UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-04875

Name of Registrant: Royce Value Trust, Inc.

Address of Registrant: 745 Fifth Avenue

New York, NY 10151

| Name and address of agent for service: | John E. Denneen, Esq. |

| | 745 Fifth Avenue |

| | New York, NY 10151 |

Registrant's telephone number, including area code: (212) 508-4500

Date of fiscal year end: December 31, 2021

Date of reporting period: January 1, 2021– June 30, 2021

Item 1. Reports to Shareholders.

Royce Closed-End Funds 2021 Semiannual

Review and Report to Stockholders

June 30, 2021

Royce Global Value Trust

Royce Micro-Cap Trust

Royce Value Trust

| | | | |

| | A Few Words on Closed-End Funds | |

| | | | |

| | Royce Investment Partners manages three closed-end funds: Royce Global Value Trust, which invests primarily in companies with headquarters outside of the United States; Royce Micro-Cap Trust, which invests primarily in micro-cap securities; and Royce Value Trust, which invests primarily in small-cap securities. A closed-end fund is an investment company whose shares are listed and traded on a stock exchange. Like all investment companies, including open-end mutual funds, the assets of a closed-end fund are professionally managed in accordance with the investment objectives and policies approved by the fund’s Board of Directors. A closed-end fund raises cash for investment by issuing a fixed number of shares through initial and other public offerings that may include shelf offerings and periodic rights offerings. Proceeds from the offerings are invested in an actively managed portfolio of securities. Investors wanting to buy or sell shares of a publicly traded closed-end fund after the offerings must do so on a stock exchange, as with any publicly traded stock. Shares of closed-end funds frequently trade at a discount to their net asset value. This is in contrast to openend mutual funds, which sell and redeem their shares at net asset value on a continuous basis. | |

| | | | |

| | A Closed-End Fund Can Offer Several Distinct Advantages | |

| | • | A closed-end fund does not issue redeemable securities or offer its securities on a continuous basis, so it does not need to liquidate securities or hold uninvested assets to meet investor demands for cash redemptions. | |

| | • | In a closed-end fund, not having to meet investor redemption requests or invest at inopportune times can be effective for value managers who attempt to buy stocks when prices are depressed and sell securities when prices are high. | |

| | • | A closed-end fund may invest in less liquid portfolio securities because it is not subject to potential stockholder redemption demands. This is potentially beneficial for Royce-managed closed-end funds, with significant investments in small- and micro-cap securities. | |

| | • | The fixed capital structure allows permanent leverage to be employed as a means to enhance capital appreciation potential. | |

| | • | Royce Micro-Cap Trust and Royce Value Trust distribute capital gains, if any, on a quarterly basis. Each of these Funds has adopted a quarterly distribution policy for its common stock. | |

| | | | |

| | We believe that the closed-end fund structure can be an appropriate investment for a long-term investor who understands the benefits of a more stable pool of capital. | |

| | | | |

| | Why Dividend Reinvestment Is Important | |

| | A very important component of an investor’s total return comes from the reinvestment of distributions. By reinvesting distributions, our investors can maintain an undiluted investment in a Fund. To get a fair idea of the impact of reinvested distributions, please see the charts on pages 56 and 57. For additional information on the Funds’ Distribution Reinvestment and Cash Purchase Options and the benefits for stockholders, please see page 58 or visit our website at www.royceinvest.com. | |

| | | | |

| | Managed Distribution Policy | |

| | The Board of Directors of each of Royce Micro-Cap Trust and Royce Value Trust has authorized a managed distribution policy (“MDP”). Under the MDP, Royce Micro-Cap Trust and Royce Value Trust pay quarterly distributions at an annual rate of 7% of the average of the prior four quarter-end net asset values, with the fourth quarter being the greater of these annualized rates or the distribution required by IRS regulations. With each distribution, the Fund will issue a notice to its stockholders and an accompanying press release that provides detailed information regarding the amount and composition of the distribution (including whether any portion of the distribution represents a return of capital) and other information required by a Fund’s MDP. You should not draw any conclusions about a Fund’s investment performance from the amount of distributions or from the terms of a Fund’s MDP. A Fund’s Board of Directors may amend or terminate the MDP at any time without prior notice to stockholders; however, at this time there are no reasonably foreseeable circumstances that might cause the termination of any of the MDPs. | |

| | | | |

| | This page is not part of the 2021 Semiannual Report to Stockholders | |

| | | | |

Table of Contents

This page is not part of the 2021 Semiannual Report to Stockholders

Letter to Our Stockholders

WHY TWO MAXIMS ARE ESPECIALLY RELEVANT NOW

The first six months of 2021 offered an important reminder that the economy and the equity markets—small cap stocks included—advance at their own speeds. The first quarter of 2021 saw economic acceleration in the form of U.S. real GDP growth of 6.3%, a considerable increase from 4Q20’s also strong 4.3% mark. This growth continued into 2Q21, when real GDP came in at 6.5%, both quarters in line with current consensus estimates of 6-7% annual growth. Over the same period, small cap returns, as measured by the Russell 2000 Index, moved at the opposite pace, from 31.4% in 4Q20 to 12.7% in 1Q21, and finally to 4.3% for 2Q21.

Decelerating Market, Accelerating Economy

Russell 2000 Index Quarterly Returns vs. U.S. Real GDP Growth (annualized, quarter over quarter)

Source: Bloomberg

These seemingly disconnected results are actually more closely connected than they appear. They also provide us with the

opportunity to remind investors of an important investment maxim: that it often makes sense to discount the relevance of current economic news when thinking about how to invest. The stock market has a well-founded reputation as a forward-looking force, often traveling six to 12 months ahead of economic results. This dynamic highlights why the best returns often come when current economic news seems dire or pedestrian. March 2020 provided just the latest example of this long-running phenomenon. And—as the direction of small-cap’s last three quarterly returns makes clear—the other side of this relationship is also frequently accurate: prospective equity returns can be far more subdued when the economy is most robust. (There is a silver lining for active managers to this market-economy dynamic, but more on that later.) Seen from this perspective, the first half’s simultaneous economic acceleration and small-cap deceleration was, in a period that continues to provide plenty of atypical behavior, reassuringly conventional.

The first half of the year also came to a close with nearly every trend established within the equity markets from the March 2020 troughs still firmly in place. To wit: small cap finished ahead of large cap for the year-to-date period ended 6/30/21, as measured by the Russell 2000 (+17.5%) and Russell 1000 (+15.0%) indexes, thus extending the leadership

| 2 | This page is not part of the 2021 Semiannual Report to Stockholders | Past performance is no guarantee of future results. |

LETTER TO OUR STOCKHOLDERS

Our research delves into equity returns during previous periods of strong nominal GDP growth, current valuation levels, and historical small cap returns patterns, all of which have given us what we admit is an arguably paradoxical point of view: a strong sense of guarded optimism.

shift that began more than 15 months ago. Similarly, the Russell 2000 Value Index, which advanced 26.7%, solidified its nascent market cycle advantage over the Russell 2000 Growth Index—which rose 9.0%—following nearly a decade of underperformance—an unprecedented length of time for growth to outpace value since the inception of the style indexes. Also within small cap, cyclical sectors maintained a convincing lead over their defensive counterparts.

Will these trends continue? We think they will. What we flesh out in this letter, then, is our case for extended small-cap leadership and, within the asset class, ongoing outperformance for value. Our research delves into equity returns during previous periods of strong nominal GDP growth, current valuation levels, and historical small cap returns patterns, all of which have given us what we admit is an arguably paradoxical point of view: a strong sense of guarded optimism.

BE AWARE OF RECENCY BIAS

Some readers may think we are on shaky ground in arguing that small cap’s first-half leadership looks built to last. And there are reasons that might appear to support the notion that leadership has moved back to large caps. After its historic one-year rally through the end of March 2021—which included three consecutive quarters outperforming large caps—small cap’s advance moderated. The Russell 2000 also fell behind its large-cap sibling during the second quarter of 2021, up 4.3% versus 8.5% for the Russell 1000. And while the Russell 2000 established its latest all-time peak on March 15th, the Russell 1000 reached its latest peak as recently as July 26th, after making previous new highs several times toward the end of the second quarter. In this context, we suspect a certain amount of recency bias may be preventing small-cap skeptics from seeing just how strong

first-half performance was—and not just for small cap, but for cyclicals, small-cap value, and micro-cap stocks (which rose 29.0%, as measured by the Russell Microcap Index). For example, the Russell 2000’s 17.5% gain was well above the index’s rolling monthly average six-month return of 6.7% since its inception (12/31/78). History also shows that intra-cycle leadership shifts occur with some regularity during market cycles, as do changes in the tempo of performance. For example, after small caps experienced a very strong absolute and relative recovery in 2009, a digestion period followed in which returns were negative over the next six months before the asset class resumed a positive pace and held on to market leadership.

