Registration No. 333-280925

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| FATPIPE, INC. |

| (Exact name of registrant as specified in its charter) |

| Utah | | 7372 | | 27-1113325 |

(State or other jurisdiction of incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification Number) |

392 East Winchester Street, Fifth Floor

Salt Lake City, Utah 84107

(801) 281-3434

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Ragula Bhaskar

Sanchaita Datta

FatPipe, Inc.

392 East Winchester Street, Fifth Floor

Salt Lake City, Utah 84107

(801) 281-3434

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

Darrin M. Ocasio, Esq. Matthew Siracusa, Esq. Sichenzia Ross Ference Carmel LLP 1185 Avenue of the Americas, 31st Floor New York, NY 10036 (212) 930-9700 | | Ryan C. Wilkins Amanda P. McFall Stradling Yocca Carlson & Rauth LLP 660 Newport Center Drive, Suite 1600 Newport Beach, CA 92660 (949) 725-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | | Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said section 8(a), may determine.

| The information in this preliminary prospectus supplement is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus supplement is not an offer to sell these securities and it is not solicitating an offer to buy these securities in any jurisdiction where the offer or sale is not permitted. |

Subject to completion, dated , 2024

PRELIMINARY PROSPECTUS

Shares

FatPipe, Inc.

Common Stock

This is the initial public offering of shares of the common stock, no par value per share, of FatPipe, Inc., a Utah corporation (the “Company,” “FatPipe,” “we,” “us,” or “our”). Prior to this offering, there has been no public market for our common stock. The initial public offering price is expected to be between $ and $ per share of common stock.

We intend to apply to have our common stock listed on The Nasdaq Capital Market (“Nasdaq”) under the symbol “FATN.”

This offering is being underwritten on a firm commitment basis. We have granted the underwriters an option to buy up to an additional shares of common stock from us to cover over-allotments, which the underwriters may exercise at any time and from time to time during the 45-day period following the closing of this offering.

| | | No Exercise of Over- Allotment | | | Full Exercise of Over- Allotment | |

| | | Per Share | | | Total | | | Per Share | | | Total | |

| Public offering price | | $ | | | | $ | | | | $ | | | | $ | | |

| Underwriting discounts and commissions(1) | | $ | | | | $ | | | | $ | | | | $ | | |

| Proceeds to us, before expenses | | $ | | | | $ | | | | $ | | | | $ | | |

| (1) | We have agreed to issue to the representative warrants to purchase shares of common stock equal to 10% of the shares issued in this offering and to reimburse certain expenses of the representative in connection with this offering. In addition, we have agreed to reimburse the underwriters for certain expenses. See the section titled “Underwriting” beginning on page 55 of this prospectus for additional information. |

Investing in our securities involves a high degree of risk. See the section titled “Risk Factors” beginning on page 4 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities.

We are an “emerging growth company” under the federal securities laws and may elect to comply with certain reduced public company reporting requirements for future filings.

Neither the Securities and Exchange Commission nor any foreign or state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

We have granted the underwriters an option to purchase an additional shares of common stock from us, at the public offering price per share, less underwriting discounts and commissions, for 45 days from the date of this prospectus.

The underwriters expect to deliver the shares of common stock to the purchasers on or about , 2024.

The date of this prospectus is , 2024.

Sole Bookrunning Manager

Roth Capital Partners

Co-Manager

Craig-Hallum

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. The information contained in this prospectus is accurate only as of the date of this prospectus. Our business, financial condition, results of operations and prospects may have changed since such date. Other than as required under the federal securities laws, we undertake no obligation to publicly update or revise such information, whether as a result of new information, future events or any other reason.

The distribution of this prospectus and the offering of our securities in certain jurisdictions may be restricted by law. This prospectus does not constitute, and may not be used in connection with, an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so to any person to whom it is unlawful to make such offer or solicitation. See the section titled “Underwriting” beginning on page 55 of this prospectus. In this prospectus, references to “FatPipe,” “the Company,” “we,” “us,” and “our” refer to FatPipe, Inc. and its subsidiaries. Unless otherwise specified, all dollar amounts are expressed in United States dollars.

INDUSTRY AND MARKET DATA

This prospectus contains statistical data, estimates, and forecasts that are based on various sources, including independent industry publications and other publicly available information, as well as other information based on our internal sources. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to these data, estimates, and forecasts. We have not independently verified the accuracy or completeness of the data contained in these industry publications and other publicly available information. Our industry and market data are subject to a variety of risks and uncertainties, including those described in the section titled “Risk Factors,” which could cause results to differ materially from those expressed in these publications and reports.

Certain information in the text of this prospectus is from industry data sources and publicly available data and reports. The content of the below sources, except to the extent specifically set forth in this prospectus, does not constitute a portion of this prospectus and is not incorporated herein. The sources are provided below:

| | ● | According to Gartner, Inc., the software- defined wide area network market is forecasted to be $5.3 billion for 2023, growing to more than $8 billion by 2026 (https://www.sdxcentral.com/articles/analysis/sd-wan-by-the-numbers-market-size-growth-adoption/2023/08/); |

| | ● | According to Gartner, Inc., the market for secure access service edge will grow at a compound annual growth rate of 36%, reaching almost $15 billion by 2025 (https://www.gartner.com/en/documents/4004092); |

| | ● | Global Software-Defined Wide Area Network (SD-WAN) Industry Research Report, Competitive Landscape, Market Size, Regional Status and Prospect, Maia Research Report, 2023; |

| | ● | Global SASE (Secure Access Service Edge) Industry Research Report, Competitive Landscape, Market Size, Regional Status and Prospect, Maia Research Report, 2023; |

| | ● | Global Network Monitoring Industry Research Report, Competitive Landscape, Market Size, Regional Status and Prospect, Maia Research Report, 2023; and |

| | ● | SD-WAN-Midmarket Report by Software Reviews, A Division of Info-Tech Research Group (https://www.infotech.com/). |

PROSPECTUS SUMMARY

This summary provides an overview of selected information contained elsewhere in this prospectus and does not contain all of the information you should consider before investing in our securities. You should carefully read this prospectus and the registration statement of which this prospectus is a part in their entirety before investing in our securities, including the information discussed under “Risk Factors” beginning on page 4 and our historical and pro forma financial statements and notes thereto that appear elsewhere in this prospectus. Some of the statements in this prospectus constitute forward-looking statements that involve risks and uncertainties. For additional information, refer to the section titled “Special Note Regarding Forward-Looking Statements.”

FATPIPE, INC.

Overview

FatPipe is a pioneer in enterprise-class, application-aware, secure software-defined wide area network (“SD-WAN”) solutions for organizations, including enterprises, communication service providers, security service providers, government organizations, and middle-market companies.

Organizations, large and small, have become increasingly dependent on their information technology (“IT”) network infrastructure for data access and communications, and the critical importance of network reliability, extensibility, and durability has continued to grow as the volume of traffic across those networks expands. The management, monitoring, and security of an organization’s network has become increasingly complicated in an era of growing demands from remote work, increasing connectivity points, and disparate operations, while network integrity is challenged by ever more sophisticated cyber threats. These factors are conspiring to increase an organization’s reliance on its computer networks while simultaneously making the management and maintenance of those networks more costly and complex.

