P3YP3Yhttp://fasb.org/us-gaap/2024#RelatedPartyMemberhttp://fasb.org/us-gaap/2024#RelatedPartyMemberhttp://fasb.org/us-gaap/2024#RelatedPartyMemberhttp://fasb.org/us-gaap/2024#RelatedPartyMemberhttp://fasb.org/us-gaap/2024#UnrealizedGainLossOnInvestmentshttp://fasb.org/us-gaap/2024#UnrealizedGainLossOnInvestmentshttp://fasb.org/us-gaap/2024#OtherAssetshttp://fasb.org/us-gaap/2024#OtherAssets

Blackstone Inc. (“Blackstone”) is filing this exhibit (the “Exhibit”) to update certain information in Part I. Item 1. Business and to reflect changes to the presentation of its financial information as set forth in its Annual Report on

Form 10-K

for the year ended December 31, 2023 (“Blackstone’s

10-K”),

as filed with the SEC on February 23, 2024. This Exhibit is being filed solely to retrospectively recast Blackstone’s historical segment reporting financial information to reflect changes effective the quarter ended June 30, 2024, as previously disclosed. This Exhibit speaks as of the original filing date of Blackstone’s

10-K,

does not reflect events that may have occurred subsequent to the original filing date and does not modify or update in any way the disclosures made other than as required to reflect the revised segment information and to identify the current names and compositions of Blackstone’s existing segments, businesses and platforms.

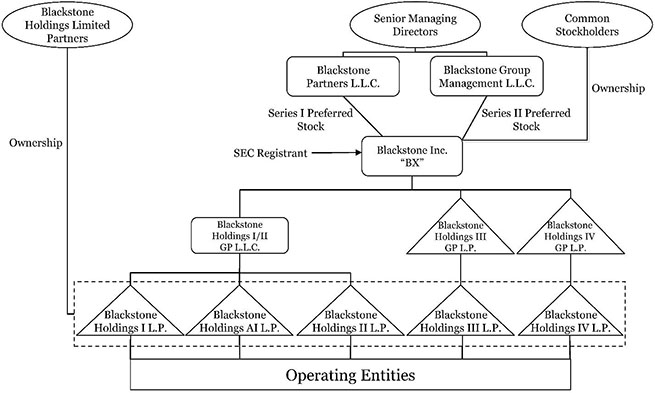

In this report, references to “Blackstone,” the “Company,” “we,” “us” or “our” refer to Blackstone Inc. and its consolidated subsidiaries.

“Series I Preferred Stockholder” refers to Blackstone Partners L.L.C., the holder of the sole outstanding share of our Series I preferred stock.

“Series II Preferred Stockholder” refers to Blackstone Group Management L.L.C., the holder of the sole outstanding share of our Series II preferred stock.

“Blackstone Funds,” “our funds” and “our investment funds” refer to the funds and other vehicles that are managed by Blackstone. “Our carry funds” refers to funds managed by Blackstone that have commitment-based multi-year drawdown structures that pay carry on the realization of an investment.

“Our hedge funds” refers to our funds of hedge funds, hedge funds, certain of our real estate debt investment funds and certain other credit-focused funds which are managed by Blackstone.

We refer to our separately managed accounts as “SMAs.”

“Total Assets Under Management” refers to the assets we manage. Our Total Assets Under Management equals the sum of:

| | (a) | the fair value of the investments held by our carry funds and our and co-investment entities managed by us plus the capital that we are entitled to call from investors in those funds and entities pursuant to the terms of their respective capital commitments, including capital commitments to funds that have yet to commence their investment periods, |

| | (b) | the net asset value of (1) our hedge funds, real estate debt carry funds, Blackstone Property Partners (“BPP”) funds, certain co-investments managed by us, certain credit-focused funds, and our Multi-Asset Investing drawdown funds (plus, in each case, the capital that we are entitled to call from investors in those funds, including commitments yet to commence their investment periods), and (2) our funds of hedge funds, our Multi-Asset Investing registered investment companies, Blackstone Real Estate Income Trust, Inc. (“BREIT”) and Blackstone European Property Income (“BEPIF”) funds, |

| | (c) | the invested capital, fair value or net asset value of assets we manage pursuant to separately managed accounts, |

| | (d) | the amount of debt and equity outstanding for our collateralized loan obligations (“CLO”) during the reinvestment period, |

| | (e) | the aggregate par amount of collateral assets, including principal cash, for our CLOs after the reinvestment period, |

| | (f) | the gross or net amount of assets (including leverage where applicable) for our credit-focused registered investment companies and business development companies (“BDCs”), |

| | (g) | the fair value of common stock, preferred stock, convertible debt, term loans or similar instruments issued by Blackstone mortgage Trust, Inc. (“BXMT”) and |

| | (h) | borrowings under and any amounts available to be borrowed under certain credit facilities of our funds. |

Our carry funds are commitment-based drawdown structured funds that do not permit investors to redeem their interests at their election. Our funds of hedge funds, hedge funds, funds structured like hedge funds and other open-ended funds in our Real Estate, Credit & Insurance and Multi-Asset Investing segments generally have structures that afford an investor the right to withdraw or redeem their interests on a periodic basis (for example, annually, quarterly or monthly), typically with 2 to 95 days’ notice, depending on the fund and the liquidity profile of the underlying assets. In our Perpetual Capital vehicles where redemption rights exist, Blackstone has the ability

to fulfill redemption requests only (a) in Blackstone’s or the vehicles’ board’s discretion, as applicable, or (b) to the extent there is sufficient new capital. Investment advisory agreements related to certain separately managed accounts in our Credit & Insurance and Multi-Asset Investing segments, excluding our separately managed accounts in our insurance platform, may generally be terminated by an investor on 30 to 90 days’ notice. Separately managed accounts in our insurance platform can generally only be terminated for long-term underperformance, cause and certain other limited circumstances, in each case subject to Blackstone’s right to cure.

“Fee-Earning

Assets Under Management” refers to the assets we manage on which we derive management fees and/or performance revenues. Our

Fee-Earning

Assets Under Management equals the sum of:

| | (a) | for our Private Equity segment funds, Real Estate segment carry funds including certain Blackstone Real Estate Debt Strategies (“BREDS”) funds, and certain Multi-Asset Investing funds, the amount of capital commitments, remaining invested capital, fair value, net asset value or par value of assets held, depending on the fee terms of the fund, |

| | (b) | for our credit-focused carry funds, the amount of remaining invested capital (which may include leverage) or net asset value, depending on the fee terms of the fund, |

| | (c) | the remaining invested capital or fair value of assets held in co-investment vehicles managed by us on which we receive fees, |

| | (d) | the net asset value of our funds of hedge funds, hedge funds, BPP, certain co-investments managed by us, certain registered investment companies, BREIT, BEPIF, and certain of our Multi-Asset Investing drawdown funds, |

| | (e) | the invested capital, fair value of assets or the net asset value we manage pursuant to separately managed accounts, |

| | (f) | the net proceeds received from equity offerings and accumulated distributable earnings of BXMT, subject to certain adjustments, |

| | (g) | the aggregate par amount of collateral assets, including principal cash, of our CLOs and |

| | (h) | the gross amount of assets (including leverage) or the net assets (plus leverage where applicable) for certain of our credit-focused registered investment companies and BDCs. |

Each of our segments may include certain

Fee-Earning

Assets Under Management on which we earn performance revenues but not management fees.

Our calculations of Total Assets Under Management and

Fee-Earning

Assets Under Management may differ from the calculations of other asset managers, and as a result this measure may not be comparable to similar measures presented by other asset managers. In addition, our calculation of Total Assets Under Management includes commitments to, and the fair value of, invested capital in our funds from Blackstone and our personnel, regardless of whether such commitments or invested capital are subject to fees. Our definitions of Total Assets Under Management and

Fee-Earning

Assets Under Management are not based on any definition of Total Assets Under Management and

Fee-Earning

Assets Under Management that is set forth in the agreements governing the investment funds that we manage.