In addition, it’s worth noting that first-half returns being highest for the smallest capitalization asset classes (as well as being significantly in value’s favor) lines up exactly as we would expect during a period of widespread economic recovery. Equally important, we see little on the horizon in the economy, the market itself, or—and this is always most relevant to us—in our analysis of companies and conversations with management teams—to suggest that small cap’s leadership phase has run its course.

HAS SMALL-CAP’S RUN ONLY JUST BEGUN?

The growing economy underpins an important part of our optimism for small cap’s continued leadership over large cap. Notwithstanding ever-present sources of concern, our bottom-up view of the economy, which we glean from analyzing a wide swath of companies, shows that the U.S. in particular continues to skew heavily toward expansion. The U.S. consumer, whose spending comprises roughly 70% of our economy, is financially flush. With notably strong consumer balance sheets and low mortgage rates, the housing market remains healthy while

| Past performance is no guarantee of future results. | This page is not part of the 2021 Semiannual Report to Stockholders | 3 |

LETTER TO OUR STOCKHOLDERS

also boasting favorable long-term demographic trends. Retail and restaurant sales are increasing steadily, passenger air travel remains on the rise, and roads and highways are busy. We would also add lower unemployment, and the potential boost—after the requisite political wrangling—of additional fiscal stimulus, much of it in the form of long needed infrastructure spending, to this list of positives.

And while past performance is no guarantee of future results, history is admirably clear about the pattern of U.S. equity leadership when the economy expanded. During prior periods of robust economic growth, small caps have enjoyed a decided performance edge over their large cap siblings. When nominal U.S. GDP growth exceeded 5% in year-over-year periods, the Russell 2000 beat the Russell 1000 65% of the time with an average annual return of 22.1% versus 17.0%. This is especially relevant to the current environment because consensus projections call for nominal GDP growth in the 8-10% range for 2021 and 5-7% for 2022.

Small Caps Have Tended to Outpace Large Caps in Periods of High Economic Growth

Russell 2000 vs Russell 1000 Regimes from 6/30/01 to 6/30/21

Batting average refers to the percentage of 1-year periods in which the Russell 2000 outperformed the Russell 1000.

The state of valuations between small and large caps is also relevant. With more and more market observers expressing concern about share prices in the U.S. market being unsustainably elevated, we looked at the situation by dividing the market by capitalization. To gauge valuations, we used one of our preferred metrics, enterprise value divided by the last 12 months’ earnings before interest & taxes (“LTM EV/EBIT”), excluding companies with negative EBIT. Although small cap delivered a significant outperformance over large cap over the past year (+62.0% vs. +43.1%), small-cap stocks are still

relatively undervalued versus large caps when compared against their valuation range over the past 20 years.

Relative Valuations for Small Caps Are Near Their Lowest in 20 Years

Russell 2000 vs. Russell 1000 Median LTM EV/EBIT1 (ex. Negative EBIT Companies) from 6/30/01 to 6/30/21

1 Earnings before interest and taxes. Source: FactSet

We think that the combination of the asset class’s strong history in growing economies and its more attractive relative valuations make a powerful case for small cap’s ongoing leadership in the U.S. equity market.

SMALL-CAP VALUE’S ADVANTAGE

In addition to looking for small caps to continue posting attractive relative and solid absolute results, we also expect small-cap value to maintain leadership within small cap—and for the same two reasons as small cap’s relative advantage over large caps: 1) Small-cap value has enjoyed a pronounced tendency to outperform small-cap growth when nominal economic growth has been above average and 2) small-cap value’s relative valuation compared with its historic range also looks attractive. The rationale for small-cap value outperforming in periods of high nominal economic growth is rooted in the idea that small-cap value is both more cyclically sensitive than its growth sibling and a greater beneficiary of inflation for relative earnings growth and valuation.

Our research confirmed this relationship as we looked back over the past 20 years and found that in one-year periods with at least 5% nominal GDP growth, the Russell 2000 Pure Value Index outperformed the Russell 2000 Pure Growth Index 68% of the time by an average of 420 basis points. In contrast, when nominal GDP growth fell between 3-5%, the small-cap value

| 4 | This page is not part of the 2021 Semiannual Report to Stockholders | Past performance is no guarantee of future results. |

LETTER TO OUR STOCKHOLDERS

index outperformed only 32% of the time and lagged small-cap growth by an average of 100 basis points. As noted earlier, with consensus projections for nominal GDP growth for 2021 and 2022 both in excess of 5%, the future environment seems well suited to continued outperformance for value.

Strong Economic Expansion Has Favored Value

Rolling 1-Year Returns for the Russell 2000 Pure Value vs Russell 2000 Pure Growth Indexes from 6/30/01 to 6/30/21

Batting average refers to the percentage of 1-year periods in which the Russell Pure Value outperformed the Russell Pure Growth Index. Source: Russell Investments

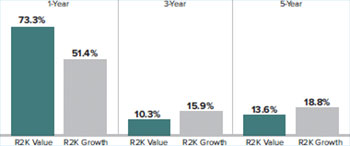

Despite these favorable conditions, some readers, in noting that small cap value has already beaten small-cap growth by a sizable margin over the last year (+73.3% versus +51.4%), may be wondering how much more outperformance value has left. We’d suggest that extending the time periods from the last one year to include the last three and five years reveals a starkly different picture. The Russell 2000 Value lagged its growth counterpart by more than 500 basis points for both the three-and five-year annualized periods ended 6/30/21. Given the depth of value’s underperformance over much of the past five years, then, the idea that value’s run might also be over seems ill founded to us.

Despite Leading from One Year, Value Trails by a Large Margin for Three- and Five-Year Periods

Russell 2000 Value vs Russell 2000 Growth Average Annual Total Returns as of 6/30/21

Current valuations add one final piece of the puzzle: just as small cap valuations finished June looking more attractive than those of large cap, small-cap value wound down 2021’s first half looking far more attractively valued than its growth counterpart—based on the same LTM EV/EBIT metric we used above. Indeed, even after accounting for its recent performance dominance, small-cap value stocks are as inexpensive compared to their small-cap growth cousins than at any time in the last 20 years. At the end of June 2021, the Russell 2000 Value Index had a relative valuation of 22% of the Russell 2000 Growth Index compared to a 20-year average of 85% This most recent relative valuation shows how much cheaper small-cap value stocks are compared with their historic relationship with valuations for small-cap growth stocks.

THE SECOND MAXIM

With all of the ups and downs the market has experienced since June 30, 2016, many investors may not realize that small caps have more than doubled over that five-year span. A multi-year period of moderately lower returns is to be expected after that high level of performance.

Which brings us to the aforementioned silver lining. The second investment maxim that is especially relevant to the current environment is that, perhaps paradoxically, active small-cap managers have actually added their greatest share of excess return when the Russell 2000 has delivered lower returns—single-digit results over five-year periods to be precise.

Monthly Rolling 5-Year U.S. Small Blend1 Average Excess Returns During Russell 2000 Return Ranges from 12/31/78 through 6/30/21

Russell 2000 Five-Year Return Range (12/31/78 through 6/30/21)

| 1 | | There were 514 US Fund Small Blend Funds tracked by Morningstar with at least five years of performance history as of 6/30/21. The excess return for a Morningstar category would be the category’s return for the period minus the Index return. Source: Morningstar |

| Past performance is no guarantee of future results. | This page is not part of the 2021 Semiannual Report to Stockholders | 5 |

LETTER TO OUR STOCKHOLDERS

THE AGE OF ALPHA?

For most of the last decade, simply buying the market worked very well. The conditions were close to ideal for a market cap weighted, index-based approach. Large cap beat small cap, and mega caps beat large caps. The economy grew very slowly and with a good deal of volatility, while 10-year Treasury yields ended the period at less than half of the 3.2% at which they started it. This significant decline in yield fused with the scarcity of economic growth to drive outperformance for duration-sensitive mega-cap growth stocks. The behemoths in turn drove index returns. We would describe this roughly 10-year period as “the era of beta” because overall market returns were so much higher than economic and profit growth, making it difficult for active strategies to stand out. Yet we believe that what we’re calling the “age of alpha” is in front of us—alpha being the term that describes an investment approach’s ability to beat the market.

As we have outlined, there’s good reason to anticipate a period of above-average economic and profit growth that’s accompanied by more subdued market returns. We believe this kind of environment gives disciplined active managers, especially those with a quality bias, an excellent opportunity

to excel. A market in which there will be considerable differentiation is apt to reward the very fundamentals we focus on most. So while we anticipate lower overall U.S. equity returns than what the markets have given investors over the last 12-15 months, we also anticipate positive results—for small caps as an asset class and, more specifically, for small-cap value and select cyclicals.