We are dedicated to continually improving the way organizations connect, ensuring their networks are secure, reliable, and support their continued success. Our commitment lies in empowering our customers with a seamless and dependable connectivity infrastructure that safeguards their critical data and fosters business continuity. We further aim to ensure our customers have unparalleled insights into their network operations.

Through our integrated suite of software solutions, we offer our customers a reliable and secure platform to support mission-critical applications running on cloud, hybrid cloud and on-premise networks. Our core offerings include SD-WAN, secure access service edge (“SASE”), and network monitoring service (“NMS”) software solutions, each of which is typically offered to our customers as a subscription service. These solutions address a broad set of network management needs and include an integrated set of capabilities to automate the complex requirements of network optimization.

The market for these network services is large, global in nature and growing at attractive rates. The total global market for SD-WAN solutions and services, our core offering, was estimated by the Maia Research Report to grow from $4.5 billion in 2022 to over $17.6 billion in 2030. The Maia Research Report also projects the total market size for SASE software and platforms to expand from $6.4 billion in 2022 to $27.2 billion in 2030, and the total market for NMS to grow from $2.0 billion to $4.4 billion over the same period. Each of these individual markets are expected to grow at a compounded rate of between 10% and 20% through 2030, with SD-WAN’s projected growth rate to be approximately 18.5% through 2030.

Our Solution

Our objective is to offer a suite of solutions to ensure our customers can securely support their networks in this cloud-first world. We are committed to driving a trusted customer experience through innovation and a diverse set of capabilities. Our core offerings are based on a complete, integrated suite of software solutions, including SD-WAN, SASE, and NMS capabilities, each of which can be individually licensed to create an experience tailored to a customer’s needs and network configuration. Additionally, all of our technologies are available for commercial sale. Further, our product pipeline consists of new SD-WAN security features and enhancements to the NMS. Currently, SD-WAN, SASE, and NMS revenues are packaged as part of managed service contracts. Our solutions have been designed for high levels of flexibility, providing an ability to customize our services and configure offerings to incorporate each customer’s preferred digital platform, including integrating with a variety of leading platform, wide area network (“WAN”), security, and cloud providers.

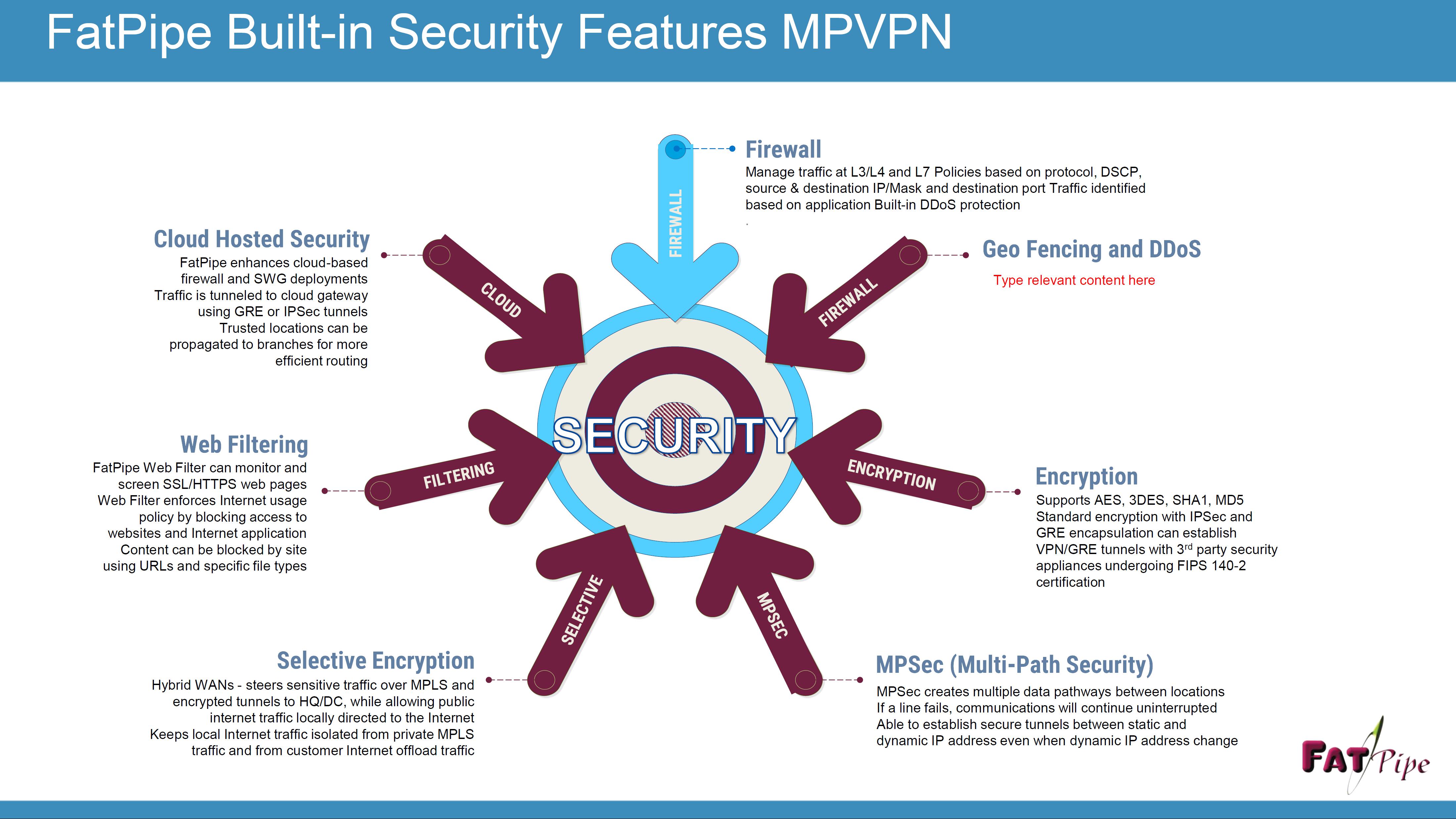

| | ● | SD-WAN: Our primary offering is an SD-WAN, WAN Edge software platform that integrates a broad array of network traffic management and routing, security, and monitoring functions and is predominately sold on a subscription basis. The platform can be delivered on a dedicated commodity appliance or virtual configuration, and can be installed in a variety of network environments, including cloud, hybrid or on-premise. |

| | ● | SASE: Our SASE offering provides virtual network and next generation security functions, which combine networking and next generation network security services into a single cloud-delivered solution. |

| | ● | NMS: Our EnterpriseView Reporting System for network monitoring provides a platform to monitor an end-user’s WAN, security compliance parameters and the performance of FatPipe devices under management. |

Our core technology has been developed internally by its founding management team and supported by a long-tenured group of engineers and software developers. We hold a portfolio of 13 patents that cover a range of SD-WAN and related capabilities.

Our software solutions are provided through a subscription-based model. We offer a portfolio of services such as customer technical support, professional services, and training during the fixed term of the subscription, which generally requires a contractual commitment of 36 to 60 months. We sell our software and services predominantly through a network of distributors, value-added resellers, internet service providers (“ISPs”) and other third parties. We service customers globally, with our largest customer populations located in the United States and India.