For our carry funds, Total Assets Under Management includes the fair value of the investments held and uncalled capital commitments, whereas

Fee-Earning

Assets Under Management may include the total amount of capital commitments or the remaining amount of invested capital at cost, depending on whether the investment period has expired or as specified by the fee terms of the fund. As such, in certain carry funds

Fee-Earning

Assets Under Management may be greater than Total Assets Under Management when the aggregate fair value of the remaining investments is less than the cost of those investments.

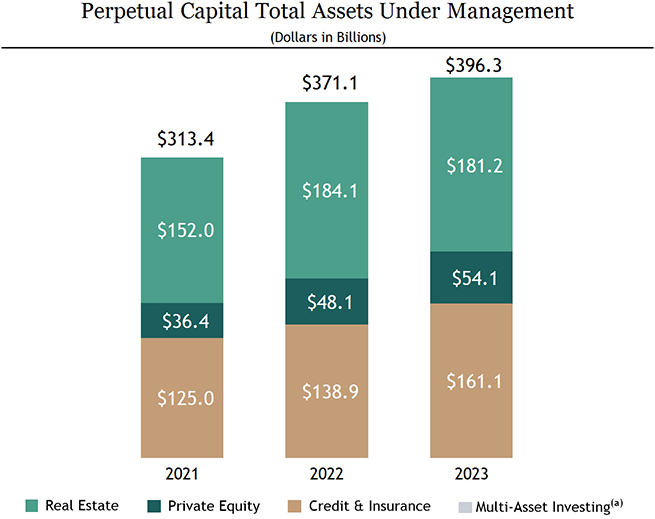

“Perpetual Capital” refers to the component of assets under management with an indefinite term, that is not in liquidation, and for which there is no requirement to return capital to investors through redemption requests in the ordinary course of business, except where funded by new capital inflows. Perpetual Capital includes

co-investment

capital with an investor right to convert into Perpetual Capital.

This report does not constitute an offer of any Blackstone Fund.

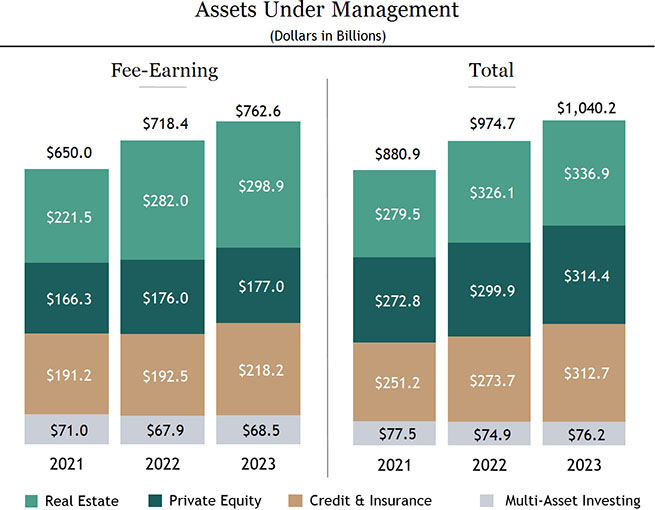

Blackstone is the world’s largest alternative asset manager. We seek to deliver compelling returns for institutional and individual investors by strengthening the companies and assets in which we invest. Our more than $1.0 trillion in Total Assets Under Management as of December 31, 2023 include global investment strategies focused on real estate, private equity, infrastructure, life sciences, growth equity, credit, real assets, secondaries and hedge funds.

Our businesses use a solutions-oriented approach to drive better performance. We believe our scale, diversified business, long record of investment performance, rigorous investment process and strong client relationships position us to continue to perform well in a variety of market conditions, expand our assets under management, and innovate.

We invest across asset classes on behalf of our investors, including pension funds, insurance companies and individual investors. Our mission is to fulfill our fiduciary duty by creating long-term value for our investors. We aim to do this by strengthening the companies, real estate assets and other investments in our portfolio, equipping them to thrive in the global economy. To the extent our funds perform well, we can support a better retirement for tens of millions of pensioners, including teachers, nurses and firefighters.

As of December 31, 2023, we employed approximately 4,735 people, including our 239 senior managing directors, at our headquarters in New York and around the world. Our employees are integral to Blackstone’s culture of integrity, professionalism and excellence. We believe hiring, training and retaining talented individuals, coupled with our rigorous investment process, has supported our excellent investment record over many years. This record, in turn, has enabled us to innovate into new strategies, drive growth and better serve our investors.

Our four business segments are: (a) Real Estate, (b) Private Equity, (c) Credit & Insurance and (d) Multi-Asset Investing.

Information about our business segments should be read together with “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

For more information concerning the revenues and fees we derive from our business segments, see “—Fee Structure/Incentive Arrangements.”

Our Real Estate business is a global leader in real estate investing, with $336.9 billion of Total Assets Under Management as of December 31, 2023. Our Real Estate segment operates as one globally integrated business with approximately 870 employees and has investments across the globe, including in the Americas, Europe and Asia. Our real estate investment teams seek to utilize our global expertise and presence to generate attractive risk-adjusted returns for our investors.

Our Blackstone Real Estate Partners (“BREP”) business is geographically diversified and targets a broad range of opportunistic real estate and real estate-related investments. The BREP platform includes global funds as well as funds focused specifically on Europe or Asia investments. BREP seeks to invest thematically in high-quality assets, focusing where we see outsized growth potential driven by global economic and demographic trends. BREP has made significant investments in logistics, rental housing, hospitality, office and retail properties around the world, as well as in a variety of real estate operating companies.

Our Core+ real estate strategy invests in substantially stabilized real estate globally primarily through perpetual capital vehicles. Our Core+ real estate strategy includes our (a) Blackstone Property Partners (“BPP”) funds, which is focused on high-quality assets in the Americas, Europe and Asia and (b) our

non-listed

REIT, Blackstone Real Estate Income Trust, Inc. (“BREIT”) and our Blackstone European Property Income (“BEPIF”) vehicles, which provide income-focused individual investors access to institutional quality real estate primarily in the Americas and Europe, respectively.

Our Blackstone Real Estate Debt Strategies (“BREDS”) platform primarily targets real estate-related debt investment opportunities. BREDS invests in both public and private markets, primarily in the U.S. and Europe. BREDS’ scale and investment mandates enable it to provide a variety of lending options for our borrowers and investment options for our investors, including commercial real estate and mezzanine loans, residential mortgage loan pools and liquid real estate-related debt securities. The BREDS platform includes high-yield real estate debt funds, liquid real estate debt funds and Blackstone Mortgage Trust, Inc. (“BXMT”), a NYSE-listed real estate investment trust (“REIT”).

Our Private Equity segment encompasses global businesses with a total of approximately 650 employees managing $314.4 billion of Total Assets Under Management as of December 31, 2023. Our Private Equity segment includes our Corporate Private Equity business, which consists of: (a) our global private equity funds, Blackstone Capital Partners (“BCP”), (b) our sector-focused funds, including our energy- and energy transition-focused funds, Blackstone Energy Transition Partners (“BETP”), (c) our Asia-focused private equity funds, Blackstone Capital Partners Asia and (d) our core private equity funds, Blackstone Core Equity Partners (“BCEP”). Our Private Equity segment also includes (a) our opportunistic investment platform that invests flexibly across asset classes, industries and geographies, Blackstone Tactical Opportunities (“Tactical Opportunities”), (b) our secondary funds business, Strategic Partners Fund Solutions (“Strategic Partners”), and our business that targets minority investments in the general partners of private equity and other private market alternative asset management firms (“GP Stakes”) as “Secondaries”, (c) our infrastructure-focused funds, Blackstone Infrastructure Partners (“BIP”), (d) our life sciences investment platform, Blackstone Life Sciences (“BXLS”), (e) our growth equity investment platform, Blackstone Growth (“BXG”), (f) our investment platform offering eligible individual investors access to Blackstone’s private equity capabilities, Blackstone Private Equity Strategies Fund (“BXPE”), (g) our multi-asset investment program for eligible

investors offering exposure to certain of Blackstone’s key illiquid investment strategies through a single commitment, Blackstone Total Alternatives Solution (“BTAS”) and (h) our capital markets services business, Blackstone Capital Markets (“BXCM”).