There are always challenges, of course—and surprises, such as the Dow’s 500-point swoon on July 20th. It’s also true that small cap will almost definitely be contending with two countervailing forces over at least the next year or more: their fall through most of June and July notwithstanding, slowly rising rates seem likely to push down on valuations just as many companies are likely to be reporting healthy and growing earnings through at least the end of next year. These forces, however, will not affect all small-cap stocks equally. We believe that we offer our investors the requisite experience, discipline, and expertise to select those companies best positioned to benefit from the more challenging environment we see ahead—one that looks like a promising period for active small-cap management.

| Sincerely, | | |

|  |  |

| | | |

Charles M. Royce Chairman, Royce Investment Partners | Christopher D. Clark Chief Executive Officer, and Co-Chief Investment Officer, Royce Investment Partners | Francis D. Gannon Co-Chief Investment Officer, Royce Investment Partners |

| July 30, 2021 | | |

| 6 | This page is not part of the 2021 Semiannual Report to Stockholders | Past performance is no guarantee of future results. |

Performance

| NAV Average Annual Total Returns | | | | | | | | |

| As of June 30, 2021 (%) | | | | | | | | |

| | | | | | | | | | | SINCE | INCEPTION |

| | YTD¹ | 1-YR | 3-YR | 5-YR | 10-YR | 15-YR | 20-YR | 25-YR | 30-YR | INCEPTION | DATE |

| Royce Global Value Trust | 9.50 | 40.77 | 13.32 | 15.13 | N/A | N/A | N/A | N/A | N/A | 9.09 | 10/17/13 |

| Royce Micro-Cap Trust | 21.12 | 72.54 | 17.54 | 18.99 | 13.31 | 9.82 | 10.86 | 11.52 | N/A | 11.87 | 12/14/93 |

| Royce Value Trust | 16.77 | 56.22 | 15.61 | 17.32 | 11.39 | 8.99 | 9.57 | 10.92 | 11.60 | 11.16 | 11/26/86 |

| INDEX | | | | | | | | | | | |

| MSCI ACWI Small Cap Index | 15.43 | 54.07 | 12.20 | 14.13 | 9.90 | 8.64 | 9.96 | 8.43 | N/A | N/A | N/A |

| Russell Microcap Index | 29.02 | 75.77 | 14.47 | 18.13 | 13.06 | 8.73 | 9.26 | N/A | N/A | N/A | N/A |

| Russell 2000 Index | 17.54 | 62.03 | 13.52 | 16.47 | 12.34 | 9.51 | 9.26 | 9.33 | 10.65 | N/A | N/A |

| 1 Not annualized. | | | | | | | | | | | |

Important Performance and Risk Information

All performance information in this Review and Report reflects past performance, is presented on a total return basis, net of the Fund’s investment advisory fee, and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when sold. Current performance may be higher or lower than performance quoted. Current month-end performance may be obtained at www.royceinvest.com. The Funds are closed-end registered investment companies whose respective shares of common stock may trade at a discount to the net asset value. Shares of each Fund’s common stock are also subject to the market risk of investing in the underlying portfolio securities held by each Fund. Each Fund is subject to market risk-the possibility that common stock prices will decline, sometimes sharply and unpredictably, over short or extended periods of time. Such declines may be caused by various factors, including market, financial, and economic conditions, governmental or central bank actions, and other factors, such as the recent COVID-19 pandemic, that may not be directly related to the issuer of a security held by a Fund. This pandemic could adversely affect global market, financial, and economic conditions in ways that cannot necessarily be foreseen. All indexes referenced are unmanaged and capitalization-weighted. Each index’s returns include net reinvested dividends and/or interest income. Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 Index is an index of domestic small-cap stocks that measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 Index. The Russell Microcap Index includes 1,000 of the smallest securities in the small-cap Russell 2000 Index, along with the next smallest eligible securities as determined by Russell. The MSCI ACWI Small Cap Index is an unmanaged, capitalization-weighted index of global small-cap stocks. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Index returns include net reinvested dividends and/or interest income. Royce Value, Micro-Cap, and Global Value Trust shares of common stock trade on the NYSE. Royce Fund Services, LLC (“RFS”) is a member of FINRA and files certain material with FINRA on behalf of each Fund. RFS is not an underwriter or distributor of any of the Funds.

This page is not part of the 2021 Semiannual Report to Stockholders | 7

MANAGER’S DISCUSSION (UNAUDITED)

Royce Global Value Trust (RGT)

Chuck Royce

FUND PERFORMANCE

Royce Global Value Trust advanced 9.5% on an NAV (net asset value) basis and 12.1% on a market price basis for the year-to-date period ended 6/30/21, posting strong absolute results that nonetheless trailed the 15.4% gain for its benchmark, the MSCI ACWI Small Cap Index, for the same period. The Fund’s relative results were stronger over longer-term periods as it beat its global small-cap benchmark on both an NAV and market price basis for the three- and five-year periods ended 6/30/21.

WHAT WORKED… AND WHAT DIDN’T

Five of the 10 equity sectors in which the Fund held investments made a positive contribution to performance in 2021’s first half. Industrials led by a wide margin, followed by Financials and Information Technology. Of the four sectors that detracted—Health Care was essentially flat—Materials, Communication Services, and Consumer Staples made the largest negative impact. At the industry level, two areas from Industrials made significant positive contributions—professional services and trading companies & distributors—while insurance (Financials) was also notably strong. The three industries that detracted most were internet & direct marketing retail (Consumer Discretionary), metals & mining (Materials), and interactive media & services (Communication Services).

The Fund’s top contributor at the position level was Marlowe, a firm based in and focused on the United Kingdom. Marlowe provides a range of commercial services and software products grouped into four areas: Health and Safety, Fire Safety, Water Safety, and Air Quality. We like the company’s position in essential, critical, and/or mandated services in growing markets, each with a highly fragmented customer base. Marlowe is also an acquisition-led consolidator of its large and fragmented markets, which enables it to re-deploy its cash flows into M&A and breeds cross-selling opportunities and scale advantages. The second quarter saw a steady flow of positive news, including M&A announcements and the release of final results at the end of June that showed improved revenue and earnings. Next came AutoCanada, a North American automobile business that sells multiple brands and operates 50 franchised dealerships in Canada, as well as a group in Illinois. In early May, the company reported record-setting revenue and earnings along with a ninth consecutive quarter of outracing the Canadian new vehicle retail market, though AutoCanada’s used vehicle and F&I (Finance & Insurance) segments were the key drivers behind 1Q21’s improved earnings.

RGT’s top detracting position was CDON, a Swedish e-commerce company that operates a website which sells music, books, t-shirts, and other merchandise—it is phasing out a legacy brick-and-mortar retail business. As an established e-commerce name in Nordic countries, CDON is expected to grow rapidly in the region, where online shopping habits trail those in much of the developed world but are expected to catch up in the coming years. The company hit a speed bump earlier in the year when a new technical platform proved both more expensive and harder to bring to optimal functionality than anticipated. Thinking that the company can overcome these obstacles, we held our shares at the end of June. The next biggest detractor was Haemonetics Corporation, which designs and manufactures automated systems for the collection, processing, and surgical salvage of donor and patient blood while also offering related information services and data management software. Its shares suffered a significant decline in April with the departure of a large customer in plasma distribution. Confident in the company’s expertise in its niche, we maintained our stake at the end of June.

Relative to the MSCI ACWI Small Cap in the first half of 2021, both stock selection and sector allocation hurt, with the former making a much larger negative impact. On a sector basis, ineffective stock picks in Materials and an equal combination of our lower weighting and poor stock picking in the resurgent Energy sector detracted most, along with the negative effect of the Fund’s cash holdings. On the other hand, our higher weighting in Industrials was additive versus the benchmark. Also helping relative performance were our lower weighting and savvy stock picks in Real Estate and our lack of exposure to Utilities, two sectors that lagged within the benchmark.

| | | | | | | |

| | Top Contributors to Performance | | | Top Detractors from Performance | | |

| | Year-to-Date Through 6/30/21 (%)1 | | | Year-to-Date Through 6/30/21 (%)2 | | |

| | | | | | | |

| | Marlowe | 0.63 | | CDON | -0.45 | |

| | AutoCanada | 0.52 | | Haemonetics Corporation | -0.43 | |

| | Transcat | 0.51 | | Cartrack Holdings | -0.26 | |

| | ProAssurance Corporation | 0.51 | | a2 Milk | -0.25 | |

| | SThree | 0.48 | | TKC Corporation | -0.22 | |

| | 1 Includes dividends | | | 2Net of dividends | | |

| | | | | | | |

CURRENT POSITIONING AND OUTLOOK

Our outlook has not changed in any significant way since the end of 2020. In spite of considerable near-term uncertainty, we believe that the global economic recovery will continue, albeit with more fits and starts—as well as market volatility—than many were anticipating as recently as May. In July, however, worrisome signs of a slowdown came from China, and the globe faces a major challenge in containing the Delta COVID variant. We are cautiously optimistic, however, that the global economy will continue to expand, benefiting more economically sensitive sectors of the world’s economies, particularly as supply chains are reestablished and pent-up demand—which remains robust through most of the developed world—is released. As always, we are prepared to act when market volatility gives us the opportunity to build existing holdings at more attractive prices.