Selected Risk Factors

Investing in our common stock involves risks. You should carefully read “Risk Factors” beginning on page 4 for an explanation of these risks before investing in our common stock. In particular, the following considerations, among others, may offset our competitive strengths or have a negative effect on our growth strategy, which could cause a decline in the price of our common stock and result in a loss of all or a portion of your investment.

| | ● | Our operating results are likely to vary significantly and be unpredictable. |

| | ● | Our historical financial information may not be representative of our results as a public company. |

| | ● | We rely heavily on our reselling partners and our ability to work with suitable partners may impact our growth plans. |

| | ● | If we do not increase the effectiveness of our sales organization, we may have difficulty adding new end-customers or increasing sales to our existing end-customers and our business may be adversely affected. |

| | ● | We are dependent on the continued services and performance of our senior management, the loss of any of whom could adversely affect our business, operating results, and financial condition. |

| | ● | If our new software solutions and enhancements do not achieve sufficient market acceptance, our results of operations and competitive position will suffer. |

| | ● | If functionality similar to that offered by our software solutions is incorporated into our competitors’ existing network infrastructures, our customers may decide against adding our appliances to their network, which would have an adverse effect on our business. |

| | ● | The network security market is rapidly evolving and the complex technologies incorporated in our software solutions make them difficult to develop. If we do not accurately predict, prepare for and respond promptly to technological and market developments and changing end-customer needs, our competitive position and prospects may be harmed. |

| | ● | Our business is subject to the risks of warranty claims, product liability and product defects. |

| | ● | Our proprietary rights may be difficult to enforce and we may be subject to claims by others that we infringe their proprietary technology. |

| | ● | If our estimates or judgments relating to our critical accounting policies are based on assumptions that change or prove to be incorrect, our operating results could fall below expectations of securities analysts and investors, resulting in a decline in our stock price. |

Corporate Information

We were incorporated as a Utah corporation in October 14, 2010. Our principal executive office is located at 392 East Winchester Street, Fifth Floor, Salt Lake City, UT 84107. FatPipe, Inc. has two wholly owned subsidiaries, FatPipe Networks Private Limited, a company registered in Tamil Nadu India, and FatPipe Technologies, a Utah corporation. Our telephone number at our principal executive office is (801) 281-3434. Our website address is www.fatpipe.com. We do not incorporate the information on or accessible through our website into the prospectus, and you should not consider any information on, or that can be accessed through, our website as part of this prospectus.

THE OFFERING

| Common stock offered by us | | shares. |

| | | |

| Underwriters’ option to purchase additional shares of common stock | | We have granted the underwriters an option to purchase up to an additional shares of common stock, from us at the public offering price per share, less underwriting discounts and commissions, for a period of 45 days from the date of this prospectus. |

| | | |

Common stock outstanding after this offering | | shares, or shares if the underwriters exercise in full their option to purchase additional shares of common stock. |

| Use of proceeds | | The net proceeds from our sale of shares of our common stock in this offering will be approximately $ , after deducting estimated underwriting discounts and commissions and offering expenses payable by us. If the underwriters exercise their option in full to purchase additional shares of common stock, our net proceeds from this offering will be approximately $ . We plan to use approximately $ of the net proceeds from this offering for sales and marketing activities, to enhance our customer support operations, and for ongoing corporate purchases and research and development, with the remaining net proceeds to be used for general working capital purposes. For additional information please refer to the section titled “Use of Proceeds” on page 27 of this prospectus. |

| | | |

| Risk factors | | Investing in our securities involves a high degree of risk. You should carefully review and consider the “Risk Factors” section of this prospectus for a discussion of factors to consider before deciding to invest in shares of our common stock. |

| | | |

| Representative’s Warrants | | We have agreed to issue to the lead underwriter, as representative of the several underwriters, warrants to purchase a number of shares of common stock equal to 10.0% of the shares of common stock sold in this offering by us (including any shares of common stock sold upon exercise of the over-allotment option). The warrants will be exercisable at a price per share equal to 100% of the public offering price of the common stock in this offering. The warrants are exercisable at any time and from time to time, in whole or in part, during the four-and-a-half-year period commencing six months from the date of commencement of sales of this offering. See the section titled “Underwriting.” |

| | | |

Proposed Nasdaq trading symbol | | We intend to apply to have our shares of common stock listed on Nasdaq under the symbol “FATN.” |

The number of shares of common stock that will be outstanding after this offering set forth above is based upon 13,026,464 shares of common stock outstanding as of December 5, 2024.

Except as otherwise indicated herein, all information in this prospectus assumes the following:

| ● | no exercise by the underwriters of their option to purchase additional shares of common stock; and |

| | |

| ● | no exercise of the representative’s warrant. |

RISK FACTORS

You should carefully consider the risks and uncertainties described below as well as other information provided to you in this document, including information in the section of this document titled “Special Note Regarding Forward-Looking Statements.” The occurrence of any of the following risks, as well as any risks or uncertainties not currently known to us or that we currently do not believe to be material, could materially and adversely affect our business, financial condition or results of operations could be materially adversely affected, the value of our common stock could decline, and you may lose all or part of your investment.

Summary of Risk Factors

| ● | Our operating results are likely to vary significantly and be unpredictable. |

| ● | We rely heavily on our reselling partners and our ability to work with suitable partners may impact our growth plans. |

| ● | If we are unable to develop and introduce new solutions and improve existing solutions in a cost-effective and timely manner, then our competitive position may be negatively impacted and our business, results of operations, and financial condition may be adversely affected. |

| ● | We invest significantly in research and development (“R&D”), and to the extent our R&D efforts are unsuccessful, our competitive position may be negatively impacted and our business, results of operations, and financial condition may be adversely affected. |

| ● | We operate in a highly competitive market. |

| ● | Increases in costs of the materials and other components that we use in our solutions would adversely affect our business, results of operations, and financial condition. |

| ● | Adverse economic conditions, such as a possible recession and possible impacts of inflation or stagflation, increasing or decreasing interest rates, reduced information technology spending or any economic downturn or recession, may adversely impact our business. |

| ● | Our billings, revenue and free cash flow growth may slow or may not continue, and our operating margins may decline. |

| ● | We are dependent on the continued services and performance of our senior management, the loss of any of whom could adversely affect our business, operating results and financial condition. |

| ● | If we are unable to attract, retain, and motivate key employees, then our business, results of operations, and financial condition would be adversely affected. |

| ● | We may need to raise additional capital in the future, which may not be available on terms acceptable to us, or at all. |

| ● | If we do not increase the effectiveness of our sales organization, we may have difficulty adding new end-customers or increasing sales to our existing end-customers and our business may be adversely affected. |

| ● | Unless we continue to develop better market awareness of our company and our software solutions, and to improve lead generation and sales enablement, our revenue may not continue to grow. |

| ● | We face competition in our market and we may not maintain or improve our competitive position. |

| ● | If our new software solutions and enhancements do not achieve sufficient market acceptance, our results of operations and competitive position will suffer. |

| ● | Demand for our software solutions may be limited by market perception that individual software solutions from one vendor that provide multiple layers of security protection in one offering are inferior to point solution network security solutions from multiple vendors. |

