As filed with the Securities and Exchange Commission on April 11, 2024.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

___________________________

Proficient Auto Logistics, Inc.

(Exact name of registrant as specified in its charter)

___________________________

Delaware | | 7549 | | 93-1869180 |

(State or other jurisdiction of

incorporation or organization) | | (Primary Standard Industrial

Classification Code Number) | | (I.R.S. Employer

Identification Number) |

c/o The Corporation Trust Company

1209 Orange Street

Wilmington, Delaware 19801

(415) 412-7448

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

___________________________

Ross Berner

Proficient Auto Logistics, Inc.

c/o The Corporation Trust Company

1209 Orange Street

Wilmington, Delaware 19801

(415) 412-7448

(Name, address, including zip code, and telephone number, including area code, of agent for service)

___________________________

Copies to:

Edward S. Best, Esq.

Mayer Brown LLP

71 South Wacker Drive

Chicago, IL 60606

(312) 701-7100 | | Christopher D. Lueking Jonathan E. Sarna Latham & Watkins LLP 330 North Wabash Avenue, Suite 2800 Chicago, IL 60611 (312) 876-7700 |

___________________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | | ☐ | | Accelerated filer | | ☐ |

Non-accelerated filer | | ☒ | | Smaller reporting company | | ☐ |

| | | | | Emerging growth company | | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated April 11, 2024

Shares

Proficient Auto Logistics, Inc.

Common Stock

___________________________

This is the initial public offering of shares of common stock of Proficient Auto Logistics, Inc. We are selling shares of our common stock.

Prior to this offering, there has been no public market for our common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to apply to list our common stock on the Nasdaq Global Market, subject to notice of official issuance, under the symbol “PAL.”

We are an “emerging growth company” under applicable Securities and Exchange Commission rules and will be subject to reduced public company reporting requirements.

Investing in our common stock involves substantial risks. See “Risk Factors” beginning on page 13 to read about factors you should consider before buying shares of stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| | Per share | | Total |

Public offering price | | $ | | | $ | |

Underwriting discounts and commissions(1) | | $ | | | $ | |

Proceeds to us (before expenses) | | $ | | | $ | |

We have granted the underwriters a 30-day option to purchase up to an additional __________shares of common stock from us at the initial public offering price, less the underwriting discount.

The underwriters expect to deliver the shares of common stock to purchasers on or about , 2024.

Joint Book-Running Managers |

Stifel | | Raymond James | | William Blair |

The date of this prospectus is , 2024.

Table of Contents

TABLE OF CONTENTS

PROSPECTUS

i

Table of Contents

Neither we nor the underwriters have authorized anyone to provide you any information or make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by or on behalf of us or to which we have referred you. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the underwriters are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside of the United States, we have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside of the United States.

Prior to this offering, Proficient Auto Logistics, Inc. entered into agreements to acquire in multiple, separate acquisitions (the “Combinations”) five operating businesses and their respective affiliated entities, as applicable, operating under the following names: (i) Delta Automotive Services, Inc., doing business as Delta Auto Transport, Inc., (“Delta”), (ii) Deluxe Auto Carriers, Inc. (“Deluxe”), (iii) Sierra Mountain Group, Inc. (“Sierra”), (iv) Proficient Auto Transport, Inc. (“Proficient Transport”), and (v) Tribeca Automotive Inc. (“Tribeca” and, together with Delta, Deluxe, Sierra, and Proficient Transport, the “Founding Companies”). Proficient Auto Logistics, Inc. will not close the acquisition of any of the Founding Companies unless Proficient Auto Logistics, Inc. closes the acquisition of all the Founding Companies. Furthermore, the closing of the Combinations and this offering are conditioned on the closing of each other. Therefore, if we fail to close the Combinations, this offering will not close. Because of this structure, Proficient Auto Logistics, Inc. has not yet operated as a combined company and does not currently have a combined operating history. See “Business — Overview of Founding Companies” and “Certain Relationships and Related Person Transactions — The Combinations with the Founding Companies” for additional information.

Unless the context requires otherwise, references in this prospectus to “Proficient” refers solely to Proficient Auto Logistics, Inc. prior to the Combinations, and references to the “Company,” “we,” “us,” and “our” refer to Proficient Auto Logistics, Inc. and its subsidiaries after giving effect to the Combinations.

For accounting and reporting purposes, Proficient Transport has been identified as the designated accounting acquirer of each of the Founding Companies. Proficient Transport has been identified as the designated accounting predecessor to the Company.

ii

Table of Contents

TRADEMARKS, SERVICE MARKS, AND TRADE NAMES

This prospectus includes our trademarks and service marks, which are protected under applicable intellectual property laws and owned by us. This prospectus also contains trademarks, service marks, trade names, and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other parties’ trademarks, trade names, or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

iii

Table of Contents

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus and is qualified in its entirety by the more detailed information included elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should carefully read this entire prospectus, including the information in the sections titled “Risk Factors,” “Special Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in our audited financial statements and the related notes included elsewhere in this prospectus, before making an investment decision.

OVERVIEW

We are a leading non-union, specialized freight company focused on providing auto transportation and logistics services. Formed in connection with this offering through the combination of the Founding Companies, five industry-leading operating companies, we will operate one of the largest auto transportation fleets in North America based upon information obtained from leadership of the Auto Haulers Association of America, utilizing roughly 1,130 auto transport vehicles and trailers on a daily basis, including 615 Company-owned transport vehicles and trailers, and employing 649 dedicated employees as of November 30, 2023. Prior to the completion of this offering, we have not operated as a combined company and are dependent upon this offering to complete the Combinations. From our 49 strategically located facilities across the United States, we offer a broad range of auto transportation and logistics services, primarily focused on transporting finished vehicles from automotive production facilities, marine ports of entry, or regional rail yards to auto dealerships around the country. We have developed a differentiated business model due to our scale, breadth of geographic coverage, and embedded customer relationships with leading auto original equipment manufacturing companies (“OEMs”). Our customers range from large, global auto companies, such as General Motors, BMW, Stellantis, and Mercedes Benz, to electric vehicle (“EV”) producers, such as Tesla and Rivian. Additional customers include auto dealers, auto auctions, rental car companies, and auto leasing companies. For the year ended December 31, 2023, we had pro forma combined total operating revenue of $ million, pro forma combined net income of $8.3 million, and pro forma combined EBITDA of $ million. Our pro forma combined financial results cover periods during which we were not under common control or management and, therefore, may not be indicative of our future financial or operating results. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for information regarding our use of EBITDA and a reconciliation to net income.