| 8 | | 2021 Semiannual Report to Stockholders |

| PERFORMANCE AND PORTFOLIO REVIEW (UNAUDITED) | SYMBOLS MARKET PRICE RGT NAV XRGTX |

Performance

Average Annual Total Return (%) Through 6/30/21

| | JAN-JUN 20211 | 1-YR | 3-YR | 5-YR | SINCE INCEPTION (10/17/13) |

| RGT (NAV) | 9.50 | 40.77 | 13.32 | 15.13 | 9.09 |

1 Not Annualized

Market Price Performance History Since Inception (10/17/13)

Cumulative Performance of Investment 1

| | 1-YR | 5-YR | 10-YR | 15-YR | 20-YR | SINCE INCEPTION (10/17/13) |

| RGT | 41.0% | 122.8% | N/A | N/A | N/A | 94.9% |

| ¹ | Reflects the cumulative performance experience of a continuous common stockholder who purchased one share at inception ($8.975 IPO) and reinvested all distributions. |

| ² | Reflects the actual month-end market price movement of one share as it has traded on NYSE. |

Morningstar Style Map™ As of 6/30/21

The Morningstar Style Map is the Morningstar Style Box™ with the center 75% of fund holdings plotted as the Morningstar Ownership Zone™. The Morningstar Style Box is designed to reveal a fund’s investment strategy. The Morningstar Ownership Zone provides detail about a portfolio’s investment style by showing the range of stock sizes and styles. The Ownership Zone is derived by plotting each stock in the portfolio within the proprietary Morningstar Style Box. Over time, the shape and location of a fund’s ownership zone may vary. See page 60 for additional information.

| Top 10 Positions | | | |

| % of Net Assets | | | |

| | | | |

| ProAssurance Corporation | | | 2.1 | |

| Descartes Systems Group (The) | | | 2.1 | |

| James River Group Holdings | | | 1.9 | |

| SEI Investments | | | 1.8 | |

| Marlowe | | | 1.8 | |

| IPH | | | 1.6 | |

| Morningstar | | | 1.6 | |

| Transcat | | | 1.5 | |

| CMC Materials | | | 1.5 | |

| Sprott | | | 1.5 | |

| Portfolio Sector Breakdown | | | |

| % of Net Assets | | | |

| | | | |

| Industrials | | | 29.0 | |

| Information Technology | | | 20.3 | |

| Financials | | | 18.0 | |

| Health Care | | | 7.5 | |

| Materials | | | 5.5 | |

| Consumer Discretionary | | | 3.4 | |

| Communication Services | | | 3.2 | |

| Real Estate | | | 1.5 | |

| Consumer Staples | | | 1.5 | |

| Energy | | | 0.6 | |

| Cash and Cash Equivalents, Net of Outstanding Line of Credit | | | 9.5 | |

| Calendar Year Total Returns (%) | | | |

| | | | |

| YEAR | | RGT | |

| 2020 | | | 19.7 | |

| 2019 | | | 31.2 | |

| 2018 | | | -16.1 | |

| 2017 | | | 31.1 | |

| 2016 | | | 11.1 | |

| 2015 | | | -3.4 | |

| 2014 | | | -6.2 | |

| Portfolio Country Breakdown1,2 | | | |

| % of Net Assets | | | |

| | | | |

| United States | | | 30.7 | |

| United Kingdom | | | 12.9 | |

| Canada | | | 10.8 | |

| Sweden | | | 4.8 | |

| South Africa | | | 3.0 | |

¹ Represents countries that are 3% or more of net assets.

² Securities are categorized by the country of their headquarters.

| Portfolio Diagnostics | | |

| | | |

| Fund Net Assets | | $92 million |

| Number of Holdings | | | 119 |

| Turnover Rate | | | 33% |

| Net Asset Value | | | $16.37 |

| Market Price | | | $14.98 |

| Average Market Capitalization1 | | | $2,112 million |

| Weighted Average P/E Ratio2,3 | | | 29.1x |

| Weighted Average P/B Ratio2 | | | 3.2x |

| Active Share4 | | | 98% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Royce believes offers a more accurate measure of average market cap than a simple mean or median. |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | The Fund’s P/E ratio calculation excludes companies with zero or negative earnings (20% of portfolio holdings as of 6/30/21). |

| 4 | Active Share is the sum of the absolute values of the different weightings of each holding in the Fund versus each holding in the benchmark, divided by two. |

Important Performance and Risk Information

All performance information reflects past performance, is presented on a total return basis, net of the Fund’s investment advisory fee, and reflects the reinvestment of distributions. Past performance is no guarantee of future results. Current performance may be higher or lower than performance quoted. Returns as of the most recent month-end may be obtained at www.royceinvest.com. The market price of the Fund’s shares will fluctuate, so that shares may be worth more or less than their original cost when sold. The Fund invests primarily in securities of small- and mid-cap companies, which may involve considerably more risk than investments in securities of larger-cap companies. The Fund’s broadly diversified portfolio does not ensure a profit or guarantee against loss. From time to time, the Fund may invest a significant portion of its net assets in foreign securities, which may involve political, economic, currency and other risks not encountered in U.S. investments. Regarding the “Top Contributors” and “Top Detractors” tables shown above, the sum of all contributors to, and all detractors from, performance for all securities in the portfolio would approximate the Fund’s year-to-date performance for 2021.

