growth company if we have more than $1.235 billion in annual revenue, have more than $700 million in market value of our shares held by non-affiliates or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. We have elected to take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act, for complying with new or revised accounting standards that have different effective dates for public and private companies until the earlier of the date we (i) are no longer an emerging growth company or (ii) affirmatively and irrevocably opt out of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act.

1,200,000 shares (or 1,380,000 shares if the underwriter exercises its over-allotment option in full).

Over-allotment option

We have granted to underwriter an option to purchase up to an additional 180,000 shares of common stock (equal to 15% of the number of shares of common stock sold in the offering) from us, solely to cover over-allotments, if any, at the applicable public offering price less the underwriting discounts and commissions shown on the cover page of this prospectus. The underwriter may exercise this option in full or in part at any time and from time to time until 45 days after the date of this prospectus.

Common stock outstanding immediately before this offering

13,762,379 shares

Common stock outstanding immediately after this offering

14,962,379 shares, or 15,142,379 shares if the over-allotment option is exercised in full.

Assumed offering price

$4.50 per share, which is the midpoint of the estimated price range set forth on the cover page of this prospectus.

Use of proceeds

We expect to receive net proceeds from this offering of approximately $5.4 million (or approximately $6.2 million if the underwriter exercises in full its option to purchase 180,000 additional shares of our common stock), assuming an initial public offering price of $4.50 per share, the midpoint of the estimated price range set forth on the cover page of this prospectus, and after deducting underwriting discounts and commissions and estimated offering expenses. We currently intend to use the net proceeds we receive from this offering to invest in the Initial Development Opportunities, to pay bonuses due to our Chief Executive Officer and Chairman ($100,000), to repay $42,500 in non-interest bearing cash advances provided to the Company by our Chief Executive Officer, and for general corporate purposes, including working capital and operating expenses. In addition, we may use a portion of the net proceeds of this offering to finance future acquisitions. However, we do not have any agreements or commitments with respect to any such acquisitions or investments at this time

Risk Factors