| ● | If functionality similar to that offered by our software solutions is incorporated into our competitors’ existing network infrastructures, our customers may decide against adding our appliances to their network, which would have an adverse effect on our business. |

| ● | Because some of the key components in our network server come from limited sources of supply, we are susceptible to supply shortages, long or uncertain lead times for components, and supply changes, each of which could disrupt or delay our scheduled software deliveries to our customers, result in inventory shortage, cause loss of sales and customers or increase component costs resulting in lower gross margins and free cash flow. |

| ● | The sales prices of our hardware and software solutions may decrease, which may reduce our gross profits and operating margin and may adversely impact our financial results and the trading price of our common stock. |

| ● | The network security market is rapidly evolving and the complex technologies incorporated in our software solutions make them difficult to develop. If we do not accurately predict, prepare for and respond promptly to technological and market developments and changing end-customer needs, our competitive position and prospects may be harmed. |

| ● | Our ability to sell our software solutions is dependent on our quality control processes and the quality of our technical support services, and our failure to offer high-quality technical support services could have a material adverse effect on our sales and results of operations. |

| ● | Our business is subject to the risks of warranty claims, product liability and product defects. |

| ● | Our historical financial information may not be representative of our results as a public company. |

| ● | If our internal enterprise IT networks, on which we conduct internal business and interface externally, our operational networks, through which we connect to customers, vendors and partners systems and provide services, or our R&D networks, our back-end labs and cloud stacks hosted in our data centers, colocation vendors or public cloud providers, through which we research, develop and host software solutions are compromised, public perception of our offerings may be harmed, our customers may be breached and harmed, we may become subject to liability, and our business, operating results and stock price may be adversely impacted. |

| ● | Our proprietary rights may be difficult to enforce and we may be subject to claims by others that we infringe their propriety technology. |

| ● | Claims by others that we infringe their proprietary technology or other litigation matters could harm our business. |

| ● | Failure to comply with laws and regulations applicable to our business could subject us to fines and penalties and could also cause us to lose end-customers in the public sector or negatively impact our ability to contract with the public sector. |

| ● | We are subject to governmental export and import controls that could subject us to liability or restrictions on sales, and that could impair our ability to compete in international markets. |

| ● | Investors’ expectations of our performance relating to environmental, social and governance factors may impose additional costs and expose us to new risks. |

| | | |

| | ● | We have incurred indebtedness and may incur other debt in the future, which may adversely affect our financial condition and future financial results. |

| ● | If our estimates or judgments relating to our critical accounting policies are based on assumptions that change or prove to be incorrect, our operating results could fall below expectations of securities analysts and investors, resulting in a decline in our stock price. |

| ● | We are affected by fluctuations in currency exchange rates, including those in connection with recent inflationary trends in the United States. |

| ● | We could be subject to changes in our tax rates, the adoption of new U.S. or international tax legislation, exposure to additional tax liabilities or impacts from the timing of tax payments. |

| ● | Forecasting our estimated annual effective tax rate is complex and subject to uncertainty, and there may be material differences between our forecasted and actual tax rates. |

| ● | As a public company, we will be subject to compliance initiatives that will require substantial time from our management and result in significantly increased costs that may adversely affect our operating results and financial condition. |

| ● | If securities or industry analysts stop publishing research or publish inaccurate or unfavorable research about our business, our stock price and trading volume could decline. |

| ● | Global economic uncertainty, an economic downturn, the possibility of a recession, inflation, rising interest rates, weakening software demand caused by political instability, changes in trade agreements and conflicts such as the war in Ukraine, could adversely affect our business and financial performance. |

| ● | Changes in financial accounting standards may cause adverse unexpected fluctuations and affect our reported results of operations. |

Risks Related to Our Business and Financial Position

Our operating results are likely to vary significantly and be unpredictable.

Our operating results have historically varied from period to period, and we expect that they will continue to do so as a result of a number of factors, many of which are outside of our control or may be difficult to predict, including:

| ● | Economic conditions, including macroeconomic and regional economic challenges resulting, for example, from a recession or other economic downturn, increased inflation or possible stagflation in certain geographies, rising interest rates, the war in Ukraine, tensions between China and Taiwan, or other factors; |

| ● | our ability to attract and retain new end-customers or sell additional platform solutions to our existing end-customers; |

| ● | component shortages, including chips and other components, and product inventory shortages, including those caused by factors outside of our control, such as epidemics and pandemics, supply chain disruptions, inflation and other cost increases, international trade disputes or tariffs, natural disasters, health emergencies, power outages, civil unrest, labor disruption, international conflicts, terrorism, wars, such as rising tensions between China and Taiwan, and critical infrastructure attacks; |

| ● | the level of demand for our software solutions may render forecasts inaccurate; |

| ● | supplier cost increases and any lack of market acceptance of our price increases designed to help offset any supplier cost increases; |

| ● | the impact to our business, the global economy, disruption of global supply chains and creation of significant volatility and disruption of the financial markets due to factors such as increased inflation or possible stagflation in certain geographies, fluctuating interest rates, rising tensions between China and Taiwan and other factors; |

| ● | any actual or perceived vulnerabilities in our software solutions, and any actual or perceived breach of our network or our customers’ networks; |

| ● | increased expenses, unforeseen liabilities or write-downs and any negative impact on results of operations from any acquisition or equity investment consummated, as well as accounting risks, integration risks related to software plans and software solutions and risks of negative impact by such acquisitions and equity investments on our financial results; |

| ● | investors’ expectations of our performance relating to environmental, social and governance (“ESG”) and commitment to carbon neutrality; |

| ● | certain customer agreements which contain service-level agreements, under which we guarantee specified availability of our platform and solutions; |

| ● | data security requirements that may be enforced inconsistently in certain jurisdictions; |

| ● | any decreases in demand by customers, including any such decreases caused by factors outside of our control such as natural disasters and health emergencies, including earthquakes, droughts, fires, power outages, typhoons, floods, pandemics or epidemics and manmade events such as civil unrest, labor disruption, international trade disputes, international conflicts, terrorism, wars, such as the war in Ukraine, and critical infrastructure attacks; |

| ● | the effectiveness of our sales organization, generally or in a particular geographic region, including the time it takes to hire sales personnel, the timing of hiring and our ability to hire and retain effective sales personnel, as well as our efforts to align our sales capacity and market demand; |

| ● | sales execution risk related to effectively selling to all segments of the market, including small- and medium-sized businesses, government organizations and service providers, and risks associated with the complexity and distraction in selling to all segments, such as increased competition, the unpredictability closing larger enterprise and large organization deals, and the risk that our sales representatives do not effectively sell our software solutions; |

| ● | execution risk associated with our efforts to capture the opportunities related to our identified growth drivers, such as our ability to capitalize on the convergence of networking and security, vendor consolidation of various cyber security solutions, SD-WAN, infrastructure security, security operations, SASE and other cloud security solutions, endpoint protection, Internet of Things (“IoT”) and security opportunities; |

| ● | the timing and degree of our investments in sales and marketing, and the impact of such investments on our operating expenses, operating margin and the productivity, capacity, tenure and effectiveness of execution of our sales and marketing teams; |