2021 Semiannual Report to Stockholders | 9

Royce Global Value Trust

Schedule of Investments

Common Stocks – 90.5%

| | | SHARES | | | VALUE | |

| | | | | | | |

| AUSTRALIA – 2.9% | | | | | | | | |

| Cochlear | | | 4,000 | | | $ | 754,960 | |

| IPH | | | 249,720 | | | | 1,460,765 | |

| Steadfast Group | | | 53,300 | | | | 175,878 | |

| Technology One | | | 40,400 | | | | 282,074 | |

| Total (Cost $1,443,715) | | | | | | | 2,673,677 | |

| | | | | | | | | |

| BERMUDA – 2.4% | | | | | | | | |

| Assured Guaranty 1 | | | 10,800 | | | | 512,784 | |

| †James River Group Holdings | | | 45,900 | | | | 1,722,168 | |

| Total (Cost $1,954,639) | | | | | | | 2,234,952 | |

| | | | | | | | | |

| BRAZIL – 1.7% | | | | | | | | |

| OdontoPrev | | | 312,000 | | | | 817,355 | |

| TOTVS | | | 97,885 | | | | 740,957 | |

| Total (Cost $1,178,333) | | | | | | | 1,558,312 | |

| | | | | | | | | |

| CANADA – 10.8% | | | | | | | | |

| Alamos Gold Cl. A | | | 132,200 | | | | 1,009,950 | |

| Altus Group | | | 10,700 | | | | 495,898 | |

| AutoCanada 2 | | | 20,400 | | | | 821,859 | |

| Centerra Gold | | | 39,000 | | | | 296,055 | |

| Descartes Systems Group (The) 1,2 | | | 27,400 | | | | 1,894,984 | |

| FirstService | | | 1,400 | | | | 239,764 | |

| LifeWorks | | | 36,500 | | | | 984,051 | |

| Major Drilling Group International 2 | | | 168,000 | | | | 1,161,472 | |

| †Onex Corporation | | | 6,000 | | | | 435,673 | |

| Pan American Silver 1 | | | 22,300 | | | | 637,111 | |

| Sprott | | | 34,360 | | | | 1,352,391 | |

| Stella-Jones | | | 16,000 | | | | 576,057 | |

| Total (Cost $6,144,315) | | | | | | | 9,905,265 | |

| | | | | | | | | |

| DENMARK – 0.2% | | | | | | | | |

| Chr. Hansen Holding | | | 1,800 | | | | 162,456 | |

| Total (Cost $155,783) | | | | | | | 162,456 | |

| | | | | | | | | |

| FRANCE – 0.8% | | | | | | | | |

| Esker | | | 1,800 | | | | 525,050 | |

| Interparfums | | | 3,102 | | | | 201,565 | |

| Total (Cost $210,145) | | | | | | | 726,615 | |

| | | | | | | | | |

| GERMANY – 2.7% | | | | | | | | |

| Carl Zeiss Meditec | | | 3,400 | | | | 656,941 | |

| CompuGroup Medical | | | 3,300 | | | | 258,452 | |

| New Work | | | 3,600 | | | | 1,131,206 | |

| STRATEC | | | 3,300 | | | | 460,948 | |

| Total (Cost $1,639,224) | | | | | | | 2,507,547 | |

| | | | | | | | | |

| GREECE – 0.7% | | | | | | | | |

| Sarantis | | | 64,500 | | | | 680,680 | |

| Total (Cost $554,222) | | | | | | | 680,680 | |

| | | | | | | | | |

| ICELAND – 0.8% | | | | | | | | |

| Ossur 2 | | | 101,500 | | | | 748,555 | |

| Total (Cost $657,869) | | | | | | | 748,555 | |

| | | | | | | | | |

| INDIA – 2.0% | | | | | | | | |

| AIA Engineering 2 | | | 35,100 | | | | 1,014,443 | |

| WNS Holdings ADR 1,2,3 | | | 10,500 | | | | 838,635 | |

| Total (Cost $1,463,783) | | | | | | | 1,853,078 | |

| | | | | | | | | |

| ISRAEL – 1.8% | | | | | | | | |

| Nova Measuring Instruments 1,2 | | | 5,700 | | | | 586,473 | |

| Tel Aviv Stock Exchange | | | 164,600 | | | | 1,016,838 | |

| Total (Cost $591,484) | | | | | | | 1,603,311 | |

| | | | | | | | | |

| ITALY – 1.1% | | | | | | | | |

| Carel Industries | | | 35,800 | | | | 859,609 | |

| Gruppo MutuiOnline | | | 2,900 | | | | 138,235 | |

| Total (Cost $489,921) | | | | | | | 997,844 | |

| | | | | | | | | |

| JAPAN – 2.6% | | | | | | | | |

| As One | | | 2,800 | | | | 365,705 | |

| Benefit One | | | 13,700 | | | | 430,996 | |

| Fukui Computer Holdings | | | 10,800 | | | | 408,299 | |

| NSD | | | 12,200 | | | | 203,818 | |

| TechnoPro Holdings | | | 7,200 | | | | 170,319 | |

| TKC Corporation | | | 25,500 | | | | 772,380 | |

| Total (Cost $1,288,537) | | | | | | | 2,351,517 | |

| | | | | | | | | |

| MEXICO – 0.5% | | | | | | | | |

| Becle | | | 63,000 | | | | 166,491 | |

| Bolsa Mexicana de Valores | | | 120,600 | | | | 266,199 | |

| Total (Cost $400,551) | | | | | | | 432,690 | |

| | | | | | | | | |

| NETHERLANDS – 1.0% | | | | | | | | |

| IMCD | | | 5,500 | | | | 874,550 | |

| Total (Cost $387,492) | | | | | | | 874,550 | |

| | | | | | | | | |

| NEW ZEALAND – 2.0% | | | | | | | | |

| †a2 Milk 2 | | | 60,000 | | | | 269,982 | |

| Fisher & Paykel Healthcare | | | 17,000 | | | | 369,799 | |

| †NZX | | | 330,300 | | | | 461,759 | |

| †Pushpay Holdings 2 | | | 583,000 | | | | 733,531 | |

| Total (Cost $1,776,018) | | | | | | | 1,835,071 | |

| | | | | | | | | |

| NORWAY – 1.7% | | | | | | | | |

| Protector Forsikring | | | 70,000 | | | | 672,346 | |

| TGS | | | 45,600 | | | | 581,244 | |

| †Tomra Systems | | | 6,000 | | | | 331,005 | |

| Total (Cost $1,247,085) | | | | | | | 1,584,595 | |

| | | | | | | | | |

| POLAND – 0.4% | | | | | | | | |

| Warsaw Stock Exchange | | | 29,100 | | | | 363,578 | |

| Total (Cost $351,627) | | | | | | | 363,578 | |

| | | | | | | | | |

| SINGAPORE – 1.8% | | | | | | | | |

| †Karooooo 2 | | | 11,409 | | | | 423,531 | |

| Midas Holdings 2,4 | | | 400,000 | | | | 0 | |

| XP Power | | | 16,300 | | | | 1,258,167 | |

| Total (Cost $1,061,256) | | | | | | | 1,681,698 | |

| | | | | | | | | |

| SOUTH AFRICA – 3.0% | | | | | | | | |

| JSE | | | 53,000 | | | | 394,531 | |

| PSG Group | | | 114,900 | | | | 640,399 | |

| †Stadio Holdings 2 | | | 3,541,372 | | | | 766,305 | |

| Transaction Capital | | | 344,100 | | | | 911,335 | |

| Total (Cost $2,003,626) | | | | | | | 2,712,570 | |

| | | | | | | | | |

| SWEDEN – 4.8% | | | | | | | | |

| Biotage | | | 42,100 | | | | 996,654 | |

| Bravida Holding | | | 68,900 | | | | 996,696 | |

| †CDON 2 | | | 7,300 | | | | 300,424 | |

| Dometic Group | | | 15,500 | | | | 263,975 | |

| Karnov Group | | | 161,481 | | | | 992,498 | |

| 10 | 2021 Semiannual Report to Stockholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

June 30, 2021 (unaudited)

Schedule of Investments (continued)

| | | SHARES | | | VALUE | |

| | | | | | | |

| SWEDEN (continued) | | | | | | | | |

| OEM International Cl. B | | | 59,425 | | | $ | 890,184 | |

| Total (Cost $3,335,230) | | | | | | | 4,440,431 | |

| | | | | | | | | |

| SWITZERLAND – 1.2% | | | | | | | | |

| Kardex Holding | | | 2,400 | | | | 555,093 | |

| LEM Holding | | | 150 | | | | 314,510 | |

| VZ Holding | | | 2,900 | | | | 245,728 | |

| Total (Cost $482,877) | | | | | | | 1,115,331 | |

| | | | | | | | | |

| UNITED KINGDOM – 12.9% | | | | | | | | |

| Ashmore Group | | | 101,000 | | | | 537,896 | |

| CentralNic Group 2 | | | 136,073 | | | | 158,113 | |

| †Countryside Properties 2 | | | 100,000 | | | | 653,747 | |

| Diploma | | | 8,200 | | | | 329,402 | |

| DiscoverIE Group | | | 60,800 | | | | 796,471 | |

| Eckoh | | | 103,927 | | | | 92,727 | |

| FDM Group Holdings | | | 46,800 | | | | 660,332 | |

| Ferroglobe (Warranty Insurance Trust) 2,4 | | | 41,100 | | | | 0 | |

| Genuit Group | | | 68,300 | | | | 578,214 | |

| Halma | | | 18,700 | | | | 696,359 | |

| Intertek Group | | | 9,300 | | | | 711,417 | |

| Keystone Law Group | | | 95,940 | | | | 902,454 | |

| Learning Technologies Group | | | 342,800 | | | | 891,961 | |

| Marlowe 2 | | | 132,500 | | | | 1,612,928 | |

| Mortgage Advice Bureau Holdings | | | 36,100 | | | | 589,258 | |

| Restore 2 | | | 180,700 | | | | 974,853 | |

| RWS Holdings | | | 45,100 | | | | 351,550 | |

| SThree | | | 146,600 | | | | 935,884 | |

| YouGov | | | 18,600 | | | | 303,607 | |

| Total (Cost $7,620,728) | | | | | | | 11,777,173 | |

| | | | | | | | | |

| UNITED STATES – 30.7% | | | | | | | | |

| Air Lease Cl. A 1 | | | 20,123 | | | | 839,934 | |

| APi Group 1,2 | | | 50,700 | | | | 1,059,123 | |

| BOK Financial 1 | | | 6,350 | | | | 549,910 | |

| CIRCOR International 1,2 | | | 28,300 | | | | 922,580 | |

| CMC Materials 1 | | | 9,150 | | | | 1,379,271 | |

| Cognex Corporation 1 | | | 4,837 | | | | 406,550 | |

| Colfax 1,2 | | | 21,400 | | | | 980,334 | |

| Diodes 1,2 | | | 7,000 | | | | 558,390 | |

| ESCO Technologies 1 | | | 5,500 | | | | 515,955 | |

| FARO Technologies 1,2 | | | 7,250 | | | | 563,832 | |

| †FormFactor 2 | | | 10,000 | | | | 364,600 | |

| GCM Grosvenor Cl. A | | | 109,626 | | | | 1,142,303 | |

| †Haemonetics Corporation 2 | | | 6,600 | | | | 439,824 | |

| Helios Technologies 1 | | | 7,506 | | | | 585,843 | |

| Innospec 1 | | | 6,228 | | | | 564,319 | |

| Kadant 1 | | | 3,700 | | | | 651,533 | |

| KBR 1 | | | 34,800 | | | | 1,327,620 | |

| Kennedy-Wilson Holdings | | | 30,000 | | | | 596,100 | |

| Lindblad Expeditions Holdings 2 | | | 21,500 | | | | 344,215 | |

| Lindsay Corporation 1 | | | 3,910 | | | | 646,245 | |

| Mesa Laboratories 1 | | | 3,660 | | | | 992,482 | |

| Momentive Global 2 | | | 60,000 | | | | 1,264,200 | |

| Morningstar 1 | | | 5,640 | | | | 1,450,100 | |

| National Instruments 1 | | | 19,420 | | | | 821,078 | |

| †New York Times Cl. A | | | 12,100 | | | | 526,955 | |

| PAR Technology 1,2 | | | 12,341 | | | | 863,130 | |

| ProAssurance Corporation 1 | | | 83,900 | | | | 1,908,725 | |

| Quaker Chemical 1 | | | 2,710 | | | | 642,785 | |

| SEI Investments 1 | | | 26,750 | | | | 1,657,698 | |

| Transcat 2 | | | 24,577 | | | | 1,388,846 | |

| Upland Software 1,2 | | | 19,900 | | | | 819,283 | |

| †Vontier Corporation | | | 41,300 | | | | 1,345,554 | |

| Total (Cost $19,753,954) | | | | | | | 28,119,317 | |

| | | | | | | | | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Cost $56,192,414) | | | | | | | 82,940,813 | |