Our combined total operating revenue has grown at a compounded annual growth rate (“CAGR”) of approximately 15% from 2019 to 2023. We believe this historical growth is largely attributable to (i) market share shifting from union to non-union auto transportation and logistics companies, (ii) price increases resulting from industry-leading service levels provided to OEMs, coupled with significant trucking and rail capacity shortages, and (iii) OEMs partnering with auto transportation service providers with nationwide geographic coverage to service their growing network of dealerships. The COVID-19 pandemic created significant production headwinds for the automotive manufacturing sector due to supply chain disruptions and component shortages. As a result of these issues, domestic auto sales, which had averaged 17.2 million units annually in the four years prior to 2020, dropped to 14.5 million units in 2020 following the onset of the pandemic and declined to 13.8 million units in 2022 due to the supply chain issues and semiconductor shortages in that year. Despite the decrease in units, we increased our combined total operating revenue by $148.3 million from 2019 to 2023 as we benefited from market share gains and price increases. Industry production volumes are beginning to rebound, and are expected to be a continuing tailwind for the auto transportation and logistics industry throughout the next three to five years. We believe the combination of our executive management team, the management of the Founding Companies, and the fragmented nature of the auto transportation and logistics market will provide us with the capability and opportunity to continue to expand both organically and via effective tuck-in acquisitions.

1

Table of Contents

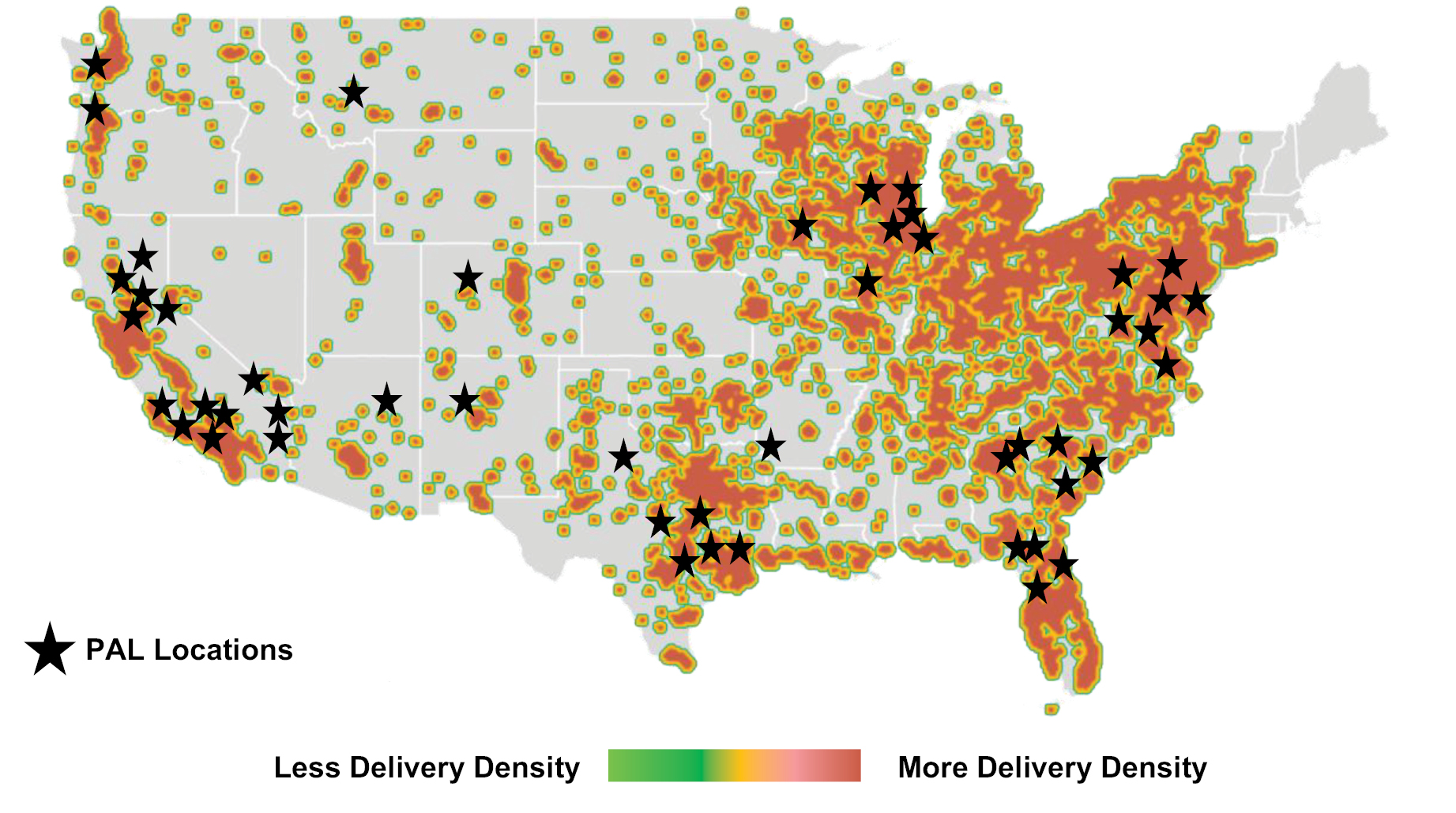

Source: Management estimates and Bureau of Transportation Statistics.

The above chart presents growth in our combined total operating revenue and combined total units delivered by the Founding Companies despite the significant decline in the seasonally adjusted annual rate (“SAAR”) of auto sales and the number of delivered units. We believe our growth will continue as production volumes increase to a more normalized level and industry tailwinds support growth over the next five years.

Corporate History and Structure

We were founded in June 2023 but have generated no revenue and have conducted no operations to date.

We will be comprised of five operating businesses and their respective affiliated entities, as applicable, operating under the following names: (i) Delta, (ii) Deluxe, (iii) Sierra, (iv) Proficient Transport, and (v) Tribeca.

Despite the fact the Founding Companies have worked in the industry for over thirty years, we have no experience operating as a combined company and will not operate as such until the closing of the Combinations. Thus, we have no combined corporate culture or institutional knowledge.

Immediately upon the closing of the Combinations, we will begin to integrate all our operations. While many portions of the businesses of each of the Founding Companies will remain separately managed, we have hired a new chief commercial officer who will be responsible for overseeing business development between the various parts of our business to assure coordination across the platform and to minimize conflicts of interest. Strategic decisions, including acquisitions and fleet expansion, will be made centrally. We also expect to centralize certain administrative functions at our headquarters in Jacksonville, Florida, including insurance, employee benefits, purchasing, accounting, treasury, and risk management.

However, there can be no assurance that we will be able to integrate the operations of the Founding Companies successfully or institute the necessary systems and procedures, including accounting and financial reporting systems, to manage the combined enterprise on a profitable basis. In addition, there can be no assurance that our recently assembled management team will be able to successfully manage the combined entity and effectively implement our operating or growth strategies.

Competitive Strengths

We believe the following key strengths have been instrumental in our success and position us well to continue growing our business and market share:

Ability to Capitalize on Favorable Industry Tailwinds. We, as well as the overall auto transportation and logistics subsector, stand to benefit from several distinct tailwinds impacting the market, including (i) recovering auto sales and production volumes, (ii) transportation equipment capacity shortages, (iii) a shift toward non-union auto transportation and logistics companies, (iv) financial pressures on smaller auto transportation and logistics companies,

2

Table of Contents

(v) increasing auto replacement rates, (vi) growth in EV consumption, and (vii) leaner supply chain models. We expect these secular and cyclical factors to drive volume growth, pricing improvements, margin expansion, and improving network efficiencies. For example, as a result of these favorable industry trends, our combined average revenue per unit delivered increased from $105 in 2016 to $139 in 2020 and $196 in 2023, representing a CAGR of approximately 9.3% from 2016 to 2023. We believe our competitive position will allow us to capitalize on these trends to an even greater extent than the general auto transportation and logistics subsector.