We are a global leader in private equity investing. Our Corporate Private Equity business pursues transactions across industries on a global basis. It strives to create value by investing in great businesses where our capital, strategic insight, global relationships and operational support can drive transformation. Corporate Private Equity’s investment strategies and core themes continually evolve in anticipation of, or in response to, changes in the global economy, local markets, regulation, capital flows and geopolitical trends. We seek to construct a differentiated portfolio of investments with a well-defined, post-acquisition value creation strategy. Similarly, we seek investments that can generate strong unlevered returns regardless of entry or exit cycle timing.

BCEP pursues control-oriented investments in high-quality companies with durable businesses and seeks to offer a lower level of risk and a longer hold period than traditional private equity.

Tactical Opportunities pursues a thematically driven, opportunistic investment strategy. Our flexible, global mandate enables us to find differentiated opportunities across asset classes, industries and geographies and invest behind them with the frequent use of structure to generate attractive risk-adjusted returns. Tactical Opportunities’ ability to dynamically shift focus to the most compelling opportunities in any market environment, combined with the business’ expertise in structuring complex transactions, enables Tactical Opportunities to invest in attractive market areas, often with securities that provide downside protection and maintain upside return.

Secondaries is comprised of our Strategic Partners and GP Stakes businesses. Strategic Partners is a total fund solutions provider. As a secondary investor, it acquires interests in high-quality private funds from original holders seeking liquidity. Strategic Partners focuses on a range of opportunities in underlying funds such as private equity, real estate, infrastructure, venture and growth capital, credit and other types of funds, as well as general

partner-led

transactions and primary investments and

co-investments

with financial sponsors. Strategic Partners also provides investment advisory services to separately managed account clients investing in primary and secondary investments in private funds and

co-investments.

Effective the quarter ended June 30, 2024, our GP Stakes business moved from our Multi-Asset Investment segment to our Private Equity segment. GP Stakes targets minority investments in the general partners of private equity and other private market alternative asset management firms globally, with a focus on delivering a combination of recurring annual cash flow yield and long-term capital appreciation.

BIP targets a diversified mix of core+, core and public-private partnership investments across all infrastructure sectors, including energy infrastructure, transportation, digital infrastructure and water and waste, with a primary focus in the U.S. BIP applies a disciplined, operationally intensive investment approach to investments, seeking to apply a long-term

strategy to large-scale infrastructure assets with a focus on delivering stable, long-term capital appreciation together with a predictable annual cash flow yield.

BXLS invests across the life cycle of companies and products within the life sciences sector. BXLS primarily focuses on investments in life sciences products in late-stage clinical development within the pharmaceutical, biotechnology and medical technology sectors.

BXG seeks to deliver attractive risk-adjusted returns by investing in dynamic, growth-stage businesses, with a focus on the consumer, consumer technology, enterprise solutions, financial services and healthcare sectors.

BXPE invests primarily in privately negotiated, equity-oriented investments, leveraging the talent and investment capabilities of Blackstone’s private equity platform to create an attractive portfolio of alternative investments diversified across geographies and sectors for eligible individual investors.

Our Credit & Insurance segment has approximately 625 employees and manages $312.7 billion of Total Assets Under Management as of December 31, 2023. Effective January 1, 2024, our corporate credit (formerly Blackstone Credit or BXC), asset based finance and insurance (“insurance platform” and formerly Blackstone Insurance Solutions or BIS) groups were integrated into a single new unit, Blackstone Credit & Insurance (“BXCI”). BXCI offers its clients and borrowers a comprehensive solution across corporate and asset based, as well as investment grade and

non-investment

grade, private credit. BXCI is one of the largest credit-oriented managers and CLO managers in the world. The investment portfolios of the funds BXCI’s credit platform manages or

sub-advises

consist primarily of loans and securities of

non-investment

and investment grade companies spread across the capital structure including senior debt, subordinated debt, preferred stock and common equity.

BXCI is organized into three overarching credit investing strategies: private corporate credit, liquid corporate credit and infrastructure and asset based credit. The private corporate credit strategies include mezzanine and direct lending funds, private placement strategies and stressed/distressed strategies. The direct lending funds include Blackstone Private Credit Fund (“BCRED”) and Blackstone Secured Lending Fund (“BXSL”), both of which are business development companies (“BDCs”). The liquid corporate credit strategies consist of CLOs, closed-ended funds, open-ended funds, systematic strategies and separately managed accounts. The infrastructure and asset based credit strategies include our energy strategies (including our sustainable resources platform) and asset based finance strategies focused on privately originated, income-oriented credit assets secured by physical or financial collateral.

Our insurance platform focuses on providing full investment management services for insurers’ general accounts, seeking to deliver customized and diversified portfolios that include allocations to Blackstone managed products and strategies across asset classes and Blackstone’s private credit origination capabilities. Through this platform, we provide our clients tailored portfolio construction and strategic asset allocation, seeking to generate risk-managed, capital-efficient returns, diversification and capital preservation that meets clients’ objectives. We also provide similar services to clients through separately managed accounts or by

sub-managing

assets for certain insurance-dedicated funds and special purpose vehicles. Through the insurance platform, we currently manage assets for clients that include Corebridge Financial Inc., Everlake Life Insurance Company, Fidelity & Guaranty Life Insurance Company and Resolution Life Group, among others.

Effective the quarter ended March 31, 2024, our Hedge Fund Solutions segment was renamed “Multi-Asset Investing.” Working with our clients for more than 30 years, our Multi-Asset Investing group is a leading manager of institutional funds with approximately 245 employees managing $76.2 billion of Total Assets Under Management as of December 31, 2023. Our Multi-Asset Investing segment seeks to grow investors’ assets through investment strategies designed to deliver, primarily through the public markets, compelling risk-adjusted returns. Blackstone Multi-Asset Investing (“BXMA”) is the world’s largest discretionary allocator to hedge funds, managing a broad range of commingled and customized fund solutions since its inception in 1990. BXMA is organized into two primary platforms: Absolute Return and Multi-Strategy. Absolute Return is designed to pursue consistent, efficient and diversifying returns across multiple market environments. Absolute Return manages a broad range of commingled and customized fund solutions, a seeding business and registered funds that provide alternative asset solutions through daily liquidity products. Multi-Strategy aims to generate strong risk-adjusted returns through opportunistic, asset-class agnostic investing, including structured risk transfer and equity capital markets strategies. Effective the quarter ended June 30, 2024, our platform managed by Harvest Fund Advisors LLC (“Harvest”) moved from our Credit & Insurance segment to our Multi-Asset Investing segment. Harvest primarily invests in publicly traded energy infrastructure, renewables and master limited partnerships holding midstream energy assets in North America.

Each of our business segments currently includes Perpetual Capital assets under management, which refers to assets under management with an indefinite term, that are not in liquidation and for which there is no requirement to return capital to investors through redemption requests in the ordinary course of business, except where funded by new capital inflows. In recent years, we have continued to meaningfully increase our assets under management in such vehicles. Perpetual Capital strategies represent a significant and growing portion of our overall business, and the management fees and performance revenues we receive. Among the strategies in each of our segments, Perpetual Capital strategies include, without limitation, (a) in our Real Estate segment, Core+ real estate (including BREIT and BEPIF) and BXMT, (b) in our Private Equity segment, BIP, GP Stakes and BXPE, and (c) in our Credit & Insurance segment, BXSL and BCRED. In addition, assets managed for certain of our insurance clients are Perpetual Capital assets under management.