| | | | | | | | | |

| REPURCHASE AGREEMENT– 13.8% | | | | | | | | |

Fixed Income Clearing Corporation, 0.00% dated 6/30/21, due 7/1/21, maturity value $12,652,210 (collateralized by obligations of various U.S. Government Agencies, 1.25% due 6/30/28, valued at $12,905,261) | | | | | | | | |

| (Cost $12,652,210) | | | | | | | 12,652,210 | |

| | | | | | | | | |

| TOTAL INVESTMENTS – 104.3% | | | | | | | | |

| (Cost $68,844,624) | | | | | | | 95,593,023 | |

| | | | | | | | | |

| LIABILITIES LESS CASH AND OTHER ASSETS – (4.3)% | | | | | | | (3,917,001 | ) |

| | | | | | | | | |

| NET ASSETS – 100.0% | | | | | | $ | 91,676,022 | |

ADR – American Depository Receipt

| 1 | All or a portion of these securities were pledged as collateral in connection with the Fund’s revolving credit agreement at June 30, 2021. Total market value of pledged securities at June 30, 2021, was $10,566,649. |

| 3 | At June 30, 2021, a portion of these securities were rehypothecated in connection with the Fund’s revolving credit agreement in the aggregate amount of $830,648. |

| 4 | Securities for which market quotations are not readily available represent 0.0% of net assets. These securities have been valued at their fair value under procedures approved by the Fund’s Board of Directors. These securities are defined as Level 3 securities due to the use of significant unobservable inputs in the determination of fair value. See Notes to Financial Statements. |

Securities of Global/International Funds are categorized by the country of their headquarters.

Bold indicates the Fund’s 20 largest equity holdings in terms of June 30, 2021, market value.

TAX INFORMATION: The cost of total investments for Federal income tax purposes was $68,875,155. At June 30, 2021, net unrealized appreciation for all securities was $26,717,868 consisting of aggregate gross unrealized appreciation of $28,591,699 and aggregate gross unrealized depreciation of $1,873,831. The primary cause of the difference between book and tax basis cost is the timing of the recognition of losses on securities sold.

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | 2021 Semiannual Report to Stockholders | 11 |

| Royce Global Value Trust | June 30, 2021 (unaudited) |

Statement of Assets and Liabilities

| ASSETS: | | |

| Investments at value | $ | 82,940,813 |

| Repurchase agreements (at cost and value) | | 12,652,210 |

| Receivable for dividends | | 203,271 |

| Prepaid expenses and other assets | | 17,613 |

| Total Assets | | 95,813,907 |

| LIABILITIES: | | |

| Revolving credit agreement | | 4,000,000 |

| Payable for investment advisory fee | | 75,579 |

| Payable for directors’ fees | | 5,838 |

| Payable for interest expense | | 3,609 |

| Accrued expenses | | 52,859 |

| Total Liabilities | | 4,137,885 |

| Net Assets | $ | 91,676,022 |

| ANALYSIS OF NET ASSETS: | | |

| Paid-in capital - $0.001 par value per share; 5,600,791 shares outstanding (150,000,000 shares authorized) | $ | 47,249,348 |

| Total distributable earnings (loss) | | 44,426,674 |

| Net Assets (net asset value per share - $16.37) | $ | 91,676,022 |

| Investments at identified cost | $ | 56,192,414 |

| 12 | 2021 Semiannual Report to Stockholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| Royce Global Value Trust | Six Months Ended June 30, 2021 (unaudited) |

Statement of Operations

| INVESTMENT INCOME: | | |

| INCOME: | | |

| Dividends | $ | 757,592 |

| Foreign withholding tax | | (63,412) |

| Total income | | 694,180 |

| EXPENSES: | | |

| Investment advisory fees | | 437,913 |

| Custody and transfer agent fees | | 32,556 |

| Administrative and office facilities | | 28,706 |

| Stockholder reports | | 28,111 |

| Interest expense | | 23,369 |

| Professional fees | | 21,699 |

| Directors’ fees | | 13,518 |

| Other expenses | | 15,879 |

| Total expenses | | 601,751 |

| Compensating balance credits | | (2) |

| Net expenses | | 601,749 |

| Net investment income (loss) | | 92,431 |

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY: | | |

| NET REALIZED GAIN (LOSS): | | |

| Investments | | 10,343,291 |

| Foreign currency transactions | | 36,704 |

| NET CHANGE IN UNREALIZED APPRECIATION (DEPRECIATION): | | |

| Investments | | (2,559,531) |

| Other assets and liabilities denominated in foreign currency | | 11,128 |

| Net realized and unrealized gain (loss) on investments and foreign currency | | 7,831,592 |

| NET INCREASE (DECREASE) IN NET ASSETS FROM INVESTMENT OPERATIONS | $ | 7,924,023 |

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | 2021 Semiannual Report to Stockholders | 13 |

Royce Global Value Trust

Statement of Changes in Net Assets

| | | SIX MONTHS ENDED | | |

| | | 6/30/21 | | |

| | | (UNAUDITED) | | YEAR ENDED 12/31/20 |

| | | | | |

| INVESTMENT OPERATIONS: | | | | |

| Net investment income (loss) | $ | 92,431 | $ | (209,532) |

| Net realized gain (loss) on investments and foreign currency | | 10,379,995 | | 25,222,265 |

| Net change in unrealized appreciation (depreciation) on investments and foreign currency | | (2,548,403) | | (473,615) |

| Net increase (decrease) in net assets from investment operations | | 7,924,023 | | 24,539,118 |

| DISTRIBUTIONS: | | | | |

| Total distributable earnings | | – | | (12,499,130) |

| Total distributions | | – | | (12,499,130) |

| CAPITAL STOCK TRANSACTIONS: | | | | |

| Reinvestment of distributions | | – | | 4,684,326 |

| Value of shares tendered | | – | | (75,782,536) |

| Total capital stock transactions | | – | | (71,098,210) |

| Net Increase (Decrease) In Net Assets | | 7,924,023 | | (59,058,222) |

| NET ASSETS: | | | | |

| | | | | |

| Beginning of period | | 83,751,999 | | 142,810,221 |

| End of period | $ | 91,676,022 | $ | 83,751,999 |

| 14 | 2021 Semiannual Report to Stockholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

| Royce Global Value Trust | Six Months Ended June 30, 2021 (unaudited) |

Statement of Cash Flows

| CASH FLOWS FROM OPERATING ACTIVITIES: | | |

| Net increase (decrease) in net assets from investment operations | $ | 7,924,023 |

| Adjustments to reconcile net increase (decrease) in net assets from investment operations to net cash provided by operating activities: | | |

| Purchases of long-term investments | | (28,180,092) |

| Proceeds from sales and maturities of long-term investments | | 33,498,170 |

| Net purchases, sales and maturities of short-term investments | | (1,392,318) |

| Net (increase) decrease in dividends receivable and other assets | | (14,184) |

| Net increase (decrease) in interest expense payable, accrued expenses and other liabilities | | (64,328) |

| Net change in unrealized appreciation (depreciation) on investments | | 2,559,531 |

| Net realized gain (loss) on investments | | (10,343,291) |

| Net cash provided by operating activities | | 3,987,511 |

| CASH FLOWS FROM FINANCING ACTIVITIES: | | |

| Decrease in revolving credit agreement | | (4,000,000) |

| Distributions | | – |

| Reinvestment of distributions | | – |

| Net cash used for financing activities | | (4,000,000) |

| INCREASE (DECREASE) IN CASH: | | (12,489) |

| Cash and foreign currency at beginning of period | | 12,489 |

| Cash and foreign currency at end of period | $ | – |

Supplemental disclosure of cash flow information:

For the six months ended June 30, 2021, the Fund paid $73,410 in interest expense.

| THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS | 2021 Semiannual Report to Stockholders | 15 |

Royce Global Value Trust

Financial Highlights

This table is presented to show selected data for a share outstanding throughout each period, and to assist stockholders in evaluating the Fund’s performance for the periods presented.