Scaled Provider of Auto Transportation and Logistics with a Large, Modern Fleet. Through the combination of the five Founding Companies, we will become one of North America’s largest providers of auto transportation and logistics services based upon data obtained from the U.S. Department of Transportation Safety and Fitness Electronic Records System and Transport Topics and information obtained from leadership of the Auto Haulers Association of America, with an established, nationwide geographic footprint. We will operate one of North America’s largest auto transportation and logistics networks with access to roughly 1,130 trucks, including 615 Company-owned tractors and trailers as of November 30, 2023, with an average age of approximately 5.8 years and approximately 5.6 years, respectively. Given our large scale and extensive infrastructure, we offer both network density and broad geographic coverage to better meet our customers’ transportation needs. Greater network density also leads to greater utilization of our transportation equipment, which results in greater profitability. We believe our scale and financial strength will provide us with access to capital necessary to consistently invest in our capacity, technology, and people to drive performance and growth and to comply with industry regulations. Our scale will also give us significant purchasing benefits in outsourced third-party capacity, fuel, equipment and maintenance, repair, and operational costs, lowering our costs compared to smaller competitors. Lastly, our network of 49 leased terminal locations provides an important local presence in select geographic regions.

Blue Chip Customer Base Comprised of Leading Automotive Original Equipment Manufacturers. We service 17 of the top 18 global OEMs by sales volume in 2022 that sell in the United States, and management estimates that our average customer tenure with our top 10 customers is over seven years. We possess multi-year contracts with each of our OEM customers. These contracts are generally neither exclusive nor do they have specified minimum levels of usage or revenue. Through the combination of the five Founding Companies, we believe there will be significant opportunities to cross-sell our services across our nationwide geographic footprint as OEMs continue to look for guaranteed, nationwide capacity.

Highly Experienced Management Team with Significant Industry Expertise. Our management team consists of industry veterans with significant experience operating in the transportation and logistics industry. Our Chief Executive Officer Richard O’Dell has over 23 years of experience operating in the transportation and logistics industry, having served as the former Chief Executive Officer of Saia, Inc. (NASDAQ: SAIA) (“Saia”), a transportation company providing less-than-truckload and other value-added services, including non-asset truckload, expedited and logistics services across North America, for 14 years. Randy Beggs, our President and Chief Operating Officer, has over 35 years operating in the auto transportation and logistics industry, having served as CEO of Proficient Auto Transport since 2018. Mr. O’Dell and Mr. Beggs will be supported by a highly talented group of tenured auto transportation and logistics veterans, who have an average of over 25 years of experience operating within the auto transportation and logistics subsector and broader trucking industry. We believe our leadership team is well positioned to execute our strategy and remains a key driver of our financial and operational success. Our leadership team will also benefit from the experience of the members of our board of directors (the “Board”), including James B. Gattoni, President and Chief Executive Officer of Landstar System, Inc., a worldwide, technology-enabled, asset-light provider of integrated transportation management solutions, and Douglas Col, the current Executive Vice President and Chief Financial Officer of Saia.

Leading Auto Transportation and Logistics Provider with Non-Unionized Employee Base. Our employee base comprises one of the largest pools of non-unionized drivers in the auto transportation and logistics industry based upon information obtained from the Auto Haulers Association of America. We believe our non-unionized operating model allows us to provide a higher level of service to our customers, while securing a cost advantage relative to our unionized competitors, and enabling us to attract and retain highly qualified, motivated individuals.

Barriers to Entry Driving Competitive Moat. The auto transportation and logistics industry is characterized by high equipment prices and specialized service requirements from OEMs. Furthermore, the ability to leverage a large network and broad customer base favors larger auto transportation and logistics companies that can maximize backhaul opportunities. Small auto transportation and logistics companies, such as one-truck operators with the ability to compete for wallet share within the general freight market, are losing share within the auto transportation and logistics sector as key customers are shifting volume toward auto transportation and logistics companies with the equipment capacity, scale, reputation, and density to service their more specific demands.

3

Table of Contents

Our Strategy

Our strategy is to be one of the nation’s leading providers of auto transportation and logistics services by focusing on broadening our platform and expanding our service offerings while maintaining the high quality of our existing services and increasing our operational efficiency. We intend to achieve this objective by executing the following business strategies.

Operating Strategy

Drive Organic Growth by Offering Committed Capacity and Consistently High-Quality Service to Expand Existing Relationships. We believe that the ability to commit transportation equipment capacity and timely, professional, and dependable service are the most important factors in maintaining and expanding customer relationships in the auto transportation and logistics industry. We intend to use our scale to offer customers committed transportation equipment capacity and our financial strength to consistently invest in our capacity. We intend to implement proven practices of the Founding Companies throughout our operations in areas as dispatching technology, driver training and professionalism, preventive maintenance, and safety. We intend to cross-sell the consistently high-quality service across our expanded platform to existing customers of our various Founding Companies.

Expand Service Offerings to Further Entrench Existing Customer Relationships and Win New Customers. We have strategically identified select customers looking for additional related services that would expand our relationships with these customers. For example, there is an opportunity to further expand our operations of regional auto storage yards on behalf of major automotive OEMs, which we believe will lead to future revenue opportunities. We believe that our expanded scale and other resources will permit us to acquire new customers that require greater auto transportation and logistics capacity and storage capabilities than those possessed by smaller operators. We also intend to utilize our geographic diversity to pursue additional business from existing customers that operate on a regional or national basis, such as auto OEMs, leasing companies, insurance companies, and automobile auction companies.

Achieve Operating Efficiencies. We intend to have the Founding Companies operate under their existing names and management teams but will seek to achieve operating efficiencies through improved asset utilization. Increased route density and backhaul opportunities lead to improved profitability, which we intend to achieve through the combination of the Founding Companies. We intend to operate all operations under one integrated transportation management software and route planning software, allowing us to have enhanced visibility and improve equipment utilization. The integration will begin immediately upon the closing of the Combinations, beginning with the accounting software. As three of the five Founding Companies already utilize the same accounting software, the costs for integration will be de minimis. Integration will also initially focus on consolidating route planning and dispatch software. Management expects this will not have significant associated expenses as we expect to utilize software already used by some of the Founding Companies. We also expect to realize cost savings by centralizing certain administrative functions at our headquarters in Jacksonville, Florida, including insurance, employee benefits, purchasing, accounting, treasury, and risk management. We believe the centralization of administrative functions can be achieved within 12 months of the closing of this offering and will not have significant associated expenses. Rather, such consolidation may incur financial benefits as administrative redundancies will be removed. We also believe there will be opportunities to use our purchasing power to seek improved pricing in areas such as purchased transportation, fuel, vehicles, and parts, and plan on creating a position tasked with overseeing collective purchasing. The expected costs of that integration are minimal, estimated to only be that of the new salary for one employee.