Blackstone’s business historically focused on the provision of investment products, such as traditional drawdown funds, to institutional investors. In recent years, we have considerably expanded the number and type of investment products we offer through various distribution channels to certain

and mass affluent individual investors in the U.S. and other jurisdictions around the world. Our Private Wealth Solutions business is dedicated to building out our distribution capabilities in the private wealth channel to provide certain individual investors with access to Blackstone products across a broad array of alternative investment strategies. In recent years, capital from the private wealth channel has represented an increasing portion of our Total Assets Under Management, and we expect this trend to continue as we continue to undertake initiatives focused on this market segment.

Investment Process and Risk Management

We maintain a rigorous investment process across all of our investment vehicles. Each investment vehicle has investment policies and procedures that generally contain requirements, guidelines and limitations for investments, such as limitations relating to the amount that will be invested in any one investment and the types of assets, industries or geographic regions in which the vehicle will invest, as well as limitations required by law.

Our investment professionals are responsible for identifying, evaluating, underwriting, diligencing, negotiating, executing, managing and exiting investments. For those of our businesses with review committees and/or investment committees, such committees review and evaluate investment opportunities in a framework that includes a qualitative and quantitative assessment of the key risks of investments. In such businesses, investment professionals generally submit investment opportunities for review and approval by a review committee and/or investment committee, subject to delineated exceptions set forth in the funds’ investment committee charters or resolutions. Review and investment committees are generally comprised of senior leaders and other senior professionals of the applicable investment business, and in many cases, other senior leaders of Blackstone and its businesses. Considerations that review and investment committees take into account when evaluating an investment may include, without limitation and depending on the nature of the investing business and its strategy, the quality of the business or asset in which the fund proposes to invest, the quality of the management team, likely exit strategies and factors that could reduce the value of the business or asset at exit, the ability of the business in which the investment is made to service debt in a range of economic and interest rate environments, macroeconomic trends in the relevant geographic region or industry and the quality of the businesses’ operations. In addition, the majority of our businesses have ESG policies that address, among other things, the review of ESG risks in the respective business’s investment process. Existing investments are reviewed and monitored on a regular basis by investment and asset management professionals. In addition, our investment professionals, Portfolio Operations professionals work with our portfolio company senior executives to identify opportunities to drive operational efficiencies and growth.

In addition, before deciding to invest in an investment fund or an alternative asset manager, as applicable, our Multi-Asset Investing and Secondaries teams conduct diligence in a number of areas, which, depending on the nature of the investment, may include, among others, the fund’s/manager’s performance, investment terms, investment strategy and investment personnel, as well as its operations, processes, risk management and internal controls. With respect to liquid credit clients and other clients whose portfolios are actively traded in our Credit & Insurance segment, our industry-focused research analysts provide the review and/or investment committee with a formal and comprehensive review of new investment recommendations and portfolio managers and trading

professionals discuss, among other things, risks associated with overall portfolio composition. Our Credit & Insurance segment’s research team monitors the operating performance of underlying issuers, while portfolio managers, together with our traders, focus on optimizing asset composition to maximize value for our investors. This investment process is assisted by a variety of proprietary and

non-proprietary

research models and methods.

Structure and Operation of Our Investment Vehicles

Our asset management businesses include private investment funds, registered funds, BDCs, REITs, CLOs, SMAs and other vehicles focused on real estate, private equity, infrastructure, life sciences, growth equity, credit, real assets and secondary funds, all on a global basis. Many of our private investment funds and other vehicles are targeted at institutional investors. We also have several products, such as BREIT, BCRED and BXPE, among others, that are targeted at individual investors, including

investors (“Private Wealth Products”).

Our private investment funds are generally organized as limited partnerships with respect to U.S. domiciled vehicles and limited partnerships or other similar limited liability entities with respect to

non-U.S.

domiciled vehicles. These funds accept commitments and/or subscriptions for investment from institutional investors and/or

individuals. Our Private Wealth Products are organized using a variety of structures, including corporations, statutory trusts, limited partnerships or other vehicles, and accept subscriptions for investment from

individuals and/or other individual investors. Our private investment funds are generally either commitment-structured funds, where commitments are generally drawn down from investors on an

as-needed

basis to fund investments (or for other permitted purposes) over a specified term, or open-ended funds, where the investor’s capital may be fully funded on or shortly after the investor’s subscription date and cash proceeds resulting from the disposition of investments can be reinvested, subject to certain limitations and limited investor withdrawal rights. In most of our Private Wealth Products, the investor’s capital is fully funded on the subscription date. Our BXCI insurance platform is generally structured around separately managed accounts and our BXCI CLO vehicles are generally private companies with limited liability.

Our investment funds, separately managed accounts and other vehicles not domiciled in the European Economic Area (the “EEA”) are each generally advised by a Blackstone entity serving as investment adviser that is registered under the U.S. Investment Advisers Act of 1940, as amended (the “Advisers Act”). For our investment funds, separately managed accounts and other vehicles domiciled in the EEA, a Blackstone entity domiciled in the EEA generally serves as external alternative investment fund manager (“AIFM”), and the AIFM typically delegates its portfolio management function to a Blackstone-affiliated investment adviser registered under the Advisers Act. The Blackstone entity serving as investment adviser or AIFM, as applicable, typically carries out substantially all of the

operations of each investment vehicle pursuant to an investment advisory, investment management, AIFM or other similar agreement. Generally, the material terms of our investment advisory and AIFM agreements, as applicable, relate to the scope of services to be rendered by the investment adviser or the AIFM to the applicable vehicle, the calculation of management fees to be borne by investors in our investment vehicles, the calculation of and the manner and extent to which other fees received by the investment adviser or the AIFM, as applicable, from funds or fund portfolio companies serve to offset or reduce the management fees payable by investors in our investment vehicles and certain rights of termination with respect to our investment advisory and AIFM agreements.

Our private investment funds do not generally register as investment companies under the U.S. Investment Company Act of 1940, as amended (the “1940 Act”), in reliance on the statutory exemptions provided by Section 3(c)(7), Section 3(c)(5)(C) or Section 3(c)(1) thereof. Section 3(c)(7) of the 1940 Act exempts from its registration requirements investment vehicles privately placed in the United States whose securities are beneficially owned exclusively by persons who, at the time of acquisition of such securities, are “qualified purchasers” as defined under the 1940 Act. In addition, under current interpretations of the SEC, Section 3(c)(7) of

the 1940 Act exempts from registration any

non-U.S.

investment vehicle all of whose outstanding securities are beneficially owned either by

non-U.S.

residents or by U.S. residents that are qualified purchasers. Section 3(c)(5)(C) of the 1940 Act exempts from its registration requirements certain companies engaged primarily in investment in mortgages and other liens or investments in real estate. Section 3(c)(1) of the 1940 Act exempts from its registration requirements privately placed investment vehicles whose securities are beneficially owned by not more than 100 persons. Additionally, under current interpretations of the SEC, Section 3(c)(1) of the 1940 Act exempts from registration any

non-U.S.

investment vehicle not publicly offered in the U.S. all of whose outstanding securities are beneficially owned by not more than 100 U.S. residents. In addition, each of BXMT and BREIT conducts its operations in a manner that allows it to maintain its REIT qualification and avail itself of the statutory exemption provided by Section 3(c)(5)(C) of the 1940 Act and our U.S. BXPE vehicle relies on Section 3(c)(7) of the 1940 Act. Our Private Wealth Products include funds that are registered, or regulated as a BDC, under the 1940 Act. In addition, certain of our investment advisers or AIFMs advise or

sub-advise

funds domiciled in, and subject to registration and regulatory requirements of, the EEA.