| ● | the timing of revenue recognition for our sales, including any impacts resulting from extension of payment terms to distributors and fluctuations in backlog levels, which could result in more variability and less predictability in our quarter-to-quarter revenue and operating results; |

| ● | the level of perceived threats to network security, which may fluctuate from period-to-period; |

| ● | changes in the requirements, market needs or buying practices and patterns of our distributors, resellers or customers; |

| ● | changes in the growth rates of the network security market in particular and other security and networking markets, such as SD-WAN, IoT, switches, access points, security operations, SASE and other cloud solutions for which we and our competitors sell software solutions; |

| ● | the timing and success of new software solutions or enhancements by us or our competitors, or any other change in the competitive landscape of our industry, including consolidation among our competitors, partners or customers; |

| ● | the deferral of orders from distributors, resellers or end-customers in anticipation of new software solutions or enhancements announced by us or our competitors, price decreases or changes in our registration policies, or the acceleration of orders in response to our announced or expected price list increases; |

| ● | increases or decreases in our billings, revenue and expenses caused by fluctuations in foreign currency exchange rates or a strengthening of the U.S. dollar, as a portion of our expenses is incurred and paid in currencies other than the U.S. dollar and the impact such fluctuations may have on the actual prices that our partners and customers are willing to pay for our software solutions and services; |

| ● | compliance with existing laws and regulations; |

| ● | our ability to obtain and maintain permits, clearances and certifications that are applicable to our ability to conduct business with the U.S. federal government, other international and local governments and other industries and sectors; |

| ● | potential litigation, litigation fees and costs, settlements, judgments and other equitable and legal relief granted related to litigation; |

| ● | the impact of cloud-based security solutions on our billings, revenue, operating margins and free cash flow; |

| ● | decisions by potential end-customers to purchase network security solutions from newer technology providers, from larger, more established security vendors or from their primary network equipment vendors; |

| ● | price competition and increased competitiveness in our market, including the competitive pressure caused by software refresh cycles; |

| ● | our ability to both increase revenue and manage and control operating expenses in order to maintain or improve our operating margins; |

| ● | changes in customer renewal rates or attach rates for our software solutions; |

| ● | changes in the timing of our billings, collection for our contracts or the contractual term of the software solutions sold; |

| ● | changes in our estimated annual effective tax rates and the tax treatment of R&D expenses and the related impact of cash from operations; |

| ● | changes in circumstances and challenges in business conditions, including decreased demand, which may negatively impact our channel partners’ ability to sell the current inventory they hold and negatively impact their future purchases of software solutions from us; |

| ● | increased demand for cloud-based services and the uncertainty associated with transitioning to providing such services; |

| ● | our partners having insufficient financial resources to withstand changes and challenges in business conditions; |

| ● | disruptions in our channel or termination of our relationship with important partners, including as a result of consolidation among distributors and resellers of security solutions; |

| ● | insolvency, credit or other difficulties confronting our key channel partners, which could affect their ability to purchase or pay for our software solutions; |

| ● | policy changes and uncertainty with respect to immigration laws, trade policy and tariffs, including increased tariffs applicable to countries where we manufacture our hardware, foreign imports and tax laws related to international commerce; |

| ● | future accounting pronouncements or changes in our accounting policies as well as the significant costs that may be incurred to adopt and comply with these new pronouncements; and |

| ● | legislative or regulatory changes, such as with respect to privacy, information and cybersecurity, exports, the environment, regional component bans, and requirements for local manufacture. |

Any one of the factors above or the cumulative effect of some of the factors referred to above may result in significant fluctuations in our quarterly financial and other operating results. This variability and unpredictability could result in our failing to meet our internal operating plan or the expectations of securities analysts or investors for any period. If we fail to meet or exceed such expectations for these or any other reasons, the market price of our shares could fall substantially and we could face costly lawsuits, including securities class action suits. Accordingly, in the event of revenue shortfalls, we are generally unable to mitigate the negative impact on margins in the short term.

We rely heavily on our reselling partners and our ability to work with suitable partners may impact our growth plans.

Within our partner network, our two largest reselling partners accounted for over 49.5% of our total revenues in our fiscal year ended March 31, 2024, and 50.8% of our total revenues in our fiscal year ended March 31, 2023. One reselling partner accounted for 45.09% and 43.59% of our total revenue in fiscal 2024 and 2023, respectively. For the six months ended September 30, 2024, two of our largest reselling partners accounted for approximately 51.6%, and 6.29% of our total revenue. For the six months ended September 30, 2023, two partners accounted for approximately 46.69% and 3.60% of our revenue respectively. We continue to engage with new partners and expand our existing relationships to mitigate customer concentration risk. Additionally, we are in discussions with multiple potential partners in Southeast Asia to address the Southeast Asia market and there are no assurances we will find a suitable qualified partners.

If we are unable to develop and introduce new software solutions and improve existing software solutions in a cost-effective and timely manner, then our competitive position may be negatively impacted and our business, results of operations, and financial condition may be adversely affected.

If we are unable to adapt to rapidly evolving technological advancements and market demands within the enterprise network software sector, our competitive position could be undermined, leading to adverse effects on our business, results of operations, and financial condition. The network software industry is characterized by swift changes in customer preferences, emerging security threats, and evolving performance expectations. Failing to anticipate and address these shifts could result in our solutions becoming outdated or less effective, which may cause customers to seek alternatives from our competitors. Additionally, the complex nature of SD-WAN, SASE, and SIEM solutions demand continuous R&D efforts to ensure compatibility with new networking protocols, hardware platforms, and cloud architectures. Delays or inefficiencies in the development processes could hinder our ability to capture new market opportunities and retain existing customers. Therefore, our inability to proactively develop and introduce innovative solutions, as well as enhance our existing offerings, could weaken our competitive stance and negatively impact our overall business prospects.

We invest significantly in research and development, and to the extent our research and development efforts are unsuccessful, our competitive position may be negatively impacted and our business, results of operations, and financial condition may be adversely affected.

Our success depends heavily on our ability to attract and retain highly skilled and experienced R&D personnel. The network software industry is marked by rapid technological advancements, evolving market trends, and intense competition. If we fail to effectively recruit and retain top-tier R&D personnel, our capacity to innovate, develop new solutions, and enhance existing software solutions may be compromised. Competition for skilled engineers and developers is strong, and an inability to assemble a proficient R&D team could hinder our ability to respond promptly to market demands and stay ahead of technological shifts. Though we mitigate this with our robust talent development pipeline, a shortage of qualified candidates may negatively impact our performance. Furthermore, if key R&D personnel were to leave or if we encounter challenges in maintaining a collaborative and innovative work environment, our research outcomes might suffer, negatively impacting the quality and speed of our software development. In such scenarios, our competitive standing could weaken, potentially leading to a decline in market share, revenue, and overall business performance.

We operate in a highly competitive market.

The intense competition within our market poses a risk to our business operations, financial performance, and overall market position. Our industry is comprised of a number of players, including both established companies and emerging startups. As a result, we face pressure to differentiate our offerings, maintain competitive pricing, and consistently deliver high-quality solutions. If we fail to navigate this competitive landscape, we could experience challenges in acquiring new customers, expanding our market share, and retaining existing customers. Furthermore, the emergence of new competitors or the rapid advancement of alternative technologies could disrupt our current business model. Therefore, our ability to successfully compete is critical to our long-term success.