Maintain Local Expertise. We anticipate that members of management of the Founding Companies and companies to be acquired in the future will continue to maintain local control of their daily operations and work in coordination with each other, rather than compete, for business opportunities in their local markets. We believe this approach will enable us to take advantage of the local and regional market knowledge, name recognition, and customer relationships possessed by each acquired company while still allowing us to bring greater operating efficiency to the larger platform. We believe this structure will be attractive to owners who desire to benefit from being part of a larger platform while continuing to operate the companies they built.

Optimize Asset Flexibility. We intend to own and operate a significant percentage of the tractors and trailers we utilize in our daily operations, as opposed to primarily outsourcing to owner-operators or sub-haulers. For the year ended December 31, 2023, 34% of our combined revenue came from company-operated vehicles. We believe this approach allows us to maximize our profitability because it permits us to manage down underlying operating costs versus paying a higher fixed percentage of revenue to third-party haulers. This approach also provides more certainty

4

Table of Contents

to our customers because of the Company’s ability to provide guaranteed capacity in an increasingly complex market. By combining the five Founding Companies, we believe there will be more favorable purchasing opportunities with our vendors to allow us to add more Company trucks and Company drivers. At the same time, we expect to utilize a diversified approach to securing additional capacity to service our customers where we do not currently possess significant network density.

Acquisition Strategy

Expand Within Existing Geographic Markets and Select New Markets. The auto transportation and logistics industry is highly fragmented, with the majority of the industry represented by smaller, regional providers representing attractive tuck-in acquisition opportunities for us. We see opportunity with regional providers that overlap existing geographic footprints of the Founding Companies that would improve our network density in select geographies and add new customers. We believe there will be significant opportunities to acquire and integrate these smaller acquisition candidates into our existing infrastructure, providing opportunities for cost synergies and cross-selling. In addition, we may seek to vertically integrate our operations by acquiring companies that offer complementary services that we do not currently offer. There are several new geographic regions where we can expand our footprint via the acquisition of smaller regional providers. When pursuing an acquisition, we intend to acquire established, high-quality companies in markets where we can establish a leading market position to serve as core businesses into which additional operations may be consolidated.

The Combinations

Prior to this offering, Proficient Auto Logistics, Inc. entered into agreements to acquire in multiple, separate acquisitions five operating businesses and their respective affiliated entities, as applicable: (i) Delta, (ii) Deluxe, (iii) Sierra, (iv) Proficient Transport, and (v) Tribeca. The closing of the Combinations is expected to occur concurrently with the closing of this offering. The Founding Companies will be acquired for approximately $180.4 million in cash and approximately shares of our common stock, assuming an initial public offering price of $ per share. The stock consideration payable in certain of the Combinations transactions will vary depending on the initial public offering price in this offering but the aggregate number of shares of our common stock issuable in the Combinations will in no event be less than shares nor more than shares. A portion of the net proceeds from this offering will be used to pay the cash portion of the Combinations consideration payable to the equity holders of the Founding Companies. We will not close the acquisition of any of the Founding Companies unless we close the acquisition of all of the Founding Companies. Furthermore, the closing of the Combinations and this offering are conditioned on the closing of each other. Therefore, if we fail to close the Combinations, this offering will not close. Because of this structure, we have not yet operated as a combined company and do not currently have a combined operating history. See “Business — Overview of Founding Companies” and “Certain Relationships and Related Person Transactions — The Combinations with the Founding Companies” for additional information.

The above chart depicts our corporate structure after the completion of the Combinations.

5

Table of Contents

Summary Risk Factors

Investing in our common stock involves substantial risk. The risks are discussed more fully in the section titled “Risk Factors” immediately following this Prospectus Summary. These risks include, but are not limited to, the following:

• The Combinations and this offering are dependent upon each other. There can be no guarantee that the closing of the Combinations, and therefore this offering, will occur.

• We have not operated as a combined company, and we may not be able to successfully integrate the Founding Companies into one entity.

• Increased competition in the auto transportation and logistics industry could result in a loss of our market share or a reduction in our rates, which could have a material adverse effect on our operations.

• We are highly dependent on the automotive industry, and a decline in the automotive industry could have a material adverse effect on our operations.

• We are dependent on a small number of customers for a large portion of our revenue.

• Our business depends upon compliance with numerous government regulations.

• Arrangements with independent contractors expose us to risks that we do not face with employees.

• Any unionization efforts or labor regulation changes in certain jurisdictions in which we operate could divert management’s attention and could have a materially adverse effect on our operating results or limit our operational flexibility.

• Increases in driving associate compensation or difficulties attracting and retaining qualified driving associates could have a materially adverse effect on our profitability and the ability to maintain or grow our business.

• We will need to build or acquire integrated information technology systems, and our business may be seriously harmed if we fail to maintain, upgrade, enhance, protect, and integrate our information technology systems.

• Operational risks, including the risk of cyberattacks, may disrupt our business and could result in losses.

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended (the “JOBS Act”). As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

• being permitted to present only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure in this prospectus;

• reduced disclosure about our executive compensation arrangements;

• not being required to hold advisory votes on executive compensation or to obtain stockholder approval of any golden parachute arrangements not previously approved;

• an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; and

• an exemption from compliance with the requirements of the Public Company Accounting Oversight Board regarding the communication of critical audit matters in the auditor’s report on the financial statements.

6

Table of Contents

We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an “emerging growth company.” We would cease to be an emerging growth company on the date that is the earliest of (i) the last day of the fiscal year in which we have total annual gross revenue of $1.235 billion or more, (ii) the last day of our fiscal year following the fifth anniversary of the date of the completion of this offering, (iii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years, or (iv) the date on which we are deemed to be a large accelerated filer (as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). We will be deemed to be a “large accelerated filer” at such time that we (a) have an aggregate worldwide market value of common equity securities held by non-affiliates of $700.0 million or more as of the last business day of our most recently completed second fiscal quarter, (b) have been required to file annual and quarterly reports under the Exchange Act, for a period of at least 12 months, and (c) have filed at least one annual report pursuant to the Exchange Act. We may choose to take advantage of some but not all of these exemptions. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from other public companies in which you hold stock. Additionally, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. This allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to avail ourselves of this exemption, and, therefore, while we are an emerging growth company, we will not be subject to new or revised accounting standards at the same time that they become applicable to other public companies that are not emerging growth companies. As a result of this election, our financial statements may not be comparable to those of other public companies that comply with new or revised accounting pronouncements as of public company effective dates. We may choose to early adopt any new or revised accounting standards whenever such early adoption is permitted for private companies.

Corporate Information

Proficient Auto Logistics, Inc. was incorporated in Delaware on June 13, 2023. Our principal executive offices are located at 12276 San Jose Blvd, Suite 426, Jacksonville, FL 32223, and our telephone number is (904) 772-1175. Our website address is . Information contained on, or that can be accessed through, our website does not constitute a part of this prospectus and is not incorporated by reference herein. We have included our website address in this prospectus solely for informational purposes.