In addition to having an investment adviser, each investment fund that is a limited partnership, or “partnership” fund, also has a general partner that, apart from partnership funds domiciled in the EEA, generally makes all operational and investment decisions, including the making, monitoring and disposing of investments. Investment vehicles in our Private Wealth Products typically have a board that includes independent directors. In the case of our separately managed accounts, the investor, rather than we, generally holds or has custody of the investments. The investors in our investment funds generally take no part in the conduct or control of the business of the investment funds, have no right or authority to act for or bind the investment funds and have no influence over the voting or disposition of the securities or other assets held by the investment funds. Third party investors in some of our partnership funds have the right to remove the general partner of the fund or to accelerate the termination of the fund without cause by a majority or supermajority vote. In addition, the governing agreements of many of our partnership funds provide that in the event certain “key persons” in our partnership funds do not meet specified time commitments with regard to managing the fund, then (a) investors in such funds have the right to vote to terminate the investment period by a specified percentage (including, in certain cases a simple majority) vote in accordance with specified procedures, or accelerate the withdrawal of their capital on an

basis, or (b) the fund’s investment period will automatically terminate and a specified percentage (including, in certain cases a simple majority) in accordance with specified procedures is required to restart it. In addition, the governing agreements of some of our partnership funds provide that investors have the right to terminate the investment period for any reason by a supermajority vote of the investors in such fund.

Fee Structure/Incentive Arrangements

The following is a general description of the management fees earned by Blackstone. Management fees are generally based on an annual rate but payable on a regular basis (typically monthly or quarterly). Management fees received are not subject to clawback.

| | • | | In our carry funds, the investment adviser or AIFM (depending on the domicile of the fund) receives a management fee based on a percentage of the fund’s capital commitments, invested capital and/or undeployed capital during the investment period and the fund’s invested capital, investment fair value or capital commitments after the investment period. Management fees are generally payable over either the term or life of the fund. Depending on the fee basis, negative performance of one or more investments in the fund may reduce the total management fee paid for the relevant period, but not the fee rate. |

| | • | | In our other fund structures, unless outlined differently below, the investment adviser or AIFM (depending on the domicile of the fund) receives a management fee based on a percentage of the fund’s |

| | net asset value over the term or life of the fund. These funds may permit investors to withdraw or redeem their interests periodically, in some cases following the expiration of a specified period of time when capital may not be withdrawn. Decreases in net asset value reduce the total management fee paid for the relevant period, but not the fee rate. |

| | • | | In our CLOs, the investment adviser typically receives a base management fee and a subordinated management fee, which are calculated as a percentage of the CLO’s assets. Although varying from deal to deal, a CLO will typically be wound down within eight to eleven years of being launched. The amount of fees will decrease as the CLO deleverages toward the end of its term. |

| | • | | In our separately managed accounts, the investment adviser generally receives a management fee based on a percentage of each account’s net asset value or invested capital. Such management fees are generally subject to contractual rights the investor has to terminate our management on generally as short as 30 days’ notice. |

| | • | | In our credit-focused registered investment companies and our BDCs, the investment adviser typically receives a management fee based on a percentage of net asset value or total managed assets. Such management fees are generally subject to contractual rights of the company’s board of directors to terminate our management of an account on as short as 30 days’ notice. |

| | • | | For BXMT, the investment adviser receives a management fee based on a percentage of BXMT’s net proceeds received from equity offerings and accumulated “distributable earnings” (which is generally equal to its net income, calculated under GAAP, excluding certain non-cash and other items), subject to certain adjustments. |

For additional information regarding the management fee rates we receive, see “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Critical Accounting Policies — Revenue Recognition — Management and Advisory Fees, Net.”

Our incentive arrangements are composed of (a) contractual incentive fees received from certain investment vehicles upon achieving specified cumulative investment returns (“Incentive Fees”), and (b) a disproportionate allocation of the income generated by investment vehicles otherwise allocable to investors upon achieving certain investment returns (“Performance Allocations”, and, together with Incentive Fees, “Performance Revenues”).

In our carry funds, our Performance Revenues consist of the Performance Allocations to which the general partner or an affiliate thereof is entitled, commonly referred to as carried interest. Our ability to generate and realize carried interest is an important element of our business and has historically accounted for a very significant portion of our income.

Carried interest is typically structured as a net profits interest in the applicable fund. In the case of our carry funds, carried interest is generally calculated on a “realized gain” basis, and each general partner (or affiliate) is generally entitled to an allocation of up to 20% of the net realized income and gains (generally taking into account realized and unrealized or net unrealized losses) generated by such fund. Net realized income or loss is not generally netted between or among funds, and in some cases our carry funds provide for allocations to be made on current income distributions (subject to certain conditions).

For most carry funds, the carried interest is subject to a preferred limited partner return generally ranging from 5% to 8% per year, subject to a

catch-up

allocation to the general partner. Some of our carry funds do not provide for a preferred return, and generally the terms of our carry funds vary in certain respects across our business units and vintages. If, at the end of the life of a carry fund (or earlier with respect to certain of our carry

funds), as a result of diminished performance of later investments in a carry fund’s life, (a) the general partner receives in excess of the relevant carried interest percentage(s) applicable to the fund as applied to the fund’s cumulative net profits over the life of the fund, or (in certain cases) (b) the carry fund has not achieved investment returns that exceed the preferred return threshold (if applicable), then we will be obligated to repay an amount equal to the carried interest that was previously distributed to us that exceeds the amounts to which we were ultimately entitled, up to the amount of carried interest received on an

after-tax

basis. This is known as a “clawback” obligation and is an obligation of any person who received such carried interest, including us and other participants in our carried interest plans.

Although a portion of any dividends paid to our stockholder may include any carried interest received by us, we do not intend to seek fulfillment of any clawback obligation by seeking to have our stockholders return any portion of such dividends attributable to carried interest associated with any clawback obligation. To the extent we are required to fulfill a clawback obligation, however, we may determine to decrease the amount of our dividends to our stockholders. The clawback obligation operates with respect to a given carry fund’s own net investment performance only and carried interest of other funds is not netted for determining this contingent obligation. Moreover, although a clawback obligation is several, the governing agreements of most of our funds provide that to the extent another recipient of carried interest (such as a current or former employee) does not fund his or her respective share of the clawback obligation then due, then we and our employees who participate in such carried interest plans may have to fund additional amounts (generally an additional 50% to 70% beyond our

pro-rata

share of such obligation) although we retain the right to pursue any remedies that we have under such governing agreements against those carried interest recipients who fail to fund their obligations. We have recorded a contingent repayment obligation equal to the amount that would be due on December 31, 2023, if the various carry funds were liquidated at their current carrying value. For additional information concerning the clawback obligations we could face, see “—Item 1A. Risk Factors — Risks Related to Our Business — We may not have sufficient cash to pay back “clawback” obligations if and when they are triggered under the governing agreements with our investors.”

In our structures other than carry funds, our Performance Revenues generally consist of performance-based allocations of a vehicle’s net capital appreciation during a measurement period, typically a year, subject to the achievement of minimum return levels, high water marks, loss carry forwards and/or other hurdle provisions, in accordance with the respective terms set out in each vehicle’s governing agreements. Such allocations are typically realized at the end of the measurement period and, once realized, are typically not subject to clawback or reversal. In particular, our ability to generate and realize these amounts is an important element of our business. Such allocations in certain of our Perpetual Capital strategies contribute a significant and growing portion to our overall revenues.