| | | SIX MONTHS | | YEARS ENDED |

| | | ENDED 6/30/21 | | | | | | | | | | |

| | | (UNAUDITED) | | 12/31/20 | | 12/31/19 | | 12/31/18 | | 12/31/17 | | 12/31/16 |

| Net Asset Value, Beginning of Period | | $ | 14.95 | | | $ | 13.60 | | | $ | 10.42 | | | $ | 12.48 | | | $ | 9.62 | | | $ | 8.81 | |

| INVESTMENT OPERATIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | | 0.02 | | | | (0.05 | ) | | | 0.06 | | | | 0.04 | | | | 0.02 | | | | 0.06 | |

| Net realized and unrealized gain (loss) on investments and foreign currency | | | 1.40 | | | | 2.63 | | | | 3.18 | | | | (2.06 | ) | | | 2.96 | | | | 0.90 | |

| Net increase (decrease) in net assets from investment operations | | | 1.42 | | | | 2.58 | | | | 3.24 | | | | (2.02 | ) | | | 2.98 | | | | 0.96 | |

| DISTRIBUTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | – | | | | – | | | | (0.06 | ) | | | (0.04 | ) | | | (0.11 | ) | | | (0.14 | ) |

| Net realized gain on investments and foreign currency | | | – | | | | (1.19 | ) | | | – | | | | – | | | | – | | | | – | |

| Total distributions | | | – | | | | (1.19 | ) | | | (0.06 | ) | | | (0.04 | ) | | | (0.11 | ) | | | (0.14 | ) |

| CAPITAL STOCK TRANSACTIONS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Effect of reinvestment of distributions by Common Stockholders | | | – | | | | (0.04 | ) | | | (0.00 | ) | | | (0.00 | ) | | | (0.01 | ) | | | (0.01 | ) |

| Total capital stock transactions | | | – | | | | (0.04 | ) | | | (0.00 | ) | | | (0.00 | ) | | | (0.01 | ) | | | (0.01 | ) |

| Net Asset Value, End of Period | | $ | 16.37 | | | $ | 14.95 | | | $ | 13.60 | | | $ | 10.42 | | | $ | 12.48 | | | $ | 9.62 | |

| Market Value, End of Period | | $ | 14.98 | | | $ | 13.36 | | | $ | 11.69 | | | $ | 8.88 | | | $ | 10.81 | | | $ | 8.04 | |

| TOTAL RETURN:1 | | | | | | | | | | | | | | | | | | | | | | | | |

| Net Asset Value | | | 9.50 | %2 | | | 19.67 | % | | | 31.20 | % | | | (16.11 | )% | | | 31.07 | % | | | 11.12 | % |

| Market Value | | | 12.13 | %2 | | | 24.42 | % | | | 32.33 | % | | | (17.50 | )% | | | 35.96 | % | | | 9.77 | % |

| RATIOS BASED ON AVERAGE NET ASSETS: | | | | | | | | | | | | | | | | | | | | | | | | |

| Investment advisory fee expense | | | 1.00 | %3 | | | 1.00 | % | | | 1.00 | % | | | 1.25 | % | | | 1.25 | % | | | 1.25 | % |

| Other operating expenses | | | 0.37 | %3 | | | 0.34 | % | | | 0.50 | % | | | 0.49 | % | | | 0.42 | % | | | 0.46 | % |

| Total expenses (net) | | | 1.37 | %3 | | | 1.34 | % | | | 1.50 | % | | | 1.74 | % | | | 1.67 | % | | | 1.71 | % |

| Expenses excluding interest expense | | | 1.32 | %3 | | | 1.24 | % | | | 1.29 | % | | | 1.53 | % | | | 1.52 | % | | | 1.57 | % |

| Expenses prior to balance credits | | | 1.37 | %3 | | | 1.34 | % | | | 1.50 | % | | | 1.74 | % | | | 1.67 | % | | | 1.71 | % |

| Net investment income (loss) | | | 0.21 | %3 | | | (0.15 | )% | | | 0.46 | % | | | 0.30 | % | | | 0.21 | % | | | 0.69 | % |

| SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net Assets, End of Period (in thousands) | | $ | 91,676 | | | $ | 83,752 | | | $ | 142,810 | | | $ | 109,254 | | | $ | 130,526 | | | $ | 100,228 | |

| Portfolio Turnover Rate | | | 33 | % | | | 54 | % | | | 48 | % | | | 57 | % | | | 34 | % | | | 59 | % |

| REVOLVING CREDIT AGREEMENT: | | | | | | | | | | | | | | | | | | | | | | | | |

| Asset coverage | | | 2392 | % | | | 1147 | % | | | 1885 | % | | | 1466 | % | | | 1732 | % | | | 1353 | % |

| Asset coverage per $1,000 | | $ | 23,919 | | | $ | 11,469 | | | $ | 18,851 | | | $ | 14,657 | | | $ | 17,316 | | | $ | 13,528 | |

| 1 | The Market Value Total Return is calculated assuming a purchase of Common Stock on the opening of the first business day and a sale on the closing of the last business day of each period. Dividends and distributions are assumed for the purposes of this calculation to be reinvested at prices obtained under the Fund’s Distribution Reinvestment and Cash Purchase Plan. Net Asset Value Total Return is calculated on the same basis, except that the Fund’s net asset value is used on the purchase, sale and dividend reinvestment dates instead of market value. |

| 16 | 2021 Semiannual Report to Stockholders | THE ACCOMPANYING NOTES ARE AN INTEGRAL PART OF THESE FINANCIAL STATEMENTS |

Royce Global Value Trust

Notes to Financial Statements (unaudited)

Summary of Significant Accounting Policies

Royce Global Value Trust, Inc. (the “Fund”), is a diversified closed-end investment company that was incorporated under the laws of the State of Maryland on February 14, 2011. The Fund commenced operations on October 18, 2013.

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services-Investment Companies.”

Royce & Associates, LP, the Fund’s investment adviser, is a majority-owned subsidiary of Franklin Resources, Inc. and primarily conducts business using the name Royce Investment Partners (“Royce”).

VALUATION OF INVESTMENTS:

Securities are valued as of the close of trading on the New York Stock Exchange (NYSE) (generally 4:00 p.m. Eastern time) on the valuation date. Securities that trade on an exchange, and securities traded on Nasdaq’s Electronic Bulletin Board, are valued at their last reported sales price or Nasdaq official closing price taken from the primary market in which each security trades or, if no sale is reported for such day, at their highest bid price. Other over-the-counter securities for which market quotations are readily available are valued at their highest bid price, except in the case of some bonds and other fixed income securities which may be valued by reference to other securities with comparable ratings, interest rates and maturities, using established independent pricing services. The Fund values its non-U.S. dollar denominated securities in U.S. dollars daily at the prevailing foreign currency exchange rates as quoted by a major bank. Securities for which market quotations are not readily available are valued at their fair value in accordance with the provisions of the 1940 Act, under procedures approved by the Fund’s Board of Directors, and are reported as Level 3 securities. As a general principle, the fair value of a security is the amount which the Fund might reasonably expect to receive for the security upon its current sale. However, in light of the judgment involved in fair valuations, there can be no assurance that a fair value assigned to a particular security will be the amount which the Fund might be able to receive upon its current sale. In addition, if, between the time trading ends on a particular security and the close of the customary trading session on the NYSE, events occur that are significant and may make the closing price unreliable, the Fund may fair value the security. The Fund uses an independent pricing service to provide fair value estimates for relevant non-U.S. equity securities on days when the U.S. market volatility exceeds a certain threshold. This pricing service uses proprietary correlations it has developed between the movement of prices of non-U.S. equity securities and indices of U.S.-traded securities, futures contracts and other indications to estimate the fair value of relevant non-U.S. securities. When fair value pricing is employed, the prices of securities used by the Fund may differ from quoted or published prices for the same security. Investments in money market funds are valued at net asset value per share.