7

Table of Contents

THE OFFERING

Common stock offered by us | | shares. |

Option to purchase additional shares of common stock | | The underwriters have an option to purchase up to additional shares of common stock from us at the initial public offering price, less underwriting discounts and commissions. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. |

Common stock to be outstanding immediately after this offering | | shares (or shares if the underwriters exercise their option to purchase additional shares of our common stock in full). |

Use of proceeds | | We estimate that the net proceeds from this offering will be approximately $ million (or approximately $ million if the underwriters exercise their option to purchase additional shares of our common stock in full), based on the assumed initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover page of this prospectus, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| | | We intend to use the net proceeds from this offering, together with our existing cash and cash equivalents, as follows: |

| | | • approximately $ million will be used to pay the cash portion of the Combinations consideration payable to the equity holders of the Founding Companies; |

| | | • approximately $ will be used to pay expenses incurred in connection with the Combinations; and |

| | | • any remaining net proceeds will be used for general corporate purposes, which are expected to include working capital and future acquisitions. |

| | | See the section titled “Use of Proceeds” for additional information. |

Risk factors | | See the section titled “Risk Factors” beginning on page 13 and other information included in this prospectus for a discussion of factors you should consider carefully before deciding to invest in our common stock. |

Directed share program | | At our request, Stifel, Nicolaus & Company, Incorporated and its affiliates, or the DSP Underwriter, has reserved for sale, at the initial public offering price, up to 5% of the shares of our common stock offered hereby for officers, directors, employees and certain related persons. Any directed shares not purchased will be offered by the DSP Underwriter to the general public on the same basis as all other shares offered by this prospectus. We have agreed to indemnify the DSP Underwriter against certain liabilities and expenses, including liabilities under the Securities Act, in connection with the sales of the directed shares. See “Underwriting — Directed Share Program.” |

Proposed Nasdaq Global Market trading symbol | | “PAL” |

8

Table of Contents

The number of shares of our common stock that will be outstanding after the completion of this offering is based on 2,939,130 shares of Proficient common stock outstanding as of December 31, 2023, and includes shares of common stock deliverable in connection with the Combinations, assuming an initial public offering price of $ per share, which is the midpoint of the estimated price range set forth on the cover page of this prospectus, and excludes shares of common stock that will become available for future grants under our 2024 Long-Term Incentive Plan, which will become effective prior to and in connection with the completion of this offering.

Unless otherwise indicated, this prospectus assumes or gives effect to:

• the issuance of shares of common stock, assuming an initial public offering price of $ per share, upon the closing of this offering in connection with the consummation of the Combinations;

• a for stock split of our common stock, to be effected on , 2024;

• no exercise by the underwriters of their option to purchase additional shares; and

• the filing and effectiveness of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws, each of which will occur immediately prior to the closing of this offering.

9

Table of Contents

SUMMARY FINANCIAL DATA

The following summary historical financial data for Proficient Auto Logistics, Inc. (“Proficient”) (the accounting acquirer and registrant) as of and for the period from its inception through December 31, 2023 are derived from the audited financial statements of Proficient included elsewhere in this prospectus. The following summary historical financial data for Proficient Auto Transport, Inc. (“Proficient Transport”) (the accounting predecessor) for the years ended December 31, 2023, 2022 and 2021 are derived from the audited financial statements of Proficient Transport included elsewhere in this prospectus.

The summary unaudited pro forma financial data as of and for the year ended December 31, 2023 are derived from the unaudited pro forma financial statements included elsewhere in this prospectus. The unaudited pro forma financial data give effect to the completion of the Combinations and the completion of this offering and the use of the proceeds therefrom. The pro forma adjustments are based on currently available information and certain estimates and assumptions, and, therefore, the actual effects of the transactions reflected in the pro forma data may differ from the effects reflected below. However, management believes that the assumptions provide a reasonable basis for presenting the significant effects of these transactions as contemplated and that the pro forma adjustments give appropriate effect to those assumptions.

You should review the information below together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the Unaudited Pro Forma Financial Statements and the related notes beginning on page F-4 of this prospectus, and the audited financial statements of Proficient and Proficient Transport and the related notes all included elsewhere in this prospectus.

| | Proficient

From June 13, 2023

(Inception)

to December 31, 2023 |

Actual

(From

June 13, 2023

(Inception) to

December 31,

2023) | | Pro Forma

(Year Ended

December 31,

2023) |

| | | (dollars in thousands) |

Proficient | | | | | | | |

Total operating revenues | | $ | — | | | $ | |

Total operating expenses | | | 573 | | | | |

Total operating income | | | — | | | | |

Net income | | | (573 | ) | | | |

| | Proficient Transport |

| | | Year Ended December 31, |

| | | 2023 | | 2022 | | 2021 |

| | | (in thousands) |

Proficient Auto Transport, Inc. | | | | | | | | | |

Total operating revenues | | $ | 135,756 | | $ | 130,160 | | $ | 63,041 |

Total operating expenses | | | 125,403 | | | 115,466 | | | 60,515 |

Total operating income | | | 10,353 | | | 14,694 | | | 2,526 |

Net income | | | 7,156 | | | 10,399 | | | 3,166 |

EBITDA(1) | | | 12,877 | | | 16,983 | | | 6,924 |

10

Table of Contents

| | As of December 31, 2023 |

| | | Proficient | | Proficient

Transport | | Pro Forma |

| | | (in thousands) |

Balance Sheet Data: | | | | | | | | | |

Cash and cash equivalents | | $ | 458 | | $ | 4 | | $ | |

Total assets | | | 4,395 | | | 42,995 | | | |

Long-term debt, less current portion net | | | — | | | 5,036 | | | |

Stockholders’ and Members’ equity (deficit) | | | 389 | | | 7,753 | | | |

11

Table of Contents

Summary Individual Founding Company Financial Data

The summary historical financial data as of and for the years ended December 31, 2023, 2022 and 2021 for each of the Founding Companies are derived from the audited financial statements of each such Founding Company included elsewhere in this prospectus.

You should review the information below together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements of each of the Founding Companies and the related notes included elsewhere in this prospectus. These summary historical financial results may not be indicative of our future financial or operating results.