The following is a general description of the Performance Revenues earned by Blackstone in structures other than carry funds:

| | • | | In our Multi-Asset Investing segment, the investment adviser of certain of our funds of hedge funds, hedge funds, separately managed accounts that invest in hedge funds and certain non-U.S. registered investment companies, is entitled to an incentive fee generally between 0% to 20%, as applicable, of the applicable investment vehicle’s net appreciation, subject to “high water mark” provisions and in some cases a preferred return. |

| | • | | The general partners or similar entities of each of our real estate and credit hedge fund structures receive incentive fees of generally up to 20% of the applicable fund’s net capital appreciation per annum. |

| | • | | The investment adviser of our BDCs receives (a) income incentive fees of 12.5% or 17.5%, as applicable, subject to, in certain cases, certain hurdles, catch-ups and caps, payable quarterly, and (b) capital gains incentive fees (net of realized and unrealized losses) of 12.5% or 17.5%, as applicable, payable annually. |

| | • | | The investment manager of BXMT receives an incentive fee generally equal to 20% of BXMT’s distributable earnings in excess of a 7% per annum return on stockholders’ equity (excluding stock appreciation or depreciation), provided that BXMT’s distributable earnings over the prior three years is greater than zero. |

| | • | | The general partner or special limited partner of each of BREIT, BEPIF and BXPE receives a performance participation allocation of 12.5% of total return, subject to a 5% hurdle amount with a catch-up and recouping any loss carry forward amounts, measured annually and payable quarterly. |

| | • | | The general partners of certain open-ended BPP and BIP funds are entitled to an incentive fee allocation generally between 7% and 12.5% of net profit, subject to a hurdle amount generally of between 5.5% and 7%, a loss recovery amount and a catch-up. Incentive allocations for these funds are generally realized every three years from when a limited partner makes its initial investment, or upon a limited partner’s redemption from the fund. |

Advisory and Transaction Fees

Some of our investment advisers or their affiliates receive customary fees (for example, acquisition, origination and other transaction fees) upon consummation of their funds’ transactions, and may from time to time receive advisory, monitoring and other fees in connection with their activities. For most of the funds where we receive such fees, we are required to reduce the management fees charged to the funds’ investors by 50% to 100% of such limited partner’s share of such fees.

Capital Invested In and Alongside Our Investment Funds

To further align our interests with those of investors in our investment funds, we have invested the firm’s capital and that of our personnel in the investment funds we sponsor and manage. Minimum general partner capital commitments to our investment funds are determined separately with respect to each of our investment funds and, generally, are less than 5% of the limited partner commitments of any particular fund. See “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources” for more information regarding our minimum general partner capital commitments to our funds. We determine whether to make general partner capital commitments to our funds in excess of the minimum required commitments based on, among other things, our anticipated liquidity, working capital and other capital needs. In many cases, we require our senior managing directors and other professionals to fund a portion of the general partner capital commitments to our funds. In other cases, we may from time to time offer to our senior managing directors and employees a part of the funded or unfunded general partner commitments to our investment funds. Our general partner capital commitments are funded with cash and not with carried interest or deferral of management fees.

Investors in many of our funds also receive the opportunity to make additional

“co-investments”

with the investment funds. Our personnel, as well as Blackstone itself and certain Blackstone relationships, also have the opportunity to make investments, in or alongside our funds and other vehicles we manage, in some instances without being subject to management fees, carried interest or incentive fees. In certain cases, limited partner investors may pay additional management fees or carried interest in connection with such

co-investments.

The asset management industry is intensely competitive, and we expect it to remain so. We compete both globally and on a regional, industry and sector basis. We compete on the basis of a number of factors, including investment performance, transaction execution skills, access to capital, access to and retention of qualified personnel, reputation, range of products and services, innovation and price.

We face competition in the pursuit of institutional and individual investors for our investment funds. Although over time many institutional and individual investors have increased the amount of capital they commit to alternative investment funds, such increases may create increased competition with respect to fees charged by our funds. Certain institutional investors have demonstrated a preference to

in-source

their own investment professionals and to make direct investments in alternative assets without the assistance of private equity advisers like us. We compete for investments with such institutional investors and such institutional investors could cease to be our clients. With respect to the private wealth channel and insurance sector, the market for capital is highly competitive, requires significant investment and is highly regulated, which could create competitive challenges for us.

We also face competition in the pursuit of attractive investment opportunities for our funds. Depending on the investment, we face competition primarily from sponsors managing other funds, investment vehicles and other pools of capital, other financial institutions and institutional investors (including sovereign wealth and pension funds), corporate buyers and other parties. Several of these competitors have significant amounts of capital and many of them have investment objectives similar to ours, which may create additional competition for investment opportunities. Some of these competitors may also have a lower cost of capital and access to funding sources or other resources that are not available to us, which may create competitive disadvantages for us with respect to investment opportunities. In addition, some of these competitors may have higher risk tolerances, different risk assessments or lower return thresholds, which could allow them to consider a wider variety of investments and to bid more aggressively than us for investments. Corporate buyers may be able to achieve synergistic cost savings with regard to an investment or be perceived by sellers as otherwise being more desirable bidders, which may provide them with a competitive advantage in bidding for an investment.

In all of our businesses, competition is also intense for the attraction and retention of qualified employees. Our ability to continue to compete effectively in our businesses will depend upon our ability to attract new employees and retain and motivate our existing employees.

For additional information concerning the competitive risks that we face, see “—Item 1A. Risk Factors — Risks Related to Our Business — The asset management business is intensely competitive.”

Environmental, Social and Governance

Our investors have relied on our relentless commitment to excellence for nearly 40 years. Our ESG efforts are anchored in our goal of generating strong returns for investors to fulfil our fiduciary duty. Our integrated team includes dedicated coverage at the firm level and at individual business units. Senior management reports quarterly to our board of directors, which is responsible for reviewing our ESG strategy, including on the basis of periodic reports from management addressing relevant matters and practices.

Our strategy prioritizes (a) reinforcing strong governance, a foundation of resilient companies, (b) accelerating decarbonization by investing in the energy transition and driving value-accretive emissions reduction in our portfolio and (c) building workplaces by expanding talent pools. We have pursued attractive investments in

companies and assets that support the global energy transition. We are also focused on helping select portfolio companies capture cost savings through greenhouse gas emission reduction efforts as part of our Emissions Reduction Program. This program aims to reduce Scope 1 and Scope 2 carbon emissions by 15% on average across certain new investments where we control energy usage during the first three full calendar years of ownership. At a corporate level, we seek to advance corporate sustainability, energy efficiency and environmental performance at out global office locations.

At Blackstone, our people are our most valuable asset. We seek to attract, develop and retain outstanding talent across a wide spectrum of disciplines. We believe building inclusive workplaces positions us and our portfolio companies to access a broad pool of qualified talent, including from historically under-tapped talent pools, and foster inclusive cultures that generate lasting value for our investors. See “—Human Capital Management.”

Blackstone’s employees are integral to our culture of integrity, professionalism, excellence and cooperation. The intellectual capital collectively possessed by our employees is our most important asset. We hire qualified people, train them and encourage them to work together to provide their best thinking to the firm for the benefit of the investors in the funds we manage. As of December 31, 2023, we employed approximately 4,735 people. During 2023, our total number of employees increased by approximately 40.

Our board of directors plays an active role in overseeing our human capital management efforts. To that end, senior management reviews with our board of directors management succession planning and development and other key aspects of our talent management strategy.

We believe a workforce reflecting a breadth of backgrounds and experiences makes us better investors and a better firm. Our diversity, equity and inclusion strategy leverages a people-driven framework based on four key pillars: recruiting, talent development, community and inclusion and accountability. We believe that by focusing on each of these pillars and investing in our people and our culture, we will create an inclusive environment that helps expand our access to the best available talent and drives retention and advancement opportunities for our employees.

To that end, our employee affinity networks, which are open to all employees, serve as a platform for our professionals to expand cultural awareness and connect to other employees, including through speaker series, professional development panels and social events. We also seek to enable ourselves and our portfolio companies to access a broad pool of qualified talent, including through firm programs aimed at introducing talented undergraduate students to financial services and Blackstone and portfolio programs aimed at helping our portfolio companies access historically under-tapped talent pools.