Increases in costs of the materials and other components that we use in our solutions would adversely affect our business, results of operations, and financial condition.

Fluctuations or increases in the costs of materials and components to our hardware or software solutions pose a risk to our business. When customers cannot host our software solutions, we procure hardware components to deploy to customer sites. Any significant rise in these costs, whether due to supply chain disruptions, market volatility, or external factors, could lead to elevated production expenses and impact our profit margins or customer demand if the cost is passed on. Failure to manage and mitigate these cost pressures could impact profitability or revenue. Additionally, if we are unable to adapt to changing cost dynamics, it could impede our ability to invest in R&D or expansion efforts, further limiting our growth prospects. Therefore, our capability to effectively manage material and component costs is a factor in our operational resilience and long-term financial success.

Adverse economic conditions, such as a possible recession and possible impacts of inflation or stagflation, increasing or decreasing interest rates, reduced information technology spending or any economic downturn or recession, may adversely impact our business.

Our business depends on the overall demand for information technology and on the economic health of our current and prospective customers. In addition, the purchase of our software solutions is often discretionary and may involve a significant commitment of capital and other resources. Weak global and regional economic conditions, fluctuating spending environments, a potential recession, the effects of ongoing or increased inflation, possible stagflation in certain geographies, variable interest rates, geopolitical instability and uncertainty, a reduction in information technology spending regardless of macroeconomic conditions, the effects of epidemics and pandemics, and the impact of the war in Ukraine each could have a material adverse impact on our financial condition, results of operations, and our business. Our inability to mitigate any of the foregoing events may result in longer sales cycles, a decrease in prices of our software solutions, increased component costs, higher default rates among our channel partners, reduced unit sales, or a decline in growth.

The existence of inflation in certain economies has resulted in, and may continue to result in, increasing or decreasing interest rates and capital costs, increased component or shipping costs, increased costs of labor, weakening exchange rates and other similar effects. We may not be able to successfully mitigate these risks in a timely manner. These economic challenges may also adversely impact spending patterns by our distributors, resellers and end-customers.

Our billings, revenue and free cash flow growth may slow or may not continue, and our operating margins may decline.

We may experience slowing growth or a decrease in billings, revenue, operating margin and free cash flow for a number of reasons, including a slowdown in demand for our hardware or software solutions, a shift in demand from hardware to software solutions, decrease in revenue growth, increased competition, worldwide or regional economic challenges based on inflation or possible stagflation, a regional or global recession, rising interest rates, the war in Ukraine, a decrease in the growth of our overall market or softness in demand in certain geographies or industry verticals, such as the service provider industry, changes in our strategic opportunities, execution risks, lower sales productivity and our failure for any reason to continue to capitalize on sales and growth opportunities due to other risks identified in the risk factors described in this prospectus. Our expenses, as a percentage of total revenue, may be higher than expected if our revenue is lower than expected. If our investments in sales and marketing and other functional areas do not result in expected billings and revenue growth, we may experience margin declines. In addition, we may not be able to sustain profitability in future periods if we fail to increase billings, revenue or deferred revenue, and do not appropriately manage our cost structure, free cash flow, or encounter unanticipated liabilities. As a result, any failure by us to maintain profitability and margins and continue our billings, revenue and free cash flow growth could cause the price of our common stock to materially decline.

We are dependent on the continued services and performance of our senior management, the loss of any of whom could adversely affect our business, operating results and financial condition.

Our future performance depends on the continued services and continuing contributions of our senior management to execute on our business plan and to identify and pursue new opportunities and software solutions. The loss of services of members of senior management, or of any of our senior sales leaders or functional area leaders, could significantly delay or prevent the achievement of our development and strategic objectives. The loss of the services or the distraction of our senior management for any reason could adversely affect our business, financial condition and results of operations.

Dr. Bhaskar and Ms. Datta are the primary inventors of our Company’s technology and have been instrumental in developing key partnerships. While our management team also supports the continuing operations, our two founders continue to play a key role in the company and in developing new ideas and building new partnerships.

If we are unable to attract, retain, and motivate key employees, then our business, results of operations, and financial condition would be adversely affected.

Hiring and retaining qualified executives, developers, engineers, technical staff, and sales representatives are critical to our business. The competition for highly skilled employees in our industry is increasingly intense. Competitors for technical talent increasingly may seek to hire our employees. Changes in the interpretation and application of employment-related laws to our workforce practices may also result in increased operating costs and less flexibility in how we meet our changing workforce needs. To help attract, retain, and motivate qualified employees, we intend to use employee incentives such as share-based awards. Our employee hiring and retention also depend on our ability to build and maintain a diverse and inclusive workplace culture and be viewed as an employer of choice. If our share-based or other compensation programs and workplace culture cease to be viewed as competitive, our ability to attract, retain, and motivate employees would be weakened, which would harm our results of operations. Equity compensation has been, and will continue to be, an important part of our future compensation strategy and a significant component of our future expenses, which we expect to increase over time. Moreover, sustained declines in our stock price can reduce the retention value of our share-based awards. If we do not effectively hire, onboard, retain, and motivate key employees, then our business, results of operations, and financial condition would be adversely affected.

Changes in our management team can also disrupt our business. Our management and senior leadership team has significant industry experience, and their knowledge and relationships would be difficult to replace. Leadership changes may occur from time to time, and we cannot predict whether significant resignations will occur or whether we will be able to recruit qualified personnel.

We may need to raise additional capital in the future, which may not be available on terms acceptable to us, or at all.

A majority of our operating expenses are for sales and marketing, and R&D activities. Our capital requirements will depend on many factors, including, but not limited to:

| ● | technological advancements; |

| ● | market acceptance of our solutions and solution enhancements, and the overall level of sales of our software solutions; |

| ● | R&D expenses; |

| ● | our relationships with our customers and partners; |

| ● | our ability to control costs; |

| ● | sales and marketing expenses; |

| ● | enhancements to our infrastructure and systems and any capital improvements to our facilities; |

| ● | working capital for inventory; |

| ● | potential acquisitions of businesses and product lines; and |

| ● | general economic conditions, including, inflation, rising interest rates, and international conflicts and their impact on the tech industry in particular. |

If our capital requirements are materially different from those currently planned, we may need additional capital sooner than anticipated. If additional funds are raised through the issuance of equity or convertible debt securities, our stockholders may be diluted. Additional financing may not be available on favorable terms, on a timely basis, or at all. If adequate funds are not available or are not available on acceptable terms, we may be unable to continue our operations as planned, develop or enhance our solutions, expand our sales and marketing programs, take advantage of future opportunities, or respond to competitive pressures.

Risks Related to Our Sales and End-Customers

If we do not increase the effectiveness of our sales organization, we may have difficulty adding new end-customers or increasing sales to our existing end-customers and our business may be adversely affected.