| | Year Ended December 31, |

| | | 2023 | | 2022 | | 2021 |

| | | (in thousands) |

Proficient Auto Transport, Inc. | | | | | | | | | | |

Total operating revenues | | $ | 135,756 | | $ | 130,160 | | $ | 63,041 | |

Total operating expenses | | | 125,403 | | | 115,466 | | | 60,515 | |

Total operating income | | | 10,353 | | | 14,694 | | | 2,526 | |

EBITDA(1) | | | 12,877 | | | 16,983 | | | 6,924 | |

Net income | | | 7,156 | | | 10,399 | | | 3,166 | |

| | | | | | | | | | | |

Delta Automotive Services, Inc. | | | | | | | | | | |

Total operating revenues | | $ | 55,116 | | $ | 44,643 | | $ | 33,451 | |

Total operating expenses | | | 51,199 | | | 41,596 | | | 35,135 | |

Total operating income | | | 3,917 | | | 3,047 | | | (1,684 | ) |

EBITDA(1) | | | 11,421 | | | 10,347 | | | 5,245 | |

Net income | | | 3,701 | | | 3,659 | | | (994 | ) |

| | | | | | | | | | | |

Deluxe Auto Carriers, Inc. | | | | | | | | | | |

Total operating revenues | | $ | 94,682 | | $ | 76,460 | | $ | 59,710 | |

Total operating expenses | | | 92,500 | | | 74,473 | | | 61,677 | |

Total operating income | | | 2,182 | | | 1,987 | | | (1,967 | ) |

EBITDA(1) | | | 7,752 | | | 12,975 | | | 8,124 | |

Net income | | | 1,421 | | | 5,907 | | | (871 | ) |

| | | | | | | | | | | |

Sierra Mountain Group, Inc. | | | | | | | | | | |

Total operating revenues | | $ | 74,570 | | $ | 73,767 | | $ | 69,337 | |

Total operating expenses | | | 70,125 | | | 71,727 | | | 63,667 | |

Total operating income(2) | | | 4,445 | | | 2,040 | | | 5,670 | |

EBITDA(1) | | | 5,429 | | | 2,961 | | | 6,722 | |

Net income | | | 3,950 | | | 1,388 | | | 4,850 | |

| | | | | | | | | | | |

Tribeca Automotive Inc. | | | | | | | | | | |

Total operating revenues | | $ | 54,756 | | $ | 50,108 | | $ | 44,635 | |

Total operating expenses | | | 50,039 | | | 49,646 | | | 49,941 | |

Total operating income | | | 4,717 | | | 462 | | | (5,306 | ) |

EBITDA(1) | | | 8,896 | | | 6,925 | | | (116 | ) |

Net income | | | 4,392 | | | 699 | | | (5,148 | ) |

12

Table of Contents

RISK FACTORS

Investing in our common stock involves a high degree of risk. Before deciding to invest in shares of our common stock, you should carefully consider the risks described below, together with the other information contained in this prospectus, including in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in our audited financial statements and the related notes included elsewhere in this prospectus. We cannot assure you that any of the events discussed below will not occur. These events could adversely impact our business, financial condition, results of operations and prospects. If that were to happen, the trading price of our common stock could decline, and you could lose all or part of your investment.

Risks Related to Our Business and Operations

The Combinations and this offering are dependent upon each other. There can be no guarantee that the closing of the Combinations, and therefore this offering, will occur.

Prior to this offering, Proficient entered into agreements to combine with each of the Founding Companies. This offering is conditioned on the closing of the Combinations with each of the Founding Companies. Therefore, if we fail to close the Combinations, this offering will not close. There can be no assurance that all of the conditions precedent to the Combinations will be satisfied or waived, or, if satisfied or waived, when they will be satisfied or waived. Accordingly, there is no guarantee that the closing of the Combinations or this offering will occur.

We have not operated as a combined company, and we may not be able to successfully integrate the Founding Companies into one entity.

The Founding Companies have historically operated independently of one another. There can be no assurance that we will be able to integrate the operations of the Founding Companies successfully or institute the necessary systems and procedures, including accounting and financial reporting systems, to manage the combined enterprise on a profitable basis and report the results of operations of the combined entities on a timely basis. In addition, there can be no assurance that our recently assembled management team will be able to successfully manage the combined entity and effectively implement our operating or growth strategies. Our pro forma combined financial results cover periods during which we were not under common control or management and, therefore, may not be indicative of our future financial or operating results. Our success will depend on management’s ability to integrate the companies successfully.

Increased competition in the auto transportation and logistics industry could result in a loss of our market share or a reduction in our rates, which could have a material adverse effect on our operations.

The auto transportation and logistics market is a highly competitive and fragmented industry. We currently compete with other auto carriers of varying sizes, logistics, brokerage and transportation services providers of varying sizes, as well as with railroads and independent owner-operators. Competition for the freight we transport or manage is based primarily on service, efficiency, available capacity and, to some degree, on freight rates alone. Our competitors periodically reduce their freight rates to gain business, especially when economic conditions are present, which negatively impact customer shipping volumes, truck capacities, or operating costs. In addition, certain of the Company’s customers may develop new methods for hauling vehicles, such as using local drive-away services to facilitate local delivery of products. Railroads, which specialize in long-haul transportation, may be able to provide delivery services at costs to customers that are less than the long-haul delivery cost of our services. Additionally, the continuing trend toward consolidation in the trucking industry may result in more large carriers with greater financial resources, and the development of new methods or technologies for hauling vehicles could lead to increased investments to remain competitive, either of which may lead to new market entrants and increased competition overall. If we lose market share to these competitors or have to reduce our rates in order to retain our market share, our financial condition and results of operations could be materially and adversely affected.

We are highly dependent on the automotive industry and a decline in the automotive industry could have a material adverse effect on our operations.

The automotive transportation market in which we operate is dependent upon the volume of new automobiles, sport utility vehicles (“SUVs”), and light trucks manufactured, imported and sold by the automotive industry in the United States, Canada, and Mexico. The automotive industry is highly cyclical, and the demand for new automobiles, SUVs and light trucks is directly affected by such external factors as general economic conditions in the

13

Table of Contents

United States, Canada and Mexico, unemployment rates, labor shortages or strikes, consumer confidence, government policies, continuing activities of war, terrorist activities and the availability of affordable new car financing. As a result, our results of operations could be adversely affected by downturns in the general economy and in the automotive industry, and by changing consumer preferences in purchasing new automobiles, SUVs and light trucks or the overall financial condition of our major customers. A significant decline in the volume of automobiles, SUVs and light trucks manufactured, imported and sold in the United States could have a material adverse effect on our operations.

We are dependent on a small number of customers for a large portion of our revenue.

Historically, a select group of our customers have made up a majority of our revenue. Specifically, for the year ended December 31, 2023, our top five customers accounted for 59.6% of our combined total operating revenue and our top ten customers accounted for 84.3% of our combined total operating revenue. General Motors Company accounted for 25.6% of our combined total operating revenue, Stellantis N.V. accounted for 8.9% of our combined total operating revenue, BMW accounted for 8.9% of our combined total operating revenue, Mercedes Benz accounted for 8.4% of our combined total operating revenue and Toyota accounted for 7.8% of our combined total operating revenue for the year ended December 31, 2023. There is no assurance any of our customers, including this select group of customers, will continue to utilize our services, renew our existing contracts, or continue at the same volume levels. Despite the existence of contractual arrangements, certain of our customers may engage in competitive bidding processes that could negatively impact our contractual relationships. A loss of any of these customers would have a material adverse effect on the Company’s results of operations and financial condition.

Our business depends upon compliance with numerous government regulations.

Our operations are regulated and licensed by various federal, state, and local transportation agencies in the United States. We are subject to licensing and regulation by the U.S. Department of Transportation (the “DOT”) for the transportation of property. The DOT prescribes qualifications for acting in this capacity, including certain surety bonding requirements. We also have and maintain other licenses as required by law. In addition to the DOT, various federal and state agencies exercise broad regulatory powers over the transportation industry, generally governing such activities as operations of and authorization to engage in motor carrier freight transportation, safety, contract compliance, insurance requirements, tariff and trade policies, taxation, and financial reporting.

We are audited periodically by the DOT to ensure that we are in compliance with various safety, hours-of-service, and other rules and regulations. If we were found to be out of compliance or receive an unsatisfactory DOT safety rating, the DOT could restrict or otherwise materially adversely impact our business, financial conditions and results of operations.