Various inputs are used in determining the value of the Fund’s investments, as noted above. These inputs are summarized in the three broad levels below:

| | Level 1 – | quoted prices in active markets for identical securities. |

| | Level 2 – | other significant observable inputs (including quoted prices for similar securities, foreign securities that may be fair valued and repurchase agreements). The table below includes all Level 2 securities. Any Level 2 securities with values based on quoted prices for similar securities would be noted in the Schedule of Investments. |

| | Level 3 – | significant unobservable inputs (including last trade price before trading was suspended, or at a discount thereto for lack of marketability or otherwise, market price information regarding other securities, information received from the company and/or published documents, including SEC filings and financial statements, or other publicly available information). |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s investments as of June 30, 2021. For a detailed breakout of common stocks by country, please refer to the Schedule of Investments.

| | | LEVEL 1 | | | LEVEL 2 | | | LEVEL 3 | | | TOTAL | |

| Common Stocks | | | $82,940,813 | | | | $ – | | | | $0 | | | | $82,940,813 | |

| Repurchase Agreement | | | – | | | | 12,652,210 | | | | – | | | | 12,652,210 | |

Level 3 Reconciliation:

| | BALANCE AS OF 12/31/20 | PURCHASES | SALES | REALIZED GAIN (LOSS) | UNREALIZED GAIN (LOSS) 1 | BALANCE AS OF 6/30/21 |

| Common Stocks | $0 | $– | $– | $– | $– | $0 |

| 1 | The net change in unrealized appreciation (depreciation) is included in the accompanying Statement of Operations. Change in unrealized appreciation (depreciation) includes net unrealized appreciation (depreciation) resulting from changes in investment values during the reporting period and the reversal of previously recorded unrealized appreciation (depreciation) when gains or losses are realized. Net realized gain (loss) from investments and foreign currency transactions is included in the accompanying Statement of Operations. |

| 2021 Semiannual Report to Stockholders | 17 |

Royce Global Value Trust

Notes to Financial Statements (unaudited) (continued)

REPURCHASE AGREEMENTS:

The Fund may enter into repurchase agreements with institutions that the Fund’s investment adviser has determined are creditworthy. The Fund restricts repurchase agreements to maturities of no more than seven days. Securities pledged as collateral for repurchase agreements, which are held until maturity of the repurchase agreements, are marked-to-market daily and maintained at a value at least equal to the principal amount of the repurchase agreement (including accrued interest). Repurchase agreements could involve certain risks in the event of default or insolvency of the counter-party, including possible delays or restrictions upon the ability of the Fund to dispose of its underlying securities. The remaining contractual maturity of the repurchase agreement held by the Fund at June 30, 2021 is overnight and continuous.

FOREIGN CURRENCY:

Net realized foreign exchange gains or losses arise from sales and maturities of short-term securities, sales of foreign currencies, expiration of currency forward contracts, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the value of assets and liabilities, other than investments in securities at the end of the reporting period, as a result of changes in foreign currency exchange rates.

The Fund does not isolate that portion of the results of operations resulting from fluctuations in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

DISTRIBUTIONS AND TAXES:

As a qualified regulated investment company under Subchapter M of the Internal Revenue Code, the Fund is not subject to income taxes to the extent that it distributes substantially all of its taxable income for its fiscal year. The Schedule of Investments includes information regarding income taxes under the caption “Tax Information.”

The Fund pays any dividends and capital gain distributions annually in December. Because federal income tax regulations differ from generally accepted accounting principles, income and capital gain distributions determined in accordance with tax regulations may differ from net investment income and realized gains recognized for financial reporting purposes. Accordingly, the character of distributions and composition of net assets for tax purposes differ from those reflected in the accompanying financial statements.

CAPITAL GAINS TAXES:

The Fund may be subject to a tax imposed on capital gains on securities of issuers domiciled in certain countries. The Fund records an estimated deferred tax liability for gains in these securities that have been held for less than one year. This amount, if any, is reported as deferred capital gains tax in the accompanying Statement of Assets and Liabilities, assuming those positions were disposed of at the end of the period.

INVESTMENT TRANSACTIONS AND RELATED INVESTMENT INCOME:

Investment transactions are accounted for on the trade date. Dividend income is recorded on the ex-dividend date. Non-cash dividend income is recorded at the fair market value of the securities received. Interest income is recorded on an accrual basis. Premiums and discounts on debt securities are amortized using the effective yield-to-maturity method. Realized gains and losses from investment transactions are determined on the basis of identified cost for book and tax purposes.

EXPENSES:

The Fund incurs direct and indirect expenses. Expenses directly attributable to the Fund are charged to the Fund’s operations, while expenses applicable to more than one of the Royce Funds are allocated equitably. Certain personnel, occupancy costs and other administrative expenses related to the Funds are allocated by Royce under an administration agreement and are included in administrative and office facilities and professional fees.

COMPENSATING BALANCE CREDITS:

The Fund has an arrangement with its custodian bank, whereby a portion of the custodian’s fee is paid indirectly by credits earned on the Fund’s cash on deposit with the bank. This deposit arrangement is an alternative to purchasing overnight investments. Conversely, the Fund pays interest to the custodian on any cash overdrafts, to the extent they are not offset by credits earned on positive cash balances.

Capital Stock:

The Fund issued 349,058 shares of Common Stock as reinvestment of distributions for the year ended December 31, 2020.

| 18 | 2021 Semiannual Report to Stockholders |

Royce Global Value Trust

Notes to Financial Statements (unaudited) (continued)

Capital Stock (continued):

On October 28, 2020, the Fund announced the commencement of a conditional cash tender offer for up to 40% of the Fund’s issued and outstanding shares of common stock as of October 12, 2020 (i.e., 4,201,388 shares) at a price per share equal to 100% of the Fund’s net asset value per share as of the close of regular trading on the New York Stock Exchange (the “NYSE”) on the trading day immediately following the expiration date for the offer. The tender offer was set to expire at 11:59 p.m. Eastern Time on December 16, 2020, unless extended. The closing of the tender offer was contingent on the Fund’s stockholders approving a new investment advisory agreement between the Fund and Royce in accordance with the requirements of the Investment Company Act of 1940.

On December 7, 2020, the Fund announced its Board of Directors had approved amended terms for its previously announced conditional cash tender offer. The Fund offered to purchase up to 50% of its issued and outstanding shares of common stock as of October 12, 2020 (i.e., 5,251,735 shares) at a price per share equal to 100% of the Fund’s net asset value per share as of the close of regular trading on the NYSE on the trading day immediately following the expiration date for the offer. The expiration date for the tender offer was extended until 11:59 P.M. on December 21, 2020. The closing of the tender offer, however, remained contingent on stockholder approval of a new investment advisory agreement between the Fund and Royce.

The Fund’s stockholders approved a new investment advisory agreement between the Fund and Royce at a special meeting of stockholders held on December 17, 2020. In accordance with the terms and conditions of the tender offer, because the number of shares tendered by stockholders exceeded the number of shares offered to be purchased by the Fund, the Fund purchased the full amount of 5,251,735 shares from tendering stockholders on a pro-rata basis (disregarding fractional shares). The purchase price of the properly tendered shares was equal to $14.43 per share (the Fund’s net asset value per share as of the close of regular trading on the NYSE on December 22, 2020) for an aggregate purchase price of $75,782,536. The direct expenses associated with the conduct of the tender offer and the preparation of the tender offer materials, including legal fees, information agent fees, depositary fees, and the costs of printing and mailing the tender offer materials, were borne by Franklin Resources, Inc., Royce’s ultimate corporate parent, and not by the Fund.

Borrowings:

The Fund is party to a revolving credit agreement (the credit agreement) with BNP Paribas Prime Brokerage International, Limited (BNPPI). The Fund pays a commitment fee of 0.50% per annum on the unused portion of the then-current maximum amount that may be borrowed by the Fund under the credit agreement. The credit agreement has a 179-day rolling term that resets daily. The Fund is required to pledge portfolio securities as collateral in an amount up to two times the loan balance outstanding, or as otherwise required by applicable regulatory standards, and has granted a security interest in the securities pledged to, and in favor of, BNPPI as security for the loan balance outstanding. If the Fund fails to meet certain requirements, or comply with other financial covenants set forth in the credit agreement, the Fund may be required to repay immediately, in part or in full, the loan balance outstanding under the credit agreement, which may necessitate the sale of portfolio securities at potentially inopportune times. BNPPI may terminate the credit agreement upon certain ratings downgrades of its corporate parent, which would result in the Fund’s entire loan balance becoming immediately due and payable. The occurrence of such ratings downgrades may necessitate the sale of portfolio securities at potentially inopportune times. BNPPI may also terminate the credit agreement upon sixty (60) calendar days’ prior written notice to the Fund in the event the Fund’s net asset value per share as of the close of business on the last business day of any calendar month declines by thirty-five percent (35%) or more from the Fund’s net asset value per share as of the close of business on the last business day of the immediately preceding calendar month.

The credit agreement also permits, subject to certain conditions, BNPPI to rehypothecate portfolio securities pledged by the Fund up to the amount of the loan balance outstanding. The Fund continues to receive payments in lieu of dividends and interest on rehypothecated securities. The Fund also has the right under the credit agreement to recall the rehypothecated securities from BNPPI on demand. If BNPPI fails to deliver the recalled security in a timely manner, the Fund is compensated by BNPPI for any fees or losses related to the failed delivery or, in the event a recalled security is not returned by BNPPI, the Fund, upon notice to BNPPI, may reduce the loan balance outstanding by the value of the recalled security failed to be returned. The Fund receives a portion of the fees earned by BNPPI in connection with the rehypothecation of portfolio securities.

The maximum amount the Fund could borrow under the credit agreement during the year ended December 31, 2020 was $8,000,000. Such maximum borrowing amount was subsequently reduced from $8,000,000 to $4,000,000 through an amendment to the credit agreement dated as of January 6, 2021. The Fund has the right to further reduce the maximum amount it can borrow under the credit agreement upon one (1) business day’s prior written notice to BNPPI. In addition, the Fund and BNPPI may agree to increase the maximum amount the Fund can borrow under the credit agreement, which amount may not exceed $15,000,000.