Employee and Community Engagement

Blackstone is committed to ensuring our employees are engaged with their work and with their local communities. Blackstone regularly gathers feedback from our employees via internal and/or external surveys to assess employee engagement and satisfaction and develop targeted solutions. Blackstone also supports its employee affinity networks in their efforts to expand cultural awareness and connection across the firm.

In addition, the Blackstone Charitable Foundation (“BXCF”) was established in 2007 and is committed to supporting Blackstone’s goal of helping foster economic opportunity and career mobility for historically

underrepresented groups. This includes, among other initiatives, its signature Blackstone LaunchPad network, which seeks to close the opportunity gap by equipping college and university students with the entrepreneurial skills they need to build lasting careers, and BX Connects, a global program that provides Blackstone employees with the opportunity to support their local communities through volunteering and giving. BX Connects uses the firm’s scale, talent and resources to make grants, develop nonprofit partnerships and create employee engagement opportunities. Nearly 90% of our employees engaged globally with BXCF’s charitable initiatives in 2023.

Talent Acquisition, Development and Retention

We believe the talent of our employees, coupled with our rigorous investment process, has supported our excellent investment record over many years. We are therefore focused on hiring, training, motivating and retaining talented individuals. Across all our businesses, we face intense competition for qualified personnel.

We seek to attract and retain the brightest minds across a wide spectrum of disciplines and from varied backgrounds and experiences. We believe our reputation, talent development opportunities and compensation make us an attractive employer. We encourage independent thinking and reward initiative while providing training and development opportunities to help our employees grow professionally. In addition, our Respect at Work programs and trainings help maintain an inclusive work environment in which all individuals are treated with respect and dignity. Employee education and training are also critical to maintaining a culture of compliance.

Blackstone offers a wide range of learning and professional development opportunities, both formally and informally, to help employees advance their careers and maximize the value they can add to the global firm. Incoming analyst classes are provided with training that spans their first few years. In addition, our new hires are provided with training and other opportunities to help them thrive in our culture, including through our Culture Program and our Leadership Speaker Series. Blackstone employees are trained or enrolled in compliance training when they start at the firm, and we retrain employees globally at least once annually. Over the course of their careers at Blackstone, employees are offered learning opportunities in a number of areas including leadership and management development and communication skills, among others. We offer a global development curriculum on key capabilities required to succeed at Blackstone, and we partner with external organizations to deliver training programs for our employees. We consistently seek to create visibility and opportunities for talent to take on roles beyond their current positions, and for managers to connect regularly to discuss and match talent with critical roles. These efforts result in cross-pollination of talent that we believe engages our people and generates stronger outcomes for the firm.

As discussed below, we seek to retain and incentivize the performance of our employees through our compensation structure. We also enter into

non-competition

and

non-solicitation

agreements with certain employees. See “Part III. Item 11. Executive Compensation —

Non-Competition

and

Non-Solicitation

Agreements” for a description of the material terms of such agreements.

Compensation, Benefits and Wellness

Our compensation is designed to motivate and retain employees and align their interests with those of the investors in our funds. In particular, incentive compensation for our senior managing directors and employees involves a combination of annual cash bonus payments and performance interests or deferred equity awards, which we believe encourages them to focus on the performance of our investment funds and the overall performance of the firm. The proportion of compensation that is “at risk” generally increases as an employee’s level of responsibility rises. Employees at higher total compensation levels are generally targeted to receive a greater percentage of their total compensation payable in annual cash bonuses, participation in performance

interests and deferred equity awards and a lesser percentage in the form of base salary compared to employees at lower total compensation levels. To further align their interests with those of investors in our funds, we provide employees with the opportunity to make investments in or alongside certain of the funds and other vehicles we manage. We also provide our employees robust health and retirement offerings, as well as a variety of quality of life benefits, including

time-off

options and well-being and family planning resources.

We believe our current compensation and benefit allocations for senior professionals are best in class and are consistent with companies in the alternative asset management industry. Our senior management periodically reviews the effectiveness and competitiveness of our compensation program. Most of our current senior managing directors and other senior personnel have equity interests in our business that entitle such personnel to cash distributions. See “Part III. Item 11. Executive Compensation–Compensation Discussion and Analysis–Overview of Compensation Philosophy and Program” for more information on compensation of our senior managing directors and certain other employees.

We care greatly about the health, safety and wellbeing of our employees. Blackstone also offers comprehensive and competitive benefits to its full-time employees, including primary and secondary caregiver leave, adoption leave, phased back to work, fertility coverage, back up childcare and more. We continually evaluate and enhance our offerings to meet the needs of our employees. For example, we offer additional family planning benefits for U.S. employees such as enhancing infertility benefits to include cryopreservation and primary caregiver leave up to 21 weeks. We offer employee well-being programs, including an online therapy program and access to an education platform with coaching to support working parents and caretakers caring for children who have behavioral problems, autism or developmental disabilities. We also provide access to programs to further assist our employees in managing their lives outside of work, such as group legal services to help with estate planning and surrogacy agreements.

Data Privacy and Security

Blackstone is committed to data privacy. These topics are included in routine training received at least once annually by employees. Data privacy is typically addressed in the Global Head of Compliance’s annual update to our board of directors. Blackstone’s approach to data protection is set out in our Online Privacy Notice and its Investor Data Privacy Notice. Senior management oversees privacy, data protection and information risk management efforts, leading the privacy and data protection function, which conducts privacy impact assessments, implements

initiatives and reconciles global privacy programs with local privacy requirements. Our privacy function also supports the Data Protection Operating Committee, Blackstone’s global privacy compliance steering committee. Please see “—Part I, Item 1C. Cybersecurity” for a discussion of our cybersecurity risk management, strategy and governance.

Regulatory and Compliance Matters

Our businesses, as well as the financial services industry generally, are subject to extensive regulation in the United States and in many of the markets in which we operate.

Many of our businesses are subject to compliance with laws and regulations of U.S. federal and state governments,

non-U.S.

governments, their respective agencies and/or various self-regulatory organizations or exchanges. The SEC and various self-regulatory organizations, state securities regulators and international securities regulators have in recent years increased their regulatory activities, including regulation, examination and enforcement in respect of asset management firms, including Blackstone. Any failure to comply with these regulations could expose us to liability and/or damage our reputation. Our businesses have operated for many years within a legal framework that requires us to monitor and comply with a broad range of legal and regulatory

developments that affect our activities. However, additional legislation, changes in rules promulgated by financial regulatory authorities or self-regulatory organizations or changes in the interpretation or enforcement of existing laws and rules, either in the United States or abroad, may directly affect our mode of operation and profitability.

All of the investment advisers of our investment funds operating in the U.S. are registered as investment advisers with the SEC under the Advisers Act (other investment advisers may be registered in

non-U.S.

jurisdictions). Registered investment advisers are subject to the requirements and regulations of the Advisers Act. Such requirements relate to, among other things, fiduciary duties to advisory clients, maintaining an effective compliance program and code of ethics, investment advisory contracts, solicitation agreements, conflicts of interest, recordkeeping and reporting requirements, disclosure, advertising and custody requirements, political contributions, limitations on agency cross and principal transactions between an adviser and advisory clients, and general anti-fraud prohibitions. Certain investment advisers are also registered with international regulators in connection with their management of products that are locally distributed and/or regulated.