We could become subject to new or more restrictive regulations, such as regulations relating to U.S. Environmental Protection Agency mandated engine emissions requirements, drivers’ hours of service, occupational safety and health, ergonomics, cargo security, collective bargaining, and other matters affecting safety or operating methods. Our drivers also must comply with the safety and fitness regulations promulgated by the DOT, including those relating to drug and alcohol testing and hours of service. Compliance with all such regulations could substantially require changes in our operating practices, influence the demand for auto transportation and logistics services, reduce equipment and driver productivity and our load factor, and the costs of compliance could incur significant additional expenses.

Any such change in an applicable regulation or ruling in a judicial proceeding could have a material adverse effect on our business. See “Business — Government Regulation and Environmental Matters.”

We cannot predict the impact that future regulations may have on our business. Our failure to maintain required permits or licenses, or to comply with applicable regulations, could result in substantial fines or revocation of our operating permits and licenses.

Our engagement of owner-operators to provide a portion of our capacity exposes us to different risks than we face with our company drivers.

We face a complex and increasingly stringent regulatory and statutory scheme relating to wages, classification of employees and alternate work arrangements. Tax and other regulatory authorities, as well as owner-operators themselves, have increasingly asserted that owner-operators within our industry are employees, rather than independent contractors. Automotive transportation companies have been, and may continue to be, subject to lawsuits alleging that

14

Table of Contents

their drivers were misclassified as independent contractors rather than employees. Further, class actions and other lawsuits have been filed against us and others in our industry seeking to reclassify owner-operators as employees for a variety of purposes, including workers’ compensation and health care coverage. If any such cases are judicially determined in a manner adverse to us or our businesses, there could be an adverse impact on our operations in the effected jurisdictions. Taxing and other regulatory authorities and courts apply a variety of standards in their determination of independent contractor status. If the owner-operators we contract with are deemed employees, we could incur additional exposure under laws for federal and state tax, workers’ compensation, unemployment benefits, labor, employment and tort. The exposure could include prior period compensation, as well as potential liability for employee benefits and tax withholdings. For example, Sierra and Deluxe, in 2022 and 2020, respectively, reclassified their owner-operators in California as sub-haulers and employees, as appropriate. While the entities experienced increased expenses associated with additional employees, the reclassification did not impact revenue recognition. We continue to evaluate the classification of drivers to ensure compliance with all relevant laws. While we continue to engage owner-operators where permissible and do not believe any future reclassifications would be material, we cannot guarantee an immaterial impact. Any such change in applicable regulation or ruling in a judicial proceeding could have a material adverse effect on our business. See “Business — Government Regulation and Environmental Matters.”

In addition, our lease contracts with owner-operators are governed by federal leasing regulators, which impose specific requirements on us and owner-operators retained by us. Litigation alleging violations of lease agreements or contractual terms could result in adverse decisions against us.

There has been no independent valuation of the Founding Companies to support the consideration that we agreed to pay, which means the Founding Companies may be worth less than the purchase price.

The consideration payable for the Founding Companies has been determined by Proficient without independent valuations, appraisals or fairness opinions. In determining and negotiating the consideration to be paid in the Combinations to each of the individual Founding Companies, Proficient relied on the experience and judgment of its founders, Ross Berner and Mark McKinney, who leveraged their 20 years of experience in investing in public securities across multiple industries, including transportation and logistics companies. Their evaluation considered a variety of metrics, including a review of enterprise value/EBITDA, enterprise value/EBITDA-capex, free cash flow multiples and sustainability of revenues and operating margins. Despite the detailed evaluation led by Messrs. Berner and McKinney, this valuation is still subjective. Thus, the Founding Companies may have a value that is lower than the agreed upon consideration.

We may be adversely impacted by fluctuations in the price and availability of fuel and our ability to collect fuel surcharges.

We must purchase large quantities of fuel to operate our business, which is a significant operating expense. The price and availability of fuel can be highly volatile and can be impacted by factors beyond our control, such as natural disasters, adverse weather conditions, political events or international conflicts, price and supply decisions by oil producing countries, or changes to trade agreements. An increase in fuel prices or diesel fuel taxes, or any change in federal or state regulations that results in such an increase, could have an adverse effect on our operating results.

We typically are able to pass through a portion of our fuel costs to our customers. Changes in fuel costs will not result in a direct offset to fuel surcharges due to the nature of the calculation of fuel surcharges, which is customer-specific and fluctuates as a result of miles driven, changes in the number and types of units hauled per customer, as well as the relationship of the national average cost of fuel (the national average diesel price index) or other contractually determined customer index benchmarks compared to actual fuel prices paid at the pump. In addition, depending on the base rate and fuel surcharge levels agreed upon by our customers, there could be a delay in reflecting increases in our surcharges to customers resulting from a rapid and significant change in the cost of diesel fuel, which could also have a material adverse effect on our operating results.

15

Table of Contents

We may not be able to secure additional financing on favorable terms, or at all, to meet our future capital needs.

We require substantial amounts of cash to cover operating expenses as well as to fund capital expenditures, working capital changes, principal and interest payments on debt obligations, lease payments and tax payments. In the future, we may require additional capital to cover such expenses. Any debt financing obtained by us in the future may contain, certain restrictive covenants that limit our ability, among other things, to engage in certain activities that are in our long-term best interests, including our ability to:

• incur additional indebtedness;

• incur certain liens;

• consolidate, merge or sell or otherwise dispose of our assets;

• make investments, loans, advances, guarantees and acquisitions;

• enter into swap agreements;

• redeem, repurchase or refinance our other indebtedness; and

• amend or modify our governing documents.

Such covenants may make it more difficult for us to operate our business, obtain additional capital and pursue business opportunities, including potential acquisitions. If we are unable to obtain adequate financing or financing on terms satisfactory to us, when we require it, our ability to continue to grow or support our business and respond to business challenges could be significantly limited.

Our operations expose us to potential environmental liabilities.

Our operations are subject to a number of federal, state and local laws and regulations relating to the storage of petroleum products and hazardous materials, as well as safety regulations relating to the upkeep and maintenance of our vehicles. In particular, our operations are subject to federal, state and local laws and regulations governing leakage from salvage vehicles, waste disposal, the handling of hazardous substances, environmental protection, remediation, workplace exposure and other matters. It is possible that an environmental claim could be made against us or any of the Founding Companies or that one or more of them could be identified by the Environmental Protection Agency, a state agency or one or more third parties as a potentially responsible party under federal or state environmental laws. If we or any of the Founding Companies were to be named a potentially responsible party, we could be forced to incur substantial investigation, legal and remediation costs, which could have a material adverse effect on our business, financial condition and results of operations. See “Business — Government Regulation and Environmental Matters.”

We may be adversely impacted by work stoppages and other labor matters.

A substantial number of the employees of our largest customers are members of trade unions and are employed under the terms of collective bargaining agreements. During 2023, labor strikes by the United Auto Workers of its employees at certain facilities of Ford, General Motors and Stellantis caused a 45-day shutdown of the affected manufacturing operations. While the limited scope and duration of this strike did not have a material adverse effect on our revenues or profitability, future work stoppages at our automotive customers or their suppliers could negatively impact our revenues and profitability.