Although we have a channel sales model, sales in our industry are complex and members of our sales organization often engage in direct interaction with our prospective end-customers, particularly for larger deals involving larger end-customers. Therefore, we continue to be substantially dependent on our sales organization to obtain new end-customers and sell additional software solutions and services to our existing end-customers. There is significant competition for sales personnel with the skills and technical knowledge that we require, including experienced enterprise sales employees and others. Our ability to grow our revenue depends, in large part, on our success in recruiting, training and retaining sufficient numbers of sales personnel to support our growth and on the effectiveness of our sales strategy, sales execution, and sales personnel selling successfully in different contexts, each of which has its own different complexities, approaches and competitive landscapes, such as managing and growing the channel business for sales to small businesses and more actively selling to the end-customer for sales to larger organizations. New hires require substantial training and may take significant time before they achieve full productivity. Our recent hires and planned hires may not become productive as quickly as we expect, and we may be unable to hire or retain sufficient numbers of qualified individuals in the markets where we do business or plan to do business. Furthermore, hiring sales personnel in new countries requires additional setup and upfront costs that we may not recover if the sales personnel fail to achieve full productivity. If our sales employees do not become fully productive on the timelines that we have projected, our revenue may not increase at anticipated levels and our ability to achieve long-term projections may be negatively impacted. If we are unable to hire and train sufficient numbers of effective sales personnel, the sales personnel are not successful in obtaining new end-customers or increasing sales to our existing customer base or sales personnel do not effectively sell our Enhanced Platform Technology software solutions, our business, operating results and prospects may be adversely affected. If we do not hire properly qualified and effective sales employees and organize our sales team effectively to capture the opportunities in the various customer segments we are targeting, our growth and ability to effectively support growth may be harmed.

In addition, in light of macroeconomic trends and in the event of sales execution challenges for any reason, we may face excess sales capacity, low sales productivity generally, and a decline in productivity in our sales organization. If we are not able to align our sales capacity and market demand, or if the productivity of our sales organization decreases, our operating results and financial condition could be harmed.

Unless we continue to develop better market awareness of our company and our software solutions, and to improve lead generation and sales enablement, our revenue may not continue to grow.

Increased market awareness of our capabilities and software services and increased lead generation are essential to our continued growth and our success in all of our markets, particularly the market for sales to large businesses, service providers and government organizations. While we have increased our investments in sales and marketing, it is not clear that these investments will continue to result in increased revenue. If our investments in additional sales personnel or our marketing programs are not successful in continuing to create market awareness of our company and software solutions or increasing lead generation, in growing billings for our broad software solutions or if we experience turnover and disruption in our sales and marketing teams, we may not be able to achieve sustained growth, and our business, financial condition and results of operations may be adversely affected.

Risks Related to Our Industry, Customers, Software and Services

We face competition in our market and we may not maintain or improve our competitive position.

The market for network security software solutions is competitive and dynamic and we expect to face competitors across different cybersecurity markets.

Some of our existing and potential competitors enjoy competitive advantages such as:

| ● | greater name recognition and/or longer operating histories; |

| ● | larger sales and marketing budgets and resources; |

| ● | broader distribution and established relationships with distribution partners and end-customers; |

| ● | access to larger customer bases; |

| ● | greater customer support resources; |

| ● | greater resources to make acquisitions; |

| ● | stronger U.S. government relationships; |

| ● | lower labor and development costs; and |

| ● | substantially greater financial, technical and other resources. |

In addition, certain of our larger competitors have broader product offerings, and leverage their relationships based on other products or incorporate functionality into existing products in a manner that discourages customers from purchasing our software solutions. These larger competitors often have broader product lines and market focus, and are in a better position to withstand any significant reduction in capital spending by end-customers in these markets. Therefore, these competitors will not be as susceptible to downturns in a particular market. Also, many of our smaller competitors that specialize in providing protection from a single type of security threat are often able to deliver these specialized security products to the market more quickly than we can.

Conditions in our markets could change rapidly and significantly as a result of technological advancements or continuing market consolidation. Our competitors and potential competitors may also be able to develop products or services, and leverage new business models, that are equal or superior to ours, achieve greater market acceptance of their products and services, disrupt our markets, and increase sales by utilizing different distribution channels than we do. In addition, current or potential competitors may be acquired by third parties with greater available resources, and new competitors may arise pursuant to acquisitions of network security companies or divisions. As a result of such acquisitions, competition in our market may continue to increase and our current or potential competitors might be able to adapt more quickly to new technologies and customer needs, devote greater resources to the promotion or sale of their products and services, initiate or withstand substantial price competition, take advantage of acquisition or other opportunities more readily, or develop and expand their product and service offerings more quickly than we do. In addition, our competitors may bundle products and services competitive with ours with other products and services. Customers may accept these bundled products and services rather than separately purchasing our software solutions and services. As our customers refresh the security products bought in prior years, they may seek to consolidate vendors, which may result in current customers choosing to purchase products from our competitors on an ongoing basis. Due to budget constraints or economic downturns, organizations may be more willing to incrementally add solutions to their existing network security infrastructure from competitors than to replace it with our solutions. These competitive pressures in our market or our failure to compete effectively may result in price reductions, fewer customer orders, reduced revenue and gross margins and loss of market share.

If our new software solutions and enhancements do not achieve sufficient market acceptance, our results of operations and competitive position will suffer.

We spend substantial amounts of time and money to internally develop software solutions and enhance versions of our software in order to incorporate additional features, improved functionality or other enhancements in order to meet our customers’ rapidly evolving demands for network security in our highly competitive industry. When we develop a software solution, or an enhanced version of an existing software, we typically incur expenses and expend resources upfront to market, promote and sell the new offering. Therefore, when we develop and introduce new or enhanced software solutions, they must achieve high levels of market acceptance in order to justify the amount of our investment in developing and bringing them to market.

Our new hardware, software solutions or enhancements could fail to attain sufficient market acceptance for many reasons, including:

| ● | delays in releasing our new hardware, software solutions or enhancements to the market; |

| ● | failure to accurately predict market demand in terms of hardware and software functionality and to supply hardware and software solutions that meet this demand in a timely fashion; |

| ● | failure to have the appropriate R&D expertise and focus to make our top strategic software solutions successful; |

| ● | failure of our sales force and partners to focus on selling new hardware and software solutions; |

| ● | inability to interoperate effectively with the networks or applications of our prospective end-customers; |

| ● | inability to protect against new types of attacks or techniques used by hackers; |

| ● | actual or perceived defects, vulnerabilities, errors or failures; |

| ● | negative publicity about their performance or effectiveness; |

| ● | introduction or anticipated introduction of competing products and services by our competitors; |

| ● | poor business conditions for our end-customers, causing them to delay IT purchases; |

| ● | changes to the regulatory requirements around security; and |

| ● | reluctance of customers to purchase software solutions that incorporate open-source software. |

If our new hardware, software solutions or enhancements do not achieve adequate acceptance in the market, our competitive position will be impaired, our revenue will be diminished and the effect on our operating results may be particularly acute because of the significant research, development, marketing, sales and other expenses we incurred in connection with our offerings.

Demand for our software solutions may be limited by market perception that individual software solutions from one vendor that provide multiple layers of security protection in one offering are inferior to point solution network security solutions from multiple vendors.