Blackstone Securities Partners L.P. (“BSP”), a subsidiary through which we conduct our capital markets business and certain of our fund marketing and distribution, is registered as a broker-dealer with the SEC and is subject to regulation and oversight by the SEC, is a member of the Financial Industry Regulatory Authority, or “FINRA,” and is registered as a broker-dealer in 50 states, the District of Columbia, the Commonwealth of Puerto Rico and the Virgin Islands. In addition, FINRA, a self-regulatory organization subject to oversight by the SEC, adopts and enforces rules governing the conduct, and examines the activities, of its member firms, including BSP. State securities regulators also have regulatory oversight authority over BSP.

Broker-dealers are subject to regulations that cover all aspects of the securities business, including, among others, the implementation of a supervisory control system over the securities business, advertising and sales practices, conduct of and compensation in connection with public securities offerings, maintenance of adequate net capital, record keeping and the conduct and qualifications of employees. In particular, as a registered broker-dealer and member of FINRA, BSP is subject to the SEC’s uniform net capital rule, Rule

15c3-1.

Rule

15c3-1

specifies the minimum level of net capital a broker-dealer must maintain and also requires that a significant part of a broker-dealer’s assets be kept in relatively liquid form. The SEC and various self-regulatory organizations impose rules that require notification when net capital of a broker-dealer falls below certain predefined criteria, limit the ratio of subordinated debt to equity in the capital structure of a broker-dealer and constrain the ability of a broker-dealer to expand its business under certain circumstances. Additionally, the SEC’s uniform net capital rule imposes certain requirements that may have the effect of prohibiting a broker-dealer from distributing or withdrawing capital and requiring prior notice to the SEC for certain withdrawals of capital.

In addition, certain of the

closed-end

and

open-end

investment companies we manage, advise or

sub-advise

are registered, or regulated as a BDC, under the 1940 Act. The 1940 Act and the rules thereunder govern, among other things, the relationship between us and such investment vehicles and limit such investment vehicles’ ability to enter into certain transactions with us or our affiliates, including other funds managed, advised or

sub-advised

by us.

Pursuant to the U.K. Financial Services and Markets Act 2000, or “FSMA,” certain of our subsidiaries are subject to regulations promulgated and administered by the Financial Conduct Authority (“FCA”). The FSMA and rules promulgated thereunder form the cornerstone of legislation which governs all aspects of our investment business in the United Kingdom, including sales, provision of investment advice, use and safekeeping of client funds and securities, regulatory capital, recordkeeping, approval standards for individuals, anti-money laundering, periodic reporting and settlement procedures. Blackstone Europe LLP (formerly known as Blackstone Group International Partners LLP) (“BELL”) acts as a

sub-advisor

to its Blackstone U.S. affiliates in relation to the investment and

re-investment

of Europe, Middle East and Africa (“EMEA”) based assets of Blackstone Funds,

arranging transactions to be entered into by or on behalf of Blackstone Funds, and providing certain related services. Until December 31, 2020, BGIP had a MiFID II (as defined herein) cross-border passport to provide investment services into the European Economic Area (“EEA”). As of January 1, 2021, as a result of the U.K.’s withdrawal from the European Union, BGIP no longer has a MiFID II passport. Consequently, BELL can only provide investment services in certain EEA jurisdictions where it has obtained a domestic license on a cross-border services basis (currently, Belgium, Denmark, Finland and Italy), or can operate pursuant to an exemption or relief (currently Ireland, Lichtenstein and Norway), although in certain cases with limitations. BELL’s principal place of business is in London, and it has a branch in Abu Dhabi Global Market.

Blackstone Ireland Limited (formerly known as Blackstone / GSO Debt Funds Management Europe Limited) (“BIL”) is authorized and regulated by the Central Bank of Ireland (“CBI”) as an Investment Firm under the (Irish) European Union (Markets in Financial Instruments) Regulations 2017, which largely implements MiFID II in Ireland. BIL’s principal activity is the provision of management and advisory services to certain CLO and

sub-advisory

services to certain affiliates. Blackstone Ireland Fund Management Limited (formerly known as Blackstone / GSO Debt Funds Management Europe II Limited) (“BIFM”) is authorized and regulated by the CBI as an Alternative Investment Fund Manager under the (Irish) European Union (Alternative Investment Fund Managers Regulations) 2013 (“AIFMRs”), which largely implements the EU Alternative Investment Fund Managers Directive (“AIFMD”) in Ireland. BIFM acts as AIFM and provides investment management functions including portfolio management, risk management, administration, marketing and related activities to its alternative investment funds in accordance with AIFMRs and the conditions imposed by the CBI as set out in the CBI’s alternative investment fund rulebook.

Blackstone Europe Fund Management S.à r.l. (“BEFM”) is an authorized Alternative Investment Fund Manager under the Luxembourg Law of 12 July 2013 on alternative investment fund managers (as amended, the “AIFM Law”), which largely implements AIFMD in Luxembourg. BEFM may also provide discretionary portfolio management services, investment advice and reception and transmission of orders in accordance with article 5(4) of the AIFM Law. BEFM provides investment management functions including portfolio management, risk management, administration, marketing and related activities to the assets of its alternative investment funds, in accordance with the AIFM Law and the regulatory provisions imposed by the

Commission de Surveillance du Secteur Financier

in Luxembourg. BEFM may also manage undertakings for collective investment in transferable securities (UCITS). As of January 1, 2021, BEFM promotes Blackstone products and services in European countries where BELL is not otherwise licensed to do so. BEFM has branches in Paris, Milan and Frankfurt which provide marketing services and where distribution and deal sourcing individuals are based.

Certain Blackstone operating entities are licensed and subject to regulation by financial regulatory authorities in Japan, Hong Kong, Australia and Singapore: The Blackstone Group Japan K.K., a financial instruments firm, is registered with Kanto Local Finance Bureau and regulated by the Japan Financial Services Agency; The Blackstone Group (HK) Limited is regulated by the Hong Kong Securities and Futures Commission; The Blackstone Group (Australia) Pty Limited and Blackstone Real Estate Australia Pty Limited each holds an Australian financial services license authorizing it to provide financial services in Australia and is regulated by the Australian Securities and Investments Commission; and Blackstone Singapore Pte. Ltd. is regulated by the Monetary Authority of Singapore.

Rigorous legal and compliance analysis of our businesses and investments is endemic to our culture and risk management. Our Chief Legal Officer and Global Head of Compliance, together with the Chief Compliance Officers of each of our businesses, supervise our compliance personnel, who are responsible for addressing the regulatory and compliance matters that affect our activities. We strive to maintain a culture of compliance through the use of policies and procedures including a code of ethics, electronic compliance systems, testing and monitoring, communication of compliance guidance and employee education and training. Our compliance policies and procedures address regulatory and compliance matters such as the handling of material

non-public

information, personal securities trading, marketing practices, gifts and entertainment, anti-money laundering, anti-bribery and sanctions, valuation of investments on a fund-specific basis, recordkeeping, potential conflicts of interest, the allocation of investment and

co-investment

opportunities, collection of fees and expense allocation.

Our compliance group also monitors the information barriers that we maintain between Blackstone’s businesses. We believe that our various businesses’ access to the intellectual knowledge and contacts and relationships that reside throughout our firm benefits all of our businesses. To maximize that access and related synergies without compromising compliance with our legal and contractual obligations, our compliance group oversees and monitors the communications between groups that are on the private side of our information barrier and groups that are on the public side, as well as between different public side groups. Our compliance group also monitors contractual obligations that may be impacted and potential conflicts that may arise in connection with these inter-group discussions.

In addition, disclosure controls and procedures and internal controls over financial reporting are documented, tested and assessed for design and operating effectiveness in accordance with the U.S. Sarbanes-Oxley Act of 2002. Internal Audit, which independently reports to the audit committee of our board of directors, operates with a global mandate and is responsible for the examination and evaluation of the adequacy and effectiveness of the organization’s governance and risk management processes and internal controls, as well as the quality of performance in carrying out assigned responsibilities to achieve the organization’s stated goals and objectives.

Our enterprise risk management framework is designed to manage

non-investment