Any unionization efforts or labor regulation changes in certain jurisdictions in which we operate could divert management’s attention and could have a materially adverse effect on our operating results or limit our operational flexibility.

We consider our relationship with our employees to be satisfactory, and none of our employees are represented by a union in collective bargaining with us. However, efforts could be made by employees and third parties from time to time to unionize portions of our workforce. Any unionization efforts, collective bargaining agreements or work stoppages could have a materially adverse effect on our operating results or limit our operational flexibility.

16

Table of Contents

Sustained periods of severe abnormal weather can have a material adverse effect on our business.

Certain weather conditions can disrupt our operations, which will negatively affect revenues on a particular business day that may not be recouped in the future. Inefficiencies in our loading, unloading and transit times associated with cleaning snow off of our rigs before use and cleaning snow off of vehicles being transported before and after transporting them, increased lodging costs due to hours of service restrictions for our drivers and premium (overtime) pay required in order to complete the unit movements over weekends to make up for the inefficiencies caused by delayed delivery of on-ground customer inventories may also have a negative impact on earnings.

There can be no assurance that we will continue to manage our business effectively when influenced by severe weather events or that severe weather events will not have a material adverse effect on our business, financial condition and results of operations.

Our growth strategy includes acquisitions, diversification into new specialty transportation businesses and expansion into new geographic markets. We are subject to various risks in pursuing this growth strategy and we may have difficulty in integrating businesses we acquire and may be subject to unexpected liabilities.

Our business strategy includes a growth strategy in-part dependent on acquisitions, diversification into specialty transportation businesses and expansion into new geographic markets.

However, we may not be able to identify suitable acquisition candidates in the future, and we may never realize expected business opportunities and growth prospects from acquisitions. Acquisitions involve numerous risks, including, but not limited to: difficulties in integrating the operations, technologies and products acquired; the diversion of our management’s attention from other business concerns; current operating and financial systems and controls may be inadequate to deal with our growth; and the risks of entering markets in which we have limited or no prior experience and the loss of key employees. Furthermore, even if we are able to identify attractive acquisition candidates, we may not be able to obtain the financing to complete such acquisitions.

If these factors limit our ability to integrate the operations of our acquisitions, successfully or on a timely basis, our expectations of future results of operations may not be met. In addition, our growth and operating strategies for any business we acquire may be different from the strategies that such business currently is pursuing. If our strategies are not the appropriate strategies for a company we acquire, it could have a material adverse effect on our business, financial condition and results of operations. Further, there can be no assurance that we will be able to maintain or enhance the profitability of any acquired business or consolidate the operations of any acquired business to achieve cost savings.

Furthermore, there may be liabilities that we do not discover in the course of performing due diligence investigations on each company or business we have already acquired or may acquire in the future. Such liabilities could include those arising from employee benefits contribution obligations of a prior owner or noncompliance with, or liability pursuant to, applicable federal, state or local environmental requirements by prior owners for which we, as a successor owner, may be responsible. In addition, there may be additional costs relating to acquisitions including, but not limited to, possible purchase price adjustments. Rights to indemnification by sellers of assets to us, even if obtained, may not be enforceable, collectible or sufficient in amount, scope or duration to fully offset the possible liabilities associated with the business or property acquired. Any such liabilities, individually or in the aggregate, could have a material adverse effect on our business.

We currently intend to finance future acquisitions by using a combination of common stock, cash and debt. To the extent we issue shares of common stock to finance future acquisitions, the interests of existing stockholders will be diluted. If the common stock does not maintain a sufficient market value, or if potential acquisition candidates are unwilling to accept common stock as part of the consideration for the sale of their businesses, we may be required to utilize more of our cash resources, if available, in order to pursue our acquisition program. Upon consummation of the offering and application of the proceeds therefrom, we expect to have $ million of net proceeds remaining for future acquisitions and working capital. See “Use of Proceeds.” If we do not have sufficient cash resources, our growth could be limited unless we are able to obtain additional capital through debt or equity financings. There can be no assurance that we will be able to obtain the financing we will need for our acquisition program on acceptable terms, or at all. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Proficient Auto Transport, Inc. — Liquidity and Capital Resources.”

17

Table of Contents

We currently generate most of our revenue from the transportation of vehicles. However, we may grow our business by diversifying and entering into new specialty transportation businesses. To the extent we enter into such businesses, we will face numerous risks and uncertainties, including risks associated with the possibility that we have insufficient expertise to engage in such activities profitably or without incurring inappropriate amounts of risk, the required investment of capital and other resources and the loss of existing clients due to the perception that we are no longer focusing on our core business. Entry into certain new specialty transportation businesses may also subject us to new laws and regulations with which we are not familiar, or from which we are currently exempt, and may lead to increased litigation and regulatory risk. If a new specialty transportation business generates insufficient revenue or if we are unable to efficiently manage our expanded operations, our results of operations could be materially adversely affected.

Technological advances are facilitating the development of driverless vehicles, which may materially harm our business.

Driverless vehicles are being developed for the transportation and automotive industries that, if widely adopted, may materially harm our business. The eventual timing of availability of driverless vehicles is uncertain due to regulatory requirements, additional technological requirements, and uncertain consumer acceptance of these vehicles. The effect of driverless vehicles on the transportation and automotive industries is uncertain and could include changes in the level of new and used vehicles sales, the price of new vehicles, and the demand for our services, any of which could materially and adversely affect our business.

Because we have not operated as a combined company, we do not have a long-term reputation of success.

As we have not operated as a combined company, we do not have the long-term reputation of success that other well-established companies have. Particularly in the transportation market, in which trust is important, the absence of a proven reputation could make it more difficult to establish new customers. As a result, we will rely more heavily on the brand value and reputation of the individual Founding Companies.

The transportation infrastructure continues to be a target of terrorists.

Because transportation assets continue to be a target of terrorists, governments around the world are adopting or are considering adopting stricter security requirements that will increase operating costs and potentially slow service for businesses, including those in the transportation industry. These security requirements are not static, but change periodically as the result of regulatory and legislative requirements, imposing additional security costs and creating a level of uncertainty for our operations.

Ongoing insurance and claims expenses could result in significant expenditures and reduce and cause volatility in our earnings.

We, by the nature of our operations, are exposed to the potential for a variety of claims, including personal injury claims, vehicular collisions and accidents, alleged violations of federal and state labor and employment laws, such as class-action lawsuits alleging wage and hour violations and improper pay, commercial and contract disputes, cargo loss and property damage claims. Each of the Founding Companies has maintained, and we expect to maintain, insurance coverage with established insurance companies at levels they or we deem adequate. The trucking business has experienced significant increases in the cost of liability insurance, in the size of jury verdicts in personal injury cases arising from trucking accidents and in the cost of settling such claims. If the number or severity of future claims continues to increase, claims expenses might exceed historical levels or could exceed the amounts of our insurance coverage or the amount of our reserves for self-insured claims or deductible levels, which could materially adversely affect our financial condition, results of operations, liquidity and cash flows.