Sales of many of our software solutions depend on increased demand for incorporating broad security functionality into one application. If the market for these solutions fails to grow as we anticipate, our business will be negatively impacted. Target customers may view “all-in-one” network security solutions as inferior to security solutions from multiple vendors based on their perception that security functions from one vendor restrict users from choosing amongst the wide range of dedicated security applications available. Target customers might also perceive that, by combining multiple security functions into a single platform, our solutions create a “single point of failure” in their networks, which means that an error, vulnerability or failure of our offerings may place the entire network at risk. In addition, the market perception that “all-in-one” solutions may be suitable only for small and medium-sized businesses because such solution lacks the performance capabilities and functionality of other solutions may harm our sales to large businesses, service provider and government organization end-customers. If the foregoing concerns and perceptions become prevalent, even if there is no factual basis for these concerns and perceptions, or if other issues arise with our market in general, demand for multi-security functionality software solutions could be severely limited, which would limit our growth and harm our business, financial condition and results of operations. Further, a successful and publicized targeted attack against us, exposing a “single point of failure”, could significantly increase these concerns and perceptions and may harm our business and results of operations.

If functionality similar to that offered by our software solutions is incorporated into our competitors’ existing network infrastructure products, our customers may decide against adding our appliances to their network, which would have an adverse effect on our business.

Large, well-established providers of networking equipment and may continue to introduce, network security features that compete with our software solutions, either in standalone security products or as additional features in their network infrastructure products. The inclusion of, or the announcement of an intent to include, functionality perceived to be similar to that offered by our security solutions that are already generally accepted as necessary components of network architecture may have an adverse effect on our ability to market and sell our software solutions. Furthermore, even if the functionality offered by network infrastructure providers is more limited than our software solutions, a significant number of customers may elect to accept such limited functionality in lieu of adding appliances from an additional vendor such as us. Many organizations have invested substantial personnel and financial resources to design and operate their networks and have established deep relationships with other providers of networking products, which may make them reluctant to add new components to their networks, particularly from other vendors such as us. If organizations are reluctant to add additional network infrastructure from new vendors or otherwise decide to work with their existing vendors, our business, financial condition and results of operations will be adversely affected.

Because some of the key components in our hardware come from limited sources of supply, we are susceptible to supply shortages, long or uncertain lead times for components, and supply changes, each of which could disrupt or delay our scheduled software deliveries to our customers, result in inventory shortage, cause loss of sales and customers or increase component costs resulting in lower gross margins and free cash flow.

Our contract manufacturers currently purchase several key parts and components for our hardware from limited sources of supply. We are therefore subject to the risk of shortages or uncertain lead times in the supply of these components and the risk that component suppliers may discontinue or modify components used in our software. We have in the past experienced uncertain lead times for certain components. The introduction by component suppliers of new versions of their products, particularly if not anticipated by us or our contract manufacturers, could require us to expend significant resources to incorporate these new components into our solutions. In addition, if these suppliers were to discontinue production of a necessary part or component, we would be required to expend significant resources and time in locating and integrating replacement parts or components from another vendor. Qualifying additional suppliers for limited source parts or components can be time-consuming and expensive.

If we are unable to obtain sufficient quantities of hardware, we may have to find alternate sources. This could result in a delay and cancellation of orders, lost sales, reduced gross margins or damage to our end-customer relationships, which would adversely impact our business, financial condition, results of operations and prospects. Additionally, if actual demand does not directly match with our demand forecasts, due to our purchase order commitments, we could be required to accept or pay for components and finished goods. This may result in us discounting our hardware or excess or obsolete inventory, which we would be required to write down to its estimated realizable value, which in turn could result in lower gross margins. Our reliance on a limited number of suppliers involves several additional risks, including:

| ● | a potential inability to obtain an adequate supply of required parts or components when required; |

| ● | financial or other difficulties faced by our suppliers; |

| ● | infringement or misappropriation of our intellectual property (“IP”); |

| ● | failure of a component to meet environmental or other regulatory requirements; |

| ● | failure to meet delivery obligations in a timely fashion; |

| ● | failure in component quality; and |

| ● | inability to deliver software on a timely basis. |

The occurrence of any of these events would be disruptive to us and could seriously harm our business. Any interruption or delay in the supply of any of these parts or components, or the inability to obtain these parts or components from alternate sources at acceptable prices and within a reasonable amount of time, would harm our ability to meet our scheduled hardware deliveries to our distributors, resellers and end-customers. This could harm our relationships with our channel partners and end-customers and could cause delays in the installation of our software solutions and adversely affect our results of operations. In addition, increased component costs could result in lower gross margins.

The sales prices of our hardware and software solutions may decrease, which may reduce our gross profits and operating margin and may adversely impact our financial results and the trading price of our common stock.

The sales prices for our software solutions may decline for a variety of reasons or the mix of our offerings may change, resulting in lower growth and margins based on a number of factors, including competitive pricing pressures, discounts or promotional programs we offer, a change in our available offerings and anticipation of the introduction of new software solutions. We have recently conducted such price decreases. Competition continues to increase in the market segments in which we participate, and we expect competition to further increase in the future, thereby leading to increased pricing pressures. Larger competitors with more diverse product offerings may reduce the price of products and services that compete with ours in order to promote the sale of other products or services or may bundle them with other products or services. Additionally, although we price our software solutions and services worldwide in U.S. dollars, currency fluctuations in certain countries and regions have in the past, and may in the future, negatively impact actual prices that partners and customers are willing to pay in those countries and regions. Furthermore, we anticipate that the sales prices and gross profits for our hardware and software solutions will decrease over product life cycles. We cannot ensure that we will be successful in developing and introducing new offerings with enhanced functionality on a timely basis, or that those offerings, if introduced, will enable us to maintain our prices, gross profits and operating margin at levels that will allow us to maintain profitability.

The network security market is rapidly evolving and the complex technology incorporated in our software solutions make them difficult to develop. If we do not accurately predict, prepare for and respond promptly to technological and market developments and changing end-customer needs, our competitive position and prospects may be harmed.

The network security market is expected to continue to evolve rapidly. Moreover, many of our end-customers operate in markets characterized by rapidly changing technologies and business plans, which require them to add numerous network access points and adapt increasingly complex networks, incorporating a variety of hardware, software applications, operating systems and networking protocols. In addition, computer hackers and others who try to attack networks employ increasingly sophisticated techniques to gain access to and attack systems and networks. The technology in our software solutions is especially complex because it needs to effectively identify and respond to new and increasingly sophisticated methods of attack, while minimizing the impact on network performance. Additionally, some of our new offerings and enhancements may require us to develop new hardware architectures that involve complex, expensive and time-consuming R&D processes. Although the market expects rapid introduction of new software solutions and to respond to new threats, the development of these solutions is difficult, the timetable for their commercial release and availability is uncertain, and there can be long time periods between releases and availability of new software solutions. We have in the past and may in the future experience unanticipated delays in the availability of new offerings and fail to meet previously announced timetables for such availability. If we do not quickly respond to the rapidly changing and rigorous needs of our end-customers by developing, releasing and making available on a timely basis new software solutions or enhancements that can respond adequately to new security threats, our competitive position and business prospects may be harmed.

Our ability to sell our software solutions is dependent on our quality control processes and the quality of our technical support services, and our failure to offer high-quality technical support services could have a material adverse effect on our sales and results of operations.